Global Atherosclerosis Market

Global Atherosclerosis Market Size, Share, By Stages (Endothelial Damage and Immune Response, Fatty Streak, Plaque Growth, and Plaque Rupture), By Diagnosis (Ankle-brachial Index, Doppler Ultrasound, Echocardiogram, Electrocardiogram, Blood Tests, and Others), By End-User (Hospitals, Specialty Clinics, Homecare, and Others), and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2025 ? 2035

REPORT COVERAGE

Global

Market Snapshot

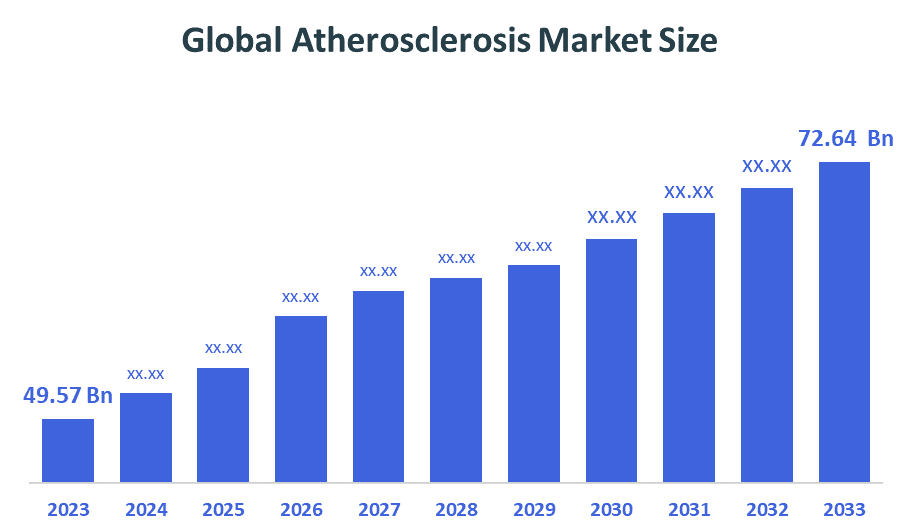

- Market Size (2025): USD 49.57Billion

- Projected Market Size (2035): USD 72.64Billion

- Compound Annual Growth Rate (CAGR): 3.9%

- Largest Regional Market: North America

- Fastest Growing Region: Asia Pacific

- 2nd Largest Region: Europe

- Base Year: 2025

- Historical Period: 2021–2024

- Forecast Period: 2025–2035

According to Decision Advisors, the Global Atherosclerosis Market Size is expected to grow from USD 49.57billion in 2025 to USD 72.64 billion by 2035, at a CAGR of 3.9% during the forecast period 2025-2035. The global atherosclerosis market is projected to grow significantly over the next decade, as the causative factors against the increasing number of damage or injury occurrences to the endothelium include high blood pressure, smoking, high levels of cholesterol, and inflammation.

Market Overview/ Introduction

Atherosclerosis represents a persistent cardiovascular disorder that results in arterial plaque accumulation through the deposition of fat, cholesterol, calcium and additional materials. The global atherosclerosis market is experiencing steady growth due to increasing cardiovascular disease burden. The occurrence of cardiovascular diseases is increasing because people develop obesity and diabetes through their lifestyle and smoking habits. The procedure for atherosclerosis diagnosis requires medical professionals to evaluate the patient's medical history, conduct a physical examination and perform different diagnostic assessments. The tests include multiple blood and urine assessments, with electrocardiogram (ECG, EKG), exercise stress tests, heart imaging assessments and Doppler ultrasound tests.

In July 2025, Novartis announced that the US Food and Drug Administration (FDA) had approved a label update for Leqvio (inclisiran), which lets doctors use the drug as the main treatment together with dietary changes and exercise to help patients with hypercholesterolemia reduce their low-density lipoprotein cholesterol (LDL-C) levels. The FDA requested the label update because they wanted to see more evidence about how PCSK9-targeting therapies help lower LDL-C levels, which exists because of the increasing number of elderly people who have difficulty metabolizing lipids and develop plaque.

- LODOCO reduces cardiac event risk in adult patients with established atherosclerotic cardiovascular disease (ASCVD) by an additional 31% on top of standard of care.

- Amgen's Repatha cuts the risk of first major adverse cardiovascular events by 25% in the landmark Phase 3 Vesalius-CV Trial in November 2025.

- In January 2025, Cyclarity Therapeutics announced the launch of a Phase 1 human clinical trial for a drug that aims to remove the arterial plaques that lead to heart attacks and strokes.

Notable Insights: -

- North America holds the largest regional market share, approximately 45% in the global Allergic Rhino Conjunctivitis market.

- Asia Pacific is the fastest-growing region in the global Atherosclerosis market.

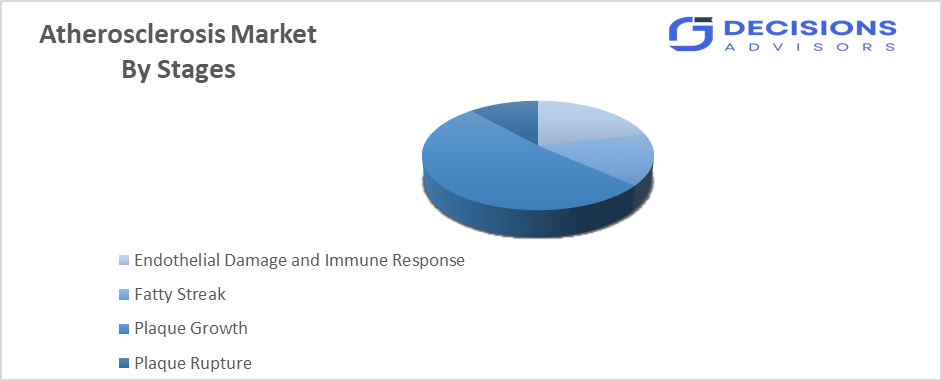

- By stages, the plaque growth segment held a dominant position of over 38% in terms of market share in 2025.

- By diagnosis, the electrocardiogram segment is the dominating one, accounting for over 70% of the global market share in 2025.

- The compound annual growth rate of the global atherosclerosis market is 3.9%.

- The market is likely to achieve a valuation of USD 72.64 billion by 2035.

What is the role of technology in grooming the market?

Technology plays a transformative role in shaping the global atherosclerosis market by the process to enhance diagnostic accuracy and treatment methods with better disease control. The combination of artificial intelligence (AI) and medical imaging, with telemedicine systems, provides healthcare professionals with tools that enable them to identify medical conditions at an early stage while delivering customized treatment solutions that improve patient results and create greater market needs. Non-invasive imaging together with digital health platforms enables healthcare providers to monitor patients continuously while delivering preventive medical services, which decrease the need for hospital admissions. The World Health Organization (WHO) estimates that cardiovascular diseases lead to 17.9 million deaths each year which represents 31% of all global deaths, and atherosclerosis stands as a major cause of these deaths according to government-supported data. The atherosclerosis market grew through technological innovation, which raised its value from USD 48.9 billion in 2026 to USD 63.9 billion by 2036. The digital health services market reached a 37.9% share of the market in 2024 which shows that more people are now using these services. Technology drives market development through its ability to create new products while making them more accessible and expanding businesses throughout international markets.

Market Drivers

The global atherosclerosis market is driven by the increasing number of cardiovascular diseases and the ongoing development of new medical treatments are the main factors behind this trend. The rise of lifestyle diseases, which include obesity, diabetes and hypertension, with the effects of aging and inactive behaviour patterns drive this trend. More than half of all cardiovascular diseases, which account for 48% of cases, result from arterial plaque buildup. This condition creates an urgent necessity for both medical treatment and early disease identification. The market for the product continues to expand because of improved screening methods and increased public knowledge about the product. The development of new products acts as a significant driving force for business expansion. The introduction of next-generation drugs, with biologics and RNA-based therapies, will create new treatment methods that will lead to market growth in the future.

Pharmaceutical companies are launching advanced therapies such as Olpasiran, Obicetrapib, and Pelacarsen, targeting lipid reduction and cardiovascular risk

Restrain

The main restraints on the global atherosclerosis market include healthcare costs deteriorate treatment access because of high expenses, which particularly affect PCSK9 inhibitors and gene therapies. The market experiences pricing pressure because of low-cost generic statins, which pharmaceutical companies widely distribute. The market experiences slow growth because of three major factors, which include limited awareness in developing regions, strict regulatory requirements and the long-term drug use side effects.

Competitive Analysis:

The report offers the appropriate analysis of the key organizations/companies involved within the atherosclerosis market, along with a comparative evaluation primarily based on their product of offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes product development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

Top Companies in Global Atherosclerosis Market

- Pfizer Inc.

- AstraZeneca plc

- Novartis AG

- Merck & Co., Inc.

- Bristol-Myers Squibb Company

- Sanofi S.A.

- Johnson & Johnson

- Amgen Inc.

- Bayer AG

- Regeneron Pharmaceuticals, Inc.

Government Initiatives

|

Country |

Key Government Initiatives |

|

Europe |

In May 2025, LIB Therapeutics Inc. (LIB), a privately-held, late-stage biopharmaceutical company advancing Lerodalcibep (LeroChol), a novel, monthly, small-dose third-generation PCSK9 inhibitor |

|

UK |

National Heart, Lung, and Blood Institute (NHLBI) funds large-scale research on cholesterol and heart disease. Million Hearts Initiative aims to prevent 1 million cardiovascular events (2017–2027). Decline in CVD mortality from 300 to 176 deaths per 100,000 |

|

China |

National cardiovascular prevention programs and screening initiatives. China has one of the highest global burdens with 32.8 million YLLs from ischemic heart disease. Stroke accounts for 40% of deaths |

|

India |

National Programme for Prevention & Control of Cancer, Diabetes, CVD and Stroke (NPCDCS). Integrated Disease Surveillance Programme (IDSP) covers 90%+ districts. CVD causes 25% of total deaths |

Market Segmentation

The atherosclerosis market share is classified into stages, diagnosis, and end user.

- The plaque growth segment dominated the market in 2025, and is projected to grow at a substantial CAGR of approximately 38% during the forecast period.

Based on the stages, the atherosclerosis market is divided into endothelial damage and immune response, fatty streak, plaque growth, and plaque rupture. Among these, the plaque growth segment dominated the market in 2025 and is projected to grow at a substantial CAGR of approximately 38% during the forecast period. The growth of the segment is driven by the fact that most medical conditions receive their diagnoses and corresponding treatments during the stage when patients first develop symptoms, and doctors can begin their medical interventions leads to increased requirements for pharmaceutical products and patient tracking systems and extended medical treatments of chronic illnesses.

- The electrocardiogram segment accounted for the largest share in 2025, and is anticipated to grow at a significant CAGR of approximately 70% during the forecast period.

Based on the diagnosis, the atherosclerosis market is divided into ankle-brachial index, doppler ultrasound, echocardiogram, electrocardiogram, blood tests, and others. Among these, the electrocardiogram segment accounted for the largest share in 2025 and is anticipated to grow at a significant CAGR of approximately 70% during the forecast period. The company controls most of its market share because it offers affordable products that customers can easily access and receive immediate results. Hospitals and primary care facilities use ECG as their standard testing method, which helps them detect cardiovascular risks in more than a million patients each year, thereby making the technology widely used across the world.

- The blood test segment dominated the market in 2025, and is projected to grow at a substantial CAGR of approximately 50% during the forecast period.

Based on the end user, the atherosclerosis market is divided into hospitals, specialty clinics, homecare, and others. Among these, the blood test segment dominated the market in 2025 and is projected to grow at a substantial CAGR of approximately 50% during the forecast period. This dominance is the advanced diagnostic facilities together with the available interventional procedures, which include angioplasty and stenting, with the treatment methods for severe cardiovascular cases, all contribute to this hospital's capability to handle its third highest patient volume.

Regional Segment Analysis of the Atherosclerosis Market

- North America (U.S., Canada, Mexico)

- Europe (Germany, France, U.K., Italy, Spain, Rest of Europe)

- Asia-Pacific (China, Japan, India, Rest of APAC)

- South America (Brazil and the Rest of South America)

- The Middle East and Africa (UAE, South Africa, Rest of MEA)

North America is anticipated to hold the largest share of the Atherosclerosis market over the predicted timeframe.

North America is anticipated to hold the largest share of the atherosclerosis market over the predicted timeframe. This market is accounting about approximately 45% of the total market share. The largest region in the global atherosclerosis market is North America, driven by the region's advantages from its advanced healthcare systems and its high rates of heart disease and substantial research and development funding. The market expansion receives a boost from regulatory backing, which agencies like the FDA provide because they expedite approval processes for new medical treatments. The United States serves as the main market contributor with Amgen, Pfizer, and Merck & Co. as its leading competitive entities. Canada plays an essential role in the market by implementing preventive strategies and making healthcare services more accessible to patients. The existence of major pharmaceutical companies creates strong new treatment development processes, which improve the medical options available to patients.

Asia Pacific is expected to grow at a rapid CAGR in the Atherosclerosis market during the forecast period. Asia Pacific is poised to be the fastest-growing region in the global atherosclerosis market, accounting for approximately20% during the forecast period of 2025 to 2035. The region has approximately 20% of the global market share because China and India represent the primary demand drivers. The introduction of advanced treatment options, with government initiatives for healthcare access improvement and awareness programs, functions as a major growth driver for the industry. The Chinese market ranks as the largest in the region because both domestic and foreign companies keep entering the marketplace. Pharmaceutical companies and healthcare providers establish partnerships that shape the competitive market because these alliances help make treatments more available to patients. The atherosclerosis market will experience substantial growth because the region continues to develop its healthcare infrastructure.

Europe is the 2nd largest region to grow in the Atherosclerosis market during the period. Europe is the second-largest market for atherosclerosis treatments, holding around 30% of the global market share. The region's growth is driven by increasing awareness of cardiovascular diseases, aging populations, and supportive regulatory frameworks. The European Medicines Agency (EMA) plays a crucial role in facilitating the approval of new therapies, which enhances market dynamics and patient access to innovative treatments. Leading countries include Germany, France, and the UK, where healthcare systems are increasingly prioritizing cardiovascular health. Major players like Novartis and Sanofi are actively involved in research and development, contributing to a competitive landscape.

Strategies to Implement for Growth of the Market in Non-Leading Regions

The atherosclerosis market in non-leading territories needs multiple strategic approaches. Expanding low-cost treatment options, especially generic statins, can address pricing barriers, while partnerships with global firms like Pfizer Inc. and Novartis AG can support technology transfer and local manufacturing. Strengthening healthcare infrastructure and increasing screening programs for early diagnosis are critical, as cardiovascular diseases account for nearly 32% of global deaths. Digital health and telemedicine can bridge rural access gaps, enabling remote monitoring and consultation. Governments should also implement reimbursement policies and public health campaigns to boost treatment adoption. Additionally, investing in clinical research and regional trials helps tailor therapies to local populations, accelerating market penetration and sustainable growth.

Future Market Trends in Global Atherosclerosis Market: -

1. Shift Toward Precision Medicine

The shift toward precision medicine is transforming the global atherosclerosis market by enabling targeted, patient-specific therapies based on genetic and biomarker data. Studies show personalized treatments can improve outcomes by 20–30%. Additionally, biomarker-based risk assessment may reduce cardiovascular events by 25%, driving adoption and supporting market growth beyond USD 60 billion by 2035.

2. Rise of RNA-Based & Biologic Therapies

The rise of RNA-based and biologic therapies is transforming atherosclerosis treatment by targeting genetic risk factors like lipoproteins. Advanced siRNA drugs such as olpasiran and lepodisiran have shown 90–97% reduction in Lp(a) levels in clinical trials, far exceeding traditional therapies. These long-acting treatments require infrequent dosing, improving patient compliance. As a result, they represent a high-growth segment in the global atherosclerosis market.

3. Integration of AI & Digital Health

Integration of AI and digital health is transforming the global atherosclerosis market by enabling early diagnosis, predictive analytics, and remote patient monitoring. AI-based tools improve diagnostic accuracy by 20–30%, while digital health adoption reached 38% market share (2024). These technologies reduce hospitalizations and enhance preventive cardiovascular care globally.

Recent Development

In January 2025, Arrowhead Pharmaceuticals, Inc. announced that the U.S. Food and Drug Administration (FDA) had accepted the New Drug Application (NDA) for investigational plozasiran for the treatment of familial chylomicronemia syndrome (FCS), a severe and rare genetic disease.

In June 2023, AGEPHA Pharma USA, LLC, announced the U.S. Food and Drug Administration (FDA) had approved LODOCO as the first anti-inflammatory atheroprotective cardiovascular treatment demonstrated to reduce the risk of myocardial infarction (MI), stroke, coronary revascularization, and cardiovascular death in adult patients with established atherosclerotic disease or with multiple risk factors for cardiovascular disease.

How is Recent Developments Helping the Market?

Recent developments are significantly helping the global atherosclerosis market by improving efficacy, convenience, and patient outcomes. Advanced therapies such as PCSK9 inhibitors and RNA-based drugs can reduce LDL cholesterol by 50–55%, with effects lasting up to six months, improving patient adherence. New experimental drugs like enlicitide have shown up to 60% LDL reduction in trials, expanding treatment options. Additionally, gene-editing technologies demonstrate up to 87% LDL reduction, indicating potential one-time cures. These innovations also promote plaque regression and reduce cardiovascular events by nearly 19–25%, enhancing clinical outcomes. Overall, such breakthroughs increase treatment effectiveness, attract investments, and expand patient populations, thereby accelerating the growth and evolution of the global atherosclerosis market

Market Segment

This study forecasts revenue at global, regional, and country levels from 2020 to 2035. Decision Advisors has segmented the atherosclerosis market based on the below-mentioned segments:

Global Atherosclerosis Market, By Stages

- Endothelial Damage and Immune Response

- Fatty Streak

- Plaque Growth

- Plaque Rupture

Global Atherosclerosis Market, By Diagnosis

- Ankle-brachial Index

- Doppler Ultrasound

- Echocardiogram

- Electrocardiogram

- Blood Tests

- Others

Global Atherosclerosis Market, By End User

- Hospitals

- Specialty Clinics

- Homecare

- Others

Global Atherosclerosis Market, By Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa

Frequently Asked Questions (FAQ).

Q: What are the most commonly used drugs for atherosclerosis?

A: The most commonly used drugs are statins, which account for 55–60% market share due to their effectiveness and affordability. Other key drug classes include antiplatelets, beta-blockers, ACE inhibitors, and newer therapies like PCSK9 inhibitors and RNA-based drugs, which are gaining popularity for high-risk patients.

Q: How are new technologies impacting treatment outcomes?

A: New technologies such as AI-based diagnostics, advanced imaging, and digital monitoring tools are improving early detection and treatment accuracy by 20–30%. These innovations enable personalized care, reduce hospitalizations, and enhance long-term disease management, significantly improving patient outcomes and supporting market growth.

Q: What role do emerging markets play in growth?

A: Emerging markets like India, China, and Brazil are key growth drivers, with expected CAGRs of 7–8%, higher than global averages. Increasing healthcare investments, growing awareness, and rising disease burden contribute to demand, making these regions attractive for pharmaceutical companies expanding their global footprint.

Check Licence

Choose the plan that fits you best: Single User, Multi-User, or Enterprise solutions tailored for your needs.

We Have You Covered

- 24/7 Analyst Support

- Clients Across the Globe

- Tailored Insights

- Technology Tracking

- Competitive Intelligence

- Custom Research

- Syndicated Market Studies

- Market Overview

- Market Segmentation

- Growth Drivers

- Market Opportunities

- Regulatory Insights

- Innovation & Sustainability

Report Details

| Scope | Global |

| Pages | 190 |

| Delivery | PDF & Excel via Email |

| Language | English |

| Release | Mar 2026 |

| Access | Download from this page |