Global Anovulation Market

Global Anovulation Market Size, Share, By Cause (Polycystic Ovary Syndrome, Hypothalamic Dysfunction, Premature Ovarian Failure, Hyperprolactinemia, Other) By Treatment Type (Ovulation Induction Therapy, Hormonal Therapy, Assisted Reproductive Technology, Lifestyle & Nutritional Interventions) By End User (Hospitals & Clinics, Fertility Centers, Research & Academic Institutes) and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2025-2035

REPORT COVERAGE

Global

Market Snapshot

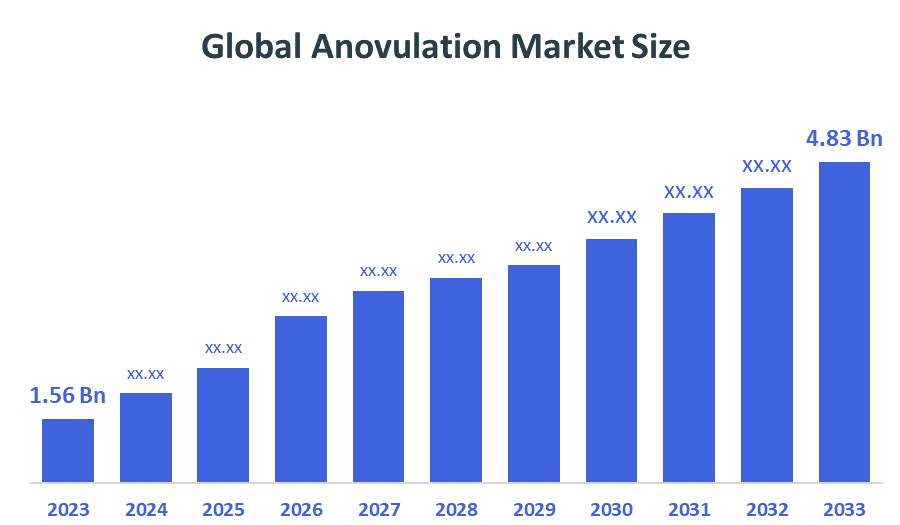

- Market Size (2025): USD 1.56 Billion

- Projected Market Size (2035): USD 4.83 Billion

- Compound Annual Growth Rate (CAGR): 11.96%

- Largest Regional Market: North America

- Fastest Growing Region: Asia Pacific

- 3rd Largest Region: Europe

- Base Year: 2025

- Historical Period: 2021–2024

- Forecast Period: 2025–2035

According to Decision Advisors, the Global Anovulation Market Size is expected to grow from USD 1.56 billion in 2025 to USD 4.83 billion by 2035, at a CAGR of 11.96% during the forecast period 2025-2035. The global anovulation market is driven by increasing government support through subsidized ART programs, rising infertility awareness, adoption of home-based FemTech devices, expanding insurance coverage for fertility treatments, technological innovations in diagnostics and wearables, and preference for safer pharmacological therapies like Letrozole.

Market Overview/ Introduction

The global anovulation market refers to the healthcare sector focused on the diagnosis, management, and treatment of anovulation, a condition where the ovaries fail to release eggs during the menstrual cycle, leading to infertility in women. Anovulation can result from hormonal imbalances, polycystic ovary syndrome (PCOS), thyroid disorders, or age-related ovarian decline. The market encompasses ovulation-inducing drugs, assisted reproductive technologies (ART) including in-vitro fertilization (IVF), ovulation monitoring kits, and emerging digital health platforms that support personalized treatment plans. Increasing awareness of infertility issues, rising prevalence of reproductive disorders, and the growing adoption of advanced fertility therapies are expanding the market’s reach. The scope covers developed regions with high healthcare accessibility, such as North America and Europe, as well as rapidly growing emerging markets in Asia Pacific, driven by large patient populations and improving healthcare infrastructure. Future opportunities in the anovulation market include the integration of AI-guided ovulation induction, personalized hormone therapy, home-based diagnostics, and telemedicine services. Rising demand for premium, clinically validated fertility treatments, coupled with expanding insurance coverage and public health initiatives, is expected to drive long-term growth globally.

- India has become a global hub for affordable fertility care, with several state and central initiatives promoting ART. Goa launched the first comprehensive Free IVF Scheme in a government hospital (2023), while Tamil Nadu and Maharashtra offer subsidized or free ART cycles for low-income families.

- Global policy support is driving market growth as WHO issued its first-ever infertility guidelines (2025), advocating low-cost, high-impact interventions, while countries like France and Denmark have expanded state-funded IVF access, including for single women and same-sex couples.

Notable Insights: -

- North America holds the largest regional market share, approximately 46.2% in the global anovulation market in 2025.

- Asia Pacific is the fastest-growing regional market, accounting for approximately 15.67% the global anovulation market in 2025.

- Europe holds the third-largest regional market share, approximately 5.24% in the global anovulation market.

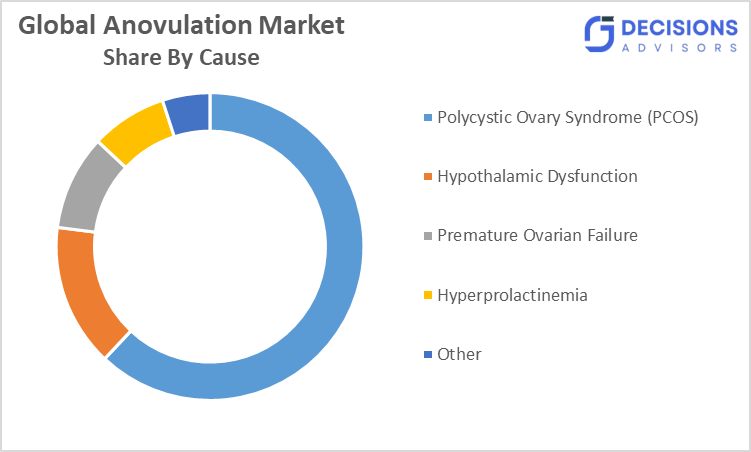

- By cause, the Polycystic Ovary Syndrome (PCOS) segment held a dominant position with approximately 62% market share in 2025.

- By treatment type, the hormonal therapy segment held a dominant position with approximately 50% market share in 2025.

- By end user, the hospitals & clinics segment held a dominant position with approximately 55% market share in 2025.

- The compound annual growth rate of the global anovulation market is 11.96%.

- The market is likely to achieve a valuation of USD 4.83 billion by 2035.

What is role of technology in grooming the market?

Technology plays a critical role in shaping the global anovulation market by improving diagnosis, personalizing treatment, and enhancing patient outcomes. Advanced ovulation monitoring devices, including digital, smartphone-compatible kits, and home-based AI predictive tools like Mira and Inito, allow women to track fertility cycles accurately from home. Wearables such as the Oura Ring and Ava Bracelet further enable precise ovulatory window prediction, boosting adoption of at-home fertility solutions. Artificial intelligence (AI) and machine learning are applied in clinics to customize ovulation induction protocols, optimizing drug dosages and reducing risks like Ovarian Hyperstimulation Syndrome (OHSS). Telemedicine and digital health platforms expand access to consultations, prescriptions, and follow-up care, particularly in remote or underserved regions. Laboratory automation, advanced ART technologies, and genetic biomarker diagnostics enhance procedural efficiency, success rates, and personalized therapy. Overall, technology increases accessibility and accuracy, strengthens patient confidence, and drives adoption of premium and advanced therapies, positioning the Anovulation market for sustained growth and innovation.

How is Recent Developments Helping the Market?

Recent developments such as product innovation, digital health platforms, and expanded access to fertility treatments are supporting the growth of the global anovulation market. In 2025-2026, several new ovulation-inducing drugs and assisted reproductive technologies (ART) were launched, reflecting strong innovation in personalized therapies and hormone protocols. Adoption of premium and advanced ovulation treatments is rising, with a growing number of patients in developed regions opting for high-quality, clinically validated therapies. Additionally, telemedicine and direct-to-consumer digital platforms have improved accessibility, allowing patients to receive consultations, prescriptions, and monitoring remotely. Technological advancements, including AI-guided ovulation induction and home-based diagnostic kits, are also enhancing treatment effectiveness and patient adherence.

Market Drivers

The global anovulation market is expanding due to increasing prevalence of infertility and ovulatory disorders among women of reproductive age. Rising awareness of reproductive health and early diagnosis is encouraging adoption of ovulation-inducing therapies and assisted reproductive technologies (ART). Technological advancements, including AI-guided ovulation induction, home-based ovulation monitoring, and telemedicine platforms, are improving treatment accuracy and accessibility. Growing demand for personalized and premium fertility therapies, supported by better healthcare infrastructure in developed regions and expanding fertility clinics in Asia Pacific, is further fueling market growth. Additionally, government initiatives, public health programs, and insurance coverage in key countries are improving affordability and access, making treatments available to a wider patient population and strengthening long-term market potential.

Restrain

Key restraints on the global anovulation market include high treatment costs, limited insurance coverage in certain regions, and stringent regulatory requirements for drug approvals. Growing patient concerns regarding side effects of hormonal therapies, social stigma associated with infertility, and variable availability of advanced fertility clinics in emerging markets also limit market penetration. Additionally, supply chain challenges for specialized fertility drugs and competition from alternative therapies, such as natural or non-hormonal fertility methods, may hinder growth.

Competitive Analysis:

The report offers the appropriate analysis of the key organizations/companies involved within the global anovulation market, along with a comparative evaluation primarily based on their product of offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes product development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

Top Companies in Global Anovulation Market

- Merck & Co., Inc.

- Ferring Pharmaceuticals Inc.

- Bayer AG

- Pfizer Inc.

- Novartis AG

- Teva Pharmaceutical Industries Ltd.

- Abbott Laboratories

- Sanofi SA

- LIVZON Pharmaceutical Group Inc.

- Zydus Cadila / Zydus Pharma

Government Initiatives

|

Country |

Key Government Initiatives |

|

India |

India is taking steps to integrate infertility care into public health programs (e.g., Ayushman Bharat), while state-level initiatives provide coverage and awareness campaigns for ovulation and assisted reproductive treatments. |

|

US |

The U.S. is promoting federal and state policy reforms to expand access to infertility services, including IVF and ovulation induction treatments, and improve insurance coverage to enhance affordability and equity in reproductive healthcare. |

|

China |

China has introduced medical insurance coverage and regional subsidies for assisted reproductive technologies (ART), including IVF and ovulation treatments, with national policies expanding availability of fertility clinics and improving access for large patient populations. |

Market Segmentation

The Anovulation market share is classified into cause, treatment type, and end user

- The Polycystic Ovary Syndrome (PCOS) segment dominated the market in 2025, and is projected to grow at a substantial CAGR of approximately 62% during the forecast period.

Based on cause, the anovulation market is divided into PCOS, Hypothalamic Dysfunction, Premature Ovarian Failure, Hyperprolactinemia, and Other. Among these, the PCOS segment held approximately 62% share in 2025. Growth is driven by high prevalence, early diagnosis, increasing awareness campaigns, and enhanced screening programs, alongside rising adoption of personalized therapies and supportive care options across developed and emerging markets worldwide.

- The hormonal therapy segment dominated the market in 2025, and is projected to grow at a substantial CAGR of approximately 50% during the forecast period.

Based on treatment type, the anovulation market is divided into ovulation induction therapy, hormonal therapy, assisted reproductive technology (ART), and lifestyle & nutritional interventions. Among these, hormonal therapy held approximately 50% share in 2025. Its growth is driven by widespread clinical adoption, proven efficacy, increasing physician preference, cost-effectiveness for diverse patient groups, and integration into standard care protocols, enabling optimized treatment outcomes globally.

- The hospitals & clinics segment dominated the market in 2025, and is projected to grow at a substantial CAGR of approximately 55% during the forecast period.

Based on end user, the anovulation market is divided into hospitals & clinics, fertility centers, and research & academic institutes. Among these, hospitals & clinics held approximately 55% share in 2025. Growth is due to robust infrastructure, multidisciplinary medical teams, high patient footfall, strong treatment adoption, advanced diagnostic facilities, and widespread access to both systemic and hormonal therapies, particularly in urban and semi-urban regions.

What is the Reason of the Region Dominance?

The dominance of certain regions in the global anovulation market is primarily driven by large patient populations, high awareness of fertility treatments, advanced healthcare infrastructure, and rising disposable incomes. Regions such as North America lead the market due to widespread adoption of assisted reproductive technologies, high per-capita healthcare spending, and strong cultural acceptance of advanced fertility solutions. Rapid urbanization, the growth of specialized fertility clinics, and increasing preference for premium, personalized ovulation therapies further support regional market dominance. Additionally, the availability of advanced reproductive technologies, skilled healthcare professionals, and regulatory support contribute to the sustained leadership of these regions.

Strategies to Implement for Growth of the Market in Non-Leading Regions

Growth in non-leading regions such as Latin America, Middle East, and Africa can be supported through strategic investments, product innovation, and expanded healthcare accessibility. Companies can increase market penetration by introducing affordable, culturally adapted fertility treatments and ovulation therapies that meet regional patient needs. Expanding telehealth, e-consultation services, and digital diagnostics can improve treatment reach in underserved areas. Partnerships with local healthcare providers, hospitals, and fertility clinics can enhance brand visibility and patient awareness. Marketing campaigns focused on education, fertility health awareness, and lifestyle integration can further drive adoption. Investment in local infrastructure, training of healthcare professionals, and accessible treatment models may reduce barriers and strengthen the regional market presence.

Regional Segment Analysis of the Anovulation Market

- North America (U.S., Canada, Mexico)

- Europe (Germany, France, U.K., Italy, Spain, Rest of Europe)

- Asia-Pacific (China, Japan, India, Rest of APAC)

- South America (Brazil and the Rest of South America)

- The Middle East and Africa (UAE, South Africa, Rest of MEA)

Asia Pacific is fastest-growing market in the global anovulation sector, accounting for approximately 15.67% of the total market share. The rapid growth in this region is driven by rising awareness of fertility treatments, expanding healthcare infrastructure, and increasing adoption of assisted reproductive technologies. Large patient populations in countries such as China and India, coupled with growing disposable incomes and urbanization, are fueling demand for premium and accessible ovulation therapies. In particular, China is a key driver of growth, with a rapidly expanding number of fertility clinics and IVF procedures, positioning Asia Pacific as a critical growth hub in the global anovulation market.

North America is anticipated to hold the largest share of the anovulation market over the predicted timeframe, accounts for approximately 46.2% of the total market share. This is driven by advanced healthcare infrastructure, high awareness of fertility treatments, increasing adoption of assisted reproductive technologies, and strong consumer preference for premium and personalized ovulation therapies. The U.S. dominates the regional market with widespread availability of IVF clinics, advanced ovulation induction protocols, and innovative fertility solutions, making it the key contributor to global market growth.

Europe is the third-largest region in the anovulation market. The region accounts for approximately 5.24% of the global market share, supported by a long-standing history of advanced reproductive healthcare and well-established fertility infrastructure in countries such as Germany, France, and Spain. Europe is a major hub for premium and specialized ovulation therapies, with strong demand for high-value treatments, personalized protocols, and advanced fertility solutions, which drive higher revenue even if patient volume growth is moderate.

Future Market Trends in Global Anovulation Market: -

1. AI-Driven Personalized Ovulation Treatment

Artificial intelligence and machine learning are increasingly being used to tailor ovulation induction protocols, optimizing drug dosages and treatment timing based on individual biomarkers. Adoption of AI-driven treatments is expected to improve success rates and reduce complications like OHSS.

2. Expansion of Digital and At-Home Ovulation Diagnostics

Digital ovulation test kits and smartphone-compatible devices are gaining traction, allowing patients to self-monitor ovulation accurately at home. Early detection and increased patient engagement are driving widespread adoption of these innovative diagnostic solutions.

3. Shift Toward Non-Hormonal and Natural Fertility Methods

Rising “hormone hesitancy” among patients is fueling demand for hormone-free fertility awareness and natural ovulation regulation methods. This trend is influencing patient preference, encouraging healthcare providers to offer alternative, less invasive ovulation management options.

Recent Development

- In March 2026, the Medically Assisted Reproduction (MAR) Drugs market was projected to reach $4.48 billion, driven by rising global infertility rates and adoption of ovulation stimulation drugs, reflecting expanding treatment access and adoption trends in the global anovulation market.

- In January 2026, TrumpRx.gov launched a direct-purchasing platform, enabling direct-to-consumer access for IVF and ovulation therapies, supporting affordability and wider adoption within the global anovulation market.

- In October 2025, EMD Serono signed an agreement with the U.S. Government to expand access to IVF therapies, including Gonal-f and Ovidrel, offering up to an 84% discount for eligible patients, strengthening accessibility initiatives in the global anovulation market.

- In May 2025, ASKA Pharmaceutical received authorization in Japan for Slinda 28, a progestogen-only oral contraceptive used for hormonal regulation in ovulatory disorders, enhancing treatment options and therapeutic innovation in the global anovulation market.

- In January 2025, Mantra Pharma launched M-METFORMIN to manage blood sugar in PCOS patients and help restore regular ovulation, highlighting pharmacological advances and targeted therapy adoption within the global anovulation market.

Market Segment

This study forecasts revenue at global, regional, and country levels from 2020 to 2035. Decision Advisor has segmented the global anovulation market based on the below-mentioned segments:

Global Anovulation Market, By Cause

- Polycystic Ovary Syndrome (PCOS)

- Hypothalamic Dysfunction

- Premature Ovarian Failure

- Hyperprolactinemia

- Other

Global Anovulation Market, By Treatment Type

- Ovulation Induction Therapy

- Hormonal Therapy

- Assisted Reproductive Technology (ART)

- Lifestyle & Nutritional Interventions

Global Anovulation Market, By End User

- Hospitals & Clinics

- Fertility Centers

- Research & Academic Institutes

Global Anovulation Market, By Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa

Frequently Asked Questions (FAQ)

Q. How could regional cultural attitudes influence the adoption of anovulation treatments?

A. Cultural beliefs around fertility and family planning can affect patient willingness to seek treatment, creating opportunities for awareness campaigns and culturally sensitive healthcare solutions in different regions.

Q. What role could insurance innovation play in expanding fertility treatment access?

A. Customized insurance products, fertility-focused plans, or outcome-based coverage can make ovulation therapies more affordable, increasing uptake in regions where cost is a barrier.

Q. How might partnerships between technology companies and clinics impact the market?

A: Collaborations can accelerate deployment of digital diagnostics, AI tools, and wearable devices, improving patient engagement and treatment personalization without requiring new regulatory frameworks.

Q. How could environmental or lifestyle risk factors shape future demand for anovulation solutions?

A. Rising urban stress, pollution, and sedentary lifestyles may increase ovulatory disorders, driving demand for early diagnostics, preventive care,

Check Licence

Choose the plan that fits you best: Single User, Multi-User, or Enterprise solutions tailored for your needs.

We Have You Covered

- 24/7 Analyst Support

- Clients Across the Globe

- Tailored Insights

- Technology Tracking

- Competitive Intelligence

- Custom Research

- Syndicated Market Studies

- Market Overview

- Market Segmentation

- Growth Drivers

- Market Opportunities

- Regulatory Insights

- Innovation & Sustainability

Report Details

| Scope | Global |

| Pages | 245 |

| Delivery | PDF & Excel via Email |

| Language | English |

| Release | Mar 2026 |

| Access | Download from this page |