Direct Current (DC) Drives Market

Global Direct Current (DC) Drives Market Size, Share, By Voltage Rating (Up to 240 V, 240 - 600 V, and 600 V and Above), By Power Rating (Up to 250 kW, 251 - 500 kW, and 500 kW and Above), By End User (Oil and Gas, Power Generation, Food and Beverage, Chemicals and Petrochemicals, Metal and Mining, Water and Wastewater, Building Automation, and Other) and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2026-2035.

CAGR

5.62%

REVENUE 2025

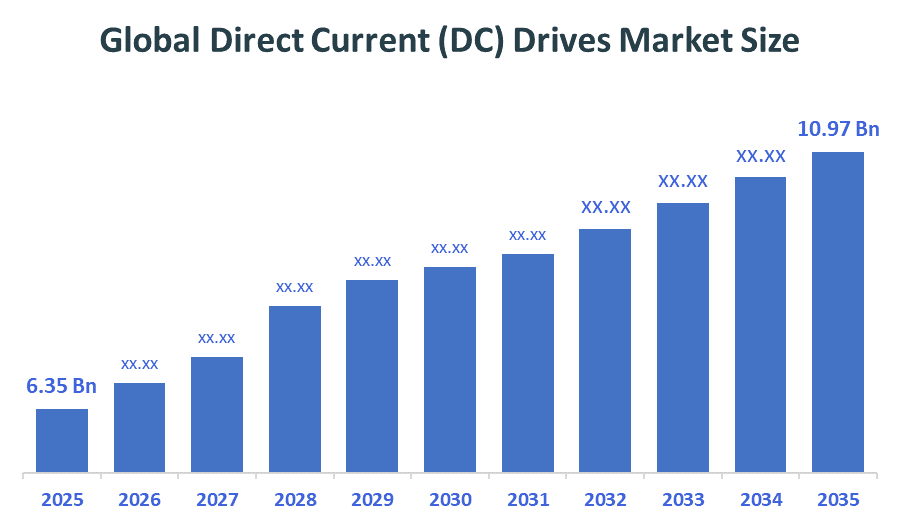

USD Billion 6.35

FORECAST 2035

USD Billion 10.97

REPORT COVERAGE

Global

The Global Direct Current (DC) Drives Market Size is forecasted to grow from USD 6.35 Billion in 2025 and going to reach approx. USD 10.97 Billion by 2035. According to Decision Advisors, there is a detailed research report on the Global Direct Current (DC) Drives Market highlights regenerative DC drives dominate the global market, accounting for approximately 58–62% of the total share worldwide. ABB Ltd. and Siemens Energy collectively generate strong revenue through their energy-saving capabilities., which accounts for approximately 18–22% market share, thus acting as a main driver that influencing innovation, automation, and energy-efficient drive solutions.

Market Snapshot

- Market Size (2025): USD 6.35 Billion

- Projected Market Size (2035): USD 10.97 Billion

- Compound Annual Growth Rate (CAGR): 5.62%

- Largest Regional Market: Asia- Pacific

- Fastest Growing Region: North America

- 3rd Largest Region: Europe

- Base Year: 2025

- Historical Period: 2021–2025

- Forecast Period: 2025–2035

Market Overview/ Introduction

The global Direct Current (DC) Drives market refers to the industry focused on manufacturing and deployment of motor control systems which regulate the speed, torque and direction of DC motors in industrial applications. DC drives are widely used in steel, mining, papermaking, cement production and manufacturing operations which require precise motor control together with high torque capabilities for their equipment to function properly at low speeds. Industrial automation expansion drives market growth together with needs to modernize older motor systems and increasing requirements for energy-efficient motor control systems. The heavy-duty market continues to use DC drives together with AC drives which have become more popular because of their superior performance in variable-speed applications. Digital control systems and PLC integration together with IoT-based monitoring and regenerative braking systems lead technological advancements which create more efficient DC drive systems with better operational control capabilities.

- In February 2025, global industries accelerated retrofitting of legacy motor systems with energy-efficient DC drives integrated with digital controllers, improving operational efficiency and reducing energy consumption across heavy industries.

- In March 2025, China accelerated DC drives demand through strong government support for electric vehicles and renewable energy projects, including solar tracking systems using Siemens SINAMICS drives, enhancing efficiency and industrial automation.

Notable Insights: -

- North America is the fastest growing region market share approximately 5.8% in the global Draught Fan Market.

- Asia Pacific holds the largest regional market share approximately 41% in the global Draught Fan Market.

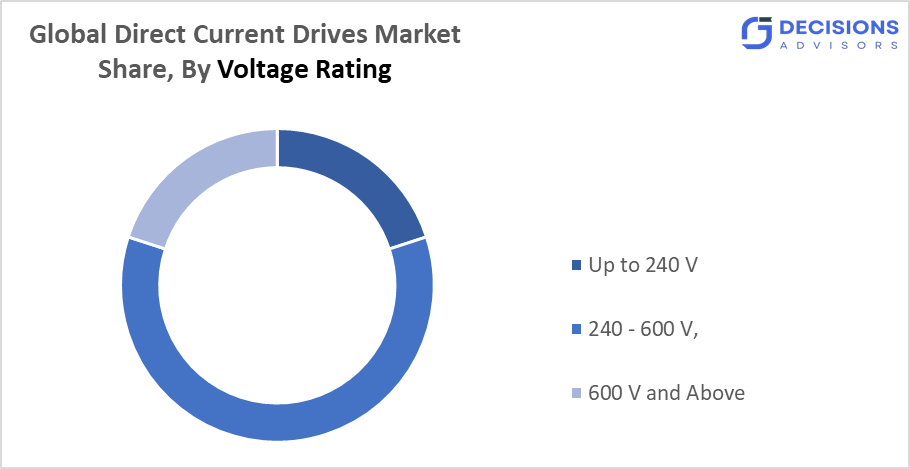

- By Voltage Rating, the 240–600 V segment held a dominant position approximately 5.8% in terms of market share in 2025.

- By Power Rating, 251–500 kW segment is the dominating accounting for approximately 5.9% of the global market share in 2025.

- The compound annual growth rate of the global Draught Fan Market is 5.62%.

- The market is likely to achieve a valuation of USD 10.97 Billion by 2035

What is role of technology in grooming the market?

The DC Drives industry is undergoing a major change because of new technological developments. Digital DC drives achieve energy efficiency improvements between 15% to 25% because they control both speed and torque with high precision. The system receives back excess energy which enables regenerative drives to achieve energy savings between 20% and 35%. IoT-enabled monitoring systems reduce downtime by 30–45% through predictive maintenance, while advanced control algorithms enhance process efficiency by 12–20%. The system achieves better operational performance through automation systems which include PLC and SCADA for increased accuracy and decreased need for human operation. Smart DC drive adoption is expected to reach almost 48% by 2030 which shows a significant increase from the 20% adoption rate in 2025 because industrial automation and energy optimization requirements drive this trend.

Market Drivers

Motor control systems must operate with maximum efficiency to meet the demand which results from industrial automation expansion that occurs at a yearly rate of 6.5%. The metals and mining sectors require DC motors so they generate approximately 38% of total market demand. Industrial facilities that upgrade their old systems through retrofit and modernization projects create approximately 30% of new installation work. Advanced DC drive systems see increased adoption because energy efficiency regulations affect approximately 68% of industrial customers. The manufacturing sector needs accurate motor control systems while heavy industries continue to grow which drives persistent market development.

Restrain

The DC Drives market encounters problems because its maintenance needs and operational difficulties exceed those of AC drives. The maintenance costs for brush and commutator systems increase because they operate with constant wear which impacts their long-term cost efficiency. The increasing use of AC drives creates a competitive threat because they require less maintenance and provide better efficiency than AC drives in specific use cases. The modern automation systems integration challenges create obstacles that hinder industry sectors from adopting new technologies

Competitive Analysis:

The report offers the appropriate analysis of the key organizations/companies involved within the Draught Fan Market, along with a comparative evaluation primarily based on their product of offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes product development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and more. This allows for the evaluation of the overall competition within the market.

Top Companies in Global Direct Current (DC) Drives Market

- ABB Ltd.

- Siemens Energy

- Schneider Electric

- Rockwell Automation

- Mitsubishi Electric

- Toshiba Corporation

- Parker Hannifin

- WEG S.A.

- Danfoss Group

- Hitachi Ltd.

- Emerson Electric Co.

- Fuji Electric

- Nidec Corporation

- General Electric

- CG Power and Industrial Solutions

Government Initiatives

|

Country |

Key Government Initiatives |

|

Europe

|

In July 2024, Europe strengthened industrial efficiency through the EU Ecodesign Directive, compelling industries to adopt energy-efficient DC drives, supporting modernization, reducing emissions, and improving overall industrial energy performance. |

|

US |

In January 2025, the United States Department of Energy advanced smart manufacturing with $33 million funding, while the Bipartisan Infrastructure Law allocated $635 million for EV charging, boosting demand for efficient DC motor controllers. |

|

India |

In January 2025, India accelerated rural electrification through the Saubhagya Scheme and Deen Dayal Upadhyaya Gram Jyoti Yojana, promoting DC power systems and drives to enhance electricity access, reliability, and efficiency across rural regions. |

Study on the Supply, Demand, Distribution, and Market Environment of Global Direct Current Drives Market

The DC drives market operates at 75% of its global production capacity because industrial demand remains stable and manufacturing operations continue throughout the world. The supply chain belongs to Original Equipment Manufacturers (OEMs) who control almost 60% of the market because their engineering strength and worldwide operational reach and superior product development capabilities. Engineering, Procurement, and Construction (EPC) contractors build large-scale industrial and infrastructure systems because they complete approximately 38% of all installed systems. The market volume reaches 32% from replacement demand which occurs when companies modernize and retrofit their outdated motor systems. Export-driven demand creates almost 30% of worldwide trade which shows that international markets are strongly integrated. The metals and mining industry maintains the highest demand at 38% while cement follows with 20% and power needs 18% and manufacturing sectors support continuous growth.

Price Analysis and Consumer Behaviour Analysis

The DC drives market displays multiple price ranges which depend on three factors system size and power capacity and application complexity. Small-scale systems typically range between USD 3,000 and 20,000 which makes them appropriate for light industrial and commercial operations. Medium-sized systems have a price range that starts at USD 20,000 and ends at USD 150,000 which manufacturers use for their mid-scale production and processing facilities. Large industrial systems which manufacturers design for heavy-duty work can cost between USD 150,000 and USD 1.8 million depending on the required custom features and performance specifications. Analysis of consumer behavior shows that 64% of buyers choose to buy DC drives based on their energy efficiency while 52% of buyers concentrate their selection process on products with low maintenance expenses. Approximately 46% of people prefer systems that combine digital technology with smart monitoring features while almost 37% of people choose to base their purchasing decisions on lifecycle costs instead of upfront expenses.

Market Segmentation

The Global Direct Current Drives Market share is classified into type, application, and industry vertical

- The 240–600 V segment dominated the market in 2024, and is projected to grow at a substantial CAGR of approximately 5.8% during the forecast period.

Based on the Voltage Rating, the Global Direct Current Drives Market is divided into Up to 240 V, 240 - 600 V, and 600 V and Above. Among these, the 240–600 V segment dominated the market in 2024, and is projected to grow at a substantial CAGR of approximately 5.8% during the forecast period. The 240–600 V segment dominates because it supports a wide range of industrial applications requiring balanced power, efficiency, and cost. It is widely used in manufacturing, metals, and processing industries, offering optimal performance for medium-to-heavy operations, making it the most preferred voltage range globally.

- The 251–500 kW segment accounted for the largest share in 2024, and is anticipated to grow at a significant CAGR of approximately 5.9 % during the forecast period.

Based on the Power Rating, the Global Direct Current Drives Market is divided into Up to 250 kW, 251 - 500 kW, and 500 kW and above. Among these, the 251–500 kW segment accounted for the largest share in 2024, and is anticipated to grow at a significant CAGR of approximately 5.9 % during the forecast period. The 251–500 kW segment dominates due to its wide application across mid-to-heavy industries such as metals, cement, and manufacturing. It offers an optimal balance between power capacity, efficiency, and cost, making it suitable for most industrial operations requiring reliable and high-performance motor control systems.

- The Metal and Mining segment dominated the market in 2024, and is projected to grow at a substantial CAGR approximately 6.2% during the forecast period.

Based on the End User, the Global Direct Current Drives Market is divided into Oil and Gas, Power Generation, Food and Beverage, Chemicals and Petrochemicals, Metal and Mining, Water and Wastewater, Building Automation, and Other. Among these, the Metal and Mining segment dominated the market in 2024, and is projected to grow at a substantial CAGR approximately 6.2% during the forecast period. This represents approximately USD 294 million of the total market value of USD 763 million in 2024. The retail pharmacy segment will grow faster than other channels due to customers prefer to buy OTC products from pharmacies which have numerous locations, pharmaceutical companies established partnership agreements, pharmacies implemented solutions to help patients with dry mouth and provide customized treatment plans for senior customers.

Strategies to Implement for Growth of the Market in Non-Leading Regions

The companies need to increase public understanding about advanced DC drive technology because this knowledge will help drive their business growth in non-dominant geographical markets. The company can demonstrate to users the advantages of energy-saving drive systems through its industrial outreach initiatives and technical training sessions. Businesses can achieve better product distribution and faster delivery times by creating local partnerships with regional OEM agents and EPC contractors and industrial suppliers. Manufacturers need to create affordable modular DC drive systems that meet the needs of developing markets which require cost-effective solutions. The combination of flexible financing options with after-sales service packages will help small and medium enterprises to adopt new products. The inclusion of IoT-enabled monitoring features into mid-range products will boost their perceived value while improving operational efficiency. The company can increase market share through collaboration with government agencies and regulatory organizations to meet energy efficiency standards and receive financial incentives. Local manufacturing facilities and service centers will create cost savings while building customer confidence which will allow the business to grow in emerging markets and areas with low market penetration.

Regional Segment Analysis of the Global Direct Current Drives Market

- North America (U.S., Canada, Mexico)

- Europe (Germany, France, U.K., Italy, Spain, Rest of Europe)

- Asia-Pacific (China, Japan, India, Rest of APAC)

- South America (Brazil and the Rest of South America)

- The Middle East and Africa (UAE, South Africa, Rest of MEA)

Asia Pacific is anticipated to hold the largest share approximately 41% of the Global Direct Current Drives Market over the predicted timeframe.

Asia Pacific holds approximately 41% of the Global Direct Current (DC) Drives Market due to rapid industrialization, expanding manufacturing sectors, and strong infrastructure development across countries like China and India. The region has a high concentration of energy-intensive industries such as metals, mining, cement, and power generation, all of which require efficient motor control systems. Increasing investments in automation, rising electricity demand, and government initiatives promoting energy efficiency further support market growth. Additionally, the presence of low-cost manufacturing hubs and growing adoption of industrial digitalization technologies contribute to the region’s dominant position in the global DC drives market.

North America is expected to grow at a rapid CAGR approximately 5.8% in the Global Direct Current Drives Marketduring the forecast period. North America is expected to grow at a CAGR of approximately 5.8% due to increasing industrial automation, modernization of aging infrastructure, and strong adoption of energy-efficient motor control systems. Industries such as metals, oil and gas, and manufacturing are investing heavily in advanced DC drives to improve operational efficiency and reduce energy consumption. Strict environmental regulations are also pushing companies to upgrade to efficient and low-emission technologies. Additionally, the rapid integration of digital solutions such as IoT-based monitoring and predictive maintenance is enhancing system performance and reliability. Government incentives for energy efficiency and infrastructure upgrades further support market growth across the region.

Europe is the 3rd largest region to grow in the Global Direct Current Drives Market during the region.

The Global Direct Current (DC) Drives Market ranks Europe as its third most significant region because of the area's strong industrial presence and commitment to energy-saving solutions and sustainable practices. The manufacturing and automotive sectors in Germany France and the UK operate their businesses by using advanced motor control systems which they require for their industrial processes. The combination of strict environmental regulations with EU energy-efficiency directives creates incentives for businesses to implement advanced low-emission drive technologies. The combination of industrial facilities that need modern upgrades and companies that invest in automation and digitalization will create a growing need for DC drives. The region experiences continuous market expansion because of its leading technology providers and their dedication to decarbonization efforts.

Future Market Trends in Global Direct Current Drives Market: -

- Shift Toward Digital DC Drives

The market is rapidly shifting toward digital DC drives with IoT integration and automation capabilities. Around 32% of new DC drives are equipped with smart sensors and cloud connectivity, while nearly 30% of installations include advanced monitoring systems. These technologies improve efficiency by up to 33% and reduce downtime by 25%, supporting Industry 4.0 adoption.

- Growth of Regenerative Technologies

Regenerative DC drives are gaining traction due to their ability to recover and reuse energy during braking processes. Approximately 28% of new DC drives now incorporate regenerative features, contributing to energy savings of 15–30% in industrial operations. This trend is especially strong in metals, mining, and heavy manufacturing sectors focusing on sustainability.

- Hybrid Systems (AC-DC Integration)

Hybrid systems combining AC and DC drives are emerging to optimize efficiency and flexibility. Around 37% of industrial motor control projects now involve AC-DC integration, leveraging AC efficiency and DC precision. These hybrid setups improve system performance by 20–25% and are increasingly adopted in complex automation and heavy-duty industrial applications.

Recent Development

- In April 2026, strong demand for high-power DC-DC converters is driven by heavy industrial applications, including automation, mining, and energy systems, where over 62% of automated production lines rely on advanced power conversion technologies, reflecting the region’s industrial focus.

- In February 2026, Siemens AG advanced DC drive and industrial efficiency solutions through its partnership with Georgia Institute of Technology, focusing on digital twins, AI-driven optimization, and energy-efficient industrial systems.

- In March 2025, ABB Ltd. offers the DCS880-S series DC drives featuring advanced regenerative capabilities, enabling energy recovery, improved motor control, reduced operational costs, and enhanced efficiency across heavy industrial applications.

- In August 2023, Toshiba Corporation launched compact intelligent power devices for brushless DC drives, while maxon motor introduced configurable, high-flexibility motor controls, enhancing efficiency, customization, and performance in industrial drive applications

How is Recent Developments Helping the Market?

The DC drives market has experienced recent changes which lead to improved operational efficiency and sustainable solutions and higher productivity levels across various industries. Industries benefit from advanced digital technologies which include IoT-enabled monitoring and predictive maintenance systems because these technologies help them achieve real-time performance tracking and unexpected failure reduction and downtime minimization. The smart systems enable users to increase reliability while decreasing maintenance expenses which makes DC drives a better option for contemporary industrial processes. The development of machine learning and data analytics technologies allows for more precise motor performance control which results in enhanced system efficiency and extended operational life. Regenerative DC drives function as vital components which drive market expansion through their growing use. The systems achieve energy savings through their ability to capture surplus operational energy which they return to the power grid. The metals and mining and manufacturing sectors increasingly implement these solutions to comply with their energy efficiency standards and their sustainability objectives. The ongoing digital transformation that all industries experience has led to increased demand for smart DC drives which include advanced control systems and remote monitoring and automation functions. The new technologies which enable industrial process enhancements will create better accuracy results and higher productivity outcomes while they allow seamless connection to existing industrial automation systems. The current innovations lead to two major outcomes which produce better results and help organizations worldwide move toward energy-saving intelligent industrial systems.

Market Segment

This study forecasts revenue at global, regional, and country levels from 2020 to 2035. Spherical Insights has segmented the Global Direct Current Drives Market based on the below-mentioned segments:

Global Direct Current Drives Market, By Voltage Rating

- Up to 240 V

- 240 - 600 V

- 600 V and Above

Global Direct Current Drives Market, By Power Rating

- Up to 250 kW

- 251 - 500 kW

- 500 kW and Above

Global Direct Current Drives Market, By End User

- Oil and Gas

- Power Generation

- Food and Beverage

- Chemicals and Petrochemicals

- Metal and Mining

- Water and Wastewater

- Building Automation

- Other

Global Direct Current Drives Market, By Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa

Frequently Asked Questions (FAQ)

- How do draught fans contribute to emission reduction in industrial plants?

Draught fans optimize airflow and combustion efficiency, ensuring complete fuel burning and reducing particulate emissions. This helps industries comply with environmental regulations and lowers overall carbon footprint.

- What is the difference between induced draught and forced draught fans in industrial applications?

Forced draught fans push air into combustion chambers, while induced draught fans extract flue gases out. Together, they maintain balanced airflow and stable pressure conditions in industrial systems.

- Why are centrifugal draught fans preferred over axial fans in heavy industries?

Centrifugal fans are preferred because they can handle high pressure, dust-laden air, and extreme temperatures, making them suitable for demanding environments like power plants and cement industries.

- How is digitalization impacting maintenance strategies in the draught fan market?

Digital tools such as IoT sensors and predictive analytics enable condition-based monitoring, reducing unexpected failures and lowering maintenance costs through early fault detection.

- What role do draught fans play in worker safety within industrial environments?

They help maintain proper ventilation, remove toxic gases, and regulate air quality, ensuring safe working conditions in confined and hazardous industrial spaces.

Check Licence

Choose the plan that fits you best: Single User, Multi-User, or Enterprise solutions tailored for your needs.

We Have You Covered

- 24/7 Analyst Support

- Clients Across the Globe

- Tailored Insights

- Technology Tracking

- Competitive Intelligence

- Custom Research

- Syndicated Market Studies

- Market Overview

- Market Segmentation

- Growth Drivers

- Market Opportunities

- Regulatory Insights

- Innovation & Sustainability

Report Details

| Scope | Global |

| Pages | 210 |

| Delivery | PDF & Excel via Email |

| Language | English |

| Release | Apr 2026 |

| Access | Download from this page |