Global Epichlorohydrin Market

Global Epichlorohydrin Market Size, Share, By Type (Oil-Based Epichlorohydrin, Bio-Based Epichlorohydrin), By Application (Epoxy Resins, Specialty Water Treatment Chemicals, and Others), By End-Use Industry (Construction, Paints and Coatings, Adhesives, and Others), and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2026 ? 2035.

REPORT COVERAGE

Global

Market Snapshot

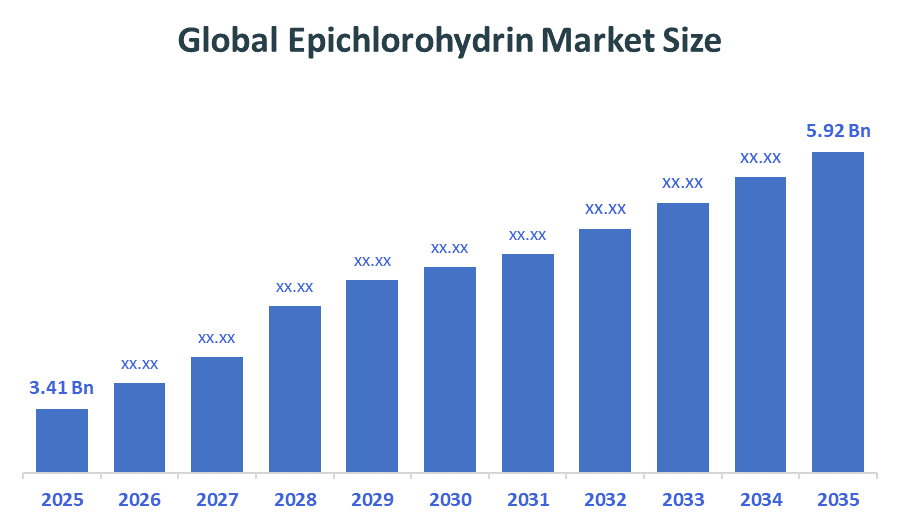

- Market Size (2025): USD 3.41 Billion

- Projected Market Size (2035): USD 5.92 Billion

- Compound Annual Growth Rate (CAGR): 6.67%

- Largest Regional Market: Asia-Pacific

- Fastest Growing Region: North America

- 3rd Largest Region: Europe

- Base Year: 2025

- Historical Period: 2021–2024

- Forecast Period: 2026–2035

According to Decision Advisors, the Global Epichlorohydrin Market Size is expected to grow from USD 3.41 billion in 2025 to USD 5.92 billion by 2035, at a CAGR of 6.67% during the forecast period 2025-2035. It is driven by the high demand for epoxy resins, which account for more than 68% of utilization in paints, coatings, construction, and electronics.

Market Overview/ Introduction

Epichlorohydrin is a colourless, volatile organochlorine compound with the chemical formula C?H?ClO. It is chiefly employed as a reactive intermediate in the synthesis of epoxy resins and other chemical derivatives, owing to its high reactivity and ability to form durable, corrosion-resistant polymers. The widespread use in the manufacture of epoxy resins, synthetic glycerin, and water treatment chemicals, the global epichlorohydrin market constitutes an essential part of the specialty chemicals sector. Epichlorohydrin is mainly used as a crucial precursor in the production of high-performance materials employed in various industries, including construction, automotive, electronics, and coatings. The market shows a steady growth in demand, bolstered by the development of infrastructure, increased use of advanced composites, and broader applications in adhesives and sealants.

- In November 2024, India imposed a five-year anti-dumping duty of up to USD 557 per ton on epichlorohydrin imports from China, South Korea, and Thailand, aiming to protect domestic producers, curb unfair pricing, and strengthen local manufacturing within the global epichlorohydrin market.

- In 2024, China’s epichlorohydrin production capacity reached approximately 2.215 million tons, marking a 20.91% year-on-year increase, significantly strengthening its global supply position and influencing pricing dynamics, trade flows, and capacity expansion trends within the global epichlorohydrin market.

Notable Insights: -

- Asia-Pacific holds the largest regional market share approximately 58% in the epichlorohydrin market.

- North America is the fastest growing region in the epichlorohydrin market the share of 45%.

- By type, oil-based epichlorohydrin segment is the dominating accounting for over 67% of the global market share in 2025.

- The compound annual growth rate of the epichlorohydrin is 6.67%.

- The market is likely to achieve a valuation of USD 5.92 billion by 2035.

What is role of technology in grooming the market?

Technology has emerged as a decisive force in sculpting the trajectory of the global epichlorohydrin market, underpinning both operational efficiency and strategic transformation across the value chain. The industry is witnessing a calibrated shift towards advanced, environmentally sustainable production methodologies, particularly the adoption of glycerin-based (bio-based) epichlorohydrin processes, which significantly curtail carbon emissions and reduce reliance on conventional petrochemical feedstock. Bio-based (glycerin-based) technologies now account for nearly 38% of global production, reflecting a clear transition toward environmentally responsible manufacturing. Simultaneously, the integration of process intensification techniques, automation, and real-time digital monitoring systems has enhanced manufacturing precision, optimized resource utilization, and lowered operational costs.

How is Recent Developments Helping the Market?

Recent developments are materially redefining the competitive landscape of the global epichlorohydrin market by fostering structural upgrades across production, supply chains, and end-use integration. Leading manufacturers are recalibrating their strategies through targeted capital expenditure in next-generation plants, with a clear emphasis on improving cost efficiencies and reducing environmental footprints. This wave of modernization is not only enhancing operational throughput but also enabling producers to offer differentiated, high-purity grades tailored to specialized industrial applications. Concurrently, the market is witnessing a discernible shift toward backward and forward integration, allowing companies to secure raw material access while strengthening their presence in high-growth downstream segments such as advanced coatings and specialty resins.

Market Drivers

A combination of structural and demand-side factors is driving the growth of the worldwide epichlorohydrin market. A key factor is the ongoing growth of the construction and infrastructure industries, which is increasing the use of epoxy resins in coatings, adhesives, and composites. Moreover, the increasing need for lightweight, high-performance materials from the automotive and electronics sectors is bolstering product adoption. The growing focus on water treatment solutions, especially in emerging economies, is further driving market growth. In addition, the sector is gaining from a slow shift to bio-based feedstocks, in accordance with worldwide sustainability requirements. The robust trends in industrialization, combined with developments in specialty chemicals, are jointly supporting a steady increase in demand across various end-use applications.

Restrain

The market faces notable constraints arising from volatility in raw material prices, particularly those linked to petrochemical derivatives, which can exert pressure on production economics. Additionally, stringent environmental regulations governing chlorinated compounds present compliance challenges for manufacturers. High capital intensity associated with advanced production technologies further limits entry of new players, while supply chain disruptions and fluctuating demand cycles continue to moderate overall market momentum.

Competitive Analysis:

The report offers the appropriate analysis of the key organizations/companies involved within the epichlorohydrin market, along with a comparative evaluation primarily based on their product of offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes product development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

Top Companies in Global Epichlorohydrin Market

- Solvay

- Sumitomo Chemical

- Olin Corporation

- Shandong Haili Chemical Industry

- Formosa Plastics

- Aditya Birla Chemicals,

- Hexion

- LOTTE Fine Chemical

- Jiangsu Yangnong Chemical

- Epigral Limited.

Government Initiatives

|

Country |

Key Government Initiatives |

|

India |

The Indian government’s “Make in India” initiative and infrastructure push have driven the establishment of domestic epichlorohydrin facilities by Epigral (formerly Meghmani) and DCM Shriram, significantly reducing import dependence and strengthening India’s position in the global epichlorohydrin market. |

|

US |

Environmental Regulation: Stringent U.S. EPA VOC regulations have significantly reduced industrial emissions, with anthropogenic VOC levels declining by nearly 87% across key sectors since 1990, while recent rules aim to cut emissions by 23,700 tons annually, accelerating adoption of bio-based epichlorohydrin from glycerol. |

|

China |

“Made in China 2025” drives chemical industry modernization, targeting approx. 70% domestic self-sufficiency in core materials by 2025, while China accounts for over 50% of global chemical output, promoting reduced import reliance and strengthening domestic epichlorohydrin production capacity within global markets. |

Market Segmentation

The epichlorohydrin market share is classified into type, application, and end use.

- The oil-based epichlorohydrin segment dominated the market in 2025, and is projected to grow at a substantial CAGR of approximately 67% during the forecast period.

Based on the type, the epichlorohydrin market is divided into oil-based epichlorohydrin, bio-based epichlorohydrin. Among these, the oil-based epichlorohydrin segment dominated the market in 2025, and is projected to grow at a substantial CAGR of approximately 67% during the forecast period. The traditional production route, which relies on propylene as a raw material, has been established for decades. Due to the presence of large-scale, efficient production plants that are well-established, it is challenging for new bio-based technologies on a smaller scale to immediately dominate the market. Oil-based epichlorohydrin is a dependable source for producing robust epoxy resins needed in applications that are demanding and take place in severe environments.

- The epoxy resins segment accounted for the largest share in 2025, and is anticipated to grow at a significant CAGR of approximately 74% during the forecast period.

Based on the application, the epichlorohydrin market is divided into epoxy resins, specialty water treatment chemicals, and others. Among these, the epoxy resins segment accounted for the largest share in 2025, and is anticipated to grow at a significant CAGR of approximately 74% during the forecast period. This segment is the main market driver, using epichlorohydrin to produce coatings, adhesives, and composites. Growth is bolstered by demand from the construction, automotive, and wind energy sectors. They are employed for purifying water and processing industrial waste, constituting a stable and considerable market segment.

- The construction segment dominated the market in 2025, and is projected to grow at a substantial CAGR of approximately 39% during the forecast period.

Based on the end use, the epichlorohydrin market is divided into construction, paints and coatings, adhesives, and others. Among these, the construction segment dominated the market in 2025, and is projected to grow at a substantial CAGR of approximately 39% during the forecast period. The demand for long-lasting materials such as epoxy resin-based concrete flooring, protective coatings for metal structures, and grouting is being fueled by large-scale urbanization initiatives, especially in India and Southeast Asia. Due to their exceptional chemical resistance, durability, and strong adhesion in harsh environments (such as pipelines and floor coatings), epichlorohydrin-derived epoxy formulations are selected for construction applications.

Strategies to Implement for Growth of the Market in Non-Leading Regions

To unlock growth in non-leading regions, a tailored, region-specific strategy focused on accessibility, adaptability, and long-term value creation is essential. To cut logistics costs and enhance responsiveness to regional demand patterns, companies should give priority to setting up localized manufacturing or blending facilities. Establishing strategic partnerships with domestic distributors and industry players can improve market penetration and credibility. It is equally crucial to tailor product offerings to fit local regulatory frameworks and end-use requirements, especially in industries like construction and water treatment. By closing knowledge gaps, investment in customer education initiatives and technical support services can further expedite adoption. Moreover, taking advantage of government incentives and infrastructure development initiatives in developing economies can foster an environment suitable for ongoing growth and competitive establishment.

A Study on the Supply, Demand, Distribution, and Market Environment

A statistical assessment of the epichlorohydrin market highlights a structured alignment between supply, demand, and distribution dynamics. Globally, production capacity has surpassed 2.5 million tons annually, with Asia-Pacific accounting for over 60% of total output, led by China. On the demand side, epoxy resins contribute nearly 65–70% of total consumption, followed by water treatment chemicals at approximately 15% share. In terms of distribution, nearly 55% of supply is consumed domestically within producing regions, while 45% enters international trade flows. Additionally, bio-based production routes now represent over 35% of total capacity, reflecting a gradual shift toward sustainable manufacturing. These figures collectively indicate a market characterized by regional concentration, steady industrial demand, and evolving supply chain efficiencies.

Regional Segment Analysis of the Epichlorohydrin Market

- North America (U.S., Canada, Mexico)

- Europe (Germany, France, U.K., Italy, Spain, Rest of Europe)

- Asia-Pacific (China, Japan, India, Rest of APAC)

- South America (Brazil and the Rest of South America)

- The Middle East and Africa (UAE, South Africa, Rest of MEA)

Asia Pacific is anticipated to hold the largest share of approximately 58% of the epichlorohydrin market over the predicted timeframe. It is attributed because China stands as the largest worldwide producer and consumer of epichlorohydrin, marked by substantial capacity growth (exceeding 600 kilotons per year) and increasing investments in glycerin-based technology. India's high growth is driven by its expanding manufacturing base and dependence on imports to satisfy demand, which is increasing at a CAGR of 5.8%. The demand for paints, coatings, and construction materials has risen significantly due to government investments in infrastructure and urbanization in China and India, with epichlorohydrin serving as an essential raw material.

North America is expected to grow at a rapid CAGR of approximately 45% in the epichlorohydrin market during the forecast period. The demand for epichlorohydrin-derived resins is being driven by significant investments in infrastructure projects across North America and by the growth of the renewable energy sector, particularly with respect to wind energy. A substantial quantity of epoxy resins is used in wind turbine blades. Producers are moving from petrochemical to bio-based ECH derived from glycerin (a biodiesel by product), which decreases dependence on fluctuating propylene prices and addresses the need for eco-friendly production.

Europe is the 3rd largest region to grow at a rapid CAGR of approximately 38% in the epichlorohydrin market during the region. The region is motivated by a move toward sustainable "green" chemistry, significant demand from the construction and automotive industries, and a robust shift toward bio-based production techniques. With around 62% of its production derived from glycerin processes in accordance with EU sustainability goals, Europe is at the forefront of bio-based ECH adoption. Manufacturers are being driven to shift from conventional petrochemical-based ECH to eco-friendly, bio-based alternatives (glycerin-to-ECH) due to stringent environmental regulations (like REACH) and the EU Green Deal.

Future Market Trends in Epichlorohydrin Market: -

- Emergence of Bio-based Production:

Producers are transitioning from petroleum-derived propylene to more sustainable, bio-based approaches, especially those that use glycerin, in order to decrease carbon emissions and comply with stricter environmental regulations.

- Asia-Pacific Dominance & Expansion:

The region continues to be the fastest-growing area, propelled by increasing demand from the electronic manufacturing, infrastructure development, and automotive sectors, led by China, India, and Taiwan.

- Expansion of Epoxy Resins:

Epoxy resins are the main driver of market growth, with high-performance demand in applications such as wind turbine blades, paints and coatings, and electric vehicle composites.

Recent Development

- In December 2024, Hexion is expanding bio-based epichlorohydrin capacity by 25,000 metric tons in the Netherlands, strengthening sustainable supply. Meanwhile, Covestro has partnered with Neste to advance renewable feedstock adoption across polymer production value chains.

- In November 2024, Epigral Limited’s board approved a plan to double epichlorohydrin (ECH) capacity at its Dahej facility in Gujarat to 100,000 TPA by adding 50,000 TPA, supporting rising domestic and global demand.

- In March 2024, Mitsubishi Chemical reportedly introduced advanced catalyst technology to enhance chlorohydrin process efficiency, reducing energy consumption by around 15% and supporting more sustainable epichlorohydrin production, though detailed public confirmation remains limited.

Market Segment

This study forecasts revenue at global, regional, and country levels from 2020 to 2035. Decision Advisor has segmented the epichlorohydrin market based on the below-mentioned segments:

Global Epichlorohydrin Market, By Type

- Oil-Based Epichlorohydrin

- Bio-Based Epichlorohydrin

Global Epichlorohydrin Market, By Application

- Epoxy Resins

- Specialty Water Treatment Chemicals

- Others

Global Epichlorohydrin Market, By End Use

- Construction

- Paints and Coatings

- Adhesives

- Others

Global Epichlorohydrin Market, By Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa

Frequently Asked Questions (FAQ)

1. How is the evolving feedstock landscape influencing cost structures in the epichlorohydrin market?

The transition from propylene-based to glycerin-based feedstocks is gradually reshaping cost dynamics. While bio-based routes initially involve higher capital investment, they offer long-term stability by reducing exposure to volatile crude-linked pricing, thereby improving margin predictability.

2. What role does capacity concentration in Asia-Pacific play in shaping global trade flows?

With Asia-Pacific contributing over 58% of global share and a dominant production base, the region significantly influences export pricing, supply availability, and trade balances, making it a critical hub for global distribution networks.

3. How are environmental compliance requirements impacting production strategies?

Stringent environmental regulations are compelling manufacturers to adopt cleaner technologies, invest in emission control systems, and transition toward sustainable production methods, thereby increasing operational complexity but enhancing long-term competitiveness.

4. In what ways does downstream industry diversification support market resilience?

The wide applicability of epichlorohydrin across construction, electronics, water treatment, and coatings ensures demand diversification, reducing dependency on a single sector and enhancing overall market stability during economic fluctuations.

5. How is technological innovation in epoxy resins influencing product demand?

Advancements in epoxy formulations, particularly for high-performance and lightweight applications, are expanding usage in wind energy, automotive composites, and electronics, thereby sustaining robust demand for epichlorohydrin.

- Introduction

- Objectives of the Study

- Market Definition

- Research Scope

- Research Methodology and Assumptions

- Executive Summary

- Premium Insights

- Porter’s Five Forces Analysis

- Value Chain Analysis

- Top Investment Pockets

- Market Attractiveness Analysis By Type

- Market Attractiveness Analysis By Application

- Market Attractiveness Analysis By End-Use

- Market Attractiveness Analysis By Region

- Industry Trends

- Market Dynamics

- Market Evaluation

- Drivers

- High Demand for epoxy resins used in coatings

- Restraints

- Stringent environmental regulation on toxic wastewater

- Opportunities

- Bio based ECH production

- Challenges

- Robust demand for epoxy resins in construction

- Global Epichlorohydrin Market Analysis and Projection, By Type

- Segment Overview

- Oil-Based Epichlorohydrin

- Bio-Based Epichlorohydrin

- Global Epichlorohydrin Market Analysis and Projection, By Application

- Segment Overview

- Epoxy Resins

- Specialty Water Treatment Chemicals

- Others

- Global Epichlorohydrin Market Analysis and Projection, By End-Use

- Segment Overview

- Construction

- Paints and Coatings

- Adhesives

- Others

- Global Epichlorohydrin Market Analysis and Projection, By Regional Analysis

- Segment Overview

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Asia-Pacific

- Japan

- China

- India

- South America

- Brazil

- Middle East and Africa

- UAE

- South Africa

- Global Epichlorohydrin Market-Competitive Landscape

- Overview

- Market Share of Key Players in the Epichlorohydrin Market

- Global Company Market Share

- North America Company Market Share

- Europe Company Market Share

- APAC Company Market Share

- Competitive Situations and Trends

- Coverage Launches and Developments

- Partnerships, Collaborations, and Agreements

- Mergers & Acquisitions

- Expansions

- Company Profiles

- Solvay

- Business Overview

- Company Snapshot

- Company Market Share Analysis

- Company Coverage Portfolio

- Recent Developments

- SWOT Analysis

- Sumitomo Chemical

- Business Overview

- Company Snapshot

- Company Market Share Analysis

- Company Coverage Portfolio

- Recent Developments

- SWOT Analysis

- Olin Corporation

- Business Overview

- Company Snapshot

- Company Market Share Analysis

- Company Coverage Portfolio

- Recent Developments

- SWOT Analysis

- Shandong Haili Chemical Industry

- Business Overview

- Company Snapshot

- Company Market Share Analysis

- Company Coverage Portfolio

- Recent Developments

- SWOT Analysis

- Formosa Plastics

- Business Overview

- Company Snapshot

- Company Market Share Analysis

- Company Coverage Portfolio

- Recent Developments

- SWOT Analysis

- Aditya Birla Chemicals

- Business Overview

- Company Snapshot

- Company Market Share Analysis

- Company Coverage Portfolio

- Recent Developments

- SWOT Analysis

- Hexion

- Business Overview

- Company Snapshot

- Company Market Share Analysis

- Company Coverage Portfolio

- Recent Developments

- SWOT Analysis

- LOTTE Fine Chemical

- Business Overview

- Company Snapshot

- Company Market Share Analysis

- Company Coverage Portfolio

- Recent Developments

- SWOT Analysis

- Jiangsu Yangnong Chemical

- Business Overview

- Company Snapshot

- Company Market Share Analysis

- Company Coverage Portfolio

- Recent Developments

- SWOT Analysis

- Epigral Limited

- Business Overview

- Company Snapshot

- Company Market Share Analysis

- Company Coverage Portfolio

- Recent Developments

- SWOT Analysis

- Solvay

List of Table

- Global Epichlorohydrin Market, By Type, 2024-2035(USD Billion)

- Global Oil-Based Epichlorohydrin, Epichlorohydrin Market, By Region, 2024-2035(USD Billion)

- Global Bio-Based Epichlorohydrin, Epichlorohydrin Market, By Region, 2024-2035(USD Billion)

- Global Epichlorohydrin Market, By Application, 2024-2035(USD Billion)

- Global Epoxy Resins, Epichlorohydrin Market, By Region, 2024-2035(USD Billion)

- Global Specialty Water Treatment Chemicals, Epichlorohydrin Market, By Region, 2024-2035(USD Billion)

- Global Others, Epichlorohydrin Market, By Region, 2024-2035(USD Billion)

- Global Epichlorohydrin Market, By End-Use, 2024-2035(USD Billion)

- Global Construction, Epichlorohydrin Market, By Region, 2024-2035(USD Billion)

- Global Paints and Coatings, Epichlorohydrin Market, By Region, 2024-2035(USD Billion)

- Global Adhesives, Epichlorohydrin Market, By Region, 2024-2035(USD Billion)

- Global Others, Epichlorohydrin Market, By Region, 2024-2035(USD Billion)

- North America Epichlorohydrin Market, By Type, 2024-2035(USD Billion)

- North America Epichlorohydrin Market, By Application, 2024-2035(USD Billion)

- North America Epichlorohydrin Market, By End-Use, 2024-2035(USD Billion)

- U.S. Epichlorohydrin Market, By Type, 2024-2035(USD Billion)

- U.S. Epichlorohydrin Market, By Application, 2024-2035(USD Billion)

- U.S. Epichlorohydrin Market, By End-Use, 2024-2035(USD Billion)

- Canada Epichlorohydrin Market, By Type, 2024-2035(USD Billion)

- Canada Epichlorohydrin Market, By Application, 2024-2035(USD Billion)

- Canada Epichlorohydrin Market, By End-Use, 2024-2035(USD Billion)

- Mexico Epichlorohydrin Market, By Type, 2024-2035(USD Billion)

- Mexico Epichlorohydrin Market, By Application, 2024-2035(USD Billion)

- Mexico Epichlorohydrin Market, By End-Use, 2024-2035(USD Billion)

- Europe Epichlorohydrin Market, By Type, 2024-2035(USD Billion)

- Europe Epichlorohydrin Market, By Application, 2024-2035(USD Billion)

- Europe Epichlorohydrin Market, By End-Use, 2024-2035(USD Billion)

- Germany Epichlorohydrin Market, By Type, 2024-2035(USD Billion)

- Germany Epichlorohydrin Market, By Application, 2024-2035(USD Billion)

- Germany Epichlorohydrin Market, By End-Use, 2024-2035(USD Billion)

- France Epichlorohydrin Market, By Type, 2024-2035(USD Billion)

- France Epichlorohydrin Market, By Application, 2024-2035(USD Billion)

- France Epichlorohydrin Market, By End-Use, 2024-2035(USD Billion)

- U.K. Epichlorohydrin Market, By Type, 2024-2035(USD Billion)

- U.K. Epichlorohydrin Market, By Application, 2024-2035(USD Billion)

- U.K. Epichlorohydrin Market, By End-Use, 2024-2035(USD Billion)

- Italy Epichlorohydrin Market, By Type, 2024-2035(USD Billion)

- Italy Epichlorohydrin Market, By Application, 2024-2035(USD Billion)

- Italy Epichlorohydrin Market, By End-Use, 2024-2035(USD Billion)

- Spain Epichlorohydrin Market, By Type, 2024-2035(USD Billion)

- Spain Epichlorohydrin Market, By Application, 2024-2035(USD Billion)

- Spain Epichlorohydrin Market, By End-Use, 2024-2035(USD Billion)

- Asia Pacific Epichlorohydrin Market, By Type, 2024-2035(USD Billion)

- Asia Pacific Epichlorohydrin Market, By Application, 2024-2035(USD Billion)

- Asia Pacific Epichlorohydrin Market, By End-Use, 2024-2035(USD Billion)

- Japan Epichlorohydrin Market, By Type, 2024-2035(USD Billion)

- Japan Epichlorohydrin Market, By Application, 2024-2035(USD Billion)

- Japan Epichlorohydrin Market, By End-Use, 2024-2035(USD Billion)

- China Epichlorohydrin Market, By Type, 2024-2035(USD Billion)

- China Epichlorohydrin Market, By Application, 2024-2035(USD Billion)

- China Epichlorohydrin Market, By End-Use, 2024-2035(USD Billion)

- India Epichlorohydrin Market, By Type, 2024-2035(USD Billion)

- India Epichlorohydrin Market, By Application, 2024-2035(USD Billion)

- India Epichlorohydrin Market, By End-Use, 2024-2035(USD Billion)

- South America Epichlorohydrin Market, By Type, 2024-2035(USD Billion)

- South America Epichlorohydrin Market, By Application, 2024-2035(USD Billion)

- South America Epichlorohydrin Market, By End-Use, 2024-2035(USD Billion)

- Brazil Epichlorohydrin Market, By Type, 2024-2035(USD Billion)

- Brazil Epichlorohydrin Market, By Application, 2024-2035(USD Billion)

- Brazil Epichlorohydrin Market, By End-Use, 2024-2035(USD Billion)

- The Middle East and Africa Epichlorohydrin Market, By Type, 2024-2035(USD Billion)

- The Middle East and Africa Epichlorohydrin Market, By Application, 2024-2035(USD Billion)

- The Middle East and Africa Epichlorohydrin Market, By End-Use, 2024-2035(USD Billion)

- UAE Epichlorohydrin Market, By Type, 2024-2035(USD Billion)

- UAE Epichlorohydrin Market, By Application, 2024-2035(USD Billion)

- UAE Epichlorohydrin Market, By End-Use, 2024-2035(USD Billion)

- South Africa Epichlorohydrin Market, By Type, 2024-2035(USD Billion)

- South Africa Epichlorohydrin Market, By Application, 2024-2035(USD Billion)

- South Africa Epichlorohydrin Market, By End-Use, 2024-2035(USD Billion)

List of Figures

- Global Epichlorohydrin Market Segmentation

- Epichlorohydrin Market: Research Methodology

- Market Size Estimation Methodology: Bottom-Up Approach

- Market Size Estimation Methodology: Top-down Approach

- Data Triangulation

- Porter’s Five Forces Analysis

- Value Chain Analysis

- Top investment pocket in the Epichlorohydrin Market

- Top Winning Strategies, 2024-2035

- Top Winning Strategies, By Development, 2024-2035(%)

- Top Winning Strategies, By Company, 2024-2035

- Moderate Bargaining power of Buyers

- Moderate Bargaining power of Suppliers

- Moderate Bargaining power of New Entrants

- Low threat of Substitution

- High Competitive Rivalry

- Top Player Positioning, 2024

- Market Share Analysis, 2024

- Restraint and Drivers: Epichlorohydrin Market

- Epichlorohydrin Market Segmentation, By Type

- Epichlorohydrin Market For Oil-Based Epichlorohydrin, By Region, 2024-2035 ($ Billion)

- Epichlorohydrin Market For Bio-Based Epichlorohydrin, By Region, 2024-2035 ($ Billion)

- Epichlorohydrin Market Segmentation, By Application

- Epichlorohydrin Market For Epoxy Resins, By Region, 2024-2035 ($ Billion)

- Epichlorohydrin Market For Specialty Water Treatment Chemicals, By Region, 2024-2035 ($ Billion)

- Epichlorohydrin Market For Others, By Region, 2024-2035 ($ Billion)

- Epichlorohydrin Market Segmentation, By End-Use

- Epichlorohydrin Market For Construction, By Region, 2024-2035 ($ Billion)

- Epichlorohydrin Market For Paints and Coatings, By Region, 2024-2035 ($ Billion)

- Epichlorohydrin Market For Adhesives, By Region, 2024-2035 ($ Billion)

- Epichlorohydrin Market For Others, By Region, 2024-2035 ($ Billion)

- Solvay: Net Sales, 2024-2035 ($ Billion)

- Solvay: Revenue Share, By Segment, 2024 (%)

- Solvay: Revenue Share, By Region, 2024 (%)

- Sumitomo Chemical: Net Sales, 2024-2035 ($ Billion)

- Sumitomo Chemical: Revenue Share, By Segment, 2024 (%)

- Sumitomo Chemical: Revenue Share, By Region, 2024 (%)

- Olin Corporation: Net Sales, 2024-2035 ($ Billion)

- Olin Corporation: Revenue Share, By Segment, 2024 (%)

- Olin Corporation: Revenue Share, By Region, 2024 (%)

- Shandong Haili Chemical Industry: Net Sales, 2024-2035 ($ Billion)

- Shandong Haili Chemical Industry: Revenue Share, By Segment, 2024 (%)

- Shandong Haili Chemical Industry: Revenue Share, By Region, 2024 (%)

- Formosa Plastics: Net Sales, 2024-2035 ($ Billion)

- Formosa Plastics: Revenue Share, By Segment, 2024 (%)

- Formosa Plastics: Revenue Share, By Region, 2024 (%)

- Aditya Birla Chemicals: Net Sales, 2024-2035 ($ Billion)

- Aditya Birla Chemicals: Revenue Share, By Segment, 2024 (%)

- Aditya Birla Chemicals: Revenue Share, By Region, 2024 (%)

- Hexion: Net Sales, 2024-2035 ($ Billion)

- Hexion: Revenue Share, By Segment, 2024 (%)

- Hexion: Revenue Share, By Region, 2024 (%)

- LOTTE Fine Chemical: Net Sales, 2024-2035 ($ Billion)

- LOTTE Fine Chemical: Revenue Share, By Segment, 2024 (%)

- LOTTE Fine Chemical: Revenue Share, By Region, 2024 (%)

- Jiangsu Yangnong Chemical.: Net Sales, 2024-2035 ($ Billion)

- Jiangsu Yangnong Chemical.: Revenue Share, By Segment, 2024 (%)

- Jiangsu Yangnong Chemical.: Revenue Share, By Region, 2024 (%)

- Epigral Limited: Net Sales, 2024-2035 ($ Billion)

- Epigral Limited: Revenue Share, By Segment, 2024 (%)

- Epigral Limited: Revenue Share, By Region, 2024 (%)

Check Licence

Choose the plan that fits you best: Single User, Multi-User, or Enterprise solutions tailored for your needs.

We Have You Covered

- 24/7 Analyst Support

- Clients Across the Globe

- Tailored Insights

- Technology Tracking

- Competitive Intelligence

- Custom Research

- Syndicated Market Studies

- Market Overview

- Market Segmentation

- Growth Drivers

- Market Opportunities

- Regulatory Insights

- Innovation & Sustainability

Report Details

| Scope | Global |

| Pages | 195 |

| Delivery | PDF & Excel via Email |

| Language | English |

| Release | Apr 2026 |

| Access | Download from this page |