Global Checkpoint Inhibitor Refractory Cancer Market

Global Checkpoint Inhibitor Refractory Cancer Market Size, Share, By Therapy (Immune Checkpoint Inhibitors, Combination Therapies, Targeted Therapies), By Cancer Type (Lung Cancer, Melanoma, Renal Cell Cancer, Urothelial Carcinoma), By Treatment Line (First-Line Treatment, Second-Line Treatment, Third-Line and Beyond), and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2025 - 2035

REPORT COVERAGE

Global

Market Snapshot

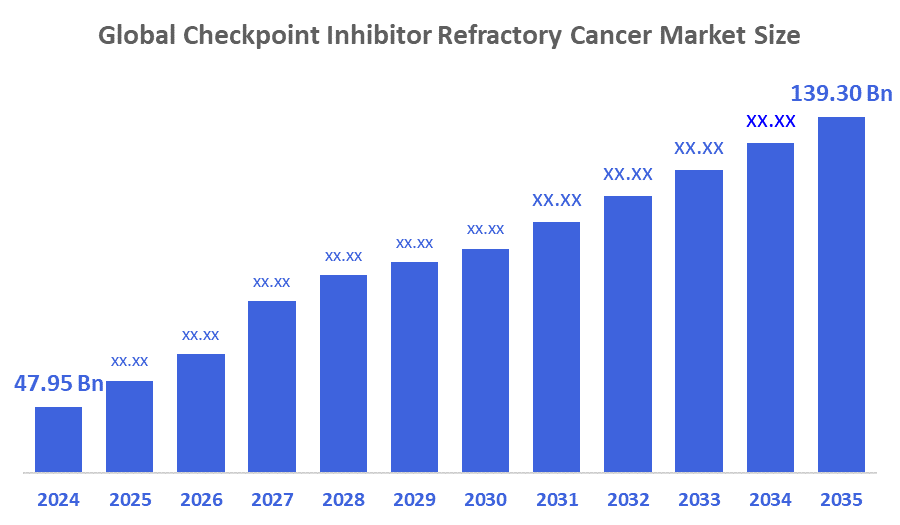

- Market Size (2025): USD 47.95 Billion

- Projected Market Size (2035): USD 139.30 Billion

- Compound Annual Growth Rate (CAGR): 11.25 %

- Largest Regional Market: North America

- Fastest Growing Region: Asia-Pacific

- 3rd Largest Region: Europe

- Base Year: 2025

- Historical Period: 2021–2024

- Forecast Period: 2026–2035

According to Decision Advisors, The Global Checkpoint Inhibitor Refractory Cancer Market Size is expected to Grow from USD 47.95 Billion in 2024 to USD 139.30 Billion by 2035, at a CAGR of 11.25 % during the forecast period 2025-2035. The Global Checkpoint Inhibitor Refractory Cancer Market is projected to grow significantly over the next decade, growth is fueled by increased clinical trials, novel combination therapies, rising cancer prevalence, high post-checkpoint failure demand, rising incidence of resistance, frontline adoption growth, pipeline innovation, modality shifts, and cell therapies.

Market Overview/ Introduction

The global market for checkpoint inhibitors for refractory cancer is growing rapidly as resistance to conventional immunotherapies becomes a major problem in oncology. Patients who do not react to first-line checkpoint inhibitors now have new hope thanks to tailored medicines that address refractory situations made possible by advances in our understanding of tumor immune evasion mechanisms. Pharmaceutical companies are concentrating on combination regimens and new targets outside of conventional pathways as a result of ongoing investment in clinical trials and biomarker-driven medication development. Because of the unmet clinical need and the considerable demand from oncologists for more effective choices, regulatory agencies are giving priority to rapid approvals in this area.

Expanding research into tumor microenvironment modulation, better patient stratification methods, and strategic partnerships between biotechnology companies and academic research centers that are paving the way for more long-lasting and individualized treatment solutions are all anticipated to benefit the market.

- The Ayushman Bharat Pradhan Mantri Jan Arogya Yojana (PM-JAY) provided ?5 lakh annual coverage per family for secondary and tertiary care across hospitals. It covered diagnostics, medicines, and hospitalization, including over 200 cancer treatment packages. The scheme supported advanced therapies, improving access and affordability, thereby indirectly contributing to growth in the checkpoint inhibitor refractory cancer market.

- The Health Minister’s Cancer Patient Fund (HMCPF) under the Rashtriya Arogya Nidhi (RAN) was established in 2009 to provide financial assistance to below-poverty-line cancer patients. It supported treatment at 27 Regional Cancer Centres, where revolving funds were created, and up to Rs. 50 lakhs were allocated to improve access to care.

- The Union Finance Minister revised customs duty rates on X-ray tubes and flat panel detectors, which were expected to positively impact the X-ray machine industry by lowering component costs. The NHM budget for FY 2024-25 was increased by approximately Rs 4,000 Cr, strengthening primary and secondary healthcare and reducing out-of-pocket expenditures.

Notable Insights: -

- North America holds the largest regional market share in the global checkpoint inhibitor refractory cancer market.

- Asia-Pacific is the fastest growing region in the global checkpoint inhibitor refractory cancer market.

- By therapy, the immune checkpoint inhibitors segment held a dominant position with over 54.35% in terms of market share in 2025.

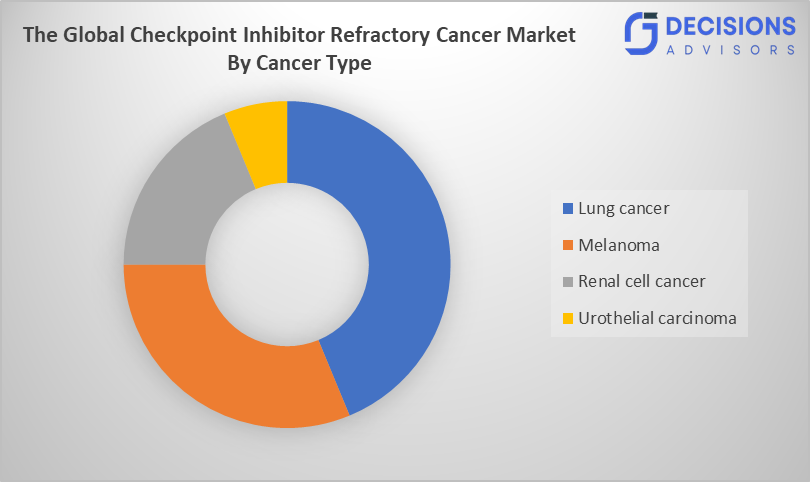

- By cancer type, lung cancer segment is the dominating accounting for over 38.70% of the global market share in 2025.

- The compound annual growth rate of the global checkpoint inhibitor refractory cancer market is 11.25 %.

- The market is likely to achieve a valuation of USD 139.30 billion by 2035.

What is role of technology in grooming the market?

Technology plays a pivotal role in shaping the global checkpoint inhibitor refractory cancer market by driving innovation, improving treatment precision, and accelerating drug development. Artificial intelligence (AI) and machine learning enable predictive modeling for therapy response, identifying patients likely to benefit from specific immunotherapies and detecting resistance mechanisms. Next-generation sequencing, molecular diagnostics, and biomarker profiling facilitate personalized treatments, optimizing outcomes for refractory patients. Advanced automation, digital pathology, and cloud-based data analytics streamline clinical trial design, patient monitoring, and real-time data integration. Additionally, telemedicine and digital platforms enhance patient access and follow-up care, expanding market reach while reducing operational costs and improving overall efficiency in delivering next-generation cancer therapies.

Market Drivers

The global checkpoint inhibitor refractory cancer market is propelled by the growing number of patients making progress following frontline immunotherapy, which is a significant accelerator, generating a pressing need for "salvage" treatments. Novel targets, including LAG-3, TIGIT, and TIM-3, are receiving a lot of funding in order to get around the immunosuppressive tumor microenvironment. By facilitating quicker approvals, simpler clinical trials, and clear routes for novel medicines, regulatory support is boosting the market for checkpoint inhibitor refractory cancer, increasing patient access and market expansion. More efficient patient categorization and customized treatment plans are made possible by the combination of cutting-edge biomarkers and AI-driven diagnostics. Current immune checkpoint inhibitors (ICIs) have a major drawback in that many patients either do not respond to anti-PD-1, anti-PD-L1, and anti-CTLA-4 drugs (primary resistance) or develop resistance over time (acquired resistance), which greatly increases the demand for alternative therapy.

Restrain

The checkpoint inhibitor refractory cancer market faces restraints from high treatment costs, limited patient access in low-income regions, and complex regulatory requirements. Additionally, adverse effects, variable patient responses, and challenges in managing resistance to immunotherapies slow adoption, potentially restricting market growth despite increasing demand for advanced cancer therapies.

Competitive Analysis:

The report offers the appropriate analysis of the key organizations/companies involved within the checkpoint inhibitor refractory cancer market, along with a comparative evaluation primarily based on their product of offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes product development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

Top Companies in Global Checkpoint Inhibitor Refractory Cancer Market

- Bristol?Myers Squibb

- Merck & Co.

- AstraZeneca

- Genentech / Hoffmann?La Roche

- Regeneron Pharmaceuticals

- Janssen Research and Development (J&J)

- 4D pharma plc

- 4SC AG

- OncoSec Medical

- Mirati Therapeutics

- Ascentage Pharma Group

- ENB Therapeutics

Government Initiatives

|

Country |

Key Government Initiatives |

|

UK |

The UK government unveiled the National Cancer Plan for England in February 2026 to modernize cancer services and accelerate access to innovative treatments. MHRA reforms introduced a fast-track route for early-phase clinical trials, enhancing the UK’s competitiveness in advanced oncology research. |

|

US |

The National Cancer Institute (NCI) received a $7.35 billion appropriation for FY 2026, up $128 million from 2025. A major portion supports the Cancer Moonshot, focusing on treatment resistance research and high-risk, high-reward immunology innovations. |

|

China |

China’s 15th Five-Year Plan (2026–2030) under the Healthy China initiative prioritizes cancer early detection and precision medicine. It promotes high-tech innovation, provides clearer regulatory pathways for first-in-class therapies, and integrates advanced biotechnology into the national healthcare system. |

Market Segmentation

The Checkpoint Inhibitor Refractory Cancer Market share is classified into therapy, cancer type, and treatment line

- The immune checkpoint inhibitors segment dominated the market in 2025 and is projected to grow at a substantial CAGR during the forecast period.

Based on the therapy, the checkpoint inhibitor refractory cancer market is divided into immune checkpoint inhibitors, combination therapies, and targeted therapies. Among these, the immune checkpoint inhibitors segment dominated over 54.35% the market in 2025 and is projected to grow at a substantial CAGR during the forecast period. It is driven by widespread adoption of PD-1, PD-L1, and CTLA-4 inhibitors like nivolumab and pembrolizumab. Despite resistance in some patients, ICIs remain the first-line immunotherapy, generating the largest revenue share, while combination and targeted therapies are rapidly growing.

- The lung cancer segment accounted for the largest share in 2025 and is anticipated to grow at a significant CAGR during the forecast period.

Based on the cancer type, the checkpoint inhibitor refractory cancer market is divided into lung cancer, melanoma, renal cell cancer, and urothelial carcinoma. Among these, the lung cancer segment accounted over 38.70% for the largest share in 2025, and is anticipated to grow at a significant CAGR during the forecast period. It is dominating due to its high global prevalence, extensive use of immunotherapies, and growing number of patients developing resistance to checkpoint inhibitors, driving demand for next-generation and combination treatments.

- The first-line treatment segment dominated the market in 2025, and is projected to grow at a substantial CAGR during the forecast period.

Based on the treatment line, the checkpoint inhibitor refractory cancer market is divided into first-line treatment, second-line treatment, third-line and beyond. Among these, the first-line treatment segment dominated the market in 2025 and is projected to grow at a substantial CAGR during the forecast period. In view of the widespread adoption of PD-1, PD-L1, and CTLA-4 inhibitors as initial therapy. Early intervention improves patient outcomes, reduces disease progression, and drives significant market demand.

Strategies to Implement for Growth of the Market in Non-Leading Regions

Growth in non-leading regions can be supported by companies that expand healthcare infrastructure by investing in oncology centers, diagnostic labs, and tertiary care facilities. Increasing awareness among physicians and patients about refractory cancers, early diagnosis, and molecular testing is essential. Collaborating with governments and insurance providers to include advanced therapies in reimbursement schemes can improve affordability. Conducting local clinical trials and population-specific research enhances regulatory approvals and treatment adoption. Strategic partnerships with regional biotech and pharmaceutical companies, combined with provider training programs, can further increase access, distribution, and utilization of next-generation immunotherapies in underserved markets.

Regional Segment Analysis of the Checkpoint Inhibitor Refractory Cancer Market

- North America (U.S., Canada, Mexico)

- Europe (Germany, France, U.K., Italy, Spain, Rest of Europe)

- Asia-Pacific (China, Japan, India, Rest of APAC)

- South America (Brazil and the Rest of South America)

- The Middle East and Africa (UAE, South Africa, Rest of MEA)

North America is anticipated to hold the largest share of the Checkpoint Inhibitor Refractory Cancer Market over the predicted timeframe.

North America is anticipated to hold the largest share of the checkpoint inhibitor refractory cancer market over the predicted timeframe. This market has a high prevalence of cancer, well?established healthcare and oncology infrastructure, and widespread adoption of immunotherapy and refractory treatment protocols. The U.S. leads in clinical research, reimbursement support, and rapid regulatory approvals, enabling early access to next?generation therapies and extensive treatment penetration

Asia Pacific is expected to grow at a rapid CAGR in the Checkpoint Inhibitor Refractory Cancer Market during the forecast period. Asia Pacific is expected to grow at a rapid CAGR in the Checkpoint Inhibitor Refractory Cancer Market during the forecast period, due to the region's high and growing cancer incidence, rising checkpoint inhibitor use, and developing healthcare infrastructure in important nations like China, India, and Japan. Higher market demand and acceptance are also being driven by government assistance, more access to cutting-edge therapies, and an increase in specialty care.

Europe is the 3rd largest region to grow in the Checkpoint Inhibitor Refractory Cancer Market during the region. Due to its established oncology infrastructure, adoption of guideline-based immunotherapy, and robust clinical trial participation in key nations like Germany, France, and the UK, Europe is anticipated to be the third-largest market in the Checkpoint Inhibitor Refractory Cancer Market. Despite differences in reimbursement between countries, these factors contribute to the increasing demand for advanced refractory cancer treatments.

Future Market Trends in Global Checkpoint Inhibitor Refractory Cancer Market: -

1. Rise of Next-Generation Immunotherapies

The rise of next-generation immunotherapies is driven by the high unmet need in patients who develop resistance to existing checkpoint inhibitors. Innovations like LAG-3, TIGIT, and bispecific antibodies aim to overcome immune evasion, improve efficacy, and reduce relapse rates. Combination therapies and advanced immune-modulating agents further enhance treatment options, fueling market growth in refractory cancers.

2. Precision Medicine & Biomarker-Driven Treatments

The growth of precision medicine and biomarker-driven treatments is fueled by the need to personalize therapy for checkpoint inhibitor–resistant cancers. Molecular profiling, genetic testing, and liquid biopsies help identify tumor-specific mutations and immune signatures, enabling tailored therapies. This approach improves response rates, reduces unnecessary treatments, and drives adoption of targeted, next-generation oncology drugs.

3. Predictive Modeling for Therapy Response

Predictive modeling for therapy response is growing due to the complexity of checkpoint inhibitor–resistant cancers. AI analyzes clinical, genomic, and treatment data to forecast patient outcomes and identify resistance mechanisms. This enables oncologists to adjust therapies proactively, improving response rates, minimizing ineffective treatments, and supporting the development of personalized, next-generation immunotherapies in refractory cancer management.

Recent Development

- In February 2026, ImmunityBio reported a 700% year-over-year revenue growth and expanded ANKTIVA approvals in lung cancer. The company established global commercial partnerships in 33 countries and implemented label expansion plans. These achievements increased patient access to advanced therapies, including those for checkpoint inhibitor–resistant cancers, and strengthened its presence in the global oncology market.

- In February 2026, the FDA fast-tracked several oncology drugs that addressed unmet medical needs in cancer treatment. These approvals targeted patients with resistant or refractory cancers, including those unresponsive to checkpoint inhibitors. The fast-track designation accelerated drug development, expanding therapeutic options and supporting growth in the checkpoint inhibitor refractory cancer market.

- In October 2025, Takeda entered a global strategic partnership with Innovent Biologics to strengthen its oncology pipeline with next-generation investigational medicines for the treatment of solid tumors. The collaboration focused on developing advanced therapies, including those for cancers resistant to checkpoint inhibitors, aiming to expand treatment options and accelerate drug development worldwide.

How is Recent Developments Helping the Market?

Checkpoint inhibitor refractory cancer market growth has been bolstered by recent breakthroughs that have increased therapeutic options and stimulated immunotherapy research. As resistance to current checkpoint inhibitors drives research and development of next-generation treatments that target different immune pathways and combination regimens, the market is expected to expand quickly. Faster commercialization of sophisticated medicines is made possible by regulatory support and expedited approval pathways, and a strong clinical pipeline of innovative medications is developing to treat refractory malignancies. Furthermore, the industry is positioned for substantial long-term expansion due to increased patient access and market demand brought about by greater immunotherapy use across cancer types, rising prevalence of advanced malignancies, and higher global healthcare spending.

Market Segment

This study forecasts revenue at global, regional, and country levels from 2020 to 2035. Decisions Advisors has segmented the Checkpoint Inhibitor Refractory Cancer Market based on the below-mentioned segments:

Global Checkpoint Inhibitor Refractory Cancer Market, By Therapy

- Immune Checkpoint Inhibitors

- Combination Therapies

- Targeted Therapies

Global Checkpoint Inhibitor Refractory Cancer Market, By Cancer Type

- Lung Cancer

- Melanoma

- Renal Cell Cancer

- Urothelial Carcinoma

Global Checkpoint Inhibitor Refractory Cancer Market, By Treatment Line

- First-Line Treatment

- Second-Line Treatment

- Third-Line and Beyond

Global Checkpoint Inhibitor Refractory Cancer Market, By Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa

Frequently Asked Questions (FAQ)

Q. What are the major challenges in developing therapies for checkpoint inhibitor refractory cancers?

A. Developing therapies for checkpoint inhibitor refractory cancers is challenging due to complex resistance mechanisms, tumor heterogeneity, limited predictive biomarkers, and the high cost of R&D. Additionally, designing effective combination regimens without increasing toxicity and managing patient safety in advanced stages hampers clinical success rates.

Q. How are combination therapies transforming treatment paradigms in refractory cancer care?

A. Combination therapies, such as pairing immune checkpoint inhibitors with targeted agents or novel immunomodulators, are transforming treatment by enhancing anti?tumor efficacy and overcoming resistance pathways. These approaches improve immune activation, extend survival, and broaden therapeutic options for patients who no longer respond to monotherapy.

Q. What role do clinical trial networks play in advancing the refractory cancer market?

A. Clinical trial networks accelerate innovation by enabling multi?center studies, rapid patient recruitment, and diverse data collection. They facilitate assessment of novel agents and combinations across populations, shorten development timelines, and provide critical evidence that supports regulatory approvals and treatment optimization.

Q. Why is patient stratification crucial for the success of refractory cancer therapies?

A. Patient stratification ensures that therapies are targeted to individuals most likely to benefit, reducing ineffective treatments and unnecessary toxicity. By using genomic and immune profiling, clinicians can identify specific resistance signatures, personalize regimens, and improve overall outcomes in refractory cancer management.

Check Licence

Choose the plan that fits you best: Single User, Multi-User, or Enterprise solutions tailored for your needs.

We Have You Covered

- 24/7 Analyst Support

- Clients Across the Globe

- Tailored Insights

- Technology Tracking

- Competitive Intelligence

- Custom Research

- Syndicated Market Studies

- Market Overview

- Market Segmentation

- Growth Drivers

- Market Opportunities

- Regulatory Insights

- Innovation & Sustainability

Report Details

| Scope | Global |

| Pages | 251 |

| Delivery | PDF & Excel via Email |

| Language | English |

| Release | Mar 2026 |

| Access | Download from this page |