Global Artificial Lung Market

Global Artificial Lung Market Size, Share, and COVID-19 Impact Analysis, By Product Type (Extracorporeal Membrane Oxygenation (ECMO) Systems, Paracorporeal Artificial Lungs, Intracorporeal Artificial Lungs, Membrane Oxygenators, and Portable Artificial Lungs), By Application (Bridge-to-Transplantation, Bridge-to-Recovery, ECMO-assisted Ventilation, Pulmonary Rehabilitation, and Long-term Support for Chronic Lung Diseases), By Distribution Channel (Hospital-based Procurement, Direct Tenders and Contracts, Group Purchasing Organizations (GPOs), Online Procurement Platforms, Third-party Distributors), By End-User (Tertiary Care Hospitals, Transplant Centers, Cardiac and Pulmonary ICUs, Research Institutions and Clinical Trial Sites, and Specialty Respiratory Clinics), and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2025-2035

REPORT COVERAGE

Global

Global Artificial Lung Market Size Insights Forecasts to 2035

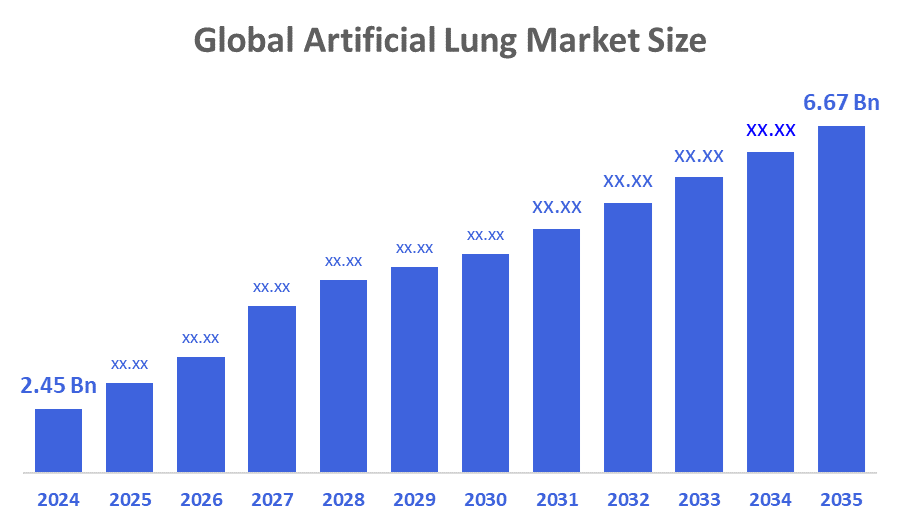

- The Global Artificial Lung Market Size Was Estimated at USD 2.45 Billion in 2024

- The Market Size is Expected to Grow at a CAGR of around 9.53 % from 2025 to 2035

- The Worldwide Artificial Lung Market Size is Expected to Reach USD 6.67 Billion by 2035

- North America is expected to grow the fastest during the forecast period.

According to a research report published by Decisions Advisors and Consulting, The Global Artificial Lung Market Size Was Worth Around USD 2.45 Billion In 2024 And Is Predicted To Grow To Around USD 6.67 Billion By 2035 With A Compound Annual Growth Rate (CAGR) Of 9.53 % From 2025 To 2035. The market is expanding due to the increasing prevalence of chronic respiratory conditions, the growing need for sophisticated respiratory support systems, continuous improvements in extracorporeal life support technology, and the transformation of critical respiratory care delivery.

Market Overview

Artificial lungs play an essential role in medical treatment for ARDS and COPD patients who need lung transplant procedures. The demand for these devices, which medical facilities use in ICUs, surgical centers and transplant programs, has increased because healthcare expenditures have risen, and people have become more aware of organ support technologies and their application of ECMO for critical care treatment after the COVID-19 pandemic. The development of membrane oxygenators together with AI-driven monitoring systems and biocompatible materials you research to create bioartificial lungs and regenerative scaffolds will boost your safety and efficiency operations. The artificial lung market undergoes a strategic transformation because medtech companies need to develop portable autonomous systems that use AI technology for respiratory medical devices. The shift creates new clinical standards that show that defence organisations and critical care healthcare technology developers need portable medical systems that operate in extreme environments. As healthcare and defence sectors converge around shared goals of resilience, portability, and autonomy, artificial lung manufacturers who embrace this direction are well-positioned for long-term growth.

According to estimates from the World Health Organisation (WHO), chronic respiratory conditions, and chronic obstructive lung disease in particular, cause 3.9 million deaths every year. More than 80% of tobacco users worldwide reside in low- and middle-income nations (LMICs), making tobacco a major risk factor.

The federal government awarded Vanderbilt University Medical Centre a share of $8.7 million to develop an artificial lung system that patients with terminal lung illness can use at home. The device, designed for patients who might not be able to wait long enough for a lung transplant or who are not eligible for one, will be developed and tested with funding from the Department of Defence's Congressionally Directed Medical Research Program (CDMRP) award.

Draper advanced artificial lung technology with a $4.9 million U.S. Army grant, earning the prestigious ASAIO Award. The innovation aims to deliver portable, efficient respiratory support for military and civilian patients, offering a potential bridge to transplant or recovery in severe lung failure cases.

Report Coverage

This research report categorizes the artificial lung market based on various segments and regions, forecasts revenue growth, and analyzes trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the artificial lung market. Recent market developments and competitive strategies, such as expansion, product launch, development, partnership, merger, and acquisition, have been included to draw the competitive landscape in the market. The report strategically identifies and profiles the key market players and analyzes their core competencies in each sub-segment of the artificial lung market.

Driving Factors

The artificial lung market is currently undergoing a major transformation because of technological progress and rising public awareness about respiratory illnesses. The development of biocompatible materials, together with the development of smaller devices, now enables artificial lungs to work better while becoming more user-friendly. The healthcare industry requires effective treatments for patients who suffer from severe lung diseases, which will result in improved patient outcomes and market expansion. The combination of artificial intelligence with respiratory health monitoring and management systems will provide extra assistance, which will enable therapists to create customised treatment plans. Artificial lung device demand will increase as healthcare systems worldwide face these challenges. The market will undergo significant changes as regulatory bodies develop safety and efficacy standards, which will impact how products are introduced to the market. The artificial lung market is poised for expansion as various stakeholders collaborate to meet the needs of patients and healthcare professionals.

ALung Technologies, Inc. announced the commercial development of its next-generation artificial lung, marking a significant step forward in respiratory care innovation. Often described as “respiratory dialysis”, the device removes carbon dioxide and delivers oxygen directly to the blood, similar to how kidney dialysis works for renal failure.

Restraining Factors

Market expansion is hampered by the high expense and technical difficulty of artificial lung systems such as extracorporeal membrane oxygenation (ECMO). Their use is restricted in lower-resource hospitals and rural healthcare settings due to the need for specialised infrastructure, ongoing monitoring, and skilled staff. Artificial lungs require significant maintenance and consumable expenditures, as well as a high staffing level, including critical care teams and perfusionists.

Market Segmentation

The artificial lung market share is classified into product type, application, distribution channel, and end user.

- The extracorporeal membrane oxygenation (ECMO) systems segment accounted for the largest market share in 2024 and is anticipated to grow at a substantial CAGR during the forecast period.

Based on the product type, the artificial lung market is divided into extracorporeal membrane oxygenation (ECMO) systems, paracorporeal artificial lungs, intracorporeal artificial lungs, membrane oxygenators, and portable artificial lungs. Among these, the extracorporeal membrane oxygenation (ECMO) systems segment accounted for the largest market share in 2024 and is anticipated to grow at a substantial CAGR during the forecast period. This is because they are effective in helping patients who are in critical condition and have significant respiratory or cardiopulmonary failure. By externally removing carbon dioxide and oxygenating blood, ECMO systems temporarily replace the lungs' gas exchange function. Their modular architecture, which includes control consoles, oxygenators, and pumps, allows for flexibility in meeting various clinical requirements.

For instance, the first meeting of the consortium promoting the innovative liquid-based ECMO system brought together leading researchers and clinicians to advance next-generation respiratory support. The consortium set collaborative priorities for developing safer, more efficient extracorporeal oxygenation, aiming to transform treatment for patients with severe lung failure and accelerate pathways toward clinical trials.

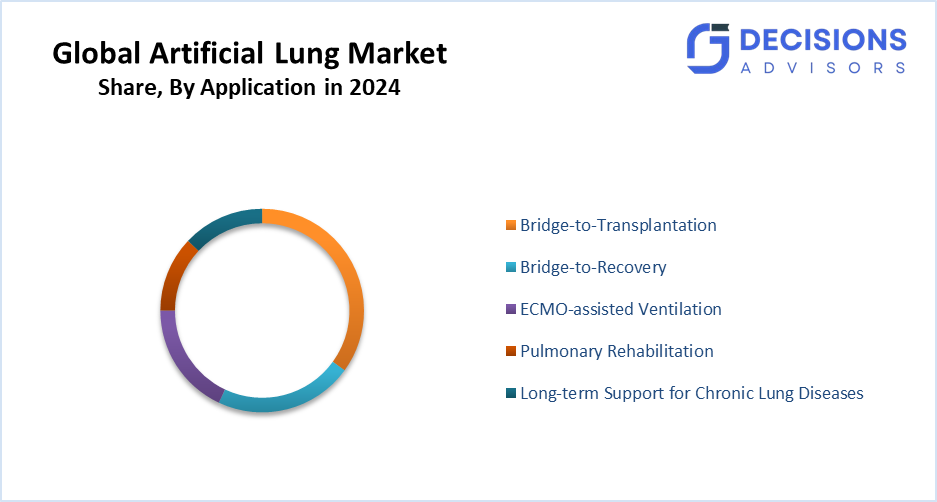

- The bridge-to-transplantation segment accounted for the highest market share in 2024 and is anticipated to grow at a notable CAGR over the forecast period.

Based on the application, the artificial lung market is divided into bridge-to-transplantation, bridge-to-recovery, ECMO-assisted ventilation, pulmonary rehabilitation, and long-term support for chronic lung diseases. Among these, the bridge-to-transplantation segment accounted for the highest market share in 2024 and is anticipated to grow at a notable CAGR over the forecast period. These systems give patients critical support while they wait for donor lung availability. Bridge-to-transplantation continues to be the most common application. Their application greatly improves the quality of life and survival rates during the crucial pre-transplant stage. Devices with low thrombogenic potential, long-duration support capabilities, and simple integration with extracorporeal life support (ECLS) protocols are given priority by hospitals.

- The hospital-based procurement segment accounted for the highest market revenue in 2024 and is projected to grow at a remarkable CAGR over the forecast period.

Based on the distribution channel, the artificial lung market is divided into hospital-based procurement, direct tenders and contracts, and group purchasing organisations (GPOs). Among these, the hospital-based procurement segment accounted for the highest market revenue in 2024 and is projected to grow at a remarkable CAGR over the forecast period. This is mainly because these gadgets are extremely specialised and need a procedural infrastructure. These deals usually take place through negotiated contracts, direct supply agreements, or bids organised by the procurement and biomedical engineering departments of transplant centres and tertiary care institutions.

- The tertiary care hospitals segment accounted for the highest market revenue in 2024 and is anticipated to grow at a significant CAGR during the forecast period.

Based on the end user, the artificial lung market is divided into tertiary care hospitals, transplant centres, cardiac and pulmonary ICUs, research institutions, clinical trial sites, and speciality respiratory clinics. Among these, the tertiary care hospitals segment accounted for the highest market revenue in 2024 and is anticipated to grow at a significant CAGR during the forecast period. The main end users of artificial lungs are tertiary care hospitals and transplant centres because of their sophisticated infrastructure and interdisciplinary teams needed to manage patients on extended extracorporeal support. These facilities have specialised cardiac and pulmonary intensive care units that can carry out risky operations, including pre-transplant stabilisation and ECMO-assisted ventilation.

For instance, the University of Maryland Medical Centre (UMMC) has become the first hospital in the world to use the Abiomed Breathe OXY-1 System for a patient. The OXY-1 System is a compact, portable artificial lung designed to provide extracorporeal respiratory support. UMMC’s pioneering use marks the system’s first-ever clinical application, setting a precedent for future patient care.

Regional Segment Analysis of the Artificial Lung Market

- North America (U.S., Canada, Mexico)

- Europe (Germany, France, U.K., Italy, Spain, Rest of Europe)

- Asia-Pacific (China, Japan, India, Rest of APAC)

- South America (Brazil and the Rest of South America)

- The Middle East and Africa (UAE, South Africa, Rest of MEA)

Asia Pacific is anticipated to hold the largest share of the artificial lung market over the predicted timeframe.

Asia Pacific is anticipated to hold the largest share of the artificial lung market over the predicted timeframe. The region experiences growth because its healthcare spending increases while more people develop chronic respiratory diseases and medical technology continues to progress. Japan and China lead the way because their governments provide public health benefits through healthcare infrastructure development and access to cutting-edge medical solutions. Market expansion results from increased public knowledge about organ donation and transplantation procedures. Japan leads the region through its companies, which develop artificial lung technology with Terumo Corporation, making important advancements. China is becoming a major industrial power because it prioritises domestic production while decreasing its need to import goods. The market situation displays established companies and new enterprises that both work to develop better solutions for treating patients.

Korean researchers achieved a breakthrough in respiratory disease research by developing a micro-structured artificial lung model using 3D bioprinting technology. The intricacy of the human lung is frequently not replicated by conventional research techniques, which results in ineffective drug development. Korean researchers are opening the door to quicker, safer, and more efficient treatments for respiratory conditions by developing a bioprinted lung that can verify virus infection and reproduction.

North America is expected to grow at a rapid CAGR in the artificial lung market during the forecast period. The region possesses both advanced healthcare systems and substantial research and development funding, together with increasing cases of respiratory illnesses. The FDA and other regulatory agencies provide approval support, which helps new products enter the market while driving technological progress. The rising need for organ replacement treatments acts as a market expansion driver. The United States controls the North American market, with Medtronic and Abbott Laboratories serving as its main industry competitors. The industry environment features active competition through ongoing technological advances and new business alliances that top companies create. Canada participates in the market by developing ways to increase healthcare availability while achieving better results for patients. The market environment remains active because established companies and new startups create competition with their operations.

Researchers at the University of Pittsburgh’s McGowan Institute for Regenerative Medicine are developing a wearable artificial lung thanks to a $3.4 million NIH grant. This project represents a step toward making artificial lungs not just life-saving, but also patient-friendly and wearable—a leap from bulky, stationary machines to something closer to a true biomedical prosthetic.

Competitive Analysis:

The report offers the appropriate analysis of the key organizations/companies involved within the artificial lung market, along with a comparative evaluation primarily based on their product offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes product development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

List of Key Companies

- Abbott Laboratories

- Abiomed (Johnson and Johnson MedTech)

- ALung Technologies, Inc.

- Braile Biomédica

- Getinge AB

- Hemovent GmbH

- LivaNova PLC

- MC3 Cardiopulmonary

- Medtronic plc

- MicroPort Scientific Corporation

- Nipro Corporation

- Novalung GmbH (a Xenios company)

- Xenios AG (Fresenius Medical Care)

- Others

Key Target Audience

- Market Players

- Investors

- End-users

- Government Authorities

- Consulting and Research Firm

- Venture capitalists

- Value-Added Resellers (VARs)

Recent Development

- In January 2026, Northwestern Medicine surgeons achieved a remarkable milestone by developing a total artificial lung (TAL) system that kept a patient alive for 48 hours without lungs, enabling a successful double-lung transplant. The patient received a double-lung transplant and has since recovered well, with fully functioning lungs.

- In December 2024, Carnegie Mellon University (CMU) researchers played a central role in a DARPA-funded project to advance artificial lung technology for military and emergency applications. DARPA awarded $18 million to a multi-institutional team that includes CMU’s Keith Cook (Biomedical Engineering).

Market Segment

This study forecasts revenue at global, regional, and country levels from 2020 to 2035. Decisions Advisors has segmented the artificial lung market based on the below-mentioned segments:

Global Artificial Lung Market, By Product Type

- Extracorporeal Membrane Oxygenation (ECMO) Systems

- Paracorporeal Artificial Lungs

- Intracorporeal Artificial Lungs

- Membrane Oxygenators

- Portable Artificial Lungs

Global Artificial Lung Market, By Application

- Bridge-to-Transplantation

- Bridge-to-Recovery

- ECMO-assisted Ventilation

- Pulmonary Rehabilitation

- Long-term Support for Chronic Lung Diseases

Global Artificial Lung Market, By Distribution Channel

- Hospital-based Procurement

- Direct Tenders and Contracts

- Group Purchasing Organisations (GPOs)

Global Artificial Lung Market, By End User

- Tertiary Care Hospitals

- Transplant Centres

- Cardiac and Pulmonary ICUs

- Research Institutions and Clinical Trial Sites

- Speciality Respiratory Clinics

Global Artificial Lung Market, By Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa

Frequently Asked Questions (FAQ)

1. How does reimbursement policy impact the adoption of artificial lung systems globally?

Reimbursement frameworks significantly influence market penetration, particularly for high-cost systems such as ECMO and portable artificial lungs. In developed economies like the United States, favourable insurance coverage and Medicare support improve hospital adoption rates. However, limited reimbursement structures in emerging economies can slow adoption despite rising clinical need.

2. What role does defence-sector funding play in artificial lung innovation?

Defence agencies are increasingly investing in portable and autonomous artificial lung systems for battlefield and emergency use. For example, funding initiatives supported by the Defence Advanced Research Projects Agency are accelerating the development of compact, wearable respiratory support systems. These innovations often transition into civilian healthcare markets.

3. How are wearable artificial lungs expected to reshape long-term respiratory care?

Wearable artificial lung systems aim to reduce ICU dependency by enabling patient mobility and at-home support. Institutions like the University of Pittsburgh are actively researching wearable platforms that could improve the quality of life for chronic lung disease patients and reduce hospitalisation costs.

4. What are the regulatory challenges associated with artificial lung device approvals?

Artificial lung devices must meet stringent safety, biocompatibility, and performance standards before approval. Regulatory authorities such as the U.S. Food and Drug Administration require extensive clinical trials, particularly for long-term implantable or intracorporeal systems, which can lengthen commercialisation timelines.

5. How is artificial intelligence (AI) enhancing artificial lung system performance?

AI-driven monitoring systems are being integrated to optimise oxygenation levels, detect early clot formation, and personalise respiratory parameters. Companies like Medtronic plc are exploring digital health integrations that enable real-time analytics and predictive maintenance for extracorporeal support devices.

6. What is the competitive differentiation strategy among artificial lung manufacturers?

Leading companies are differentiating themselves through portability, reduced thrombogenic risk, longer support duration, and integration with extracorporeal life support platforms. Firms such as Getinge AB focus on modular ECMO platforms, while emerging players prioritise compact and wearable solutions.

7. How does the organ transplant shortage influence artificial lung market growth?

The global shortage of donor lungs increases reliance on artificial lungs as bridge-to-transplant or long-term alternatives. Countries with advanced transplant programs, including Japan, are investing in artificial organ technologies to address donor scarcity and extend patient survival during waiting periods.

Check Licence

Choose the plan that fits you best: Single User, Multi-User, or Enterprise solutions tailored for your needs.

We Have You Covered

- 24/7 Analyst Support

- Clients Across the Globe

- Tailored Insights

- Technology Tracking

- Competitive Intelligence

- Custom Research

- Syndicated Market Studies

- Market Overview

- Market Segmentation

- Growth Drivers

- Market Opportunities

- Regulatory Insights

- Innovation & Sustainability

Report Details

| Scope | Global |

| Pages | 250 |

| Delivery | PDF & Excel via Email |

| Language | English |

| Release | Feb 2026 |

| Access | Download from this page |