China Semiconductor Device Market

China Semiconductor Device Market Size, Share, By Device Type (Discrete Semiconductors, Optoelectronics, Sensors and MEMS, Integreted Circuits) By Business Model (IDM, Design Vendor) and By End Use Industry (Automotive, Communication, Industrial, Computing/Data Storage, Data Center, AI, and Government), Analysis and Forecast 2025-2035

REPORT COVERAGE

country

Market Snapshot

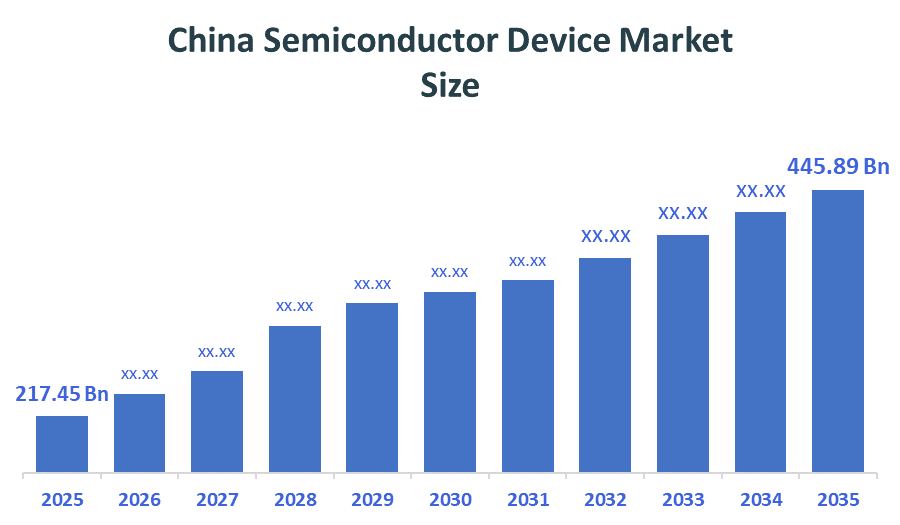

- Market Size (2025): USD 217.45 Billion

- Projected Market Size (2035): USD 445.89 Billion

- Compound Annual Growth Rate (CAGR): 7.45%

- Base Year: 2025

- Historical Period: 2021–2024

- Forecast Period: 2025–2035

According to Decision Advisors, the China Semiconductor Device Market Size is expected to grow from USD 217.45 Billion in 2024 to USD 445.89 Billion by 2035, at a CAGR of 7.45% during the forecast period 2025-2035. China semiconductor device market is projected to grow significantly over the next decade due to increasing demand for premium and craft alcoholic beverages, cocktail culture and experimental drinking, and rising disposable incomes worldwide, innovation in flavours and the drinking format.

Market Overview/Introduction

The China semiconductor device market, defined as the domestic production and consumption of semiconductor components including integrated circuits, discrete devices, sensors and power semiconductors across consumer, automotive, industrial and communications sectors, has shown robust expansion and strategic importance within the national economy. Chinese government initiatives are central to this growth, with heavy investment through the National Integrated Circuit Industry Investment Fund and mandates such as the 50?% domestic equipment usage rule to reduce foreign dependency and accelerate local semiconductor tool adoption. Regional incentives and industrial parks further support R&D, fabrication and ecosystem development. Domestic firms including SMIC, Huawei’s chip divisions and emerging design houses are scaling capacity and product portfolios, supported by implicit procurement policies that favor local technologies. Despite progress, China still lags in bleeding?edge nodes compared with global leaders, a gap that shapes strategic focus toward mature nodes, advanced packaging and compound semiconductors. Looking ahead, continued policy backing, rising localization, and technology diversification are expected to sustain mid?to?long?term growth, improve self?sufficiency and strengthen China’s position in the global semiconductor landscape through 2030.

Notable Insights: -

- By device type, the integrated segment held a dominant position with 14% in terms of market share in 2025.

- By business model, IDM segment is the dominating accounting for over 13% of the United Kingdom market share in 2025.

- The compound annual growth rate of the China semiconductor device market is 7.45%.

- The market is likely to achieve a valuation of USD 445.89 Billion by 2035.

What is role of technology in grooming the market?

The China semiconductor device market is being increasingly shaped by technological innovations that enhance both production and product performance. AI-assisted chip design, advanced lithography, and semiconductor automation streamline manufacturing, improving yields and lowering costs. Integration with IoT, cloud computing, and edge devices drives demand for high-performance, energy-efficient semiconductor. Data analytics and AI optimize supply chains, anticipate market demand, and refine production processes, while emerging technologies such as EUV lithography and advanced packaging techniques, including 2.5D and 3D ICs, enable greater miniaturization and performance. These advancements collectively strengthen competitiveness, support market growth, and facilitate rapid adaptation to evolving industry requirements.

Market Drivers

The China Semiconductor Device Market is driven by strong domestic demand for consumer electronics and automotive semiconductors, supported by government incentives and strategic investment funds aimed at achieving semiconductor self-sufficiency. China accounted for approximately 36.8% of global semiconductor consumption in 2025, reflecting robust internal demand. Adoption of emerging technologies such as 5G, AI, IoT, and industrial automation is accelerating, contributing to higher-value device requirements. Expansion of domestic chip design and fabrication capabilities, combined with strategic foreign partnerships, is strengthening the country’s competitive position. This region is expanding domestic semiconductor foundries and forming global technology partnerships, enhancing production capacity, accelerating innovation, improving supply chain resilience, and strengthening its semiconductor ecosystem to meet rising domestic and international demand.

Restrain

The China semiconductor device market faces challenges including high capital expenditure and long lead times for fabrication facilities, geopolitical tensions affecting equipment imports/exports, rapid technological obsolescence, intense competition, and supply chain volatility for critical materials such as silicon wafers and rare earth elements.

Strategies to Implement for Growth of the Market

To drive growth in the China semiconductor device market, companies should invest in expanding domestic wafer fabrication and advanced packaging capabilities, focusing on high-performance and specialty chips. Strategic partnerships and joint ventures with global technology providers can accelerate innovation and technology transfer. Adoption of AI, data analytics, and automation will optimize production, improve yield, and reduce operational costs. Expanding distribution channels, both domestically and internationally, will increase market penetration. Targeted R&D for emerging applications such as 5G, AI, EVs, and IoT devices can create high-value opportunities. Sustainable manufacturing practices and supply chain diversification further enhance resilience and long-term competitiveness.

Market Segmentation

The China Semiconductor Device Market share is classified into device type, business model, and end use industry.

- The integrated circuits segment dominated the market in 2024, and is projected to grow at a substantial CAGR of approximately 14% during the forecast period.

Based on the device type, the China semiconductor device market is divided into discrete semiconductors, optoelectronics, sensors and mems, integreted circuits. Among these, the integreted circuits segment dominated the market in 2024, and is projected to grow at a substantial CAGR of approximately 14% during the forecast period. This is because it is driven by its essential role in consumer electronics, automotive systems, industrial automation, and emerging technologies like 5G, AI, and IoT, which require high-performance logic and memory chips for widespread applications

- The IDM segment accounted for the largest share in 2024, and is anticipated to grow at a significant CAGR of approximately 13% during the forecast period.

Based on the business model, the China semiconductor device market is divided into IDM, design vendor. Among these, the IDM segment accounted for the largest share in 2024, and is anticipated to grow at a significant CAGR of approximately 13% during the forecast period. It is dominating due to its end-to-end capabilities in design, fabrication, and testing, large-scale manufacturing capacity, diversified customer base across electronics, automotive, and industrial sectors, government support, and reliable supply chains, ensuring sustained market leadership and growth

- The automotive segment dominated the market in 2024, and is projected to grow at a substantial CAGR during the forecast period.

Based on the end use industry, the China semiconductor device market is divided into automotive, communication, industrial, computing/data storage, data center, ai, and government. Among these, the automotive segment dominated the market in 2024, and is projected to grow at a substantial CAGR during the forecast period. This is a result of the increasing adoption of electric vehicles, advanced driver-assistance systems (ADAS), and smart mobility solutions, which require high-performance semiconductors such as power ICs, sensors, and microcontrollers, ensuring strong demand and substantial market share.

Recent Development

- In March 2026, Huawei launched the 950PR AI chip in China, enhancing domestic semiconductor device capabilities, supporting AI applications, and advancing local self-sufficiency in integrated circuits and data-center solutions.

- In March 2026, STMicroelectronics launched locally produced STM32 microcontrollers in China via Huahong partnership, strengthening domestic semiconductor device production, supporting industrial and consumer applications, and advancing local supply chain self-sufficiency.

- In October?2025, SiCarrier’s subsidiary Qiyunfang launched domestically developed EDA software, enhancing China’s semiconductor device design ecosystem and advancing local semiconductor self?sufficiency efforts in chip design tools.

Competitive Analysis

The report offers the appropriate analysis of the key organizations/companies involved within the China semiconductor device market, along with a comparative evaluation primarily based on their product of offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes product development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

Top Key Companies in China Semiconductor Device Market

• Semiconductor Manufacturing International Corp (SMIC)

• HiSilicon Technologies Co., Ltd

• Tsinghua Unigroup

• Yangtze Memory Technologies Co., Ltd

• Beijing Junzheng Electronics Co., Ltd

• Others

Key Target Audience

- Semiconductor Manufacturers

- Electronics OEMs

- Investors and Venture Capitalists

- Government Authorities

- Research & Consulting Firms

- Component Distributors

Market Segment

This study forecasts revenue at the China, regional, and country levels from 2020 to 2035. Spherical Insights has segmented the China semiconductor device market based on the below-mentioned segments

China Semiconductor Device Market, By Device Type

- Discrete Semiconductors

- Optoelectronics

- Sensors and MEMS

- Integreted Circuits

China Semiconductor Device Market, By Business Model

- IDM

- Design Vendor

China Semiconductor Device Market, By End Use Industry

- Automotive

- Communication

- Consumer

- Industrial

- Computing/Data Storage

- Data Center

- AI

- Government

Frequently Asked Questions (FAQ)

Q. How are global supply chain disruptions affecting China’s semiconductor device production?

A. Supply chain disruptions, such as shortages of advanced lithography equipment and raw materials like silicon wafers, have increased production costs, caused delays, and incentivized China to accelerate domestic manufacturing capabilities and local sourcing strategies.

Q. Which emerging technologies are likely to drive the next wave of semiconductor demand in China?

A. Technologies such as 5G networks, AI, electric vehicles (EVs), industrial automation, IoT, and cloud computing are expected to significantly increase demand for high-performance logic, memory, and power semiconductors.

Q. How does government policy influence foreign investment in China’s semiconductor sector?

A. Government policies, including subsidies, tax incentives, and strategic funding programs, encourage foreign companies to invest in domestic fabs, R&D centers, and joint ventures, strengthening technology transfer and domestic production capacity.

Q. What strategies are leading Chinese fabless companies using to compete with IDMs domestically and internationally?

A. Fabless companies focus on advanced chip design, specialization in niche applications, partnerships with foundries, IP licensing, and innovation in AI, IoT, and automotive semiconductors to compete with vertically integrated IDMs.

Check Licence

Choose the plan that fits you best: Single User, Multi-User, or Enterprise solutions tailored for your needs.

We Have You Covered

- 24/7 Analyst Support

- Clients Across the Globe

- Tailored Insights

- Technology Tracking

- Competitive Intelligence

- Custom Research

- Syndicated Market Studies

- Market Overview

- Market Segmentation

- Growth Drivers

- Market Opportunities

- Regulatory Insights

- Innovation & Sustainability

Report Details

| Scope | country |

| Pages | 210 |

| Delivery | PDF & Excel via Email |

| Language | English |

| Release | Apr 2026 |

| Access | Download from this page |