Global Chip Inductor Market

Global Chip Inductor Market Size, Share, By Type (Winding Type, Laminated Type, Film Type, Weaving Type, and Others) By Application (Communication Systems, Consumer Electronics, Automotive Electronics, Industrial Equipment, Power Supply Systems, and Others) By End User (Consumer Electronics Industry, Automotive Industry, Telecommunications Sector, Industrial Sector, and Healthcare Sector) and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa), Analysis and Forecast 2026 ? 2035

CAGR

6.43%

REVENUE 2025

USD Billion 5.93

FORECAST 2035

USD Billion 11.06

REPORT COVERAGE

Global

Market Snapshot

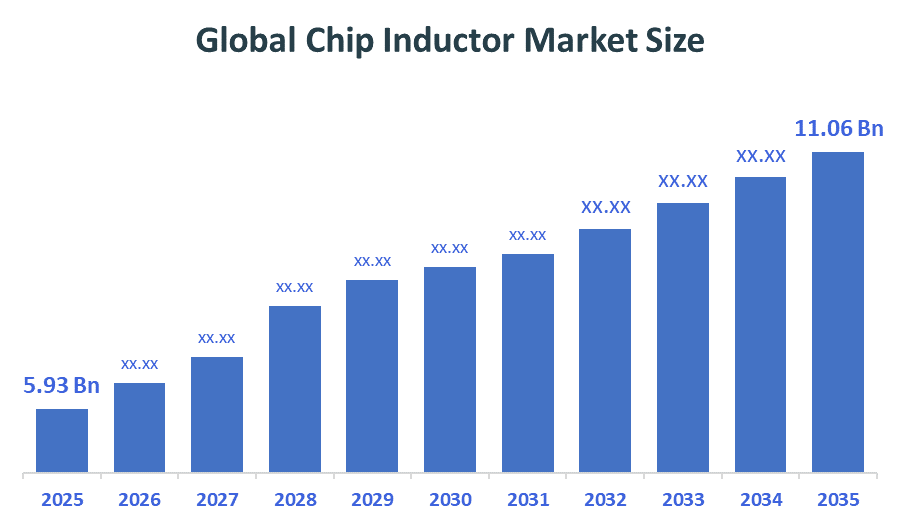

- Global Chip Inductor Market Size (2025): USD 5.93 Billion

- Global Chip Inductor Projected Market Size (2035): USD 11.06 Billion

- Global Chip Inductor Compound Annual Growth Rate (CAGR): 6.43%

- Largest Regional Market: Asia-Pacific

- Fastest Growing Region: North America

- 3rd Largest Region: Europe

- Base Year: 2025

- Historical Period: 2021–2024

- Forecast Period: 2026–2035

According to Decision Advisors, the global chip inductor market size was expected to grow from USD 5.93 billion in 2025 to USD 11.06 billion by 2035, with a CAGR of 6.43% during the forecast period from 2026 to 2035. The segment is showing steady growth owing to the growing need for efficient electronic elements for modern telecommunication systems and automobiles around the world, which has been largely driven by the growing requirement of 5G Advanced systems and the quick electrification of transportation systems. Thanks to the recent innovations in terms of metal composite core technologies as well as thin film manufacturing processes, these elements have become efficient enough to ensure thermal efficiency and reduced power losses in the process, effectively acting as a bridge between the conventional wire-wound components and the stringent needs of the new generation devices.

Market Overview / Introduction

Chip inductors form an important category of passive electrical elements that are engineered to regulate energy immediately by storing it magnetically in a small circuit layout. These devices function as an essential link between conventional bulky coils and highly dense semiconductor technologies through their use of multi-layered, wire wound, and thin-film designs. Current flows continuously in a chip inductor without taking up much of the board space thanks to innovative characteristics such as metal-composite cores and non-magnetic ceramic substrates that ensure continuous functioning while minimizing electromagnetic interference and energy losses at high frequencies. Although originally designed as a coil made of insulated copper wires, chip inductors have become complex independent platforms defined by high Q-factor values, thermal stability, and SMT assembly compatibility. The main contributor to the increasing popularity of the Global Chip Inductor Market stems from the high demand for the construction of 5G-Advanced networks and real-time data processing applications in consumer electronics and automotive modules. In recent years, several governmental interventions like the India Semiconductor Mission 2.0 and the US CHIPS and Science Act of 2026 have been launched to offer immense financial incentives for domesticating the semiconductor production pipeline and achieving 2-nanometer nodes. These policies have a profound impact, ensuring structural reliability and supply chain security as global manufacturers seek to maintain constant hardware protection and performance efficiency without relying on the volatile lead times associated with legacy component sourcing.

- Asia-Pacific holds approximately 48% of global revenue, supported by massive electronics manufacturing hubs in China, South Korea, and Japan.

- Consumer electronics and mobile communication applications account for nearly 43% of total demand, driven by the increasing use of multilayer chip inductors in 5G-Advanced smartphones, wearable IoT devices.

Notable Insights: -

- Ferrite core chip inductors make up about 55.2% of the total market share in this sector. They have gained a reputation for high efficiency in power supply operations, particularly in DC-DC converters and EMI filtering.

- About 34.4% of all installations occur in consumer electronics and mobile communication devices. These investments are stimulated mainly by high levels of integration in 5G-Advanced smartphones and wearable tech.

- Applications of chip inductors in the automotive electronics sphere account for almost 25.8% of all demand. The rapid development of electric vehicles (EVs) and autonomous driving systems, alongside increased focus on vehicle-to-everything (V2X) communication, has become one of the main drivers for using high-reliability, automotive-grade inductors.

- About 48% of the market value belongs to the Asia-Pacific region in 2026. Many countries within this region, like China, South Korea, and Japan, invest considerable amounts of money in semiconductor fabrication and electronic assembly to address the global demand for next-generation hardware and telecommunications infrastructure.

- Automotive-grade chip inductor systems show an annual increase above 5.8%.

What is the Role of Technology in Shaping the Market?

Progress in technology has led to revolutionary changes in the area of the chip inductor industry with innovations in areas like miniature components, frequency responses, and automation in regard to production accuracy. The modern induction devices are not simply passive inductors but more complex power management and signal filtering circuits that can function efficiently even at GHz frequencies because they can integrate high-grade metal compound cores, thin film deposition, and surface mount technology assembly lines.

How are Recent Developments Helping the Market?

These emerging trends, which include the implementation of nanocrystalline cores, thin-film high-performance copper traces, and three-dimensional embedded inductors, have been instrumental in helping drive growth within the market. There have been advancements within the market for chip inductors with platform technologies that allow these products to accommodate various hardware requirements, including those found in low-power wearable devices and high-power automotive power modules, operating efficiently under extreme temperature variations without losing energy. By relying on moulded metal alloy structures, they will be capable of automatically handling high saturation currents to sustain their magnetic field and prevent acoustic noises or core saturations.

Market Drivers

The global market for chip inductors is expanding in line with the rising capital expenditure by technology manufacturers and government organisations in sustainable semiconductor infrastructures and fast communication protocols to ensure adherence to the 5G and 6G adaptation standards. Modern-day inductors have acquired significant popularity in the market, benefiting from their ability to combine various capabilities, including ultra-low direct current resistance, instant frequency transitions, and extremely low-profile configurations, within a single robust and energy-efficient framework. Conversely, the rising trend of on-device artificial intelligence has increased the need for reliable power supply mechanisms that can facilitate the shift towards edge computing in smartphones or areas where the deployment of conventional bulkier inductors is being constrained by space limitations.

Restraints

The growth of the international market for the chip inductor is constrained by the difficulty of achieving stable material supply chains, such as high-purity copper and ferrite powder materials, because of the existence of volatility in pricing and trade worldwide. Furthermore, the expenses incurred during the manufacture of unique high-permeability alloys and the fabrication process in cleanrooms, as well as the costs associated with EMI shielding, make it difficult for small-scale electronic component suppliers to adopt the technology quickly.

Competitive Analysis:

The report offers the appropriate analysis of the key organisations/companies involved within the chip inductor market, along with a comparative evaluation primarily based on their product offerings, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborate analysis focusing on the current news and developments of the companies, which includes product development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

Top 10 Companies in the Global Chip Inductor Market

- TDK Corporation

- Murata Manufacturing Co., Ltd.

- Taiyo Yuden Co., Ltd.

- Vishay Intertechnology, Inc.

- Samsung Electro-Mechanics

- Chilisin Electronics Corp. (Yageo Group)

- Sumida Corporation

- Shenzhen Sunlord Electronics Co., Ltd.

- Coilcraft, Inc.

- Bourns, Inc.

Government Initiatives

|

Country |

Key Government Initiatives |

|

US |

The SEMI U.S. Policy Strategy emphasised strengthening semiconductor supply chain resilience by building on the CHIPS and Science Act, which allocated over 52 billion dollars to boost domestic manufacturing and research. The strategy prioritises expanding support to materials, components, and packaging suppliers, along with coordinated export control policies and R and D incentives to secure advanced semiconductor technologies. |

|

India |

Under the Union Budget 2026–27, the Government of India launched India Semiconductor Mission 2.0 with an estimated program outlay of around ?8,000 crores, while allocating about ?1,000 crores for FY 2026–27. The initiative focuses on strengthening domestic production of semiconductor equipment and materials, supporting the broader electronics ecosystem including passive components such as chip inductors. |

|

South Korea |

The Government of South Korea introduced a semiconductor ecosystem support package worth approximately 26 trillion to strengthen the entire chip value chain, including materials, equipment, and infrastructure. The program includes around 17 trillion in financial support and nearly 5 trillion for research and development through 2027, along with plans to develop large scale semiconductor clusters with improved power and water infrastructure. |

Study on the Supply, Demand, Distribution, and Market Environment

The success of the chip inductor manufacturing industry is contingent on striking the optimal balance between the capacity to function at its peak potential concerning electromagnetic efficacy and the emerging necessity of uninterrupted power regulation enabled by artificial intelligence. The supply chain involves a concerted effort aimed at the production of highly pure ferrite powder and extremely efficient metal composite cores that will enable instant energy storage without the unnecessary operational delays experienced in traditional wound wire designs. On the other hand, the demand factor is derived from the shift towards a more resilient 5G-Advanced system framework, the incorporation of advanced RF modules within communications devices responsible for signal filtering and voltage stabilisation, as well as ensuring structural efficacy within areas experiencing extreme miniaturisation demands. Delivery of goods is facilitated through mutually beneficial semiconductor distribution agreements, extensive automotive electronics programs, and collaborative ventures with global consumer electronics and telecommunications networks.

Price Analysis and Consumer Behaviour Analysis

The price range of the chip inductor differs according to the type of mounting, saturation current capacity, and high-frequency operation features. High-quality chip inductors with the use of thin film deposition technology, along with advanced magnetic shielding and extremely low DC resistance, cost more. Nevertheless, shield less multilayer chip inductors and smaller ferrite beads for regular consumer electronics are cheaper and constitute an excellent choice for providing local supplementary signal filtering and short-term power regulation services in confined electronic environments. Buyers have made their stance clear by opting for products that are cost-effective in the long run and can withstand heat; therefore, manufacturers should concentrate on creating products that offer operational independence, easy surface mount compatibility, and accurate inductance positioning for extended periods.

Market Segmentation

The Global Chip Inductor Market share is classified into product type, application, and end user.

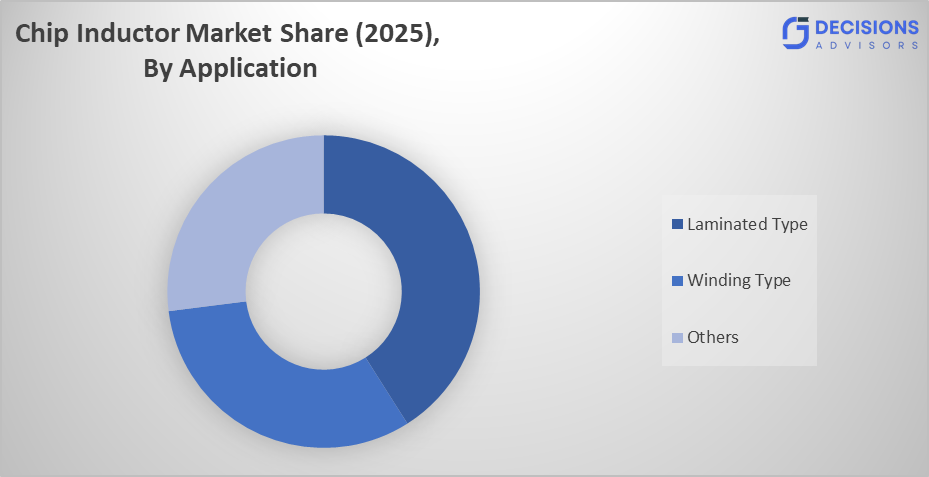

The Laminated Type segment holds the largest share, contributing approximately 41% of the market in 2025.

Based on the product type, the global chip inductor market is divided into winding type, laminated type, film type, weaving type, and others. Among these, the laminated type segment holds the largest share, contributing approximately 41% of the market in 2025. Their superiority is attributed to the high reliability of their compact design and high-frequency operation in processing signals in contemporary mobile phones without the need for large coils. The winding and film types are the other two major categories of the market that have continued to maintain relevance in the market because of their ability to carry huge currents and their role in RF filtering.

The Consumer Electronics segment accounts for the largest share, representing over 37% of the global market in 2025.

Based on the Application, the global chip inductor market is divided into communication systems, consumer electronics, automotive electronics, industrial equipment, power supply systems, and others. Among these, the consumer electronics segment accounts for the largest share, representing over 37% of the global market in 2025. These deployments are critical for maintaining the efficiency of 5G-Advanced mobile devices, improving battery life resilience, and reducing hardware heat dissipation through the adoption of modern, autonomous power management equipment. On the other hand, the Automotive Electronics segment has emerged as a rapidly growing application, thanks to the increasing construction of high-value electric vehicle (EV) powertrains and the refurbishment of advanced driver assistance systems (ADAS) in next-generation vehicles.

The telecommunications sector dominates the global market, accounting for approximately 49% of the total revenue in 2025.

Based on the End User, the global chip inductor market is divided into the consumer electronics industry, the automotive industry, the telecommunications sector, the industrial sector, and the healthcare sector. Among these, the Telecommunications Sector dominates the global market, accounting for approximately 49% of the total revenue in 2025. This segment is preferred by planners who require large-scale integrated solutions and professional engineering services for complex 5G and 6G infrastructure. The Automotive Industry category is seeing a sharp increase in use, especially by manufacturers in major automotive hubs who value the thermal stability and the convenience of high-reliability component protection for battery management systems and autonomous sensors.

Strategies to Implement for Growth of the Market in Non-Leading Regions

The ability to foster further development in the market for chip inductors in new geographic areas can be enhanced by the implementation of an effective modular power management system among local smartphone manufacturers and regional authorities responsible for overseeing telecommunications infrastructure management. Initiatives focused on the establishment of 5G-Advanced capabilities among governments in addition to the development of high-reliability standards in semiconductor fabrication, have made important contributions to demand generation in regions that present difficulties in placing high-frequency base stations in the region. Additional efforts to enhance training programs for local material science technicians and semiconductor testing centres will ensure more sustainable procurement and smart hardware responses.

Regional Segment Analysis of the Global Chip Inductor Market

- North America (U.S., Canada, Mexico)

- Europe (Germany, France, U.K., Italy, Spain, Rest of Europe)

- Asia-Pacific (China, Japan, India, South Korea, Rest of APAC)

- Latin America (Brazil and the Rest of Latin America)

- The Middle East and Africa (UAE, South Africa, Rest of MEA)

Asia-Pacific is projected to be the fastest-growing region over the forecast period. This region is anticipated to witness a growth rate of around 7.2% CAGR, maintaining a dominant market share within the global industry. In 2025, the Asia-Pacific region will already account for approximately 42.6% of global revenue. This is owing to the fast-developing consumer electronics manufacturing infrastructure, coupled with the growing demand for modern power management in countries such as China, India, and South Korea. Other reasons for the same include greater investments made toward sustainable 5G-Advanced scaling in the region, state-supported indigenous research and development projects for low-cost passive components, and widespread adoption of metal composite-based energy control strategies.

North America is expected to hold a significant share of the chip inductor market during the forecast period. This region holds approximately 24.2% share of global revenue in 2025, thanks to its highly sophisticated infrastructure related to aerospace and defense, along with the extensive adoption of AI-native hardware in both national data centre goals and high-value automotive security applications. The largest part of this region’s revenues comes from the United States, as there is a lot of spending at the government level in semiconductor fabrication assistance programs like the CHIPS Act for automated component adoption, along with local research related to sensor-integrated thin-film systems. Over-the-horizon upgrades to automotive safety codes and the early adoption of smart-connected systems in industrial retrofit operations have played key roles here.

Europe is anticipated to hold a substantial share, contributing approximately 19.3% of the global market share. There is a competitive advantage in the region owing to clusters of automotive technology innovation and financing for sustainable electrification of the environment, as well as high-reliability industrial automation research. There is also a comparative advantage with countries like Germany, France, and Italy, which are highly skilled at precision engineering for high-performance automotive-grade inductors. Moreover, the rigorous regulatory standards that they have regarding carbon neutrality and urban energy efficiency further give them a comparative advantage. The presence of big manufacturing firms, along with improved hardware reliability systems, has also helped introduce advanced chip inductors slowly but steadily.

Recent Developments

- In March 2026, leading companies such as Murata Manufacturing Co., Ltd. and TDK Corporation entered a new pricing cycle for passive components, with reported price increases exceeding 100% in certain inductor categories due to rising raw material costs and strong demand from AI infrastructure and automotive electronics sectors.

- In March 2026, the Government of India announced plans for a new semiconductor support fund of approximately 11 billion dollars to strengthen domestic chip manufacturing, with the broader semiconductor market expected to approach nearly 100 billion dollars over the next decade, significantly boosting demand for passive components such as chip inductors used in AI, telecom, and automotive electronics.

- In December 2025, under the Semicon India Programme, the Government of India approved 10 semiconductor projects with a total investment of about ?1.6 lakh crore, covering fabrication, packaging, and testing facilities, directly supporting the ecosystem for electronic components, including chip inductors used in consumer electronics and industrial applications.

- In September 2025, the Government of India launched fiscal incentives targeting semiconductor usage across 25 categories of electronics, alongside a ?1,000 crore design-linked incentive scheme supporting 23 chip design projects.

- In September 2025, the Government of India initiated the Semicon India Programme with an overall allocation of ?76,000 crores, of which nearly ?65,000 crores has already been committed, aiming to build a complete semiconductor ecosystem, including design, manufacturing, and packaging that supports the growth of chip inductor demand across multiple industries.

Market Segmentation

This study forecasts revenue at global, regional, and country levels from 2021 to 2035. Decisions Advisors segmented the global chip inductor market based on the following categories:

Global Chip Inductor Market, By Type

- Winding Type

- Laminated Type

- Film Type

- Weaving Type

- Others

Global Chip Inductor Market, By Application

- Communication Systems

- Consumer Electronics

- Automotive Electronics

- Industrial Equipment

- Power Supply Systems

- Others

Global Chip Inductor Market, By End User

- Consumer Electronics Industry

- Automotive Industry

- Telecommunications Sector

- Industrial Sector

- Healthcare Sector

Global Chip Inductor Market, By Regional Analysis

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- United Arab Emirates

- Saudi Arabia

- Qatar

- South Africa

- Rest of Middle East & Africa

Frequently Asked Questions (FAQ)

What is a chip inductor, and why is it important?

A chip inductor is a specialised passive electronic component designed to regulate current flow and filter electromagnetic interference by storing energy within a compact magnetic field. These components are essential for maintaining signal integrity and power efficiency in modern high-density circuit boards, protecting sensitive semiconductors from current fluctuations and ensuring operational stability in high-frequency environments.

What factors are driving the growth of the chip inductor market?

The market growth can be attributed to the massive investments made in 5G and 6G infrastructure by telecommunications agencies, the rising requirements for efficient power delivery in AI-native hardware, and the widespread adoption of high-reliability automotive-grade components.

Which product type dominates the chip inductor market?

Laminated type (multilayer) chip inductors represent the largest and most influential segment of the market due to their exceptional ultra-compact footprints, the capability to handle high-frequency signals, and their versatility in adapting to various surface-mount technology (SMT) assembly lines.

Which applications are widely used in this market?

Communication systems and consumer electronics are the most prominent applications due to the acute necessity to maintain stable signal transmission and provide reliable power regulation for high-speed processors and RF modules.

Check Licence

Choose the plan that fits you best: Single User, Multi-User, or Enterprise solutions tailored for your needs.

We Have You Covered

- 24/7 Analyst Support

- Clients Across the Globe

- Tailored Insights

- Technology Tracking

- Competitive Intelligence

- Custom Research

- Syndicated Market Studies

- Market Overview

- Market Segmentation

- Growth Drivers

- Market Opportunities

- Regulatory Insights

- Innovation & Sustainability

Report Details

| Scope | Global |

| Pages | 210 |

| Delivery | PDF & Excel via Email |

| Language | English |

| Release | Apr 2026 |

| Access | Download from this page |