Global Clinical Workflow Solutions Market

Global Clinical Workflow Solutions Market Size, Share, By Type (Data Integration Solutions, Care Collaboration Solutions, Workflow Automation Solutions, Enterprise Reporting & Analytics, and Others), By Delivery Mode (On-Premise, Cloud-Based, and Web-Based), By End-User (Hospitals, Clinics, Ambulatory Care Centers, and Others) and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2025 ? 2035

REPORT COVERAGE

Global

Market Snapshot

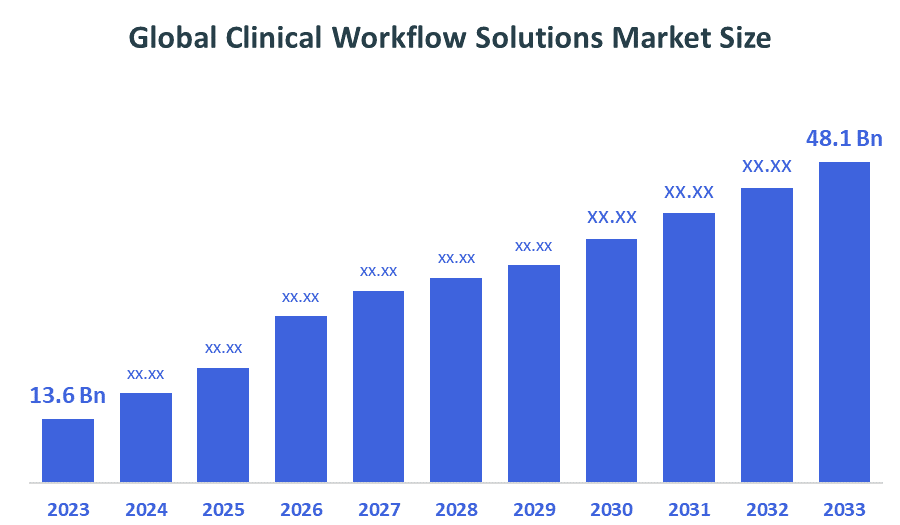

- Market Size (2025): USD 13.6 Billion

- Projected Market Size (2035): USD 48.1 Billion

- Compound Annual Growth Rate (CAGR): 13.46%

- Largest Regional Market: North America

- Fastest Growing Region: Asia Pacific

- 3rd Largest Region: Europe

- Base Year: 2025

- Historical Period: 2021–2024

- Forecast Period: 2025–2035

According to Decision Advisors, the Global Clinical Workflow Solutions Market Size is expected to grow from USD 13.6 billion in 2025 to USD 48.1 billion by 2035, at a CAGR of 13.47% during the forecast period 2025-2035. The clinical workflow solutions market is expanding rapidly due to the increasing need for healthcare efficiency, rising patient volumes, and the growing adoption of digital healthcare technologies. Clinical workflow solutions help streamline administrative and clinical processes, reduce errors, and enhance patient outcomes, which is driving their adoption globally.

Market Overview/ Introduction

The global clinical workflow solutions market is essentially the digital nervous system of modern medicine, defined as a sophisticated suite of integrated platforms designed to orchestrate the complex flow of data, tasks, and communication between healthcare providers and patients. The movement to improve healthcare technology is getting a boost from government programs like the U.S. Promoting Interoperability and Digital Health Rules in the European Union. These programs encourage hospitals to get rid of systems that do not work well together and switch to new systems that can share information easily. Big companies like Oracle, Philips and GE HealthCare are helping to make this happen by adding artificial intelligence and predictive analytics to the tools that doctors use every day. The goal of healthcare technology is to fix a problem that doctors face, which is called alert fatigue and burnout. Healthcare technology, like this, can really help doctors do their jobs better. Looking ahead, the future of the market lies in the transition from simple data management to intelligent orchestration, where automated workflows will anticipate patient needs before they become emergencies, turning hospitals into highly efficient, tech-empowered healing environments.

- Oracle Health (Cerner Corporation) is a leading global clinical workflow solutions provider, generating over $5.8 billion in revenue from its health segment. Its portfolio includes electronic health records (EHR), care coordination, and workflow automation solutions, strengthening its position in the global clinical workflow solutions market

- The Office of the National Coordinator for Health Information Technology (ONC) continues to promote digital healthcare adoption and interoperability standards. According to ONC, 96% of non-federal acute care hospitals in the U.S. have adopted certified EHR systems, accelerating demand for clinical workflow solutions.

- Ayushman Bharat Digital Mission (ABDM/NDHM) is driving healthcare digitization in India by creating a unified digital health ecosystem, including health IDs and interoperable records, supporting workflow optimization and data integration.

Notable Insights: -

- North America holds the largest regional market share in the global clinical workflow solutions market.

- Asia Pacific is the fastest-growing region in the global workflow clinical solutions market.

- By type, workflow automation solutions dominated market share in 2025.

- By end-user, hospitals accounted dominant share in the market in 2025.

- The compound annual growth rate of the global workflow clinical solutions market is 13.46%.

- The market is likely to achieve a valuation of USD 48.1 billion by 2035.

What is role of technology in grooming the market?

Technology plays a crucial role in shaping the clinical workflow solutions market by enhancing efficiency, accuracy, and patient care outcomes. Artificial intelligence and machine learning are increasingly used to automate repetitive tasks, support clinical decision-making, and predict patient outcomes. Healthcare providers using AI-enabled workflow systems have reported improvement in operational efficiency. Cloud computing is transforming the industry by enabling real-time data access, scalability, and cost-effective deployment. Additionally, interoperability technologies are ensuring seamless data exchange across systems, improving care coordination. The integration of IoT devices and wearable technologies further supports remote patient monitoring and real-time clinical insights.

How is Recent Developments Helping the Market?

Recent developments such as digital transformation initiatives, increasing adoption of telehealth, and advancements in AI-driven healthcare solutions are significantly boosting the market. In 2024, over 60% of hospitals globally adopted digital workflow solutions, reflecting strong demand for automation and efficiency. The rise of telemedicine has increased the need for integrated workflow systems to manage virtual consultations and patient data. Additionally, partnerships between healthcare IT companies and hospitals are accelerating innovation. Governments worldwide are also promoting healthcare digitization, further supporting market growth.

Market Drivers

The global clinical workflow solutions market is driven by the increasing burden on healthcare systems, rising patient volumes, and the growing need to reduce operational inefficiencies. The adoption of electronic health records and digital healthcare systems has significantly increased the demand for workflow optimization tools. In the United States, over 90% of hospitals have adopted EHR systems, creating a strong foundation for workflow solution integration. Additionally, the global shortage of healthcare professionals is driving demand for automation tools that reduce administrative workload. The shift toward value-based care and patient-centric healthcare models is also encouraging healthcare providers to adopt advanced workflow systems to improve quality and efficiency.

Restrain

The global clinical workflow solutions market is restrained by high implementation costs, data privacy concerns, lack of interoperability in legacy systems, and resistance to change among healthcare professionals. Additionally, cybersecurity risks and regulatory challenges may hinder market growth.

Competitive Analysis:

The report offers the appropriate analysis of the key organizations/companies involved within the clinical workflow solutions market, along with a comparative evaluation primarily based on their product of offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes product development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

Top Companies in Global Workflow Clinical Solutions Market

- Cerner Corporation

- McKesson Corporation

- Allscripts Healthcare Solutions

- Koninklijke Philips N.V.

- GE Healthcare

- Siemens Healthineers

- Epic Systems Corporation

- Athenahealth

- NXGN Management LLC

- eClinicalWorks

Government Initiatives

|

Country |

Key Government Initiatives |

|

UK |

The NHS Long Term Plan prioritizes digital transformation to address waiting lists and workforce shortages. Specific funding includes dollar 225 million for digital mental health and musculoskeletal initiatives. The Clinical Research, Resilience, Recovery, and Growth (RRG) program further invests in digitizing clinical research delivery to enhance the UK's capacity for cutting-edge research. |

|

US |

Initiatives focus on the effective usage of interoperability standards (like HL7 FHIR) and EHR integration. There is a strong emphasis on adopting AI-driven tools, such as ambient AI and generative AI, to automate documentation and reduce physician burnout |

|

China |

Digital health is a core pillar of the Healthy China 2030 Initiative. The government has transitioned from basic informatization to big data and internet-based healthcare. Strategies like Made in China 2025 and the latest Five-Year Plan provide substantial funding for technology development and industrial upgrading in healthcare. |

Market Segmentation

The workflow clinical solutions market share is classified into type, delivery mode, and end user.

- The workflow automation solutions segment dominated the market in 2025 and is projected to grow at a substantial CAGR during the forecast period.

Based on the type, the clinical workflow solutions market is divided into data integration solutions, care collaboration solutions, workflow automation solutions, enterprise reporting & analytics, and others. Among these, the workflow automation solutions segment dominated the market in 2025 and is projected to grow at a substantial CAGR during the forecast period. This dominance is strongly supported by the widespread adoption of digital health systems globally. For instance, according to the Centers for Disease Control and Prevention, nearly 95% of office-based physicians in the United States had adopted electronic health record (EHR) systems as of 2024, highlighting the strong digital foundation supporting workflow automation adoption. The supermarkets and hypermarkets segment accounted for the largest share in 2025, and is anticipated to grow at a significant CAGR of approximately 46 % during the forecast period.

- The cloud-based segment is expected to dominate the market during the forecast period.

Based on the delivery mode, the workflow clinical solutions market is divided into on-premise, cloud-based, and web-based. Among these, the cloud-based segment is expected to dominate the market during the forecast period. This growth is driven by scalability, cost-effectiveness, and real-time data access. According to the Office of the National Coordinator for Health Information Technology, over 70% of healthcare providers are using cloud-enabled systems to support interoperability and data exchange. The on-premise segment holds around 30–35% share, primarily due to concerns regarding data security, regulatory compliance, and reliance on legacy infrastructure in many healthcare institutions. However, its growth is comparatively slower as organizations gradually transition to cloud environments.

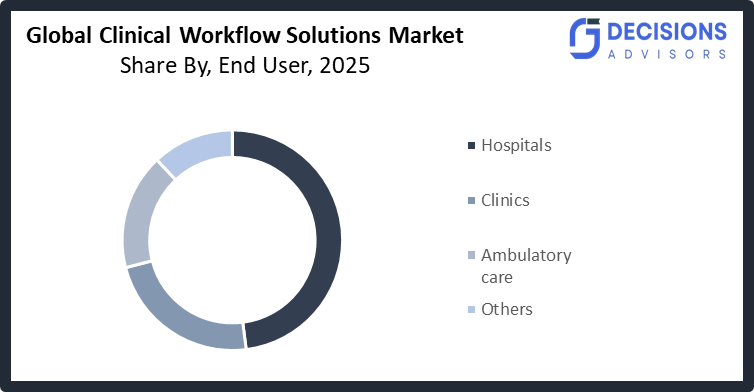

- The hospitals segment held the largest market share in 2025, contributing a dominating share in the global clinical workflow solutions market.

Based on the end-user, the clinical workflow solutions market is divided into hospitals, clinics, ambulatory care centers, and others. Among these, the hospitals segment held the largest market share in 2025, contributing a dominating share in the global clinical workflow solutions market. The segmental growth is driven by high patient volumes, complex workflows, and widespread adoption of digital health systems. The clinics segment holds the second-largest share due to the rising number of outpatient visits and increasing use of digital solutions. Ambulatory care centers are witnessing steady growth, supported by the shift toward outpatient and same-day care services. The others segment, including diagnostic centers and home healthcare settings, also contributes to the market, driven by expanding healthcare infrastructure and growing adoption of workflow optimization solutions.

What is the Reason of the Region Dominance?

The dominance of North America in the global clinical workflow solutions market is primarily driven by its highly advanced healthcare infrastructure, strong adoption of digital health technologies, and significant healthcare expenditure. The region, particularly the United States, has a well-established ecosystem of electronic health records (EHR) and hospital information systems, which creates a strong foundation for integrating clinical workflow solutions. Additionally, favourable government initiatives and regulatory frameworks, such as interoperability mandates and digital health policies, have accelerated the adoption of workflow optimisation tools across healthcare providers. The presence of major healthcare IT companies and continuous technological advancements, including artificial intelligence, cloud computing, and data analytics, further strengthens the region’s leadership.

Strategies to Implement for Growth of the Market in Non-Leading Regions

Growth in non-leading regions such as Asia-Pacific, Latin America, and the Middle East & Africa can be accelerated through strategic investments, technological adoption, and localised approaches. One of the key strategies is the expansion of cloud-based clinical workflow solutions, which reduce infrastructure costs and enable scalable deployment, making them more accessible to emerging healthcare systems. Healthcare providers and governments should focus on strengthening digital health infrastructure by investing in electronic health records (EHR), interoperability frameworks, and healthcare IT systems. Public-private partnerships can play a crucial role in accelerating digital transformation and improving access to advanced workflow technologies.

Regional Segment Analysis of the Workflow Clinical Solutions Market

- North America (U.S., Canada, Mexico)

- Europe (Germany, France, U.K., Italy, Spain, Rest of Europe)

- Asia-Pacific (China, Japan, India, Rest of APAC)

- South America (Brazil and the Rest of South America)

- The Middle East and Africa (UAE, South Africa, Rest of MEA)

North America holds the largest regional market share in the global clinical workflow solutions market.

North America holds the largest regional market share in the global clinical workflow solutions market, accounting for approximately 41.55% of the total market in 2025. This dominance is driven by the region’s highly advanced healthcare infrastructure, widespread adoption of electronic health records (EHR), and strong presence of leading healthcare IT companies. The United States, in particular, contributes the majority of the regional revenue due to high healthcare spending and rapid implementation of digital health technologies. Additionally, favorable government initiatives supporting healthcare digitization, interoperability mandates, and the growing demand for workflow automation to reduce clinician burden further strengthen the market position in North America.

Asia Pacific is the fastest growing region in the global Workflow clinical Solutions market.

Asia-Pacific is the fastest growing region in the global clinical workflow solutions market, primarily due to rapid digital health adoption and strong government-led transformation initiatives across the region. According to the World Health Organisation, digital health is expanding at an unprecedented scale in the Asia-Pacific region, driven by increasing smartphone penetration, rising demand for remote care, and government investments in healthcare digitisation. The WHO further highlights that countries across the region are actively developing national digital health strategies and frameworks, accelerating the adoption of health information systems and workflow technologies.

Europe is the 3rd largest region to grow in the Workflow Clinical Solutions market during the period. This position is supported by the region’s well-established healthcare systems, increasing adoption of digital health technologies, and strong regulatory frameworks promoting interoperability and data exchange. Countries such as Germany, the U.K., and France are investing significantly in healthcare IT infrastructure, including electronic health records (EHR) and clinical workflow optimisation tools. Additionally, the European Union’s focus on digital transformation through initiatives like the European Health Data Space (EHDS) is accelerating the adoption of integrated healthcare solutions across member states.

Future Market Trends in Global Workflow Clinical Solutions Market: -

1.AI-Driven Automation and Predictive Analytics

Artificial intelligence and machine learning are transforming clinical workflows by enabling automated documentation, smart scheduling, and predictive clinical decision support. These technologies help reduce clinician workload, improve diagnostic accuracy, and enhance patient outcomes. AI-powered systems are increasingly being used to analyze large datasets and provide real-time insights, making healthcare delivery more efficient and proactive.

2. Rapid Shift Toward Cloud-Based and Interoperable Systems

Healthcare providers are increasingly adopting cloud-native workflow solutions due to their scalability, cost efficiency, and real-time accessibility. At the same time, interoperability standards are gaining importance, allowing seamless data exchange across different healthcare systems. This trend supports integrated care delivery and improves coordination among healthcare professionals.

3. Integration of Telehealth and Remote Patient Monitoring

The growing adoption of telemedicine and connected healthcare devices is driving the integration of remote care into clinical workflows. Workflow solutions are evolving to support virtual consultations, remote monitoring, and continuous patient engagement. This trend is enabling healthcare providers to deliver care beyond traditional hospital settings and improve accessibility.

Recent Development

In March 2026, Amazon Web Services (AWS) launched Amazon Connect Health, an AI-enabled platform designed to automate healthcare administrative workflows such as patient scheduling, documentation, and medical coding, significantly reducing clinician workload and improving care delivery efficiency.

In March 2026, Oracle Health launched an upgraded clinical workflow platform that integrates EHR data with AI-driven analytics to automate documentation, scheduling, and care coordination. The company aims to compete with Epic Systems, which has seen high adoption of its own Abridge Inside and DAX Copilot integrations.

In November 2025, GE HealthCare announced the acquisition of Intelerad for approximately 2.3 billion dollars to strengthen its cloud-based imaging and workflow capabilities, supporting expansion into outpatient and enterprise imaging solutions.

Market Segment

This study forecasts revenue at global, regional, and country levels from 2020 to 2035. Decision Advisors has segmented the clinical workflow solutions market based on the below-mentioned segments:

Global Clinical Workflow Solutions Market, By Type

- Data Integration Solutions

- Care Collaboration Solutions

- Workflow Automation Solutions

- Enterprise Reporting and Analytics

Global Clinical Workflow Solutions Market, By Delivery Mode

- On-Premise

- Cloud-Based

- Web-based

Global Clinical Workflow Solutions Market, By End-User

- Hospitals

- Clinics

- Ambulatory care Centers

- Others

Global Clinical Workflow Solutions Market, By Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa

Frequently Asked Questions (FAQ)

Q. How do clinical workflow solutions help reduce clinician burnout?

A. Clinical workflow solutions automate repetitive administrative tasks such as documentation, scheduling, and data entry, allowing healthcare professionals to focus more on patient care. This reduces workload stress and improves overall job satisfaction among clinicians.

Q. What challenges do healthcare providers face when implementing workflow solutions?

A. Key challenges include high initial implementation costs, integration issues with legacy systems, data privacy concerns, and the need for staff training to effectively use new digital tools.

Q. How do clinical workflow solutions support value-based healthcare models?

A. These solutions enable better care coordination, real-time data sharing, and performance tracking, helping healthcare providers improve patient outcomes while reducing unnecessary costs, which aligns with value-based care objectives.

Q. What role does interoperability play in clinical workflow solutions?

A. Interoperability ensures seamless data exchange between different healthcare systems, enabling coordinated care, reducing duplication of efforts, and improving clinical decision-making across departments and organizations

Check Licence

Choose the plan that fits you best: Single User, Multi-User, or Enterprise solutions tailored for your needs.

We Have You Covered

- 24/7 Analyst Support

- Clients Across the Globe

- Tailored Insights

- Technology Tracking

- Competitive Intelligence

- Custom Research

- Syndicated Market Studies

- Market Overview

- Market Segmentation

- Growth Drivers

- Market Opportunities

- Regulatory Insights

- Innovation & Sustainability

Report Details

| Scope | Global |

| Pages | 248 |

| Delivery | PDF & Excel via Email |

| Language | English |

| Release | Mar 2026 |

| Access | Download from this page |