Global Autosomal Dominant Polycystic Kidney Disease Market

Global Autosomal Dominant Polycystic Kidney Disease (ADPKD) Treatment Market Size, Share, By Treatment Type (Vasoactive Intestinal Peptide Receptor Agonists, Somatostatin Analogs, Renin-Angiotensin-Aldosterone System Inhibitors, Diuretics, and Pain Medications), By Drug Class (Tolvaptan, Octreotide, Vasopressin Receptor Antagonists, Furosemide, and Ibuprofen), By Stage of Disease (Early-stage ADPKD, Mid-stage ADPKD, and Late-stage ADPKD), By Patient Population (Children and Adolescents, Adults, and Elderly Patients) and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2025-2035.

REPORT COVERAGE

Global

Market Snapshot

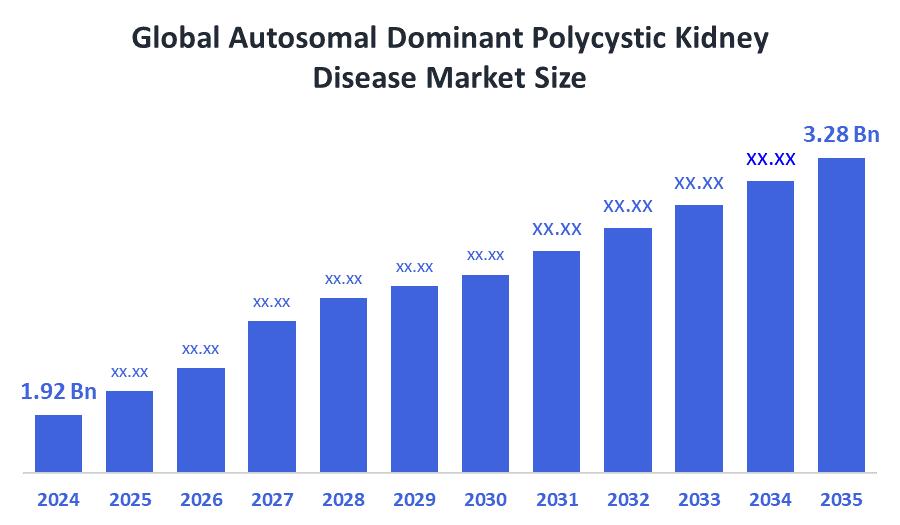

- Market Size (2025): USD 1.92 Billion

- Projected Market Size (2035): USD 3.28 Billion

- Compound Annual Growth Rate (CAGR): 5.5%

- Largest Regional Market: North America

- Fastest Growing Region: Asia-Pacific

- 3rd Largest Region: Europe

- Base Year: 2025

- Historical Period: 2021–2024

- Forecast Period: 2025–2035

According to Decision Advisors, the Global Autosomal Dominant Polycystic Kidney Disease Market Size is expected to grow from USD 1.92 billion in 2025 to USD 3.28 billion by 2035, at a CAGR of 5.5% during the forecast period 2025-2035. The global Autosomal Dominant Polycystic Kidney Disease market is growing due to rising prevalence, increased awareness, and demand for targeted therapies. Advances in diagnostics, disease-modifying treatments, precision medicine, and improved nephrology care are accelerating market development and supporting long-term growth and better patient outcomes worldwide.

Market Overview/ Introduction

The global autosomal dominant polycystic kidney disease (ADPKD) market focuses on the diagnosis, treatment, and management of a genetic disorder characterized by multiple cysts in the kidneys, often leading to progressive renal failure. Rising prevalence of genetic kidney disorders, growing awareness, and early diagnosis are driving demand for targeted, disease-modifying therapies. Technological advancements, including AI-assisted imaging, Total Kidney Volume measurements, and next-generation genetic testing, are enabling precise detection and risk stratification, while digital health platforms improve patient monitoring and adherence. The market is further supported by increasing healthcare expenditure, improved nephrology infrastructure, and regulatory encouragement for novel therapies. Investment in precision medicine and innovative therapeutics is expanding treatment options and improving clinical outcomes. Future opportunities include gene-editing technologies, personalized medicine, and AI-driven predictive diagnostics, which promise to enhance patient care, broaden accessibility, and accelerate market growth. Collectively, these factors position the ADPKD market for significant long-term expansion, driven by innovation, improved patient outcomes, and increasing adoption of advanced therapies worldwide.

- The PKD Foundation secured $15.66?million in Congressionally Directed Medical Research Programs grants in 2024, marking a 347?% increase. This funding surge accelerates the development of novel therapies, supporting research and innovation in the global autosomal dominant polycystic kidney disease market.

- The FDA cleared Vertex’s VX?407 Investigational New Drug application for ADPKD in March 2024, enabling Phase?I trials. This milestone advances targeted therapy development, strengthening the global Autosomal Dominant Polycystic Kidney Disease market and expanding potential treatment options.

- The Pradhan Mantri National Dialysis Programme (PMNDP) provides free hemodialysis for Below Poverty Line patients at district hospitals, while Ayushman Bharat – PMJAY offers financial support up to ?5?lakh per family per year for secondary and tertiary care, including dialysis.

Notable Insights: -

- North America holds the largest regional market share of approximately 43% in the global Autosomal Dominant Polycystic Kidney Disease market.

- Asia-Pacific is the fastest growing regional market share of approximately 16% in the global Autosomal Dominant Polycystic Kidney Disease market.

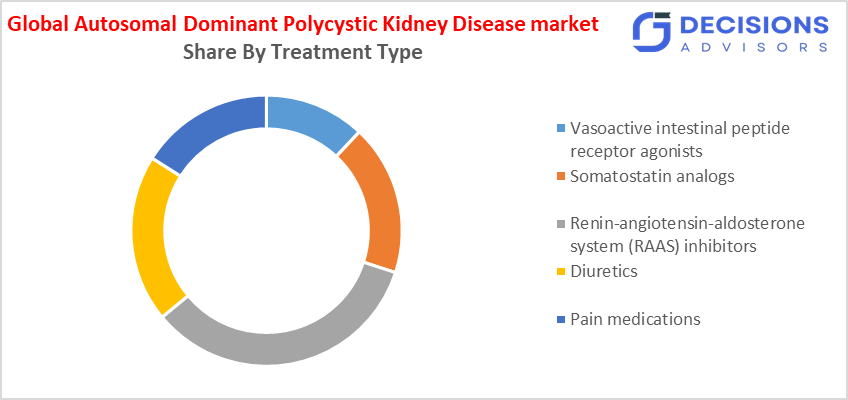

- By treatment type, the renin-angiotensin-aldosterone system (RAAS) inhibitors segment held a dominant position with 34% in terms of market share in 2025.

- By drug class, the vasopressin receptor antagonists (tolvaptan) segment is the dominating accounting for over 60% of the global market share in 2025.

- By stage of disease, the early-stage ADPKD segment is the dominating accounting for over 58% of the global market share in 2025.

- By patient population, the adult segment is the dominating accounting for over 62% of the global market share in 2025.

- The compound annual growth rate of the global spirit market is 5.5%.

- The market is likely to achieve a valuation of USD 3.28 billion by 2035.

What is role of technology in grooming the market?

Technology is playing a transformative role in grooming the global autosomal dominant polycystic kidney disease market by enhancing diagnosis, treatment, and patient management. AI and machine learning streamline diagnostic imaging, automating Total Kidney Volume measurements and enabling earlier identification of rapid progressors for personalized care. Advanced drug discovery leverages AI for high-throughput screening and repurposing opportunities. Next-generation sequencing improves detection of PKD1 and PKD2 mutations, supporting earlier family-based screening, while experimental gene-editing technologies aim to correct underlying mutations. Bioengineered 3D renal organoids provide accurate therapy testing platforms, and digital health monitoring enables remote tracking of hydration, blood pressure, and medication adherence, collectively boosting market adoption and growth.

How is Recent Developments Helping the Market?

Recent developments such as product innovation, precision-targeted therapies, and integration of AI-driven diagnostics are supporting the growth of the global Autosomal Dominant Polycystic Kidney Disease market. Novel disease-modifying therapies and combination treatments are expanding patient options and addressing unmet medical needs, driving adoption. Early detection technologies, including advanced imaging and genetic testing, are increasing the treatable population, fueling market demand. Investment in emerging therapeutics and digital patient monitoring platforms is accelerating innovation and improving care delivery. Additionally, growing awareness and enhanced nephrology infrastructure in regions such as Asia-Pacific and Latin America are enabling broader access, collectively strengthening the overall market value and long-term growth potential.

Market Drivers

The global autosomal dominant polycystic kidney disease market is propelled by the widespread adoption of tolvaptan, a vasopressin receptor antagonist, which slows cyst growth and drives treatment uptake. Early detection through genetic testing and advanced imaging expands the treatable patient population. Rising prevalence of ADPKD and associated renal failure further increases demand for therapeutics. Ongoing research and development into combination therapies and novel drugs, supported by high healthcare expenditure in developed regions, accelerates market growth. Growing awareness and improving nephrology infrastructure in emerging regions, including Asia-Pacific and Latin America, offer significant growth opportunities. Integration of AI-driven diagnostics and digital monitoring is also enhancing patient care and market potential.

Restrain

The global autosomal dominant polycystic kidney disease market is restrained by high treatment costs, limited therapeutic options, and complex regulatory approvals that delay new drugs. Additionally, unfavourable reimbursement policies and potential serious side effects, including liver damage, restrict patient access and adoption, particularly in low-to-middle-income regions, slowing overall market growth.

Competitive Analysis:

The report offers the appropriate analysis of the key organizations/companies involved within the global autosomal dominant polycystic kidney disease market, along with a comparative evaluation primarily based on their product of offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes product development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

Top Companies in Global Autosomal Dominant Polycystic Kidney Disease Market

- Otsuka Pharmaceutical Co., Ltd.

- Sanofi S.A.

- Vertex Pharmaceuticals Incorporated

- Regulus Therapeutics

- Novartis AG

- XORTX Therapeutics

- Reata Pharmaceuticals

- Kadmon Pharmaceuticals

- AceLink Therapeutics

- Healx

- Alebund Pharmaceuticals

- Chinook Therapeutics

- Palladio Biosciences

- AbbVie Inc.

Government Initiatives

|

Country |

Key Government Initiatives |

|

UK |

The PKD Charity, in collaboration with the James Lind Alliance (JLA), conducted a Priority Setting Partnership (2019–2020) to identify the top 10 research priorities for ADPKD, focusing on slowing disease progression and improving patient care. |

|

US |

FDA approved Tolvaptan in 2018, the first drug specifically to slow kidney function decline in adults at risk of rapidly progressing ADPKD. The PKD Foundation launched Centers of Excellence (COE) and Partner Clinics in 2022, establishing 37 COEs and 24 Partner Clinics by 2023 to standardize care. The NIH continues to fund research on causes, treatments, and cures for ADPKD. |

Market Segmentation

The autosomal dominant polycystic kidney disease market share is classified into treatment type, drug class, stage of disease, and patient population

- The renin-angiotensin-aldosterone system (RAAS) inhibitors segment dominated the market in 2025, and is projected to grow at a substantial CAGR of approximately 34% during the forecast period.

Based on the treatment type, the market is segmented into vasoactive intestinal peptide receptor agonists, somatostatin analogs, renin-angiotensin-aldosterone system inhibitors, diuretics, and pain medications. Among these, the RAAS inhibitors segment dominated the market in 2025, accounting for approximately 34% of the global market share. This is due to their widespread use in managing hypertension, which is one of the earliest and most common complications in ADPKD patients. These drugs are frequently prescribed as first-line therapy, ensuring consistent demand across all stages of the disease. Their affordability and availability further strengthen their dominance. Europe plays a key role in supporting this segment due to strong clinical guideline adherence.

- The vasopressin receptor antagonists (tolvaptan) segment dominated the market in 2025, and is projected to grow at a substantial CAGR of approximately 60% during the forecast period.

Based on the drug class, the ADPKD treatment market is divided into tolvaptan, octreotide, vasopressin receptor antagonists, furosemide, and ibuprofen. Among these, the vasopressin receptor antagonists segment dominated the market in 2025, accounting for approximately 60% of the global market share. This dominance is primarily attributed to the fact that tolvaptan remains the only widely approved disease-modifying therapy for ADPKD, making it the cornerstone of treatment. Its strong clinical efficacy in slowing cyst growth and preserving kidney function has significantly increased its adoption. Additionally, increasing awareness and early diagnosis are further driving demand. North America acts as a major driver for this segment due to strong regulatory approvals and high treatment accessibility.

- The early-stage ADPKD segment dominated the market in 2025, and is projected to grow at a substantial CAGR of approximately 60% during the forecast period.

Based on the stage of disease, the market is divided into early-stage ADPKD, mid-stage ADPKD, and late-stage ADPKD. Among these, the early-stage segment dominated the market in 2025, accounting for approximately 58% of the global market share. This dominance is primarily attributed to the increasing focus on early diagnosis and timely therapeutic intervention to slow disease progression. Advances in genetic testing and imaging technologies have enabled earlier detection, which leads to higher treatment adoption at initial stages. Additionally, the availability of disease-modifying therapies encourages proactive disease management. North America acts as a major driver for this segment due to strong screening programs and early treatment accessibility.

- The adults segment dominated the market in 2025, and is projected to grow at a substantial CAGR of approximately 62% during the forecast period.

Based on the patient population, the market is segmented into children and adolescents, adults, and elderly patients. Among these, the adult segment dominated the market in 2025, accounting for approximately 62% of the global market share. This is due to the higher diagnosis rate and disease progression typically occurring during adulthood, leading to increased treatment demand. Adults are more likely to undergo regular monitoring and therapeutic interventions, ensuring consistent market contribution. Additionally, improved awareness and access to healthcare further support segment growth. North America acts as a major driver for this segment due to advanced diagnostic capabilities and strong treatment accessibility.

What is the Reason of the Region Dominance?

North America’s dominance in the Autosomal Dominant Polycystic Kidney Disease market is primarily driven by its highly advanced healthcare infrastructure, which enables early diagnosis and effective disease management. The region benefits from strong research and development capabilities, leading to faster adoption of innovative and disease-modifying therapies. Additionally, high healthcare expenditure and favorable reimbursement policies ensure better patient access to expensive treatments. The presence of leading pharmaceutical companies and ongoing clinical trials further strengthens market growth. Moreover, widespread awareness, established screening programs, and a higher diagnosis rate contribute significantly to sustained demand, making North America the leading regional market.

Strategies to Implement for Growth of the Market in Non-Leading Regions

Growth in non-leading regions of the autosomal dominant polycystic kidney disease market can be driven by strengthening diagnostic infrastructure, including wider access to genetic testing and imaging for early detection. Expanding healthcare facilities and specialist care centers will improve treatment accessibility. Cost reduction strategies such as local manufacturing, generic drug adoption, and flexible pricing models can enhance affordability. Increasing awareness among patients and healthcare professionals will support early diagnosis and timely intervention. Government support through favorable policies and faster regulatory approvals will encourage market entry of new therapies. Additionally, digital health solutions such as telemedicine and remote monitoring can improve disease management and expand reach in underserved areas.

Regional Segment Analysis of the Autosomal Dominant Polycystic Kidney Disease Market

- North America (U.S., Canada, Mexico)

- Europe (Germany, France, U.K., Italy, Spain, Rest of Europe)

- Asia-Pacific (China, Japan, India, Rest of APAC)

- South America (Brazil and the Rest of South America)

- The Middle East and Africa (UAE, South Africa, Rest of MEA)

North America is anticipated to hold the largest share of the global autosomal dominant polycystic kidney disease market over the predicted timeframe. This market is accounting about approximately 43% of the total market share, the dominance of this market is driven by advanced healthcare infrastructure, strong research and development activities, and early adoption of disease-modifying therapies. Countries such as the United States and Canada have well-established healthcare systems that drive significant demand for Autosomal Dominant Polycystic Kidney Disease treatment. In particular, the United States dominates the global Autosomal Dominant Polycystic Kidney Disease market, supported by high healthcare expenditure and strong presence of leading pharmaceutical companies.

Asia Pacific is expected to grow at a rapid CAGR in the global autosomal dominant polycystic kidney disease market during the forecast period. It is the fastest growing region because it holds the highest CAGR of approximately 16% which is driven by the increasing patient population, improving diagnostic capabilities, and rising healthcare investments across countries like China and India. Nowadays patients are increasingly gaining access to advanced treatment options and early diagnosis, which is boosting the demand for effective Autosomal Dominant Polycystic Kidney Disease treatment solutions across the region.

Europe is the 3rd largest region to grow in the global autosomal dominant polycystic kidney disease market during the forecast period. It is because Europe holds approximately 30% of the total market share, driven by strong reimbursement systems and increasing adoption of genetic testing. The region has a well-established healthcare framework and high awareness regarding rare genetic disorders, which supports early diagnosis and treatment adoption. Countries such as Germany, France, and the United Kingdom play a key role in contributing to the market growth due to advanced clinical practices and supportive healthcare policies.

Future Market Trends in Global Autosomal Dominant Polycystic Kidney Disease Market: -

- Premium and Next-Generation ADPKD Therapies

Patients are increasingly adopting next-generation ADPKD treatments, preferring high-efficacy, disease-modifying options like mTOR inhibitors and novel molecules over conventional care. These advanced therapies are reshaping the market as safety, effectiveness, and innovation become priorities.

- Rising Demand for AI-Enhanced Diagnostics and Genetic Testing

Advanced diagnostic tools, including AI-powered MRI and genetic testing for PKD1/PKD2 mutations, are gaining adoption in specialty clinics. Early detection and personalized monitoring are driving growth and improving disease management outcomes.

- Growth of Combination Therapy Strategies

Combination therapies with tolvaptan or safer novel agents are increasingly favored, offering improved tolerability and reduced liver toxicity risks. This strategy is expanding the therapeutic landscape and enhancing patient care, particularly in regions with advanced healthcare infrastructure.

Recent Development

- In June 2025, Regulus Therapeutics announced positive topline results from its Phase?1b multiple?ascending dose (MAD) clinical trial of RGLS8429 (farabursen), a novel miR?17 inhibitor for ADPKD, signalling a significant expansion of the next-generation, disease-modifying therapy pipeline.

- In March 2024, Vertex Pharmaceuticals received FDA clearance for the IND application of VX?407, a first-in-class small molecule targeting PKD1 variants, marking a key milestone in precision therapy development for ADPKD.

- In October 2024, Rege Nephro Co., Ltd. secured Series?B funding and advanced its investigational ADPKD therapy RN?014 (tamibarotene) into Phase?II clinical trials, highlighting investment-driven innovation in emerging therapeutics.

Market Segment

This study forecasts revenue at global, regional, and country levels from 2020 to 2035. Decision Advisor has segmented the autosomal dominant polycystic kidney disease market based on the below-mentioned segments:

Global ADPKD Treatment Market, By Treatment Type

- Vasoactive Intestinal Peptide Receptor Agonists

- Somatostatin Analogs

- Renin-Angiotensin-Aldosterone System Inhibitors

- Diuretics

- Pain Medications

Global ADPKD Treatment Market, By Drug Class

- Tolvaptan

- Octreotide

- Vasopressin Receptor Antagonists

- Furosemide

- Ibuprofen

Global ADPKD Treatment Market, By Stage of Disease

- Early-stage ADPKD

- Mid-stage ADPKD

- Late-stage ADPKD

Global ADPKD Treatment Market, By Patient Population

- Children and Adolescents

- Adults

- Elderly Patients

Global Autosomal Dominant Polycystic Kidney Disease Market, By Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa

Frequently Asked Questions (FAQ)

Q. How are emerging digital therapeutics shaping patient adherence in ADPKD treatment?

A. Digital therapeutics, including mobile apps and remote monitoring platforms, are improving patient adherence by providing reminders, tracking biomarkers, and enabling real-time communication with healthcare providers, enhancing treatment outcomes and overall disease management.

Q. What impact could gene-editing research have on the future ADPKD market?

A. Gene-editing technologies such as CRISPR hold the potential to correct underlying PKD1/PKD2 mutations, which may transform the treatment landscape by offering curative solutions and creating new market opportunities for advanced, personalized therapies.

Q. How is telemedicine influencing ADPKD patient care in emerging regions?

A. Telemedicine is increasing access to nephrology specialists in remote or underserved regions, allowing early diagnosis, regular monitoring, and timely therapeutic interventions, which can improve outcomes and expand the patient base in these markets.

Q. Are wearable devices contributing to ADPKD disease monitoring?

A. Yes, wearable devices that track blood pressure, hydration, and kidney-related biomarkers help in continuous monitoring, providing clinicians with actionable data to adjust treatment plans and improve long-term patient management.

Q. What role do public-private partnerships play in accelerating ADPKD research and therapy availability?

A. Collaborations between government agencies, research foundations, and pharmaceutical companies enable faster clinical trials, shared resources, and broader distribution of innovative therapies, fostering growth and faster adoption of ADPKD treatments globally.

Check Licence

Choose the plan that fits you best: Single User, Multi-User, or Enterprise solutions tailored for your needs.

We Have You Covered

- 24/7 Analyst Support

- Clients Across the Globe

- Tailored Insights

- Technology Tracking

- Competitive Intelligence

- Custom Research

- Syndicated Market Studies

- Market Overview

- Market Segmentation

- Growth Drivers

- Market Opportunities

- Regulatory Insights

- Innovation & Sustainability

Report Details

| Scope | Global |

| Pages | 220 |

| Delivery | PDF & Excel via Email |

| Language | English |

| Release | Mar 2026 |

| Access | Download from this page |