Global Energy Management Systems Market

Energy Management Systems Market Size, Share, By System (IEMS, BEMS, HEMS), By Component (Hardware, Software), By Vertical (Residential, Energy & Power, Telecom & IT, Manufacturing, and Retail), and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2025 ? 2035.

REPORT COVERAGE

Global

Market Snapshot

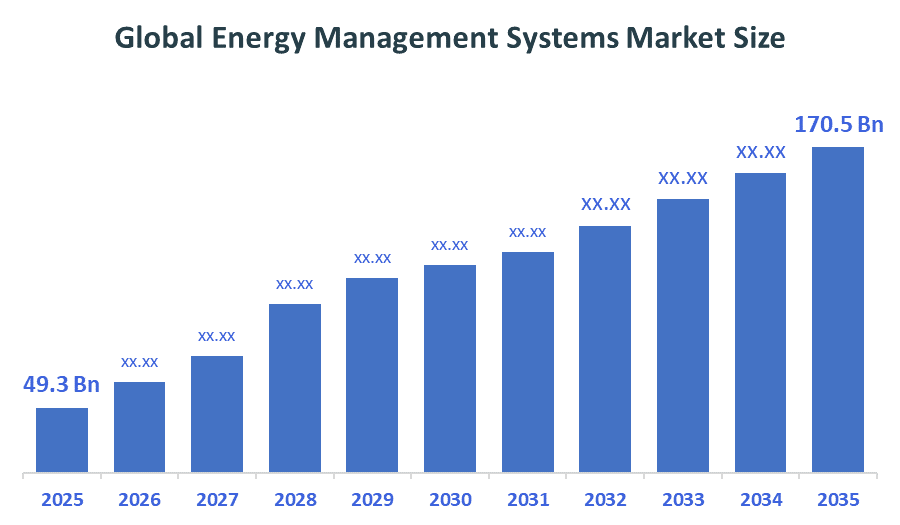

- Market Size (2025): USD 49.3 Billion

- Projected Market Size (2035): USD 170.5 Billion

- Compound Annual Growth Rate (CAGR): 13.21%

- Largest Regional Market: North America

- Fastest Growing Region: Asia-Pacific

- 3rd Largest Region: Europe

- Base Year: 2025

- Historical Period: 2021–2024

- Forecast Period: 2025–2035

According to Decision Advisors, the Energy Management Systems Market Size is expected to grow from USD 49.3 Billion in 2025 to USD 170.5 Billion by 2035, at a CAGR of 13.21% during the forecast period 2025-2035. It is motivated by escalating energy expenses, stringent governmental carbon emission policies, and the pressing requirement for industrial energy efficiency. The integration of renewable energy, the adoption of IoT/smart grid technologies, and the transition to cloud-based, real-time energy monitoring accelerate growth.

Market Overview/ Introduction

An Energy Management System is an all-encompassing platform that integrates hardware and software, enabling organizations and individuals to track, automate, and enhance energy use and performance. Energy consumption is optimized by EMS using software and hardware (such as sensors and smart meters) across industrial, building, and residential environments, with North America at the forefront of the market. The increasing energy costs, the embrace of industrial IoT, and strict decarbonization measures are propelling this growth, with industrial (IEMS) and building (BEMS) systems at the forefront of demand. The integration of AI, machine learning, and IoT-enabled devices is transforming EMS from simple monitoring to predictive, automated, and real-time energy optimization. In future AI models for forecasting demand and automatic fault detection are major growth areas, expected to deliver 15–25% operational expenditure (OPEX) reductions.

- Governments worldwide provide tax credits, subsidies, and grants to accelerate smart meter and energy-efficient system adoption; in India alone, over 5.28 crore smart meters have been installed under RDSS, significantly driving Energy Management Systems market growth.

- Energy policy initiatives targeting greenhouse gas reduction are accelerating EMS adoption; for instance, India aims to reduce emission intensity by 45% by 2030, driving demand for energy management systems across industrial, commercial, and residential sectors.

- China is investing heavily in grid modernization, with China Southern Power Grid allocating 670 billion yuan (US$105 billion) during 2021–2025, driving smart grid deployment and accelerating Energy Management Systems adoption across utilities and industries.

Notable Insights: -

- North America holds the largest regional market share approximately 36.4% in the Energy Management Systems

- Asia Pacific is the fastest growing region in the energy management systems market with a CAGR of approximately 24%.

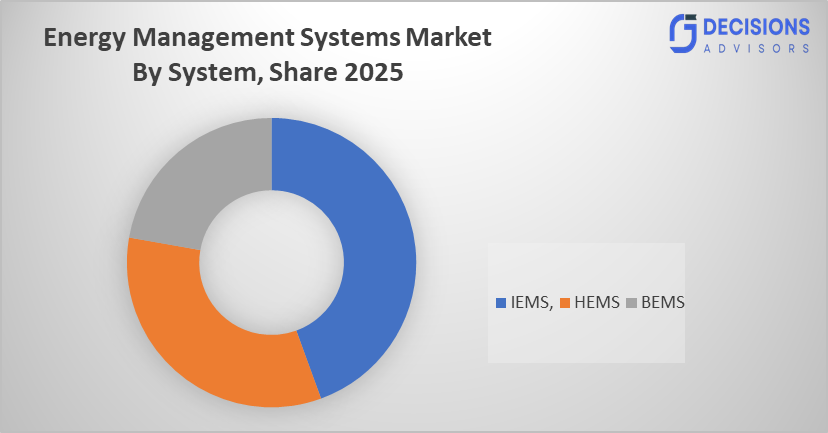

- By system, the IEMS segment held a dominant position with approximately 51% in terms of market share in 2025.

- By component, hardware segment is the dominating accounting for over 60% of the global market share in 2025.

- The compound annual growth rate of the energy management systems market is 13.21%.

- The market is likely to achieve a valuation of USD 170.5 billion by 2035.

What is role of technology in grooming the market?

Technology is playing a profoundly transformative role in grooming the energy management systems (EMS) market, not merely as an enabler but as a core architect of its accelerated expansion and value creation. The integration of advanced technologies such as artificial intelligence, machine learning, and the Internet of Things has redefined EMS capabilities by enabling real-time monitoring, predictive analytics, and automated energy optimization, thereby significantly enhancing operational efficiency and cost rationalization. Empirical trends underscore this transformation, with nearly 48% of organizations already deploying digital EMS solutions to improve energy visibility, while over 52% are leveraging predictive analytics to optimize consumption patterns and system performance

How is Recent Developments Helping the Market?

Recent developments are playing a pivotal role in accelerating the growth trajectory of the Energy Management Systems (EMS) market by enhancing both technological capabilities and market accessibility. Advances in digital technologies particularly artificial intelligence, machine learning, and the Internet of Things have significantly improved the precision, automation, and real-time responsiveness of EMS platforms, enabling predictive energy optimization and intelligent demand-side management. The rapid evolution of cloud computing and Software-as-a-Service (SaaS) models has further democratized access by reducing upfront capital requirements and enabling scalable, subscription-based deployments. Concurrently, the integration of EMS with renewable energy systems, battery storage, and electric vehicle infrastructure is expanding its application scope, particularly in decentralized and smart grid environments.

Market Drivers

The energy management systems (EMS) market is being underpinned by a powerful convergence of macroeconomic pressures, regulatory imperatives, and rapid technological advancement, collectively reinforcing its strategic relevance across industries. A primary growth catalyst is the persistent escalation in global energy costs, which is compelling enterprises to adopt intelligent systems that enable real-time monitoring, optimization, and cost rationalization. This economic driver is further amplified by increasingly stringent environmental regulations and decarbonization commitments, as governments and regulatory bodies mandate higher standards of energy efficiency and emissions reduction, positioning EMS as a critical compliance and reporting tool. Simultaneously, the accelerating transition toward renewable energy and decentralized power generation has introduced new complexities in energy flows, necessitating sophisticated management platforms capable of integrating distributed energy resources and ensuring grid stability. Technological progress particularly in artificial intelligence, the Internet of Things, and cloud-based analytics is further enhancing system capabilities, delivering predictive insights, automation, and scalability at reduced costs. Moreover, the global push toward smart infrastructure and urban modernization, especially within emerging economies, is fostering a conducive ecosystem for EMS deployment.

Restrain

The energy management systems (EMS) market, notwithstanding its strong long-term growth fundamentals, remains constrained by a confluence of structural, financial, and operational impediments that temper its rate of adoption. Chief among these is the substantial upfront capital outlay required for system deployment, encompassing advanced metering infrastructure, integration with legacy systems, and ongoing maintenance costs, which disproportionately impacts small and medium enterprises with limited financial flexibility.

Competitive Analysis:

The report offers the appropriate analysis of the key organizations/companies involved within the energy management systems market, along with a comparative evaluation primarily based on their product of offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes product development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

Top Companies in Energy Management Systems Market

- Schneider Electric

- Siemens AG

- Honeywell International Inc.

- ABB Ltd.

- General Electric (GE Vernova)

- Johnson Controls

- Emerson Electric Co.

- Rockwell Automation

- IBM Corporation

- Cisco Systems

- Eaton Corporation

- Mitsubishi Electric

- Yokogawa Electric

- Delta Electronics

- C3.ai

- GridPoint

- Itron

- Enel X

- Oracle

- SAP SE

Government Initiatives

|

Country |

Key Government Initiatives |

|

UK |

Government-led initiatives, particularly in the UK, have driven large-scale deployment of smart meters across more than 26 million households, with energy suppliers mandated to accelerate installations. |

|

US |

The U.S. Department of Energy (DOE), through its Office of Energy Efficiency and Renewable Energy (EERE), provides substantial funding and strategic support for energy efficiency initiatives, with annual investments exceeding 3 billion to advance energy technologies and infrastructure. |

|

China |

The Top-1,000 Energy-Consuming Enterprises Program, China expanded its industrial energy efficiency initiatives to cover tens of thousands of energy-intensive enterprises under the Top-10,000 Program, mandating comprehensive energy audits and structured energy management practices. |

Study on the Supply, Demand, Distribution, and Market Environment of Energy Management Systems Market

The study of supply, demand, distribution, and the market environment of the energy management systems (EMS) market reveals a structurally evolving ecosystem underpinned by technological innovation and policy-driven transformation. On the supply side, the market is dominated by a mix of multinational technology providers and niche solution vendors that are increasingly leveraging digital architectures, including cloud computing, IoT integration, and advanced analytics, to deliver scalable and interoperable EMS platforms, while continuous R&D investments and strategic alliances are enhancing product sophistication and geographic penetration. Demand dynamics are being robustly shaped by escalating energy costs, tightening environmental regulations, and the intensifying corporate focus on sustainability and carbon neutrality, with strong uptake across industrial and commercial sectors, and a progressively widening adoption base in emerging economies driven by urbanization and infrastructure modernization. From a distribution standpoint, the market is witnessing a paradigm shift from conventional direct-sales approaches to more diversified, partner-centric models, encompassing energy service companies (ESCOs), system integrators, and digital platforms, thereby enabling greater customization, faster deployment, and improved customer outreach.

Price Analysis and Consumer Behaviour Analysis

The price analysis of the energy management systems (EMS) market reflects a structurally evolving landscape characterized by high initial capital expenditure, long payback periods, and a gradual shift toward subscription-based and outcome-driven pricing models. Vendors are increasingly adopting flexible pricing architectures such as SaaS-based platforms and performance-linked contracts to enhance affordability and broaden market penetration, particularly among cost-sensitive industrial and commercial users. Simultaneously, declining hardware costs, driven by advancements in IoT sensors and cloud infrastructure, are exerting downward pressure on overall system pricing, while value-added analytics and AI-driven capabilities sustain premium positioning for advanced solutions. From a consumer behaviour standpoint, purchasing decisions are predominantly influenced by return on investment, regulatory compliance requirements, and sustainability objectives, with enterprises demonstrating a marked preference for solutions that deliver measurable energy savings and operational efficiency.

Market Segmentation

The energy management systems market share is classified into system, component, and vertical.

- The IEMS segment dominated the market in 2025, and is projected to grow at a substantial CAGR of approximately 51% during the forecast period.

Based on the system, the energy management systems market is divided into IEMS, BEMS, HEMS. Among these, the IEMS segment dominated the market in 2025, and is projected to grow at a substantial CAGR of approximately 51% during the forecast period. IEMS is crucial because the high energy consumption in manufacturing, oil & gas, and heavy industries necessitates the optimization of energy efficiency for a substantial reduction in operational costs, especially with the rise of automation.

The hardware segment accounted for the largest share in 2025, and is anticipated to grow at a significant CAGR of approximately 60 % during the forecast period.

Based on the component, the energy management systems market is divided into hardware, software. Among these, the hardware segment accounted for the largest share in 2025, and is anticipated to grow at a significant CAGR of approximately 60 % during the forecast period. To gather real-time data on energy consumption, temperature, and performance, hardware components like IoT-enabled sensors, smart meters, and controllers are necessary. The heavy industry and manufacturing sectors, which are the primary users of EMS, necessitate the use of large-scale physical installations like PLCs (Programmable Logic Controllers) and SCADA systems for energy optimization, resulting in substantial hardware revenue.

- The arrhythmia detections segment dominated the market at a CAGR of approximately 68%% in 2025, and is projected to grow at a substantial CAGR during the forecast period.

Based on the vertical, the energy management systems market is divided into residential, energy & power, telecom & IT, manufacturing, retail. Among these, the arrhythmia detections segment dominated the market at a CAGR of approximately 68% in 2025, and is projected to grow at a substantial CAGR during the forecast period. It is essential for profitability that energy use is reduced, as manufacturing facilities such as cement, chemical, and steel plants incur considerable energy costs that can account for as much as 20% of their overall operational expenses. These sectors employ intricate, high-velocity machines and processing lines (such as furnaces and compressors) that necessitate exact observation and regulation (like Siemens' SIMATIC Energy Manager) to reduce waste.

Strategies to Implement for Growth of the Market in Non-Leading Regions

The expansion of the energy management systems (EMS) market across non-leading regions will be contingent upon a calibrated blend of affordability, regulatory impetus, and technological localization. Market participants must prioritize the deployment of cost-efficient, modular, and cloud-enabled solutions to mitigate capital intensity barriers that typically constrain adoption in price-sensitive economies. Concurrently, proactive government intervention through fiscal incentives, energy-efficiency mandates, and alignment with decarbonization agendas will serve as a critical demand catalyst. Infrastructure modernization particularly the proliferation of smart grids, advanced metering infrastructure, and digital energy networks will further underpin scalable EMS integration. Strategic alliances with local utilities and ecosystem partners are likely to enhance market penetration by enabling context-specific customization and improving stakeholder trust. Moreover, targeted investments in workforce upskilling and awareness generation will address capability deficits that often impede implementation. The convergence of EMS platforms with distributed renewable energy systems and microgrid architectures presents an additional avenue for growth, particularly in regions grappling with grid instability. Ultimately, the integration of advanced technologies such as artificial intelligence, Internet of Things, and data analytics will redefine value creation by enabling predictive, real-time energy optimization, thereby positioning EMS as an indispensable pillar of sustainable industrial and urban development in emerging markets.

Regional Segment Analysis of the Energy Management Systems Market

- North America (U.S., Canada, Mexico)

- Europe (Germany, France, U.K., Italy, Spain, Rest of Europe)

- Asia-Pacific (China, Japan, India, Rest of APAC)

- South America (Brazil and the Rest of South America)

- The Middle East and Africa (UAE, South Africa, Rest of MEA)

North America is anticipated to hold the largest share of the energy management systems market over the predicted timeframe. North America is anticipated to maintain its dominant position in the energy management systems (EMS) market over the forecast horizon, underpinned by its early adoption of advanced energy technologies, robust regulatory frameworks, and deep-rooted digital infrastructure. The region accounted for over 36.4% of global EMS revenue share in 2025, firmly establishing its leadership position in the global landscape. This dominance is further reinforced by the strong presence of technologically mature economies such as the United States and Canada, where large-scale deployment of smart grids, advanced metering infrastructure, and AI-enabled energy optimization solutions has already reached significant penetration levels.

Asia Pacific is expected to grow at a rapid CAGR in the energy management systems market during the forecast period. The region is fastest growing and driven by rapid industrialization, urban expansion, and intensifying energy demand across key economies such as China, India, and Southeast Asia. The region is expected to expand at a CAGR exceeding 24% during the forecast horizon, outpacing global averages and reflecting its strong growth potential. This accelerated trajectory is underpinned by large-scale investments in smart city initiatives, grid modernization, and renewable energy integration, alongside increasing government emphasis on energy efficiency and carbon reduction targets. Notably, countries such as China and India are witnessing substantial deployment of advanced metering infrastructure and digital energy platforms, supported by favorable policy frameworks and public-private partnerships.

Europe is the 3rd largest region to grow in the energy management systems market during the region. Europe stands as the third-largest regional market for energy management systems (EMS), accounting for approximately 28% of the global market share, underpinned by a robust regulatory ecosystem, advanced energy infrastructure, and a deeply entrenched commitment to sustainability and carbon neutrality, with growth further supported by widespread adoption of smart grids, renewable integration, and stringent energy-efficiency mandates across the region.

Future Market Trends in Energy Management Systems: -

- Incorporation of AI and ML:

Future systems will be largely governed by AI, which will offer predictive analytics for demand forecasting, real-time energy optimization, and automated fault detection in both industrial and commercial environments.

- Decentralized Energy Management (Microgrids):

With the decentralization of energy generation, EMS will place greater emphasis on managing microgrids that incorporate solar PV, wind, and battery storage to maintain energy resilience and grid stability.

- Smart Grids and Demand Response:

Future EMS will engage directly with smart grids to facilitate automatic load shedding or load shifting (peak shaving), enabling companies to reduce costs during peak demand periods.

Recent Development

- In September 2025, Honeywell introduced the Ionic Modular All-in-One, a compact battery energy storage solution tailored for commercial and industrial applications, integrating advanced control systems and real-time analytics to optimize energy consumption and grid efficiency.

- In February 2025, Schneider Electric introduced the SpaceLogic Touchscreen Room Controller, an advanced building automation solution integrating AI-driven controls for HVAC, lighting, and occupancy management to enhance energy efficiency and occupant comfort.

- In November 2024, IBM released IBM Maximo Renewables, an advanced asset performance management solution designed to enhance the monitoring, management, and optimization of renewable energy assets through AI-driven analytics and predictive maintenance.

- In September 2024, Eaton launched the AbleEdge home energy management system, an integrated smart home solution combining advanced load control, real-time monitoring, and seamless integration with solar and energy storage systems.

- In June 2024, ABB launched ABB Ability OPTIMAX 6.4, an advanced digital energy management and optimization system designed for coordinated control of industrial assets, integrating AI-driven forecasting and analytics to enhance energy efficiency and support decarbonization.

Market Segment

This study forecasts revenue at global, regional, and country levels from 2020 to 2035. Decision Advisor has segmented the energy management systems market based on the below-mentioned segments:

Energy Management Systems Market, By System

- IEMS

- BEMS

- HEMS

Energy Management Systems Market, By Component

- Hardware

- Software

Energy Management Systems Market, By Vertical

- Residential

- Energy & Power

- Telecom & IT

- Manufacturing

- Retail

Energy Management Systems Market, By Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa

Frequently Asked Questions (FAQ)

1. What are the primary factors contributing to the long-term expansion of the Energy Management Systems market?

The sustained expansion of the energy management systems (EMS) market is primarily driven by the convergence of rising global energy costs, stringent environmental regulations, and the increasing urgency for carbon footprint reduction. Additionally, the proliferation of digital technologies such as artificial intelligence, IoT-enabled devices, and cloud-based analytics is enhancing system intelligence, thereby accelerating enterprise adoption across multiple sectors.

2. How are digital technologies reshaping the operational capabilities of EMS platforms?

Digital transformation has fundamentally enhanced EMS platforms by enabling real-time monitoring, predictive analytics, and automated decision-making. Technologies such as machine learning and IoT facilitate granular energy visibility, allowing organizations to optimize consumption patterns, reduce operational inefficiencies, and achieve measurable cost savings through intelligent energy orchestration.

3. Why is North America maintaining its leadership position in the EMS market?

North America’s dominance is attributed to its advanced digital infrastructure, early adoption of smart grid technologies, and strong regulatory frameworks supporting energy efficiency. The presence of key industry players and significant investments in AI-driven energy optimization further consolidate the region’s leading position in the global EMS landscape.

4. What factors are driving the rapid growth of the Asia-Pacific EMS market?

The Asia-Pacific region is witnessing accelerated growth due to rapid industrialization, urban expansion, and increasing energy demand. Government-backed smart city initiatives, large-scale renewable energy integration, and infrastructure modernization projects are significantly boosting EMS adoption, particularly in emerging economies such as China and India.

5. How do Energy Management Systems contribute to industrial cost optimization?

EMS solutions enable industries to monitor, control, and optimize energy usage across complex operations. By leveraging real-time data and predictive analytics, organizations can minimize energy wastage, improve equipment efficiency, and reduce energy-related operational expenditures, which often constitute a substantial portion of total production costs.

Check Licence

Choose the plan that fits you best: Single User, Multi-User, or Enterprise solutions tailored for your needs.

We Have You Covered

- 24/7 Analyst Support

- Clients Across the Globe

- Tailored Insights

- Technology Tracking

- Competitive Intelligence

- Custom Research

- Syndicated Market Studies

- Market Overview

- Market Segmentation

- Growth Drivers

- Market Opportunities

- Regulatory Insights

- Innovation & Sustainability

Report Details

| Scope | Global |

| Pages | 220 |

| Delivery | PDF & Excel via Email |

| Language | English |

| Release | Apr 2026 |

| Access | Download from this page |