Global Etanercept Market

Global Etanercept Market Size, Share, By Indication (Rheumatoid Arthritis, Psoriatic Arthritis, Ankylosing Spondylitis), By Dosage Form (Vials, Prefilled Syringes, Prefilled Pens / Autoinjectors), By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies), and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East & Africa), Analysis and Forecast 2026?2035

CAGR

16.86%

REVENUE 2025

USD Million 18421.67

FORECAST 2035

USD Million 87503.05

REPORT COVERAGE

Global

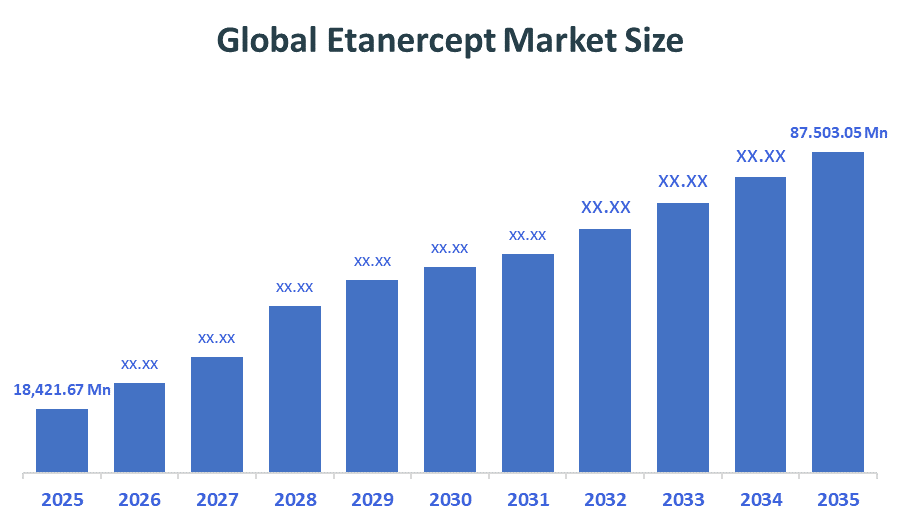

The Global Etanercept Market size is forecast to grow from USD 18,421.67 Million in 2025 to approximately USD 87,503.05 Million by 2035. According to Decision Advisors, a detailed research report on the etanercept market indicates that the biosimilars dominate the market, accounting for approximately 70-80% of the total share globally. Sandoz leads the market with an estimated 35-40% global market share. The company reported a 2025 revenue of approximately USD 700-875 million, making it one of the most influential forces shaping industry trends and overall market growth.

Market Snapshot

- Global Etanercept Market Size (2025): USD 18,421.67 Million

- Projected Global Etanercept Market Size (2035): USD 87,503.05 Million

- Global Etanercept Market Compound Annual Growth Rate (CAGR): 16.86%

- Largest Regional Market: North America

- Fastest Growing Region: Asia-Pacific

- 2nd Largest Region: Europe

- Base Year: 2025

- Historical Period: 2021–2024

- Forecast Period: 2026–2035

Market Overview/ Introduction

The Global Etanercept Market refers to revenue and volumes associated with etanercept and its biosimilars, a biologic TNFalpha inhibitor, used to treat chronic inflammatory autoimmune conditions and prescribed through specific distribution channels. Etanercept is a recombinant fusion protein designed to target TNF; TNF inhibitors are an immunology biologic category that includes etanercept; a biosimilar is a biologically similar medicine that has no clinically meaningful differences when compared with the originator; an autoinjector/prefilled syringe is a type of device that allows the medication to be self-injected. Emerging market access, expanded affordability by payers/tiered pricing strategy, differentiation via device (improves adherence), regional fill-finish to overcome supply limitations, and access through real-world evidence for switching and formulary success remain as future opportunities. This market is critical as it caters to diseases with a high burden (RA, PsA, AS); it expands the biologic arena, making it affordable to a wider range of people, it drives the immunology pricing and access strategies globally.

- EU/EEA governments drive etanercept access mainly through biosimilar policies: centralized or hospital-level tendering, prescribing guidance, and switching frameworks that encourage use of lower-cost biosimilars while maintaining pharmacovigilance. These schemes increase etanercept volumes but reduce prices, reshaping market value.

- In the UK, NHS England’s commissioning framework promotes best-value biologic use, including biosimilar adoption, supported switching, and reinvestment of savings into patient care. For etanercept, this has historically accelerated migration from originator to biosimilars via hospital prescribing and pharmacy-led switching programs, improving access and controlling budgets.

Notable Insights: -

- North America is anticipated to hold the largest share of approximately 45% in the etanercept market over the forecast period.

- Asia Pacific is expected to grow at a rapid CAGR of approximately 12% in the etanercept market during the forecast period.

- The rheumatoid arthritis segment dominated the market in 2025, approximately 60%, and is projected to grow at a substantial CAGR during the forecast period.

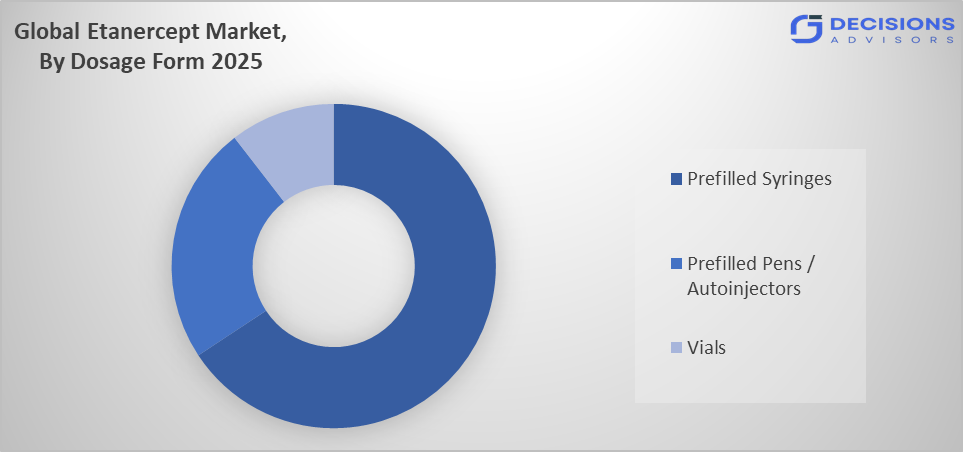

- The prefilled syringes segment dominated the market in 2025, approximately 70%, and is projected to grow at a substantial CAGR during the forecast period.

- The hospital pharmacies segment dominated the market in 2025, approximately 50%, and is projected to grow at a substantial CAGR during the forecast period.

- The compound annual growth rate of the Global Etanercept Market is 16.86%.

- The market is likely to achieve a valuation of USD 87,503.05 Million by 2035.

What is role of technology in grooming the market?

Technology is shaping the global etanercept market by improving product quality, access, and patient outcomes. Advances in biologics manufacturing (cell-line engineering, single-use bioreactors, continuous monitoring, and analytics) increase yields, reduce contamination risk, and lower cost, supporting broader biosimilar adoption. Device innovation (prefilled pens/autoinjectors, ergonomic designs, needle shielding) improves self-injection experience and adherence. Cold-chain and track-and-trace technologies (IoT temperature loggers, serialization) reduce distribution losses and strengthen supply integrity. Digital health tools, apps, tele-rheumatology, e-prescribing, and remote patient monitoring support initiation, training, refill reminders, and persistence. Real-world data platforms and AI-driven analytics help demonstrate comparative effectiveness and value, aiding payer negotiations and formulary access.

Market Drivers

The global market for dextrose injections is driven by the rising prevalence and improved diagnosis of autoimmune diseases such as rheumatoid arthritis, psoriatic arthritis, and ankylosing spondylitis. Long-term disease management needs to sustain biologic demand, supported by strong clinical evidence and physician familiarity with TNF inhibitors. Expanding reimbursement coverage and specialty pharmacy networks improve patient access, while the growth of biosimilars reduces costs and broadens the treatable population, especially in price-sensitive regions. Patient preference for convenient self-administration (prefilled syringes and autoinjector pens) and adherence-support programs also contribute to continued utilization.

Restrain

The Global Etanercept market faces restraints due to intense biosimilar price erosion, aggressive tendering and payer-driven switching, and competition from newer biologics and oral targeted therapies. Regulatory and pharmacovigilance requirements raise costs, while cold-chain logistics and supply complexity limit access in emerging markets and constrain consistent uptake.

Competitive Analysis:

The report offers the appropriate analysis of the key organizations/companies involved within the global etanercept market, along with a comparative evaluation primarily based on their product offerings, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes product development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

Top Companies in Global Etanercept Market

- Pfizer

- Sandoz

- Samsung Bioepis

- Celltrion

- Viatris

- Biocon

- Hisun Pharmaceutical

- Shanghai CP Goujian Pharmaceutical

- Dr. Reddy’s Laboratories

- Biocad

Government Initiatives

|

Country |

Key Government Initiatives |

|

USA |

The FDA launched a pilot program in October 2025 to fast-track approvals for domestic generic drugs and APIs. This initiative incentivizes U.S.-based bioequivalence testing and manufacturing to reduce foreign dependence and lower treatment costs for biologics. |

|

India |

The Union Budget 2026 introduced the ?10,000 crore Biopharma SHAKTI initiative. It aims to build a self-reliant ecosystem for biosimilar production, establish 1,000+ accredited clinical trial sites, and upgrade regulatory capacity (CDSCO) to match global standards. |

|

China |

In December 31, 2025, the State Council revised the Drug Administration Law to accelerate approval pathways for innovative biological products. The update focuses on lifecycle regulation, encouraging advanced biologics manufacturing and localized innovation in complex therapies. |

Study on the Supply, Demand, Distribution, and Market Environment of the Etanercept Market

The supply of Etanercept is robust, dominated by the reference product and multiple globally approved biosimilars, though manufacturing complexity and cold-chain logistics create supply chain vulnerabilities. Demand is strong and growing, fueled by the high global prevalence of autoimmune diseases (RA, PsA, AS) and expanding diagnostic awareness, but is price-elastic and constrained by reimbursement in cost-sensitive regions. Distribution is multi-tiered: hospital pharmacies initiate therapy, while retail, specialty, and online pharmacies manage chronic refills, with cold-chain integrity being paramount. The market environment is intensely competitive, defined by aggressive biosimilar driven price erosion, complex payer negotiations, and mandatory substitution policies in Europe, creating a high-volume, low-margin landscape where patient support programs are critical differentiators.

Price Analysis and Consumer Behaviour Analysis

Price Analysis: The Etanercept market is defined by severe price erosion due to biosimilar competition, particularly in Europe and the US. In Europe, aggressive tender-based procurement and mandated substitution have slashed reference product prices by approximately 70-80%. In the US, list prices remain high, but significant confidential rebates and patient copay assistance create a complex, lower net price landscape. This price compression is a primary driver for market volume growth, as lower costs enable broader patient access and formulary placement, especially in cost-sensitive public health systems. Consumer Behaviour Analysis: Physician prescribing is increasingly driven by payer formulary restrictions and biosimilar mandates, reducing brand loyalty. Patient choice is heavily influenced by out-of-pocket costs and copay programs. A critical behavioural trend is "therapeutic inertia" physicians and patients may resist switching from a known reference brand to a biosimilar due to perceived efficacy/safety concerns, despite regulatory equivalence. Success therefore hinges on robust patient support programs (PSPs) that improve adherence, manage injection anxiety, and provide financial navigation to overcome switching hesitancy and ensure consistent therapy use.

Market Segmentation

The Etanercept Market share is classified into indication, dosage form, and distribution channel.

- The rheumatoid arthritis segment dominated the market in 2025, approximately 60%, and is projected to grow at a substantial CAGR during the forecast period.

Based on the indication, the etanercept market is divided into rheumatoid arthritis, psoriatic arthritis, and ankylosing spondylitis. Among these, the rheumatoid arthritis segment dominated the market in 2025, approximately 60%, and is projected to grow at a substantial CAGR during the forecast period. The growth of the rheumatoid arthritis segment is growing because it is the most routinely used strength for general IV therapy. It is widely stocked for maintenance fluids, mild calorie supplementation, and as a common diluent for IV drugs. High procedure volumes and broad hospital protocols keep D5W demand consistently high.

- The prefilled syringes segment dominated the market in 2025, approximately 70%, and is projected to grow at a substantial CAGR during the forecast period.

Based on the dosage form, the etanercept market is divided into vials, prefilled syringes, and prefilled pens/autoinjectors. Among these, the prefilled syringes segment dominated the market in 2025, approximately 70%, and is projected to grow at a substantial CAGR during the forecast period. The prefilled syringes segment dominated due to their convenience, accuracy, and established patient trust. They eliminate the complexity and potential dosing errors of vial reconstitution. While autoinjector pens offer similar ease-of-use, prefilled syringes have a longer market history, broader global availability, and often a lower cost point, making them the default choice for most patients and payers.

- The hospital pharmacies segment dominated the market in 2025, approximately 50%, and is projected to grow at a substantial CAGR during the forecast period.

Based on the distribution channel, the etanercept market is divided into hospital pharmacies, retail pharmacies, and online pharmacies. Among these, the hospital pharmacies segment dominated the market in 2025, approximately 50%, and is projected to grow at a substantial CAGR during the forecast period. The growth of the hospital pharmacies segment is because high-cost biologic therapy. Rheumatologists and specialists typically prescribe and often administer the first doses in a hospital or clinic setting. These pharmacies manage complex prior authorizations, patient support programs, and cold-chain logistics. While retail and online channels handle maintenance refills, the critical first prescription and monitoring flow through hospitals.

Strategies to Implement for Growth of the Market in Non-Leading Regions

To grow the global etanercept market in non-leading regions, companies should prioritize affordability and access, expand biosimilar portfolios, use tiered pricing, and partner with governments/payers for formulary inclusion and risk-sharing agreements. Strengthen distribution by building cold-chain logistics, contracting specialty distributors, and improving last?mile delivery. Invest in physician and patient education to accelerate diagnosis and guideline-based biologic use, supported by real-world evidence demonstrating value versus alternatives. Offer device-led differentiation (prefilled pens/autoinjectors), training, and adherence programs to increase persistence. Localize manufacturing or fill-finish to reduce costs and improve supply security. Finally, pursue indication expansion and faster regulatory approvals with strong pharmacovigilance and transparent quality messaging to build trust.

Regional Segment Analysis of the Etanercept Market

- North America (U.S., Canada, Mexico)

- Europe (Germany, France, U.K., Italy, Spain, Rest of Europe)

- Asia-Pacific (China, Japan, India, Rest of APAC)

- South America (Brazil and the Rest of South America)

- The Middle East and Africa (UAE, South Africa, Rest of MEA)

North America is anticipated to hold the largest share of approximately 45% the etanercept market over the forecast period.

North America is anticipated to hold the largest share of approximately 45% the etanercept market over the forecast period. The dominance of this region is primarily driven by high biologics utilization, higher per-patient drug spending, and strong reimbursement coverage. Early adoption of TNF inhibitors, large diagnosed and treated autoimmune populations, and well-established specialty pharmacy and cold-chain distribution also support sustained volumes. The U.S. remains the key revenue contributor.

Asia Pacific is expected to grow at a rapid CAGR of approximately 12% in the etanercept market during the forecast period.

Asia Pacific is expected to grow at a rapid CAGR of approximately 12% in the etanercept market during the forecast period. This growth is driven by expanding diagnosis and treatment of autoimmune diseases, improving healthcare access, and increasing biologics penetration in major markets such as China and India. Growth is further supported by rising insurance coverage, hospital capacity, and availability of lower-cost biosimilars, which accelerates uptake and broadens the treated patient base.

Europe is the 2nd largest region to grow in the etanercept market during the period.

Europe is the second-largest region in the etanercept market because it has a substantial diagnosed population for rheumatoid arthritis, psoriatic arthritis, and ankylosing spondylitis, along with mature healthcare infrastructure and broad access to biologic therapies. Strong clinical adoption and established prescribing pathways sustain demand. At the same time, widespread biosimilar availability supports higher treatment volumes despite price pressures.

Future Market Trends in Global Etanercept Market: -

1. Rising Adoption of Biosimilars

One of the most significant future trends in the global etanercept market is the rapid growth of biosimilars. Increasing patent expirations and cost pressures are encouraging healthcare systems to adopt lower-cost alternatives. Biosimilars offer comparable efficacy at reduced prices, improving patient access and driving competition. This shift is expected to reshape pricing strategies and significantly expand market penetration worldwide.

2. Increasing Prevalence of Autoimmune Diseases

The growing global burden of autoimmune disorders such as rheumatoid arthritis and psoriasis is a major trend fueling demand for etanercept therapies. Improved diagnosis rates, aging populations, and lifestyle factors are contributing to higher patient pools. As a result, demand for effective long-term biologic treatments is increasing, positioning etanercept as a key therapeutic option in immunology.

3. Shift Toward Advanced and Patient-Centric Treatment Approaches

Future trends include the adoption of patient-friendly drug delivery systems, home-based treatment, and integration of digital health technologies. Innovations such as self-injection devices and personalized therapies are enhancing patient adherence and convenience. Additionally, ongoing research in biomarkers and combination therapies is expected to improve treatment outcomes and expand the clinical applications of etanercept globally.

Recent Development

- In July 2025, Product Launch: Biocon Biologics introduced Nepexto, an etanercept biosimilar, in Australia, expanding its global footprint and increasing competition in the etanercept biosimilars market, while improving affordability and treatment availability.

- In May 2024, Lupin and Sandoz jointly launched Rymti, an etanercept biosimilar, in Canada following regulatory approval. The launch aimed to broaden patient access to affordable biologic therapy for autoimmune conditions like rheumatoid arthritis, strengthening the companies' biosimilar footprint in the North American market.

How is Recent Developments Helping the Market?

Recent developments are supporting the global etanercept market by improving access affordability and clinical confidence in etanercept therapies. The continued rollout of biosimilar etanercept products in major regions is increasing competition which helps reduce treatment costs and expand patient uptake in rheumatoid arthritis psoriatic arthritis ankylosing spondylitis and plaque psoriasis. Regulatory approvals for additional biosimilars and new manufacturing capacity are strengthening supply reliability and reducing shortages. Better real world evidence and post marketing safety data are reinforcing physician trust especially for switching from originator to biosimilars. Expanded reimbursement coverage and tender based procurement in hospitals are accelerating adoption in public health systems. Ongoing work on improved delivery devices such as prefilled pens is also enhancing patient convenience and adherence which supports steady demand growth.

Market Segment

This study forecasts revenue at global, regional, and country levels from 2020 to 2035. Decision Advisors has segmented the global etanercept market based on the below-mentioned segments:

Global Etanercept Market, By Indication

- Rheumatoid Arthritis

- Psoriatic Arthritis

- Ankylosing Spondylitis

Global Etanercept Market, By Dosage Form

- Vials

- Prefilled Syringes

- Prefilled Pens / Autoinjectors

Global Etanercept Market, By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

Global Etanercept Market, By Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa

Frequently Asked Questions (FAQ)

Q. What factors are influencing physician preference for etanercept over alternative biologics?

A. Physician preference for etanercept is influenced by its long-established safety profile, extensive clinical data, and familiarity in treating autoimmune diseases. Additionally, its predictable efficacy, availability of multiple biosimilars, and flexible dosing options make it a reliable first-line biologic therapy, especially in rheumatoid arthritis and related chronic inflammatory conditions.

Q. How does biosimilar competition impact innovation in the etanercept market?

A. While biosimilar competition drives price reductions, it also pushes companies to innovate in areas such as drug delivery devices, patient support programs, and manufacturing efficiency. Companies focus on differentiation through improved formulations, user-friendly autoinjectors, and enhanced service offerings rather than developing entirely new etanercept-based molecules.

Q. What role do specialty pharmacies play in the etanercept market ecosystem?

A. Specialty pharmacies play a crucial role by managing high-cost biologic therapies like etanercept. They handle prior authorizations, insurance coordination, patient education, and adherence programs. Their involvement ensures proper drug storage, timely delivery, and continuous patient support, which are critical for long-term treatment success in chronic autoimmune conditions.

Q. What challenges do emerging markets face in adopting etanercept therapies?

A. Emerging markets face challenges such as limited reimbursement coverage, high out-of-pocket costs, inadequate cold-chain infrastructure, and lower awareness among patients and healthcare providers. Regulatory delays and supply constraints also hinder adoption. However, increasing availability of low-cost biosimilars and improving healthcare infrastructure are gradually addressing these barriers.

Check Licence

Choose the plan that fits you best: Single User, Multi-User, or Enterprise solutions tailored for your needs.

We Have You Covered

- 24/7 Analyst Support

- Clients Across the Globe

- Tailored Insights

- Technology Tracking

- Competitive Intelligence

- Custom Research

- Syndicated Market Studies

- Market Overview

- Market Segmentation

- Growth Drivers

- Market Opportunities

- Regulatory Insights

- Innovation & Sustainability

Report Details

| Scope | Global |

| Pages | 210 |

| Delivery | PDF & Excel via Email |

| Language | English |

| Release | Apr 2026 |

| Access | Download from this page |