Global Backflow Preventers Market

Global Backflow Preventers Market Size, Share By Product Type (Atmospheric Vacuum Breaker, Pressure Vacuum Breaker, Double Check Valve Assembly, and Reduced Pressure Zone), By Material Type (Stainless Steel, Plastic, Ductile Iron, Bronze, and Others), By Application (Residential, Commercial, Industrial, and Municipal Water Systems) and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East & Africa), Analysis and Forecast 2026-2035.

REPORT COVERAGE

Global

Market Snapshot

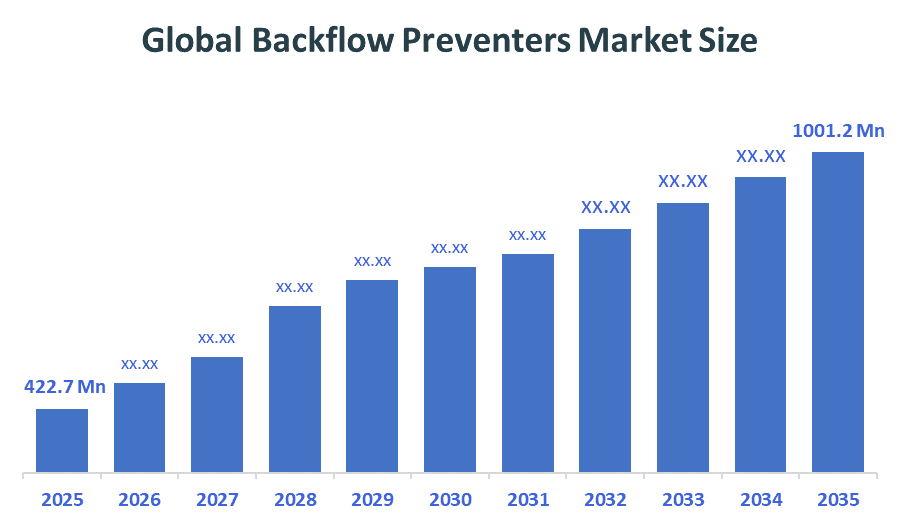

- Global Backflow Preventers Market Size (2025): USD 422.7 Million

- Projected Global Backflow Preventers Market Size (2035): USD 1001.2 Million

- Global Backflow Preventers Market Compound Annual Growth Rate (CAGR): 9.01%

- Largest Regional Market: Asia Pacific

- 2nd Largest Region: North America

- Fastest Growing Region: Europe

- Base Year: 2025

- Historical Period: 2021–2024

- Market Forecast Period: 2026–2035

According to Decision Advisors, the Global Backflow Preventers Market Size is expected to grow from USD 422.7 Million in 2025 to USD 1001.2 Million by 2035, at a CAGR of 9.01% during the forecast period 2026-2035. The Global Backflow Preventers Market growth is driven by rising emphasis on safe drinking water, stricter regulatory requirements for contamination control, and increasing investments in urban water infrastructure. Expanding construction activities and industrial water management needs further support market demand.

Market Overview/ Introduction

The Global Backflow Preventers Market consists of valve-based devices that stop reverse water flow to safeguard drinking water systems from contamination across residential, commercial, industrial, and municipal sectors. The market growth is driven by two factors, which include the rapid pace of urbanization, the ongoing development of infrastructure, rising need for secure water distribution systems. The adoption of water safety standards and cross-connection control regulations that governments have established helps for further adoption. Key companies are developing new products through the creation of smart monitoring systems and the use of strong materials and the development of new products improves their operational efficiency and legal compliance. The market operates under two strong factors which include extensive regulatory support and multiple uses of products, and ongoing need for product replacement. The upcoming growth of the market will receive support from three elements includes smart city projects, digital water management systems and global funding increases for sustainable infrastructure and water conservation initiatives.

Notable Insights: -

- Asia Pacific is anticipated to hold approximately 32% share of the global backflow preventers market over the predicted timeframe.

- North America is expected to grow at a rapid CAGR in the backflow preventers market by holding approximately 34% of the share during the forecast period.

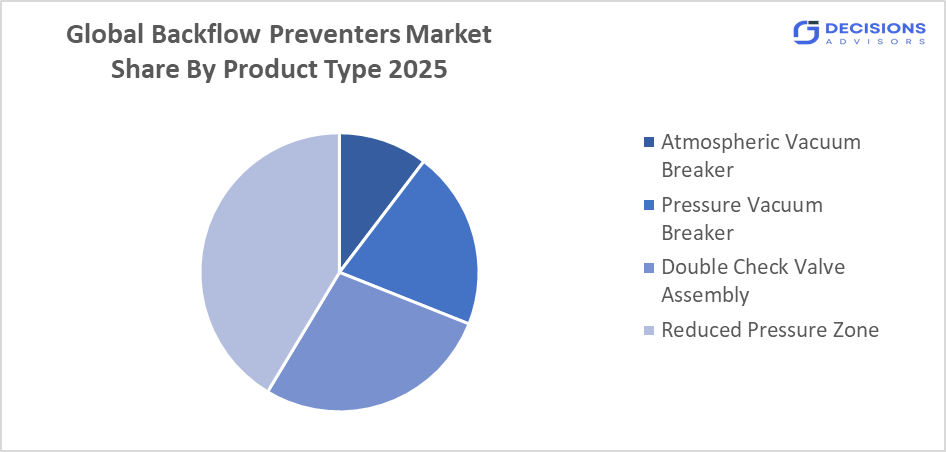

- By product type, the reduced pressure zone segment dominated the market and holds approximately 38% share in 2025 and is projected to grow at a substantial CAGR during the forecast period.

- By material type, the ductile iron segment dominated the market and holds approximately 42% share in 2025 and is projected to grow at a substantial CAGR during the forecast period.

- The compound annual growth rate of the global backflow preventers market is 9.01%.

- The market is likely to achieve a valuation of USD 1001.2 Million by 2035.

What is the role of technology in grooming the market?

Technology plays a crucial role in advancing the global backflow preventers market by improving efficiency, reliability, and monitoring capabilities. The integration of IoT-enabled sensors allows real-time tracking of pressure changes and system performance, enabling early detection of faults. Smart backflow preventers support predictive maintenance, reducing downtime and operational costs. Advanced materials such as corrosion-resistant alloys and high-performance plastics enhance durability and lifespan. Digital water management systems and automation are also increasing adoption, especially in smart city projects. Additionally, innovations in compact design and compliance technology help meet strict regulatory standards, making systems more effective and easier to install across various applications.

Market Drivers

The global backflow preventers market is supported by increasing focus on water safety and contamination prevention across residential and industrial systems. Stringent government regulations for potable water protection are driving mandatory installations. Rapid urbanization and infrastructure development are expanding the need for reliable water distribution networks. Additionally, rising investments in municipal water supply systems are strengthening demand globally. Industrial and commercial sectors are also adopting backflow prevention devices to ensure compliance and operational safety. These factors collectively contribute to steady market expansion by increasing awareness, regulatory enforcement, and the need for efficient water management solutions across developed and emerging regions.

Restrain

The global backflow preventers market faces restraints due to high installation and maintenance costs, especially for advanced systems, which limit adoption in cost-sensitive regions. Lack of awareness in developing markets further restricts widespread implementation. Additionally, retrofitting backflow preventers into existing infrastructure is complex and requires significant investment. The presence of low-cost, non-compliant alternatives in unregulated markets also challenges the growth of standardized, high-quality solutions, impacting overall market penetration and adoption rates.

Competitive Analysis:

The report offers the appropriate analysis of the key organizations/companies involved within the global backflow preventers market, along with a comparative evaluation primarily based on their product of offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes product development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

Top Companies in the Global Backflow Preventers Market

- Watts Water Technologies

- Zurn Industries

- Honeywell International

- Emerson Electric Co.

- Danfoss

- AVK Group

- Cla-Val

- Caleffi S.p.A.

- Reliance Worldwide Corporation

- Apollo Valves

Government Initiatives

|

Country |

Key Government Initiatives |

|

US |

The U.S. EPA’s Cross?Connection Control program mandates installation, testing, and maintenance of backflow preventers, driving consistent demand for devices and compliance services, directly supporting growth in the U.S. backflow preventers market. |

|

UK |

The UK’s RPZ AIM initiative, effective January 2025, standardizes installation and testing of RPZ backflow devices, enforces new test equipment specifications, and mandates tester competency to ensure potable water protection. |

|

China |

China’s GB?50015?2019 standard mandates backflow risk assessment and proper prevention facilities in water systems, driving demand for certified backflow preventers and related installation and maintenance services. |

Study on the Supply, Demand, Distribution, and Market Environment of the Backflow Preventers Market

Demand in the global backflow preventers market is driven by expanding urban infrastructure, stricter water safety regulations, and increasing adoption across residential, commercial, and industrial sectors. Supply is supported by global manufacturers focusing on durable, compliant, and technologically advanced products. Distribution occurs through plumbing distributors, contractors, and direct sales to municipalities and industries. The market environment is shaped by regulatory enforcement, infrastructure investments, and growing awareness of water contamination risks. Additionally, rising smart water management initiatives and modernization of aging pipeline systems are strengthening overall market dynamics across both developed and emerging regions.

Price Analysis and Consumer Behaviour Analysis

Pricing in the global backflow preventers market varies based on product type, material, and pressure rating. Basic devices typically range from USD 50 to USD 200, while advanced systems such as reduced pressure zone (RPZ) units, range between USD 500 and USD 3,000+ depending on capacity and features. End users prioritize reliability, compliance, and durability. Although initial costs are higher for advanced systems, they offer long-term savings through reduced maintenance and improved efficiency, making them cost-effective over time.

Market Segmentation

The global backflow preventers market share is classified into type, material type and application.

- The reduced pressure zone segment dominated the market and holds approximately 38% share in 2025 and is projected to grow at a substantial CAGR during the forecast period.

Based on the product type, the global backflow preventers market is divided into atmospheric vacuum breaker, pressure vacuum breaker, double check valve assembly, and reduced pressure zone. Among these, the reduced pressure zone segment dominated the market and holds approximately 38% share in 2025 and is projected to grow at a substantial CAGR during the forecast period. This dominance is due to its superior protection against backflow and contamination, especially in high-risk applications such as industrial facilities and municipal water systems. Its high reliability and compliance with stringent safety regulations drive widespread adoption globally.

- The ductile iron segment accounted for the largest share of approximately 42% in 2025 and is anticipated to grow at a significant CAGR during the forecast period.

Based on the material type, the global backflow preventers market is divided into stainless steel, plastic, ductile iron, bronze, and others. Among these, the ductile iron segment accounted for the largest share of approximately 42% in 2025 and is anticipated to grow at a significant CAGR during the forecast period. This dominance is driven due to its strength, durability, and cost-effectiveness, making it suitable for large-scale municipal and industrial water systems. Stainless steel is also gaining traction due to corrosion resistance.

- The municipal water systems segment accounted for the largest share of approximately 40% in 2025 and is anticipated to grow at a significant CAGR during the forecast period.

Based on the application, the market is segmented into residential, commercial, industrial, and municipal water systems. Among these, municipal water systems segment accounted for the largest share of approximately 40% in 2025 and is anticipated to grow at a significant CAGR during the forecast period. This dominance is driven due to strict regulatory requirements for water safety and large-scale deployment in urban infrastructure. Increasing investments in public water supply networks further drive segment growth.

Strategies to Implement for Growth of the Market in Non-Leading Regions

Growth in non-leading regions can be achieved by promoting cost-effective backflow prevention solutions and encouraging local manufacturing to reduce overall costs. Governments should introduce supportive regulations and incentives to ensure compliance with water safety standards. Expanding urban water infrastructure and improving access to safe drinking water will increase demand. Strategic partnerships with local distributors, contractors, and municipalities can enhance market penetration. Additionally, awareness campaigns and technical training programs can improve adoption rates. Investment in durable, low-maintenance products tailored for developing regions will further support sustainable market expansion and long-term growth.

Regional Segment Analysis of the Backflow Preventers Market

- North America (U.S., Canada, Mexico)?

- Europe (Germany, France, U.K., Italy, Spain, Rest of Europe)

- Asia-Pacific (China, Japan, India, Rest of APAC)

- South America (Brazil and the Rest of South America)?

- The Middle East and Africa (UAE, South Africa, Rest of MEA)

Asia Pacific is anticipated to hold approximately 32% share of the global backflow preventers market over the predicted timeframe.

Asia Pacific is anticipated to hold approximately 32% share of the global Backflow Preventers market over the predicted timeframe. The region’s dominance is driven by rapid urbanization, population growth, and expanding water infrastructure across countries such as China, India, and Japan. Increasing government investments in municipal water systems and rising awareness regarding water safety are further supporting market growth. Additionally, industrial expansion and construction activities are increasing demand for reliable water protection systems. The adoption of regulatory standards for contamination prevention and ongoing smart city projects are also contributing significantly to the region’s market leadership.

North America is expected to grow at a rapid CAGR in the backflow preventers market by holding approximately 34% of the share during the forecast period

North America is expected to grow at a rapid CAGR in the Backflow Preventers market by holding approximately 34% share during the forecast period. Growth is driven by stringent water safety regulations, advanced plumbing infrastructure, and strong enforcement of cross-connection control programs. Increasing investments in water system upgrades and replacement of aging infrastructure further support demand. Additionally, high awareness regarding water contamination risks and widespread adoption across residential, commercial, and industrial sectors contribute significantly to market expansion in the region.

Europe is the fastest-growing region in the backflow preventers market during the period, holding approximately 28% share.

Europe is the fastest-growing region in the Backflow Preventers market during the period, holding approximately 28% share. Growth is driven by stringent water safety regulations, increasing investments in modern water infrastructure, and strong adoption of advanced plumbing systems. Countries such as Germany, France, and the U.K. are leading due to strict compliance standards and replacement of aging water networks. Additionally, rising focus on sustainable water management and smart infrastructure development is further accelerating demand for backflow prevention devices across the region.

Future Market Trends in Global Pod Taxi Market: -

1. Smart Water Management Systems

Integration of IoT and automation is transforming water infrastructure by enabling real-time monitoring of pressure, flow, and system performance. These systems help detect faults early, reduce water losses, and improve operational efficiency. Utilities and industries benefit from predictive maintenance, lower downtime, and better compliance with safety standards, driving adoption of advanced backflow prevention solutions.

2. Adoption of Corrosion-Resistant Materials

Use of materials such as stainless steel, advanced polymers, and coated alloys is improving durability and lifespan of backflow preventers. These materials reduce wear, corrosion, and maintenance frequency, especially in harsh water conditions. As a result, end users benefit from lower lifecycle costs and improved reliability, making them increasingly preferred in industrial and municipal applications.

3. Growth in Smart Cities

Smart city projects are accelerating deployment of advanced water infrastructure, including automated and digitally monitored backflow preventers. These systems ensure safe and efficient water distribution in densely populated urban areas. Increasing investments in intelligent utilities, sustainable infrastructure, and urban development are significantly boosting demand for modern backflow prevention technologies.

4. Regulatory Expansion

Governments are strengthening regulations related to water safety and contamination prevention. Mandatory installation and regular testing of backflow preventers are being enforced across residential, commercial, and industrial sectors. These stricter compliance requirements are driving consistent demand, encouraging adoption of certified devices, and pushing manufacturers to develop high-performance, regulation-compliant solutions.

Recent Development

- In September?2024, Watts Water Technologies launched the Series LF009 RPZ backflow preventer with integrated flood sensor and SentryPlus Alert IoT capability, enabling automated alerts for relief valve discharge via BMS or cellular systems.

- In January?2024, Watts Water Technologies launched the SentryPlus Alert RPZ backflow assembly, featuring IoT-enabled automatic shutoff and remote monitoring, improving compliance and performance compared to the 2021 Guardian Series

- In August?2024, Zurn launched the 900XL3 Series small backflow preventer, featuring a compact all?bronze design with modular internals for easier installation, maintenance, and improved compliance in residential and commercial plumbing systems.

How is Recent Developments Helping the Market?

Recent developments are supporting the global backflow preventers market by improving efficiency, durability, and compliance. Innovations such as smart monitoring and advanced materials enhance performance and reduce maintenance needs. New product launches and infrastructure investments are increasing adoption across residential and industrial sectors. Additionally, stricter regulations and growing focus on water safety are encouraging the use of advanced systems, strengthening overall market growth and reliability.

Market Segment

This study forecasts revenue at global, regional, and country levels from 2020 to 2035. Decision Advisors has segmented the global backflow preventers market based on the below-mentioned segments:

Global Backflow Preventers Market, By Product Type

- Atmospheric Vacuum Breaker

- Pressure Vacuum Breaker

- Double Check Valve Assembly

- Reduced Pressure Zone

Global Backflow Preventers Market, By Material Type

- Stainless Steel

- Plastic

- Ductile Iron

- Bronze

- Others

Global Backflow Preventers Market, By Application

- Residential

- Commercial

- Industrial

- Municipal Water Systems

Global Backflow Preventers Market, By Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa

Frequently Asked Questions (FAQ)

Q. What factors influence the selection of a backflow preventer type?

Selection depends on factors such as the level of contamination risk, water pressure conditions, installation location, regulatory requirements, and system design. High-risk applications typically require more advanced devices like RPZ units, while simpler systems may use basic vacuum breakers or double check valves.

Q. Are backflow preventers suitable for retrofit projects?

Backflow preventers can be installed in existing systems, but retrofitting may require pipeline adjustments, additional space, and compatibility checks. Proper planning is essential to ensure efficient integration without disrupting system performance or increasing installation complexity and costs.

Q. How often should backflow preventers be inspected or tested?

Backflow preventers should generally be tested at least once a year to ensure proper functioning and compliance with safety standards. In high-risk environments such as industrial facilities or hospitals, more frequent inspections may be required to prevent contamination risks and maintain system reliability.

Q. Are there energy efficiency considerations for backflow preventers?

While not directly energy-consuming devices, inefficient designs can cause pressure losses, indirectly increasing pumping energy requirements. Modern designs focus on minimizing flow resistance, helping improve overall system efficiency and reducing operational costs associated with water distribution systems in industrial and municipal applications.

Check Licence

Choose the plan that fits you best: Single User, Multi-User, or Enterprise solutions tailored for your needs.

We Have You Covered

- 24/7 Analyst Support

- Clients Across the Globe

- Tailored Insights

- Technology Tracking

- Competitive Intelligence

- Custom Research

- Syndicated Market Studies

- Market Overview

- Market Segmentation

- Growth Drivers

- Market Opportunities

- Regulatory Insights

- Innovation & Sustainability

Report Details

| Scope | Global |

| Pages | 192 |

| Delivery | PDF & Excel via Email |

| Language | English |

| Release | Apr 2026 |

| Access | Download from this page |