Global Circuit Material Market

Global Circuit Material Market Size, Share, By Material Type (Copper, Aluminum, Gold, Silver, Graphene), By Manufacturing Process (Subtractive Manufacturing, Additive Manufacturing, Hybrid Manufacturing), By Application (Consumer Electronics, Automotive, Telecommunications, Healthcare, Industrial) and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East & Africa), Analysis and Forecast 2025-2035

REPORT COVERAGE

Global

Market Snapshot

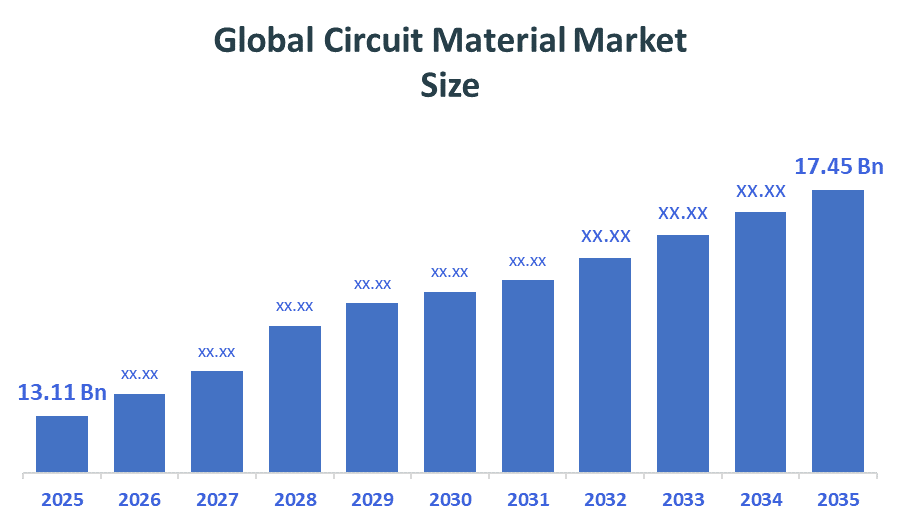

- Market Size (2025): USD 13.11 Billion

- Projected Market Size (2035): USD 17.45 Billion

- Compound Annual Growth Rate (CAGR): 2.9%

- Largest Regional Market: Asia Pacific

- Fastest Growing Region: North America

- 3rd Largest Region: Europe

- Base Year: 2025

- Historical Period: 2021–2024

- Forecast Period: 2026–2035

According to Decision Advisors, the Global Circuit Material Market Size is expected to grow from USD 13.11 billion in 2025 to USD 17.45 billion by 2035, at a CAGR of 2.9% during the forecast period 2026-2035. The global circuit material market is projected to grow significantly over the next decade. The market is expanding due to increasing adoption of targeted biologics, rising prevalence of chronic diseases, advancements in antibody engineering technologies, growing demand for personalized medicine, and increasing approvals of monoclonal antibody therapies.

Market Overview/ Introduction

The circuit materials market refers to the industry involved in the production and supply of materials such as copper, laminates, resins, and substrates used in printed circuit boards (PCBs) and electronic components. The market is witnessing steady growth due to increasing demand for consumer electronics, electric vehicles, telecommunications infrastructure, and industrial automation. Government initiatives supporting semiconductor manufacturing and electronics production, particularly in regions like North America, Europe, and Asia Pacific, are accelerating market expansion through funding, incentives, and supply chain development programs. Companies are focusing on innovations such as high-frequency laminates, flexible substrates, and sustainable materials to meet evolving performance and environmental requirements. The market offers advantages including high scalability, strong integration with growing electronics industries, and continuous technological advancements. Future growth is expected to be driven by rising adoption of 5G/6G technologies, AI-driven systems, and next-generation computing, along with increasing investments in advanced semiconductor and PCB manufacturing globally.

Notable Insights: -

- Asia Pacific is anticipated to hold the largest share of 57% in the circuit material market over the predicted timeframe.

- North America is expected to grow at a rapid CAGR in the circuit material market during the forecast period.

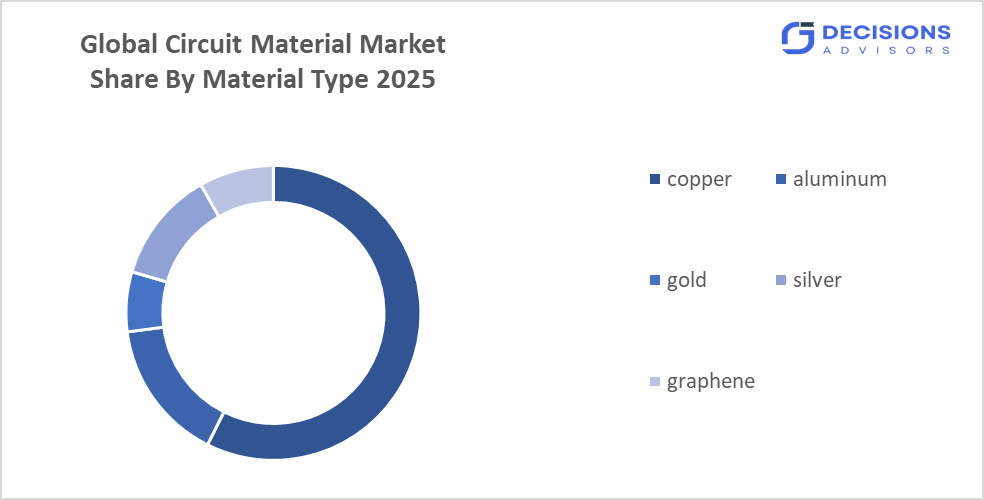

- By material type, the copper segment dominated the market in 2025 with a share of 65% and is projected to grow at a substantial CAGR during the forecast period.

- By application, the consumer electronics segment dominated the market in 2025 with a share of 48%, and is projected to grow at a substantial CAGR during the forecast period.

- The compound annual growth rate of the global circuit material market is 2.9%.

- The market is likely to achieve a valuation of USD 17.45 billion by 2035.

What is role of technology in grooming the market?

Technological advancements are transforming the circuit materials market by improving electrical conductivity, thermal stability, and miniaturization capabilities. High-frequency materials and advanced laminates enhance signal integrity while reducing energy loss in modern electronics. Flexible substrates support compact and wearable device designs. AI-driven material design and precision manufacturing increase production efficiency and reduce defects. Additionally, the development of sustainable and recyclable materials helps meet environmental regulations. Smart materials with embedded sensing features improve reliability and performance in critical applications such as automotive electronics, telecommunications, and aerospace systems, thereby expanding the overall scope and efficiency of next-generation electronic solutions.

Market Drivers

The circuit materials market is driven by increasing demand for advanced electronics such as smartphones, wearables, and IoT devices, which require high-performance and miniaturized components. The rapid growth of automotive electrification and electric vehicles is further boosting demand for advanced printed circuit materials to support complex electronic systems. Expansion of 5G and next-generation network infrastructure is accelerating the need for high-frequency, low-loss materials. Additionally, rising adoption of industrial automation and aerospace electronics is contributing to market growth, as these sectors require reliable, durable, and high-efficiency circuit materials for critical and high-performance applications.

Restrain

The circuit materials market faces challenges from raw material price volatility, which increases production costs and affects profitability. Supply chain disruptions and complexities can limit material availability and delay production timelines. Additionally, stringent environmental regulations and recycling difficulties for advanced composite materials create compliance challenges, requiring continuous innovation and sustainable material development.

Competitive Analysis:

The report offers the appropriate analysis of the key organizations/companies involved within the circuit material market, along with a comparative evaluation primarily based on their product of offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes product development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

Top Companies in the Global Circuit Material Market

- Rogers Corporation

- Shengyi Technology Co Ltd

- Kingboard Laminates Holdings Ltd

- Mitsubishi Materials Corporation

- Panasonic Corporation

- DuPont de Nemours Inc

- Isola Group Ltd

- Eternal Materials Co Ltd

- Taiflex Scientific Co Ltd

- Nikkan Industries Co Ltd

Government Initiatives

|

Country |

Key Government Initiatives |

|

US |

The CHIPS and Science Act, a key U.S. strategy, allocates 53?billion to boost domestic semiconductor manufacturing, research, and workforce development, aiming to reduce dependence on foreign supply chains and strengthen local production. |

|

Europe |

Germany plans approximately 20?billion for semiconductor projects with Intel, Infineon, and TSMC, while France’s Electronique?2030 initiative aims to expand domestic chip production and strengthen its semiconductor industry. |

|

China |

China launched Big Fund?III, a 47?billion National Integrated Circuit Industry Investment Fund, focusing on AI chips, memory technology, and supply chain improvements, boosting domestic semiconductor production and circuit material demand. |

Study on the Supply, Demand, Distribution, and Market Environment of Global Circuit Material Market

The global circuit materials market supply chain comprises raw material suppliers (copper, resins, substrates), material manufacturers, PCB producers, and OEMs. Demand is driven by consumer electronics, automotive electronics, telecommunications, and industrial applications requiring high-performance materials. Distribution occurs through direct OEM contracts, specialized distributors, and global electronics supply networks. The market environment is shaped by rapid technological advancements, strict quality standards, and environmental regulations. Increasing investments in semiconductor and electronics manufacturing, along with growing demand for high-frequency and miniaturized components, are strengthening market expansion. However, supply chain disruptions and raw material cost fluctuations continue to influence overall market stability.

Price Analysis and Consumer Behaviour Analysis

Price analysis in the circuit materials market shows that raw materials are the dominant cost driver, typically accounting for 30 to 50% of total production cost, with many estimates clustering around 35–45%. In some cases, raw material contribution can reach approximately 60%, especially in simpler circuit structures. Copper-clad laminates alone contribute approximately 27–40% of total cost, making them the single largest component. Additional factors influencing pricing include layer count, manufacturing processes, and drilling/finishing costs. Consumer behaviour prioritizes performance, durability, and thermal efficiency over price, with buyers willing to pay premiums for high-frequency and sustainable materials.

Market Segmentation

The circuit material market share is classified into material type, manufacturing process and application

- The copper segment dominated the market in 2025 with a share of 65% and is projected to grow at a substantial CAGR during the forecast period.

Based on the material type, the circuit material market is divided into copper, aluminum, gold, silver, graphene. Among these, copper segment dominated the market in 2025 with a share of 65% and is projected to grow at a substantial CAGR during the forecast period. This dominance is driven by its high electrical conductivity, excellent thermal performance, cost-effectiveness, and ease of processing, making it ideal for large-scale PCB manufacturing and reliable electronic signal transmission across applications.

- The subtractive manufacturing segment accounted for the largest share in 2025, and is anticipated to grow at a significant CAGR during the forecast period.

Based on the manufacturing process, the circuit material market is divided into subtractive manufacturing, additive manufacturing, hybrid manufacturing. Among these, the subtractive manufacturing segment accounted for the largest share in 2025, and is anticipated to grow at a significant CAGR during the forecast period. This dominance is because of its well-established infrastructure, proven reliability, and compatibility with existing PCB production systems. It offers high precision, scalability, and cost efficiency for mass production. Additionally, industry familiarity, standardized processes, and consistent quality output make it the preferred choice over emerging additive and hybrid manufacturing technologies.

- The consumer electronics segment dominated the market in 2025 with a share 48%, and is projected to grow at a substantial CAGR during the forecast period.

Based on application, the circuit material market is divided into consumer electronics, automotive, telecommunications, healthcare, industrial. Among these, the consumer electronics segment dominated the market in 2025 with a share of 45%, and is projected to grow at a substantial CAGR during the forecast period. The dominance is due to massive global demand for smartphones, laptops, tablets, and wearable devices. Continuous product innovation, shorter replacement cycles, and increasing penetration of IoT devices drive high-volume PCB production. Additionally, miniaturization and advanced functionality requirements significantly increase the consumption of circuit materials across this segment.

Strategies to Implement for Growth of the Market in Non-Leading Regions

Growth in non-leading regions of the circuit materials market can be driven through strategic investments in local manufacturing and supply chain development to reduce dependency on imports and lower costs. Establishing partnerships with global electronics and semiconductor companies enables technology transfer and enhances production capabilities. Governments can support growth through incentives, subsidies, and favorable policies for electronics manufacturing. Adoption of advanced and sustainable materials ensures compliance with global standards and improves competitiveness. Workforce development and technical training are essential to build skilled labor. Expanding demand from emerging sectors such as electric vehicles, telecommunications, and industrial automation further supports sustainable market penetration and long-term growth. (Brazil and the Rest of South America)

- The Middle East and Africa (UAE, South Africa, Rest of MEA)

Regional Segment Analysis of the Circuit Material Market

- North America (U.S., Canada, Mexico)

- Europe (Germany, France, U.K., Italy, Spain, Rest of Europe)

- Asia-Pacific (China, Japan, India, Rest of APAC)

- South America

Asia Pacific is anticipated to hold the largest share of the circuit material market over the predicted timeframe.

Asia Pacific is anticipated to hold the largest share of the circuit materials market, accounting for approximately 57% of the global market during the forecast period. This dominance is driven by the region’s strong electronics manufacturing base in China, Japan, South Korea, and Taiwan, which are global hubs for semiconductor and PCB production. High demand from consumer electronics, automotive electronics, and telecommunications industries further strengthens market growth. Additionally, cost-effective manufacturing, availability of raw materials, skilled labor, and supportive government policies promoting electronics and semiconductor industries contribute to sustained regional leadership and continuous expansion.

North America is expected to grow at a rapid CAGR in the circuit material market during the forecast period.

North America is expected to grow at a rapid CAGR in the circuit materials market during the forecast period due to increasing investments in semiconductor manufacturing and advanced electronics. Government initiatives supporting domestic chip production and supply chain resilience are accelerating regional growth. Rising demand from electric vehicles, AI systems, and high-performance computing further boosts the need for advanced circuit materials. Additionally, strong presence of key technology companies, continuous R&D activities, and adoption of high-frequency and high-reliability materials in telecommunications and aerospace sectors contribute to sustained market expansion and technological advancement across the region.

Europe is the 3rd largest region to grow in the circuit material market during the period.

Europe is the third-largest region in the circuit materials market, supported by strong demand from automotive electronics, industrial automation, and aerospace sectors. The region benefits from advanced manufacturing capabilities and strict quality and environmental regulations. Increasing investments in electric vehicles, renewable energy systems, and semiconductor production are further driving demand. Additionally, Europe’s focus on sustainable materials and circular economy practices supports steady growth and innovation in circuit materials.

Future Market Trends in the Global Circuit Material Market: -

- Shift toward advanced and nano-engineered materials

Advanced materials such as graphene, gallium nitride, and nano-composites are increasingly adopted to enhance electrical conductivity, thermal stability, and signal performance. These materials support miniaturization and high-power applications, particularly in EVs, high-frequency electronics, and semiconductor packaging, improving overall device efficiency and reliability in next-generation electronic systems.

- Growing demand for flexible and high-frequency materials

Flexible and high-frequency materials are gaining importance due to rising demand for compact, lightweight, and high-speed electronic devices. Applications in wearables, IoT devices, and 5G/6G infrastructure require materials with low signal loss, high flexibility, and durability, enabling efficient performance in dynamic and space-constrained environments. Adoption of smart packaging with tracking and monitoring technologies

- Sustainability and recyclable material adoption

Sustainability trends are driving the adoption of eco-friendly, recyclable, and low-toxicity circuit materials. Regulatory pressures and environmental concerns are encouraging manufacturers to develop biodegradable substrates and reduce hazardous substances, supporting circular economy goals while maintaining performance, compliance, and long-term cost efficiency in electronics manufacturing.

Recent Development

- In November?2025, India approved 17 electronics component manufacturing projects worth ?7,172?crores under the Electronics Component Manufacturing Scheme to boost domestic production and reduce import dependency.

- In April 2025, Rogers Corporation launched next-generation high-frequency laminates for 5G infrastructure and automotive radar, featuring high thermal stability and low dielectric loss, enhancing performance in advanced circuit material applications.

- In March 2025, Advanced Chip and Circuit Materials launched the "Celeritas Series" laminates and prepregs, enabling PCIe Gen?6/7 speeds up to 224?Gb/s for AI and HPC multilayer PCBs.

- In January 2024, Jiva Materials developed Soluboard, a water?soluble, recyclable PCB laminate that replaces fiberglass epoxy, aiming to drastically reduce PCB e?waste and improve sustainability in circuit materials.

How is Recent Developments Helping the Market?

Recent developments in the circuit materials market are improving performance, reliability, and sustainability across applications. Advancements in high-frequency and thermally stable materials enhance signal integrity and support next-generation electronics. The adoption of flexible substrates enables compact and lightweight device designs. AI-driven material development and precision manufacturing improve efficiency and reduce defects. Additionally, increasing focus on eco-friendly and recyclable materials helps companies meet regulatory requirements and sustainability goals. These developments are strengthening supply chains, enabling innovation, and expanding applications in automotive electronics, telecommunications, industrial automation, and consumer electronics, thereby supporting steady market growth.

Market Segment

This study forecasts revenue at global, regional, and country levels from 2020 to 2035. Decision Advisors has segmented the circuit material market based on the below-mentioned segments:

Global Circuit Material Market, By Material Type

- Copper

- Aluminum

- Gold

- Silver

- Graphene

Global Circuit Material Market, By Manufacturing Process

- Subtractive Manufacturing

- Additive Manufacturing

- Hybrid Manufacturing

Global Circuit Material Market, By Application

- Consumer Electronics

- Automotive

- Telecommunications

- Healthcare

- Industrial

Global Circuit Material Market, By Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa

Frequently Asked Questions (FAQ)

Q. How will quantum computing influence circuit material requirements?

A. Quantum systems require ultra-low-loss, cryogenic-compatible materials with exceptional signal stability, driving development of specialized substrates and superconducting-compatible circuit materials.

Q. What is the impact of extreme operating environments on material innovation?

- Aerospace and defense applications require materials resistant to radiation, temperature extremes, and mechanical stress, leading to innovation in high-reliability circuit materials.

Q. What role does thermal management play in next-generation circuit materials?

A. Efficient heat dissipation is critical for high-power electronics, driving innovation in materials with superior thermal conductivity to prevent overheating and ensure device longevity.

Q. What impact does high-speed data transmission have on material innovation?

A. Increasing data speeds require materials with low signal attenuation and minimal interference, driving demand for advanced substrates and high-frequency laminates.

- Introduction

- Objectives of the Study

- Market Definition

- Research Scope

- Research Methodology and Assumptions

- Executive Summary

- Premium Insights

- Porter’s Five Forces Analysis

- Value Chain Analysis

- Top Investment Pockets

- Market Attractiveness Analysis By Material Type

- Market Attractiveness Analysis By Manufacturing Process

- Market Attractiveness Analysis By Application

- Market Attractiveness Analysis By Region

- Industry Trends

- Market Dynamics

- Market Evaluation

- Drivers

- Increase in health consciousness

- Restraints

- Strict adherence to regulations required for sugar substitute products

- Opportunities

- Increased investment in R&D activities by manufacturers

- Challenges

5.5.1. Product labeling and claims issues

- Global Circuit Material Market Analysis and Projection, By Material Type

- Segment Overview

- Copper

- Aluminum

- Gold

- Silver

- Graphene

- Global Circuit Material Market Analysis and Projection, By Manufacturing Process

- Segment Overview

- Subtractive Manufacturing

- Additive Manufacturing

- Hybrid Manufacturing

- Global Circuit Material Market Analysis and Projection, By Application

- Segment Overview

- Consumer Electronics

- Automotive

- Telecommunications

- Healthcare

- Industrial

- Global Circuit Material Market Analysis and Projection, By Regional Analysis

- Segment Overview

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Asia-Pacific

- Japan

- China

- India

- South America

- Brazil

- Middle East and Africa

- UAE

- South Africa

- Global Circuit Material Market-Competitive Landscape

- Overview

- Market Share of Key Players in the Circuit Material Market

- Global Company Market Share

- North America Company Market Share

- Europe Company Market Share

- APAC Company Market Share

- Competitive Situations and Trends

- Coverage Launches and Developments

- Partnerships, Collaborations, and Agreements

- Mergers & Acquisitions

- Expansions

- Company Profiles

- Rogers Corporation

- Business Overview

- Company Snapshot

- Company Market Share Analysis

- Company Coverage Portfolio

- Recent Developments

- SWOT Analysis

- Shengyi Technology Co Ltd

- Business Overview

- Company Snapshot

- Company Market Share Analysis

- Company Coverage Portfolio

- Recent Developments

- SWOT Analysis

- Kingboard Laminates Holdings Ltd

- Business Overview

- Company Snapshot

- Company Market Share Analysis

- Company Coverage Portfolio

- Recent Developments

- SWOT Analysis

- Mitsubishi Materials Corporation

- Business Overview

- Company Snapshot

- Company Market Share Analysis

- Company Coverage Portfolio

- Recent Developments

- SWOT Analysis

- Panasonic Corporation

- Business Overview

- Company Snapshot

- Company Market Share Analysis

- Company Coverage Portfolio

- Recent Developments

- SWOT Analysis

- DuPont de Nemours Inc

- Business Overview

- Company Snapshot

- Company Market Share Analysis

- Company Coverage Portfolio

- Recent Developments

- SWOT Analysis

- Isola Group Ltd

- Business Overview

- Company Snapshot

- Company Market Share Analysis

- Company Coverage Portfolio

- Recent Developments

- SWOT Analysis

- Eternal Materials Co Ltd

- Business Overview

- Company Snapshot

- Company Market Share Analysis

- Company Coverage Portfolio

- Recent Developments

- SWOT Analysis

- Taiflex Scientific Co Ltd

- Business Overview

- Company Snapshot

- Company Market Share Analysis

- Company Coverage Portfolio

- Recent Developments

- SWOT Analysis

- Nikkan Industries Co Ltd

- Business Overview

- Company Snapshot

- Company Market Share Analysis

- Company Coverage Portfolio

- Recent Developments

- SWOT Analysis

- Rogers Corporation

List of Table

- Global Circuit Material Market, By Material Type, 2024-2035(USD Billion)

- Global Copper, Circuit Material Market, By Region, 2024-2035(USD Billion)

- Global Aluminum, Circuit Material Market, By Region, 2024-2035(USD Billion)

- Global Gold, Circuit Material Market, By Region, 2024-2035(USD Billion)

- Global Silver, Circuit Material Market, By Region, 2024-2035(USD Billion)

- Global Graphene, Circuit Material Market, By Region, 2024-2035(USD Billion)

- Global Circuit Material Market, By Manufacturing Process, 2024-2035(USD Billion)

- Global Subtractive Manufacturing, Circuit Material Market, By Region, 2024-2035(USD Billion)

- Global Additive Manufacturing, Circuit Material Market, By Region, 2024-2035(USD Billion)

- Global Hybrid Manufacturing, Circuit Material Market, By Region, 2024-2035(USD Billion)

- Global Circuit Material Market, By Application, 2024-2035(USD Billion)

- Global Consumer Electronics, Circuit Material Market, By Region, 2024-2035(USD Billion)

- Global Automotive, Circuit Material Market, By Region, 2024-2035(USD Billion)

- Global Telecommunications, Circuit Material Market, By Region, 2024-2035(USD Billion)

- Global Healthcare, Circuit Material Market, By Region, 2024-2035(USD Billion)

- Global Industrial, Circuit Material Market, By Region, 2024-2035(USD Billion)

- North America Circuit Material Market, By Material Type, 2024-2035(USD Billion)

- North America Circuit Material Market, By Manufacturing Process, 2024-2035(USD Billion)

- North America Circuit Material Market, By Application, 2024-2035(USD Billion)

- U.S. Circuit Material Market, By Material Type, 2024-2035(USD Billion)

- U.S. Circuit Material Market, By Manufacturing Process, 2024-2035(USD Billion)

- U.S. Circuit Material Market, By Application, 2024-2035(USD Billion)

- Canada Circuit Material Market, By Material Type, 2024-2035(USD Billion)

- Canada Circuit Material Market, By Manufacturing Process, 2024-2035(USD Billion)

- Canada Circuit Material Market, By Application, 2024-2035(USD Billion)

- Mexico Circuit Material Market, By Material Type, 2024-2035(USD Billion)

- Mexico Circuit Material Market, By Manufacturing Process, 2024-2035(USD Billion)

- Mexico Circuit Material Market, By Application, 2024-2035(USD Billion)

- Europe Circuit Material Market, By Material Type, 2024-2035(USD Billion)

- Europe Circuit Material Market, By Manufacturing Process, 2024-2035(USD Billion)

- Europe Circuit Material Market, By Application, 2024-2035(USD Billion)

- Germany Circuit Material Market, By Material Type, 2024-2035(USD Billion)

- Germany Circuit Material Market, By Manufacturing Process, 2024-2035(USD Billion)

- Germany Circuit Material Market, By Application, 2024-2035(USD Billion)

- France Circuit Material Market, By Material Type, 2024-2035(USD Billion)

- France Circuit Material Market, By Manufacturing Process, 2024-2035(USD Billion)

- France Circuit Material Market, By Application, 2024-2035(USD Billion)

- U.K. Circuit Material Market, By Material Type, 2024-2035(USD Billion)

- U.K. Circuit Material Market, By Manufacturing Process, 2024-2035(USD Billion)

- U.K. Circuit Material Market, By Application, 2024-2035(USD Billion)

- Italy Circuit Material Market, By Material Type, 2024-2035(USD Billion)

- Italy Circuit Material Market, By Manufacturing Process, 2024-2035(USD Billion)

- Italy Circuit Material Market, By Application, 2024-2035(USD Billion)

- Spain Circuit Material Market, By Material Type, 2024-2035(USD Billion)

- Spain Circuit Material Market, By Manufacturing Process, 2024-2035(USD Billion)

- Spain Circuit Material Market, By Application, 2024-2035(USD Billion)

- Asia Pacific Circuit Material Market, By Material Type, 2024-2035(USD Billion)

- Asia Pacific Circuit Material Market, By Manufacturing Process, 2024-2035(USD Billion)

- Asia Pacific Circuit Material Market, By Application, 2024-2035(USD Billion)

- Japan Circuit Material Market, By Material Type, 2024-2035(USD Billion)

- Japan Circuit Material Market, By Manufacturing Process, 2024-2035(USD Billion)

- Japan Circuit Material Market, By Application, 2024-2035(USD Billion)

- China Circuit Material Market, By Material Type, 2024-2035(USD Billion)

- China Circuit Material Market, By Manufacturing Process, 2024-2035(USD Billion)

- China Circuit Material Market, By Application, 2024-2035(USD Billion)

- India Circuit Material Market, By Material Type, 2024-2035(USD Billion)

- India Circuit Material Market, By Manufacturing Process, 2024-2035(USD Billion)

- India Circuit Material Market, By Application, 2024-2035(USD Billion)

- South America Circuit Material Market, By Material Type, 2024-2035(USD Billion)

- South America Circuit Material Market, By Manufacturing Process, 2024-2035(USD Billion)

- South America Circuit Material Market, By Application, 2024-2035(USD Billion)

- Brazil Circuit Material Market, By Material Type, 2024-2035(USD Billion)

- Brazil Circuit Material Market, By Manufacturing Process, 2024-2035(USD Billion)

- Brazil Circuit Material Market, By Application, 2024-2035(USD Billion)

- The Middle East and Africa Circuit Material Market, By Material Type, 2024-2035(USD Billion)

- The Middle East and Africa Circuit Material Market, By Manufacturing Process, 2024-2035(USD Billion)

- The Middle East and Africa Circuit Material Market, By Application, 2024-2035(USD Billion)

- UAE Circuit Material Market, By Material Type, 2024-2035(USD Billion)

- UAE Circuit Material Market, By Manufacturing Process, 2024-2035(USD Billion)

- UAE Circuit Material Market, By Application, 2024-2035(USD Billion)

- South Africa Circuit Material Market, By Material Type, 2024-2035(USD Billion)

- South Africa Circuit Material Market, By Manufacturing Process, 2024-2035(USD Billion)

- South Africa Circuit Material Market, By Application, 2024-2035(USD Billion)

List of Figures

- Global Circuit Material Market Segmentation

- Circuit Material Market: Research Methodology

- Market Size Estimation Methodology: Bottom-Up Approach

- Market Size Estimation Methodology: Top-down Approach

- Data Triangulation

- Porter’s Five Forces Analysis

- Value Chain Analysis

- Top investment pocket in the Circuit Material Market

- Top Winning Strategies, 2024-2035

- Top Winning Strategies, By Development, 2024-2035(%)

- Top Winning Strategies, By Company, 2024-2035

- Moderate Bargaining power of Buyers

- Moderate Bargaining power of Suppliers

- Moderate Bargaining power of New Entrants

- Low threat of Substitution

- High Competitive Rivalry

- Top Player Positioning, 2024

- Market Share Analysis, 2024

- Restraint and Drivers: Circuit Material Market

- Circuit Material Market Segmentation, By Material Type

- Circuit Material Market For Copper, By Region, 2024-2035 ($ Billion)

- Circuit Material Market For Aluminum, By Region, 2024-2035 ($ Billion)

- Circuit Material Market For Gold, By Region, 2024-2035 ($ Billion)

- Circuit Material Market For Silver, By Region, 2024-2035 ($ Billion)

- Circuit Material Market For Graphene, By Region, 2024-2035 ($ Billion)

- Circuit Material Market Segmentation, By Manufacturing Process

- Circuit Material Market For Subtractive Manufacturing, By Region, 2024-2035 ($ Billion)

- Circuit Material Market For Additive Manufacturing, By Region, 2024-2035 ($ Billion)

- Circuit Material Market For Hybrid Manufacturing, By Region, 2024-2035 ($ Billion)

- Circuit Material Market Segmentation, By Application

- Circuit Material Market For Consumer Electronics, By Region, 2024-2035 ($ Billion)

- Circuit Material Market For Automotive, By Region, 2024-2035 ($ Billion)

- Circuit Material Market For Telecommunications, By Region, 2024-2035 ($ Billion)

- Circuit Material Market For Healthcare, By Region, 2024-2035 ($ Billion)

- Circuit Material Market For Industrial, By Region, 2024-2035 ($ Billion)

- Rogers Corporation: Net Sales, 2024-2035 ($ Billion)

- Rogers Corporation: Revenue Share, By Segment, 2024 (%)

- Rogers Corporation: Revenue Share, By Region, 2024 (%)

- Shengyi Technology Co Ltd: Net Sales, 2024-2035 ($ Billion)

- Shengyi Technology Co Ltd: Revenue Share, By Segment, 2024 (%)

- Shengyi Technology Co Ltd: Revenue Share, By Region, 2024 (%)

- Kingboard Laminates Holdings Ltd: Net Sales, 2024-2035 ($ Billion)

- Kingboard Laminates Holdings Ltd: Revenue Share, By Segment, 2024 (%)

- Kingboard Laminates Holdings Ltd: Revenue Share, By Region, 2024 (%)

- Mitsubishi Materials Corporation: Net Sales, 2024-2035 ($ Billion)

- Mitsubishi Materials Corporation: Revenue Share, By Segment, 2024 (%)

- Mitsubishi Materials Corporation: Revenue Share, By Region, 2024 (%)

- Panasonic Corporation: Net Sales, 2024-2035 ($ Billion)

- Panasonic Corporation: Revenue Share, By Segment, 2024 (%)

- Panasonic Corporation: Revenue Share, By Region, 2024 (%)

- DuPont de Nemours Inc: Net Sales, 2024-2035 ($ Billion)

- DuPont de Nemours Inc: Revenue Share, By Segment, 2024 (%)

- DuPont de Nemours Inc: Revenue Share, By Region, 2024 (%)

- Isola Group Ltd: Net Sales, 2024-2035 ($ Billion)

- Isola Group Ltd: Revenue Share, By Segment, 2024 (%)

- Isola Group Ltd: Revenue Share, By Region, 2024 (%)

- Eternal Materials Co Ltd: Net Sales, 2024-2035 ($ Billion)

- Eternal Materials Co Ltd: Revenue Share, By Segment, 2024 (%)

- Eternal Materials Co Ltd: Revenue Share, By Region, 2024 (%)

- Taiflex Scientific Co Ltd.: Net Sales, 2024-2035 ($ Billion)

- Taiflex Scientific Co Ltd.: Revenue Share, By Segment, 2024 (%)

- Taiflex Scientific Co Ltd.: Revenue Share, By Region, 2024 (%)

- Nikkan Industries Co Ltd: Net Sales, 2024-2035 ($ Billion)

- Nikkan Industries Co Ltd: Revenue Share, By Segment, 2024 (%)

- Nikkan Industries Co Ltd: Revenue Share, By Region, 2024 (%)

Check Licence

Choose the plan that fits you best: Single User, Multi-User, or Enterprise solutions tailored for your needs.

We Have You Covered

- 24/7 Analyst Support

- Clients Across the Globe

- Tailored Insights

- Technology Tracking

- Competitive Intelligence

- Custom Research

- Syndicated Market Studies

- Market Overview

- Market Segmentation

- Growth Drivers

- Market Opportunities

- Regulatory Insights

- Innovation & Sustainability

Report Details

| Scope | Global |

| Pages | 210 |

| Delivery | PDF & Excel via Email |

| Language | English |

| Release | Apr 2026 |

| Access | Download from this page |