Global Bran Market

Global Bran Market Size, Share, By Source (Wheat, Rice, Corn, Barley), By Application (Food, Animal Feed, Health & Wellness), By Distribution Channel (B2B, B2C), and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2025 ? 2035.

REPORT COVERAGE

Global

Market Snapshot

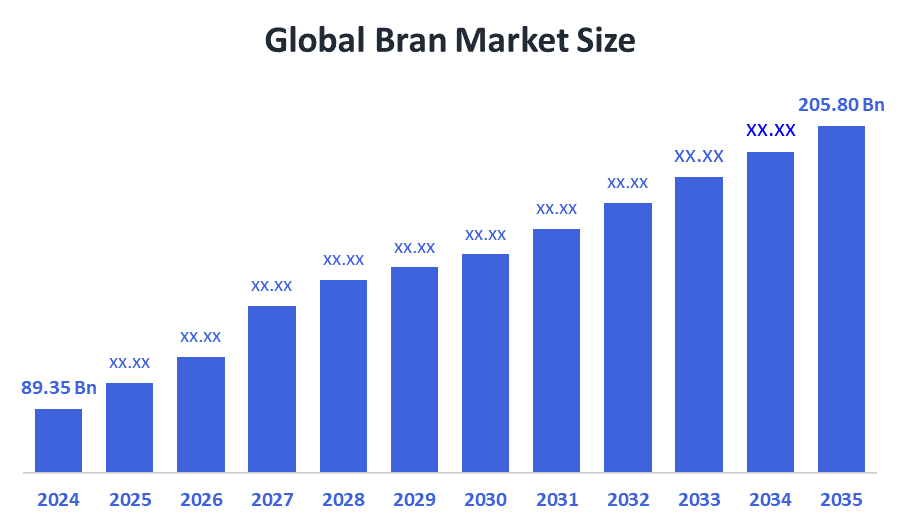

- Market Size (2025): USD 89.35 Billion

- Projected Market Size (2035): USD 205.80 Billion

- Compound Annual Growth Rate (CAGR): 8.70%

- Largest Regional Market: Asia-Pacific

- Fastest Growing Region: North America

- 3rd Largest Region: Europe

- Base Year: 2025

- Historical Period: 2021–2024

- Forecast Period: 2026–2035

According to Decision Advisors, the Global Bran Market Size is expected to grow from USD 89.35 Billion in 2024 to USD 205.80 Billion by 2035, at a CAGR of 8.70% during the forecast period 2025-2035. The Global Bran Market is expected to expand, primarily driven by growing consumer preference for high-fiber and functional foods, supported by increasing health awareness and a shift towards more nutritious dietary choices. Rising global cereal production ensures consistent bran supply, supporting scalability and market expansion.

Market Overview/ Introduction

The Global Bran Market consists of the production, processing, and utilization of cereal grain outer layers obtained during milling, primarily including wheat bran, rice bran, oat bran, and other grain-derived variants. The various uses of bran within animal feeds, food and beverages and nutraceuticals fall under the product scope with examples being used as a component of dietary fibre or as a functional additive. There is an apparent trend for increased health awareness amongst urban populations and younger consumers, leading to the development and demand for fibre-enriched clean-label food products. Consequently, there's been an increased usage of bran as a functional food in bakery products breakfasts cereal etc., which has further extended its use beyond traditional feeds as a form of functional foods.

Currently, the trend has been slowly transitioning away from low-value bulk uses, mainly animal feed, towards higher-quality applications in nutrition and speciality ingredients. The focus on health benefits, i.e., gut health improvement, weight loss, and cholesterol reduction, is resulting in increased demand for more expensive, more stabilised bran products.

- Archer Daniels Midland reported revenue of approximately USD 85.5 billion in 2024, supported by major institutional investors such as Vanguard and BlackRock, reflecting its strong global position in grain processing and bran supply.

- The APEDA promotes exports of cereal products, including bran, by providing financial assistance and infrastructure support. India’s total cereal production reached 332.05 million tonnes, strengthening export potential and supporting bran supply chains.

- China is the largest bran producer globally, driven by its extensive cereal production exceeding 640 million tonnes annually. High output of wheat, rice, and corn generates substantial bran as a byproduct, supporting large-scale availability for animal feed, food processing, and industrial applications.

Notable Insights: -

- Asia-Pacific holds the largest regional market share approximately 54% in the global bran market.

- North America is the fastest growing region in the global bran market.

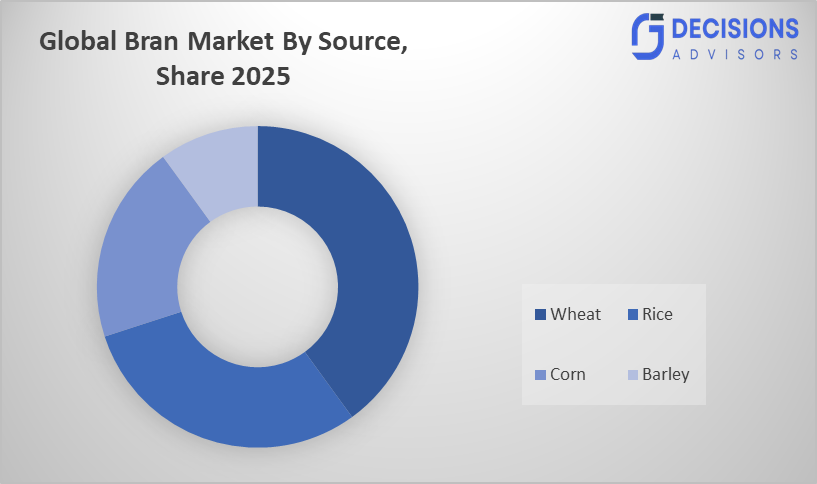

- By source, the wheat segment held a dominant position with 5.20% in terms of market share in 2025.

- By application, food segment is the dominating accounting for over 60% of the global market share in 2025.

- The compound annual growth rate of the global bran market is 8.70%.

- The market is likely to achieve a valuation of USD 205.80 billion by 2035.

What is the role of technology in grooming the market?

Technology plays an important role in improving efficiency and value across the global bran market over the long term. Stabilization of rice bran through stabilization technologies is critical because it contains 15%-20% oil and oxidizes quickly and, therefore, must be treated within 24 hours after milling to avoid rancidity. Automation of milling improves yield consistency, decreases material loss and aids in large-scale production. Digital systems along the supply chain improve traceability of product and allow for quality control throughout processing. Additionally, analytics help manufacturers track trends in consumer demand so they can create products that are high in fiber and functional. According to the Food and Agriculture Organization, global cereal production reached approximately 3,023 million tonnes in 2025, ensuring abundant raw material availability for bran processing and supporting technological advancements in the sector.

How is Recent Developments Helping the Market?

The Global Bran Market is projected to continue its growth due to new developments including innovative products, functional food products, and advances in processing technology. Furthermore, the introduction of more advanced stabilization technologies will improve shelf stability (particularly for rice bran), thus increasing their commercial feasibility. According to the Food and Agriculture Organization, global cereal utilization is projected to reach 2,943 million tonnes, reflecting sustained demand across food and feed sectors. This supports consistent bran production and its growing application in functional foods, nutraceuticals, and animal nutrition industries worldwide.

Market Drivers

The Global Bran Market is driven by increasing demand for high-fiber foods, rising health awareness, and expansion in animal nutrition. According to the OECD and Food and Agriculture Organization Agricultural Outlook, global wheat production is projected to reach approximately 840 million tonnes by 2032, supporting consistent bran availability from milling activities. Bunge Global SA reported USD 53.11 billion in revenue in 2024, highlighting strong investments in grain processing and supply chain expansion. Additionally, Wilmar International continues strengthening its market presence through strategic partnerships and downstream food ingredient developments. Increasing collaboration between milling companies and food manufacturers is driving innovation in functional and clean-label products. The rising incorporation of bran in nutraceuticals, bakery, and dietary supplements is further accelerating market growth globally.

Restrain

Due to its high natural oil content, particularly in rice bran, which speeds up oxidation and causes rancidity, short shelf life continues to be a major barrier in the bran industry. This raises operating and processing costs since it requires prompt stabilisation procedures after milling. Limited shelf stability also creates serious logistical problems for distribution, transit, and storage. Together, these characteristics impede commercial scalability and restrict wider acceptance in industrial, food, and feed applications worldwide.

Competitive Analysis:

The report offers the appropriate analysis of the key companies involved within the bran market, along with a comparative evaluation primarily based on their product of offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes product development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

Top Companies in Global Bran Market

- Archer Daniels Midland (ADM)

- Cargill, Incorporated

- Bunge Global SA

- Wilmar International Limited

- Ardent Mills

- Riceland Foods, Inc.

- Grain Millers, Inc.

- GoodMills Group GmbH

- Hindustan Animal Feeds

- Siemer Milling Company

- Didion Inc.

- Grain Processing Corporation

- Richardson International

- Viterra Limited

- Nisshin Seifun Group Inc.

Government Initiatives

|

Country |

Key Government Initiatives |

|

UK |

The UK government has implemented restrictions on the placement and promotion of products deemed high in fat, sugar, or salt, which affects marketing and promotional strategies for some processed breakfast cereals, though it encourages the reformulation of products to include higher fiber, such as bran. |

|

US |

A Department of Commerce program designed to facilitate job-creating business investment into the United States. It has supported over 265,000 U.S. jobs and facilitated over $390 billion in investment |

|

China |

The "National Unified Market" for regulatory standardization, the 14th Five-Year Plan targeting high-tech dominance, and massive consumer "trade-in" subsidies |

Market Segmentation

The bran market share is classified into source, application, and distribution channel.

- The wheat segment dominated the market in 2024, and is projected to grow at a substantial CAGR of approximately 50.2% during the forecast period.

Based on the source, the bran market is divided into wheat, rice, corn, barley. Among these, the wheat segment dominated the market in 2024, and is projected to grow at a substantial CAGR of approximately 50.2% during the forecast period. It is because of the strong global demand for wheat-based staple foods such as bread, pasta, and noodles. Growth is supported by rising population, expanding processed food consumption, and increasing use in animal feed. Advancements in high-yield and climate-resilient wheat varieties further enhance production. Additionally, growing health awareness is boosting demand for whole-grain products, while strong production and consumption in Asia Pacific continue to drive market expansion.

- The food segment accounted for the largest share in 2024, and is anticipated to grow at a significant CAGR of approximately 60% during the forecast period.

Based on the application, the bran market is divided into food, animal feed, health and wellness. Among these, the food segment accounted for the largest share in 2024, and is anticipated to grow at a significant CAGR of approximately 60% during the forecast period. The segment is dominating because of the high consumption and wide applications of bran in bakery, cereals, and snacks. Rising demand for fiber-rich diets, abundant raw material availability, and strong consumption in densely populated regions like Asia Pacific further support its leading market position.

- The B2B segment dominated the market in 2024, and is projected to grow at a substantial CAGR of approximately 50.5% during the forecast period.

Based on the distribution channel, the bran market is divided into B2B and B2C. Among these, the B2B dominated the market in 2024, and is projected to grow at a substantial CAGR of approximately 50.5% during the forecast period. This segment leads the market due to large-scale procurement by food processors, feed producers, and industrial buyers. bran serves as a cost-effective raw material in mass production, ensuring steady demand. Moreover, long-term contracts, predictable pricing, and widespread use across feed and processed food industries reinforce its dominant position.

Strategies to Implement for Growth of the Market in Non-Leading Regions

Addressing low consumer awareness and tailoring goods to local tastes are necessary for expanding the bran market in non-leading regions. By highlighting bran's high-fiber and prebiotic qualities and incorporating it into local items like snacks and baked goods, businesses may take advantage of the growing health consciousness. Creating gluten-free substitutes, such as rice or sorghum bran, can increase demand even more. While highlighting clean-label qualities, strategic marketing can raise awareness and trust through influencer partnerships and education programs. Increasing distribution via supermarkets, online retailers, and collaborations with food processors and producers of animal feed can improve accessibility, fortify supply chains, and guarantee steady demand in developing markets.

Regional Segment Analysis of the Bran Market

- North America (U.S., Canada, Mexico)

- Europe (Germany, France, U.K., Italy, Spain, Rest of Europe)

- Asia-Pacific (China, Japan, India, Rest of APAC)

- South America (Brazil and the Rest of South America)

- The Middle East and Africa (UAE, South Africa, Rest of MEA)

Asia Pacific is anticipated to hold the largest share of the bran market over the predicted timeframe.

Over the projected period, Asia Pacific is expected to have the biggest market share for bran. Due to the significant production and consumption of cereals in nations like China and India, this area has approximately 55% of the global market share. Market domination is further supported by fast urbanisation, population growth, and rising demand for diets high in fibre. India contributes 332.05 million tonnes of grains annually, producing significant amounts of bran as a milling by-product, whereas China generates over 657.5 million tonnes. Furthermore, approximately 50 million tonnes of wheat bran are produced in Asia-Pacific each year, supporting robust supply and demand in the food and feed sectors.

North America is expected to grow at a rapid ` in the bran market during the forecast period. Growing health consciousness and dietary changes toward clean-label and nutrient-rich ingredients are driving up demand for high-fiber and functional food products in this area. With more than 80% of North America's revenue, the United States leads the regional market thanks to its high consumption of baked goods and morning cereals. The U.S. produces more than 44 million tonnes of wheat a year, guaranteeing a consistent supply of bran, and the region also benefits from sophisticated food processing companies. Additionally, the industry is expanding more quickly due to the rising demand for nutraceuticals and animal feed.

Europe is the 3rd largest region to grow in the bran market during the region. It is due to its well-established food processing industry and strong demand for high-fiber products. The region accounts for approximately 20–25% of the global market share, supported by high consumption of bakery and cereal products in countries such as Germany, France, and the UK. Europe produces over 130 million tonnes of wheat annually, ensuring consistent bran availability. Additionally, rising demand for clean-label and organic foods, along with increasing health awareness, continues to support steady market growth across the region.

Future Market Trends in Global Bran Market: -

- Health and Wellness Focus

Consumers are increasingly prioritizing fiber-rich diets and functional foods, driving demand for bran as a natural source of dietary fiber and prebiotics. High-fiber food consumption has been associated with a 15–30% reduction in risk of digestive disorders and cardiovascular diseases, significantly influencing purchasing behavior toward bran-based products.

- Key Growth Segment

The breakfast cereal and snack segments are witnessing strong integration of bran to enhance nutritional value. The global breakfast cereal market, valued at over USD 40 billion, is increasingly incorporating wheat and oat bran to improve fiber content, supporting steady demand growth.

- Growth of Organic Products

Rising preference for organic and clean-label foods is boosting demand for natural, minimally processed ingredients. The global organic food market exceeds USD 220 billion, creating strong opportunities for bran, particularly rice bran, as a high-fiber, plant-based additive.

Recent Development

- In October 2025, India lifted restrictions on de-oiled rice bran exports, enabling the shipment of nearly 500,000 metric tons annually, strengthening global feed supply chains and stabilizing bran prices.

- In August 2025, Cargill expanded its grain processing capabilities in Asia to enhance wheat and rice by-product utilization, including bran, supporting growing demand from food and animal feed sectors.

- In March 2025, Archer Daniels Midland Company announced investments in milling and nutrition facilities to increase production of value-added ingredients such as wheat bran for functional food applications.

- In July 2024, Bunge Limited strengthened its oilseed and grain processing network, improving supply chain efficiency for by-products like bran used in livestock feed and food processing industries.

Market Segment

This study forecasts revenue at global, regional, and country levels from 2020 to 2035. Spherical Insights has segmented the bran market based on the below-mentioned segments:

Global Bran Market, By Source

- Wheat

- Rice

- Corn

- Barley

Global Bran Market, By Application

- Food

- Animal Feed

- Health & Wellness

Global Bran Market, By Distribution Channel

- B2B

- B2C

Global Bran Market, By Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa

Frequently Asked Questions (FAQ)

Q. What structural factors are driving the long-term expansion of the global bran market?

A. The market is expanding due to the convergence of rising health awareness, increasing demand for fiber-rich and functional foods, and the large-scale availability of bran as a by-product of global cereal production, which reached 3,023 million tonnes in 2025.

Q. How is the transition from feed-grade to value-added applications influencing market dynamics?

A. The market is shifting from low-value bulk applications such as animal feed toward high-value uses in nutraceuticals, bakery, and functional foods, driven by demand for clean-label, high-fiber ingredients and health-focused consumption patterns.

Q. What is the relationship between urbanization and bran consumption trends?

A. Increasing urbanization and changing dietary patterns are driving demand for convenient, processed, and health-oriented foods, leading to higher incorporation of bran in bakery, cereals, and packaged products.

Q. How do evolving consumer preferences influence product innovation in the bran market?

A. Rising demand for clean-label, organic, and high-fiber foods is driving innovation in bran-based ingredients, including gluten-free variants and fortified food products.

Check Licence

Choose the plan that fits you best: Single User, Multi-User, or Enterprise solutions tailored for your needs.

We Have You Covered

- 24/7 Analyst Support

- Clients Across the Globe

- Tailored Insights

- Technology Tracking

- Competitive Intelligence

- Custom Research

- Syndicated Market Studies

- Market Overview

- Market Segmentation

- Growth Drivers

- Market Opportunities

- Regulatory Insights

- Innovation & Sustainability

Report Details

| Scope | Global |

| Pages | 190 |

| Delivery | PDF & Excel via Email |

| Language | English |

| Release | Apr 2026 |

| Access | Download from this page |