Global Conductor Pipes Market

Global Conductor Pipes Market Size, Share, By Product Type (Welded Conductor Pipes, and Seamless Conductor Pipes), By Material Type (Carbon Steel, Alloy Steel, and Stainless Steel), By Application (Onshore Drilling, Offshore Drilling, and Geothermal Wells) By End User (Oil & Gas Companies, Drilling Contractors, and Energy & Utility Companies), By Diameter Size (Below 20 Inches, 20?30 Inches, and Above 30 Inches), and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2026?2035.

CAGR

8.9%

REVENUE 2025

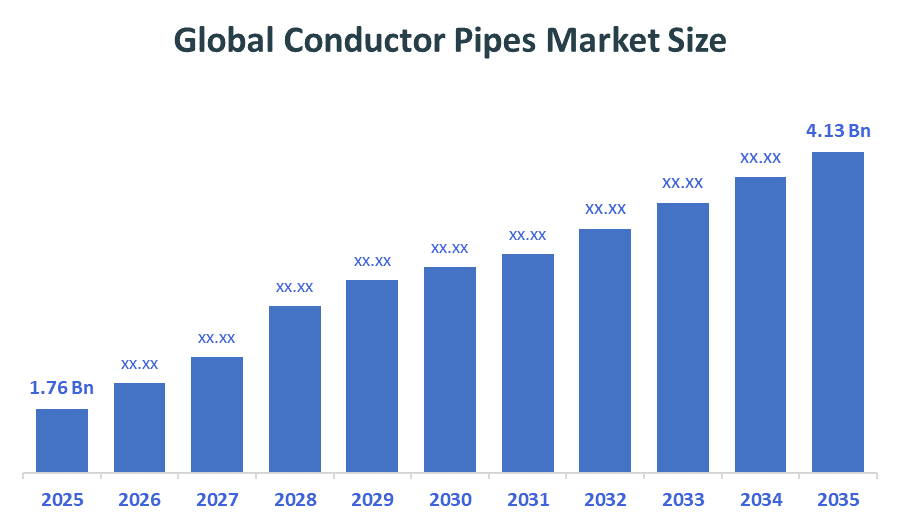

USD Billion 1.76

FORECAST 2035

USD Billion 4.13

REPORT COVERAGE

Global

The Global Conductor Pipes Market Size is projected USD 1.76 Billion in 2025 and is forecasted to reach around USD 4.13 Billion by 2035. According to Decision Advisors, a detailed report on analysis of the Global Conductor Pipes Market indicates that the Corrosion-Resistant High-Strength Conductor Pipes trend dominates the Market, accounting for approx. 35-40% of the total Global demand worldwide. Tenaris S.A. dominates the Global Conductor Pipes Market, supported by revenue of approx. USD 14–16 Billion, due to its strong global manufacturing footprint, advanced tubular technology, long-term contracts with major oil & gas companies, and extensive presence in offshore and deepwater drilling projects worldwide.

Market Snapshot

- Global Conductor Pipes Market Size (2025): USD 1.76 Billion

- Projected Global Conductor Pipes Market Size (2035): USD 4.13 Billion

- Global Conductor Pipes Compound Annual Growth Rate (CAGR): 8.9%

- Largest Regional Market: Asia Pacific

- Fastest Growing Region: North America

- 3rd Largest Region: Europe

- Base Year: 2025

- Historical Period: 2021–2024

- Forecast Period: 2026–2035

Market Overview/ Introduction

The Global Conductor Pipes Market is an integral part of the larger Oil & Gas drilling infrastructure market. Conductor pipes are huge-diameter metal pipes deployed during the early stages of drilling operations. The purpose of using conductor pipes is to offer structural support to the borehole to prevent collapsing in case of loose earth formations, and also to serve as a base for installing further strings of casings. Conductor pipes are extensively employed in drilling operations, be it oil wells, gas wells, geothermal drilling, or offshore drilling. With the growing global demand for energy and increasing activities related to oil exploration in deep water and ultra-deep waters, there has been an increased interest in the conductor pipe market. Recent technological developments in conductor pipes include the development of high-tensile steel alloys, rust-resistant coatings, and automated welds. The government's involvement in energy security and homegrown oil production will only hasten the growth of this market even more. These include:

- Growing offshore drilling regulations in areas such as the Middle East and Brazil

- Development of strategic petroleum reserves in nations like India and China

- Utilization of non-traditional sources of oil, like shale gas in North America

Furthermore, environmentalism is influencing the industry to utilize recyclable steel and environmentally friendly coatings.

- In March 2026, India’s Mission Samudra Manthan targets increasing exploratory wells from 30 to 100 annually, accelerating offshore drilling and significantly boosting demand for conductor pipes in energy infrastructure projects.

- In January 2026, India’s Hydrocarbon Exploration Licensing Policy awarded 172 blocks, attracting USD 4.36 billion investments, accelerating drilling activity and significantly boosting demand for conductor pipes in upstream energy projects.

- In April 2025, India revised the DMI&SP Policy mandating preference for domestically manufactured steel in government projects, strengthening local supply chains and supporting conductor pipe manufacturing demand.

Notable Insights: -

- Asia-Pacific holds the largest regional market share approximately 35% in the Global Conductor Pipes Market.

- North America is the fastest growing region market share approximately 29% in the Global Conductor Pipes Market.

- By product type, the Welded Conductor Pipes segment held a dominant position with 62% in terms of market share in 2025.

- By diameter size, above 30 inches segment is the dominating accounting for market is approximately 48%.

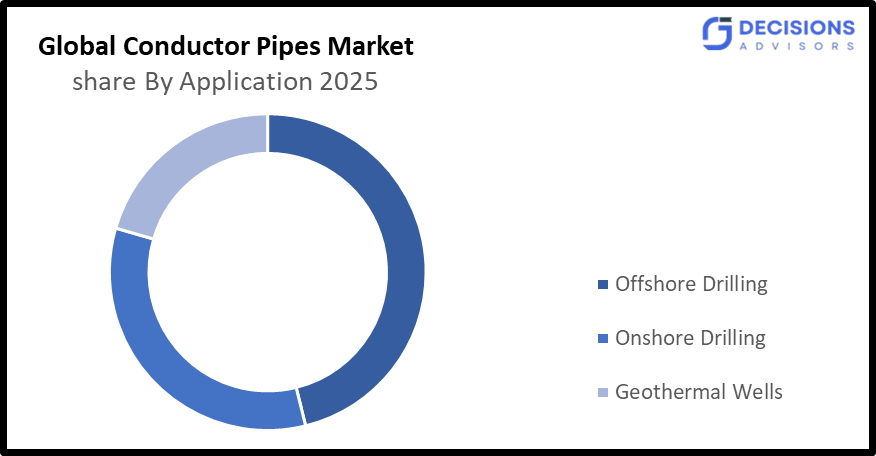

- By application, offshore drilling segment held a dominant position market is approximately 58%.

- By end user, oil & gas companies segment held a dominant position market is approximately 58%.

- By Material Type, carbon steel segment held a dominant position market is approximately 62%.

- The market is likely to achieve a valuation of USD 4.13 Billion by 2035.

What is role of technology in grooming the market?

Technology has played a major role in defining the Global Conductor Pipes Market through improved durability, efficiency, and safety for drilling activities. Present-day conductor pipes are made from durable and strong carbon steel alloys that provide greater resistance to stress and pressure. The use of advanced anti-corrosive coating technologies such as FBE (fusion bonded epoxy) and 3LPE (3-layer polyethylene) coating increases pipe life span particularly under harsh environmental conditions such as offshore drilling in seawater. Welding and manufacturing technology have ensured greater uniformity and robust structure of pipes. Technological developments have been beneficial for the growth of the market. Digital technology is increasingly making its presence felt through automated inspection of pipes for identifying faults as well as their efficient management in drilling activities through IoT-based monitoring systems. Technology has enabled greater innovation in material technology and robotics for more efficient offshore drilling activities.

How is Recent Developments Helping the Market?

The recent trends and advancements in the Global Conductor Pipes Market have been driven towards increasing the efficiency of products while maintaining a sustainable environment. Manufacturers are now introducing superior grades of steel that can be used in deepwater and ultra-deepwater well drilling. In the year 2025-2026, many companies introduced corrosion-resistant conductor pipes with an advanced layer of coating. This makes it easier for operators to conduct drilling operations without worrying about the durability of their equipment. Moreover, there is a growing trend towards automation of the process of installation of the pipes to minimize human interference in operations. The use of prefabricated conductor pipes is another development that has been seen on offshore platforms. This has helped in saving time and minimizing operational costs associated with drilling projects. Furthermore, manufacturers are focusing on the environmentally friendly approach by introducing manufacturing processes that emit fewer greenhouse gases.

Market Drivers

The major factor influencing the Conductor Pipes Market in the Global arena is increasing oil and gas exploration activities. Increasing global energy demand is forcing governments and enterprises to make huge investments in drilling operations, particularly offshore and deep-sea drilling operations. The increase in offshore drilling operations in areas like the Middle East, North Sea, and South America has significantly boosted the demand for Conductor Pipes. Besides, shale gas exploration operations in North America are also contributing to market growth. Increase in aging oil wells in various parts of the world is also driving the demand for conductors because replacing existing pipes will call for installing new pipes. Rapid industrialization and urbanization witnessed in developing countries is also increasing the demand for energy and thereby increasing drilling activities. Efforts made by government agencies for achieving energy self-reliance are also a major reason for increasing demand. Increased investments in infrastructure facilities and better drilling technology have increased the efficiency of oil extraction activities. Also, the use of advanced materials and technology to ensure corrosion resistance has enhanced the performance of the conductor pipes.

Restrain

High initial costs and volatility in raw material prices, particularly steel, act as major restraints in the Global Conductor Pipes Market. Fluctuations in oil prices can delay drilling projects, directly impacting demand. Additionally, strict environmental regulations and concerns regarding carbon emissions may hinder expansion. Limited investments in oil exploration during economic downturns also affect market growth. These factors collectively restrict adoption, especially in cost-sensitive and developing regions.

Competitive Analysis:

The report offers the appropriate analysis of the key organizations/companies involved within the Conductor Pipes market, along with a comparative evaluation primarily based on their Product of offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes Product development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and Geothermal Wells. This allows for the evaluation of the overall competition within the market.

Top Companies in Global Conductor Pipes Market

- Tenaris S.A.

- Vallourec S.A.

- Nippon Steel Corporation

- ArcelorMittal

- TMK Group

- U.S. Steel Tubular Products

- JFE Steel Corporation

- ChelPipe Group

- SeAH Steel Corporation

- National Oilwell Varco

Government Initiatives

|

Country |

Key Government Initiatives |

|

|

India

|

In March 2026, India’s Samudra Manthan initiative includes a $20 billion deepwater rig tender by ONGC, accelerating offshore drilling and significantly increasing demand for conductor pipes in oil exploration. |

|

|

U.S. |

In August 2025, U.S. offshore leasing expansion includes over 30 Gulf of Mexico auctions through 2040, accelerating drilling activity and boosting demand for conductor pipes in oil and gas infrastructure. |

|

|

China |

In March 2025, China’s NDRC gas infrastructure push prioritizes pipeline expansion and urban distribution networks, reducing coal dependence and indirectly boosting demand for conductor pipes in energy projects. |

|

Study on the Supply, Demand, Distribution, and Market Environment of Conductor Pipes Market

The Conductors Pipe Market for Oil & Gas Industry remains well-balanced, owing to its stable supply and demand levels resulting from consistent exploration and extraction of oil and gas resources in the world. The main driver behind the demand side of this market is mostly offshore drilling, oil fields on shore, and alternative energy. Approximately 65 to 70% of total demand for conductors is generated by offshore drilling because it requires robust and highly resistant conductors. Supply in this market includes mainly large steel pipe producers with worldwide distribution. Main locations of the manufacture process include Asia-Pacific, Europe, and North America because of their advanced industries. Direct contract delivery to the oil companies represents nearly 60% of the total market value, while the other channels include distributors and EPCs. Environmental drivers include safety norms, sustainability measures, and technology developments.

Price Analysis and Consumer Behaviour Analysis

The price of conductor pipes depends on the grade of the metal, diameter, coating techniques, and use. Offshore grade pipes tend to cost between 30 and 50 % more than onshore pipes because of their high levels of durability and corrosion resistance. The oil and gas industry values quality and safety issues at about 50 % in terms of purchases. Cost issues make up 30 % of the buying decision, while longevity issues represent about 20 % of purchase considerations. In developing countries, cost issues are even more important, with over 40 percent of oil and gas firms reporting that costs are an important factor in their purchase decision making processes. In developed countries, however, there is greater importance placed on sophisticated technologies and efficiency. The lifespan of conductor pipes ranges from 10 to 20 years. Renewal needs arise because of deterioration of the pipes and environmental degradation.

Market Segmentation

The Conductor Pipes Market share is classified into product type, application, end-user, and farm size

- The product type segment dominated the market in 2025, and is projected to grow at a substantial CAGR of approximately 6.5% during the forecast period.

Based on the product type, the Conductor Pipes Market is divided into Welded Conductor Pipes, and Seamless Conductor Pipes. Among these, welded conductor pipes dominate the market, accounting for approximately 60–65% of total revenue share in 2025. Their dominance is driven by cost-effectiveness, ease of manufacturing, and suitability for large-diameter applications, especially in offshore drilling. The segment is projected to grow at a CAGR of around 5.3–5.8% (2026–2035), supported by increasing demand for affordable and durable pipe solutions.

- The diameter size segment accounted for the largest share in 2025, and is anticipated to grow at a significant CAGR of approximately 6.3% during the forecast period.

Based on the Diameter Size, the Conductor Pipes Market is divided into below 20 inches, 20–30 inches, and above 30 inches. Among these, the above 30 inches segment dominates, holding approximately 45–50% of total market revenue in 2025. This is due to its widespread use in offshore drilling operations requiring high structural strength and stability. The segment is expected to grow at a CAGR of around 5.6–6.2% (2026–2035), driven by increasing deepwater exploration and large-scale energy projects globally.

- The application segment dominated the market in 2025, and is projected to grow at a substantial CAGR of approximately 6.7% during the forecast period.

Based on the application, the Conductor Pipes Market is divided into onshore drilling, offshore drilling, and geothermal wells. Among these, offshore drilling dominates the market, contributing approximately 55–60% of total revenue in 2025. This dominance is driven by rising deepwater and ultra-deepwater exploration activities worldwide. The segment is projected to grow at a CAGR of around 6.0–6.7% (2026–2035), supported by increasing investments in offshore oilfields and demand for high-performance conductor pipe systems.

- The end user segment dominated the market in 2025, and is projected to grow at a substantial CAGR of approximately 6.4% during the forecast period.

Based on the end user, the Conductor Pipes Market is divided into oil & gas companies, drilling contractors, and energy & utility companies. Among these, the oil & gas companies dominate the market, accounting for approximately 55–60% of total revenue share in 2025. Their dominance is due to direct involvement in exploration and production activities and large-scale procurement of conductor pipes. The segment is projected to grow at a CAGR of around 5.5–6.1% (2026–2035), supported by rising global energy demand and increasing drilling investments.

- The Material Type segment dominated the market in 2025, and is projected to grow at a substantial CAGR of approximately 6.6% during the forecast period.

Based on the Material Type, the Conductor Pipes Market is divided into carbon steels, alloy steels, and stainless steel. Among these, carbon steel dominates the market, holding approximately 60–65% of total revenue share in 2025. This dominance is attributed to its high strength, cost-effectiveness, and widespread use in both onshore and offshore drilling. The segment is expected to grow at a CAGR of around 5.2–5.7% (2026–2035), driven by consistent demand and large-scale oil and gas exploration projects globally.

Strategies to Implement for Growth of the Market in Non-Leading Regions

Expanding the Global Conductor Pipes Market in non-leading regions such as parts of Asia-Pacific, Latin America, and Africa requires targeted, cost-focused, and infrastructure-driven strategies. One of the most effective approaches is the development of cost-efficient conductor pipes, as nearly 35–40% of smaller oilfield operators in these regions face capital constraints. Offering flexible pricing models, leasing options, and long-term supply contracts can significantly improve adoption rates. Strengthening local manufacturing and supply chain networks is another key strategy. Establishing regional production units or partnerships with local steel manufacturers can reduce transportation costs and improve delivery timelines. Currently, around 25–30% of remote drilling sites experience delays due to supply inefficiencies, highlighting the need for localized distribution systems. Training and technical support programs are essential to enhance operational efficiency. Many regions lack skilled professionals for advanced drilling operations, which can hinder adoption. Collaborations with governments and energy organizations to provide training and certification programs can address this gap. Additionally, increasing awareness of advanced, corrosion-resistant conductor pipe technologies can drive market penetration. Government incentives, infrastructure investments, and energy security policies will further support growth, enabling wider adoption across emerging markets.

Regional Segment Analysis of the Conductor Pipes Market

- North America (U.S., Canada, Mexico)

- Europe (Germany, France, U.K., Italy, Spain, Rest of Europe)

- Asia-Pacific (China, Japan, India, Rest of APAC)

- South America (Brazil and the Rest of South America)

- The Middle East and Africa (UAE, South Africa, Rest of MEA)

Asia Pacific is anticipated to hold the largest share of the Conductor Pipes market over the predicted timeframe.

Asia-Pacific is anticipated to hold the largest share of the Global Conductor Pipes Market, accounting for approximately 35–38% in 2025. Growth is driven by rising energy demand, increasing offshore and onshore drilling activities, and expanding industrialization in countries such as China and India. The region is projected to grow at a CAGR of 5.8–6.4% during the forecast period. Government initiatives supporting domestic oil production and infrastructure development further strengthen market expansion across emerging economies in the region.

North America is expected to grow at a rapid CAGR in the Conductor Pipes market during the forecast period. North America is expected to register the fastest growth in the Global Conductor Pipes Market, holding approximately 28–30% market share in 2025. The region is projected to expand at a CAGR of 6.2–6.8% during the forecast period. Growth is primarily driven by extensive shale gas exploration, advanced drilling technologies, and strong investments in oilfield infrastructure. The presence of major industry players and continuous technological advancements further support market expansion across the United States and Canada.

Europe is the 3rd largest region to grow in the Conductor Pipes market during the region. Europe is the third-largest region in the Global Conductor Pipes Market, contributing approximately 20–23% of total revenue in 2025. The market is projected to grow at a CAGR of 5.0–5.6% over the forecast period. Growth is supported by offshore drilling activities in the North Sea, along with stringent environmental and safety regulations. Countries such as Germany, the UK, and Norway play a key role in driving demand through advanced energy infrastructure and sustained investments in oil and gas exploration.

Future Market Trends in Global Conductor Pipes Market: -

- Increasing Offshore Exploration Activities

Offshore exploration is accelerating due to rising global energy demand and depletion of onshore reserves. Deepwater and ultra-deepwater drilling projects require robust conductor pipes capable of handling high pressure, corrosive environments, and unstable seabed conditions. Governments and energy companies are investing heavily in offshore infrastructure, particularly in regions like the Middle East, Brazil, and Southeast Asia. This expansion is increasing demand for premium-grade pipes, thereby driving innovation and boosting long-term growth opportunities in the global conductor pipes market.

- Adoption of Corrosion-Resistant Materials

The increasing exposure of conductor pipes to harsh environmental conditions, especially in offshore and subsea applications, is driving the adoption of corrosion-resistant materials. Manufacturers are utilizing advanced coatings such as fusion bonded epoxy and multi-layer polyethylene to extend pipe lifespan and reduce maintenance costs. These materials help prevent structural degradation, ensuring operational safety and efficiency. As oil companies prioritize long-term performance and cost optimization, the demand for corrosion-resistant conductor pipes is expected to grow significantly across global markets.

- Integration of Smart Monitoring Systems

The integration of digital technologies in conductor pipes is transforming operational efficiency and safety in drilling activities. Smart monitoring systems equipped with sensors enable real-time tracking of pressure, temperature, and structural integrity. These systems support predictive maintenance by identifying potential failures before they occur, reducing downtime and operational risks. Oil and gas companies are increasingly adopting IoT-enabled solutions to enhance performance and reduce costs. This trend is expected to drive the development of intelligent conductor pipe systems in the future.

Recent Development

- In March 2026, Nippon Steel Corporation is advancing high-strength, corrosion-resistant steel technologies designed for extreme offshore and high-pressure environments, enhancing durability and supporting global demand for conductor pipes in energy infrastructure.

- In November 2025, Vallourec has strengthened its portfolio of high-strength, corrosion-resistant tubular solutions for ultra-deepwater offshore projects, enhancing durability and performance in extreme environments and supporting global demand for conductor pipes in energy infrastructure.

- In November 2025, TMK Group is advancing high-strength, corrosion-resistant steel pipe technologies for high-pressure oil and gas environments, improving durability and performance in harsh conditions, supporting global conductor pipes market growth.

- In May 2025, Captain Pipes Ltd commenced production at its Ahmedabad facility, expanding manufacturing capacity and strengthening India’s piping sector, indirectly supporting broader pipeline and infrastructure demand linked to conductor pipe markets.

- In May 2024, Tenaris expanded manufacturing capacity in the Asia-Pacific region to strengthen local supply chains and meet rising oil and gas tubular demand, including conductor pipes, supporting global energy infrastructure growth.

Market Segment

This study forecasts revenue at global, regional, and country levels from 2021 to 2035. Decision Advisors has segmented the Global Conductor Pipes Market based on the below-mentioned segments:

Global Conductor Pipes Market, By Product Type

- Welded Conductor Pipes

- Seamless Conductor Pipes

Global Conductor Pipes Market, By Application

- Onshore Drilling

- Offshore Drilling

- Geothermal Wells

Global Conductor Pipes Market, By End User

- Oil & Gas Companies

- Drilling Contractors

- Energy & Utility Companies

Global Conductor Pipes Market, By Diameter Size

- Below 20 Inches

- 20–30 Inches

- Above 30 Inches

Global Conductor Pipes Market, By Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa

Frequently Asked Questions (FAQ)

1. What are conductor pipes used for in the oil and gas industry?

Conductor pipes are large-diameter steel pipes installed at the top section of a wellbore to provide structural support, prevent collapse of shallow formations, and guide drilling operations safely.

2. What factors are driving the growth of the global conductor pipes market?

Growth is driven by increasing offshore drilling activities, rising energy demand, expansion of oil exploration projects, and advancements in deepwater and ultra-deepwater drilling technologies.

3. Which material is commonly used in conductor pipe manufacturing?

Carbon steel is most commonly used due to its high strength, durability, corrosion resistance (with coating), and ability to withstand high drilling loads.

4. What are the key types of conductor pipes available in the market?

The market typically includes welded conductor pipes and seamless conductor pipes, each selected based on well depth, pressure conditions, and installation requirements.

5. Which region dominates the global conductor pipes market?

North America and the Middle East are major regions due to extensive oil and gas exploration activities, followed by Asia-Pacific, which is growing steadily.

Check Licence

Choose the plan that fits you best: Single User, Multi-User, or Enterprise solutions tailored for your needs.

We Have You Covered

- 24/7 Analyst Support

- Clients Across the Globe

- Tailored Insights

- Technology Tracking

- Competitive Intelligence

- Custom Research

- Syndicated Market Studies

- Market Overview

- Market Segmentation

- Growth Drivers

- Market Opportunities

- Regulatory Insights

- Innovation & Sustainability

Report Details

| Scope | Global |

| Pages | 210 |

| Delivery | PDF & Excel via Email |

| Language | English |

| Release | Apr 2026 |

| Access | Download from this page |