Global Factor VIII Deficiency Treatment Market

Global Factor VIII Deficiency Treatment Market Size, Share, By Treatment Type (Recombinant Factor VIII Products, Plasma-Derived Factor VIII Products), By Molecular Weight (Low Molecular Weight, High Molecular Weight), By End-User (Hospitals, Specialty Clinics), and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East & Africa), Analysis and Forecast 2026?2035

CAGR

6.54%

REVENUE 2025

USD Billion 7.8

FORECAST 2035

USD Billion 14.7

REPORT COVERAGE

Global

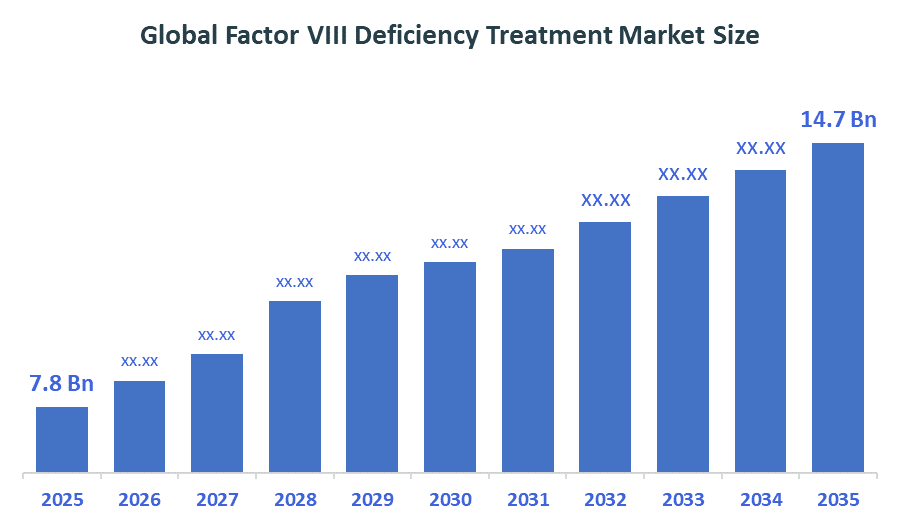

The Global Factor VIII Deficiency Treatment Market Size is forecast to grow from USD 7.8 Billion in 2025 to approximately USD 14.7 Billion by 2035. According to Decision Advisors, a detailed research report on the factor VIII deficiency treatment market indicates that the recombinant factor VIII therapies dominate the market, accounting for approximately 60-65% of the total share globally. CSL Behring the market with an estimated 20-25% global market share. The company reported a 2025 revenue of approximately USD 14+ billion, making it one of the most influential forces shaping industry trends and overall market growth.

Market Snapshot

- Global Factor VIII Deficiency Treatment Market Size (2025): USD 7.8 Billion

- Projected Global Factor VIII Deficiency Treatment Market Size (2035): USD 14.7 Billion

- Global Factor VIII Deficiency Treatment Market Compound Annual Growth Rate (CAGR): 6.54%

- Largest Regional Market: North America

- Fastest Growing Region: Asia-Pacific

- 2nd Largest Region: Europe

- Base Year: 2025

- Historical Period: 2021–2024

- Forecast Period: 2026–2035

Market Overview/ Introduction

The Global Factor VIII Deficiency Treatment Market refers to various organizations involved in the development, manufacturing, marketing, and distribution of treatments for Hemophilia A, a genetic disorder causing the disease due to insufficient levels of clotting factor VIII. Treatments of Factor VIII deficiency comprise replacement therapies, long half-life treatments, and gene therapies that will help in the restoration of normal clotting abilities and help reduce the risks of bleeding. Some of the future growth opportunities are the emergence of the latest gene-editing technology, individualized medicines, longer duration prophylaxis therapies, etc. Increasing diagnosis of Hemophilia A, awareness of the disease, technological advancements in biologics, growing penetration of the treatment in the emerging economies, and growth in government support for the treatments, along with increased healthcare infrastructure, will all lead to the growth of the Factor VIII deficiency treatment market.

- WHO promotes inclusion of recombinant factor VIII and related therapies in the Essential Medicines List, encouraging governments to adopt national procurement and reimbursement policies. This improves affordability and access to hemophilia treatments globally, especially in developing regions.

- The Indian government supports hemophilia care through awareness programs, national guidelines, and funding under public health systems. Initiatives like “One Country, One Treatment” aim to standardize factor VIII availability and improve nationwide treatment access.

Notable Insights: -

- North America is anticipated to hold the largest share of approximately 50% in the factor VIII deficiency treatment market over the forecast period.

- Asia Pacific is expected to grow at a rapid CAGR of approximately 8.7% in the factor VIII deficiency treatment market during the forecast period.

- The recombinant factor VIII products segment dominated the market in 2025, approximately 45%, and is projected to grow at a substantial CAGR during the forecast period.

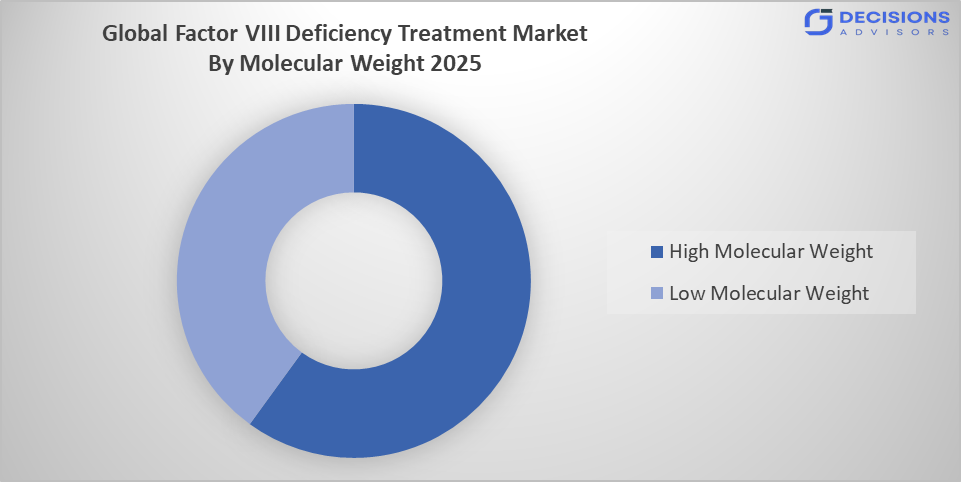

- The high molecular weight segment dominated the market in 2025, approximately 55%, and is projected to grow at a substantial CAGR during the forecast period.

- The hospitals segment dominated the market in 2025, approximately 60%, and is projected to grow at a substantial CAGR during the forecast period.

- The compound annual growth rate of the Global Factor VIII Deficiency Treatment Market is 6.54%.

- The market is likely to achieve a valuation of USD 14.7 Billion by 2035.

What is role of technology in grooming the market?

Technology plays a crucial role in grooming the Global Factor VIII Deficiency Treatment Market for Hemophilia A by improving treatment efficacy, safety, and accessibility. Advances in biotechnology have enabled the development of recombinant and extended half-life factor VIII products, which reduce infusion frequency and enhance patient adherence. Gene therapy is emerging as a breakthrough innovation, offering the potential for long-term correction of the disorder with a single treatment. Digital health tools such as telemedicine platforms and mobile applications support remote monitoring, personalized dosing, and better disease management. Artificial intelligence and data analytics help predict bleeding episodes and optimize treatment plans. Additionally, improvements in cold-chain logistics and drug delivery systems ensure better distribution of therapies globally. Overall, technological progress is transforming care standards, increasing survival rates, and significantly driving market expansion worldwide.

Market Drivers

The Global Factor VIII Deficiency Treatment Market, related to Hemophilia A, is driven by several key factors. Rising prevalence of genetic bleeding disorders and improved diagnosis rates are increasing patient identification worldwide. Advancements in recombinant factor VIII therapies and extended half-life products are enhancing treatment efficacy and compliance. Growing awareness about early disease management and availability of prophylactic therapies also support market expansion. Additionally, increasing healthcare expenditure, government funding programs, and supportive reimbursement policies are improving access to treatment. Technological innovations such as gene therapy and biotechnology-based drug development further accelerate market growth, while expanding healthcare infrastructure in emerging economies boosts adoption.

Restrain

The Global Factor viii deficiency treatment market faces restraints due to the high cost of recombinant and gene therapies, limited access in low-income regions, risk of inhibitor development in patients, and stringent regulatory approval processes, which collectively hinder widespread treatment adoption and market expansion.

Competitive Analysis:

The report offers the appropriate analysis of the key organizations/companies involved within the global factor VIII deficiency treatment market, along with a comparative evaluation primarily based on their product offerings, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes product development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

Top Companies in Global Factor VIII Deficiency Treatment Market

- CSL Behring

- Takeda Pharmaceutical Company Limited

- Bayer AG

- Novo Nordisk A/S

- Pfizer Inc.

- Sanofi S.A.

- F. Hoffmann-La Roche Ltd.

- Octapharma AG

- BioMarin Pharmaceutical Inc.

- Grifols S.A.

Government Initiatives

|

Country |

Key Government Initiatives |

|

US |

The FDA has accelerated the approval of novel therapies, including Roctavian (the first gene therapy for Hemophilia A) and Hympavzi (marstacimab) for routine prophylaxis in patients 12 and older. The CDC continues to support the Universal Data Collection (UDC) system through Hemophilia Treatment Centers (HTCs) to monitor treatment safety and outcomes nationwide. |

|

UK |

NHS England and NICE have implemented the 2024 Voluntary Scheme for Branded Medicines Pricing, Access and Growth (VPAG). This includes an innovative outcomes-based payment model designed to manage the high costs of advanced therapies while ensuring patient access to once-weekly treatments like Altuvoct (efanesoctocog alfa). |

|

India |

The National Health Mission (NHM) provides free factor support (including Factors VIII and IX) to all patients regardless of economic status. In 2025, the government intensified the Initiative on Hemophilia Care, aimed at establishing national guidelines and a "One Country, One Treatment" model to standardize care and procurement across all states. |

Study on the Supply, Demand, Distribution, and Market Environment of the Factor VIII Deficiency Treatment Market

The Global Factor VIII Deficiency Treatment Market for Hemophilia A is shaped by a dynamic supply–demand–distribution ecosystem. Supply is driven by major biopharmaceutical companies producing recombinant and plasma-derived factor VIII, though high manufacturing complexity and costs limit production scalability. Demand is steadily increasing due to rising diagnosis rates, improved awareness, and lifelong treatment requirements. Distribution is strengthened through hospitals, specialty clinics, and government procurement programs, with cold-chain logistics ensuring product stability. Market environment is highly competitive, dominated by global players investing in gene therapy and extended half-life products. Regulatory frameworks, reimbursement policies, and healthcare funding significantly influence accessibility. Additionally, technological advancements and expanding healthcare infrastructure in emerging economies are enhancing market penetration, while challenges like high treatment costs and inhibitor development continue to shape overall market dynamics globally.

Price Analysis and Consumer Behaviour Analysis

Price analysis and consumer behaviour in the Global Factor VIII Deficiency Treatment Market for Hemophilia A shows a highly cost-intensive structure driven by biologics and recombinant therapies. Pricing remains very high due to complex manufacturing of factor VIII concentrates, with recombinant and extended half-life products costing significantly more than plasma-derived alternatives. This creates a heavy financial burden on patients and healthcare systems, especially since lifelong treatment is required. Consumer behaviour is strongly influenced by physician recommendation, hospital availability, reimbursement coverage, and government support programs. In developed regions, patients prefer advanced recombinant and prophylactic therapies for better safety and fewer injections, while in developing countries, cost sensitivity leads to higher reliance on plasma-derived products or subsidized treatments. Increasing insurance coverage and awareness programs are gradually improving adoption of advanced therapies, but affordability remains the key factor shaping purchasing decisions globally.

Market Segmentation

The Factor VIII Deficiency Treatment Market share is classified into treatment type, molecular weight, and end-user.

- The recombinant factor VIII products segment dominated the market in 2025, approximately 45%, and is projected to grow at a substantial CAGR during the forecast period.

Based on the treatment type, the factor VIII deficiency treatment market is divided into recombinant factor VIII products and plasma-derived factor VIII products. Among these, the recombinant factor VIII products segment dominated the market in 2025, approximately 45%, and is projected to grow at a substantial CAGR during the forecast period. The growth of the recombinant factor VIII products segment is driven by their superior safety and reduced risk of blood-borne infections compared to plasma-derived alternatives. Their consistent quality, advanced biotechnology manufacturing, and strong physician preference further boost adoption. Increasing prophylactic treatment use and regulatory support for safer therapies continue to reinforce segment leadership globally.

- The high molecular weight segment dominated the market in 2025, approximately 55%, and is projected to grow at a substantial CAGR during the forecast period.

Based on the molecular weight, the factor VIII deficiency treatment market is divided into low molecular weight and high molecular weight. Among these, the high molecular weight segment dominated the market in 2025, approximately 55%, and is projected to grow at a substantial CAGR during the forecast period. The high molecular weight segment dominated due to its longer half-life and improved therapeutic efficacy. These formulations reduce dosing frequency, enhancing patient compliance and clinical outcomes. Growing demand for extended-duration therapies and advancements in molecular engineering have increased their preference over low molecular weight products in long-term hemophilia a management.

- The hospitals segment dominated the market in 2025, approximately 60%, and is projected to grow at a substantial CAGR during the forecast period.

Based on the end-user, the factor VIII deficiency treatment market is divided into hospitals and specialty clinics. Among these, the hospitals segment dominated the market in 2025, approximately 60%, and is projected to grow at a substantial CAGR during the forecast period. The growth of the hospitals segment is because they serve as primary treatment centers for hemophilia patients requiring specialized care and emergency bleeding management. Availability of advanced infrastructure, skilled professionals, and comprehensive diagnostic facilities drives their dominance. Additionally, hospital pharmacies handle complex biologics distribution, further strengthening their position in the global Factor VIII deficiency treatment market.

Strategies to Implement for Growth of the Market in Non-Leading Regions

To drive growth of the Global Factor VIII Deficiency Treatment Market for Hemophilia A in non-leading regions, companies and governments should focus on improving affordability and access to therapy. Expanding public–private partnerships can support subsidized procurement of factor VIII products and strengthen local healthcare infrastructure. Establishing regional plasma collection and manufacturing facilities can reduce dependency on imports and lower costs. Awareness campaigns and early diagnostic programs are essential to improve patient identification. Telemedicine and digital health platforms can enhance specialist access in remote areas. Additionally, training healthcare professionals and developing standardized treatment guidelines will improve disease management. Encouraging adoption of biosimilars and extended half-life products at reduced prices can further boost uptake. Strengthening reimbursement systems and insurance coverage will also play a key role in accelerating market penetration in emerging and underserved regions globally.

Regional Segment Analysis of the Factor VIII Deficiency Treatment Market

- North America (U.S., Canada, Mexico)

- Europe (Germany, France, U.K., Italy, Spain, Rest of Europe)

- Asia-Pacific (China, Japan, India, Rest of APAC)

- South America (Brazil and the Rest of South America)

- The Middle East and Africa (UAE, South Africa, Rest of MEA)

North America is anticipated to hold the largest share of approximately 50% the factor VIII deficiency treatment market over the forecast period.

North America is anticipated to hold the largest share of approximately 50% the factor VIII deficiency treatment market over the forecast period. The dominance of this region is primarily driven by advanced healthcare infrastructure, high diagnosis rates of hemophilia A, and strong access to recombinant therapies. Presence of leading pharmaceutical companies, favorable reimbursement policies, and increased adoption of prophylactic treatments further support regional dominance.

Asia Pacific is expected to grow at a rapid CAGR of approximately 8.7% in the factor VIII deficiency treatment market during the forecast period.

Asia Pacific is expected to grow at a rapid CAGR of approximately 8.7% in the factor VIII deficiency treatment market during the forecast period. This growth is driven by rising hemophilia awareness, improving healthcare infrastructure, and expanding access to advanced therapies. Increasing government support, growing patient diagnosis rates, and higher healthcare spending in countries like China and India are accelerating demand for Factor VIII treatments, boosting regional market growth.

Europe is the 2nd largest region to grow in the factor VIII deficiency treatment market during the period.

Europe is the second-largest region in the Factor VIII deficiency treatment market, supported by well-established healthcare systems and widespread access to advanced hemophilia therapies. Strong government funding, favorable reimbursement policies, and early adoption of recombinant Factor VIII products drive growth. Additionally, increasing awareness, robust patient registries, and presence of key pharmaceutical companies contribute to sustained regional market expansion.

Future Market Trends in Global Factor VIII Deficiency Treatment Market: -

1. Growth of Gene Therapy Adoption

Gene therapy is emerging as a major trend in the Global Factor VIII Deficiency Treatment Market for Hemophilia A due to its potential to provide long-term or one-time treatment. It reduces the need for frequent infusions and improves patient quality of life. Increasing clinical approvals and strong R&D investments by pharmaceutical companies are driving this shift toward curative solutions.

2. Expansion of Extended Half-Life Therapies

Extended half-life Factor VIII products are gaining traction because they reduce injection frequency and improve patient adherence. This trend is driven by advancements in protein engineering and rising demand for convenient prophylactic treatments. Healthcare providers prefer these therapies for better bleeding control, while patients benefit from improved lifestyle flexibility and reduced treatment burden.

3. Rising Digital Health Integration

Digital health technologies, including telemedicine and AI-based monitoring, are becoming a key trend in Hemophilia A management. These tools help track bleeding risks, optimize dosage, and improve treatment compliance. Growing adoption is supported by increasing smartphone penetration, remote healthcare needs, and demand for personalized treatment strategies, enhancing overall disease management efficiency.

Recent Development

- In June 2025, Roche announced that its next-generation bispecific antibody NXT007 showed promising early clinical results and was set to advance into Phase 3 trials beginning in 2026, targeting improved haemostasis in patients with hemophilia A. Around the same period, Novo Nordisk’s Mim8 (denecimig), another next-generation FVIII-mimetic bispecific antibody, continued progressing through late-stage Phase 3 trials, with regulatory submissions planned for 2025 and additional data expected through 2026.

- In October 2024, the U.S. FDA approved Marstacimab (HYMPAVZI), a once-weekly subcutaneous therapy for adults and adolescents (≥12 years) with hemophilia A or B without inhibitors. The approval was supported by Phase 3 BASIS trial data, which demonstrated a significant reduction in annualized bleeding rates up to around 92% compared to on-demand treatment highlighting its strong efficacy and convenience.

- In May 2024, the U.S. FDA approved ALTUVIIIO (efanesoctocog alfa), a first-in-class, high-sustained factor VIII replacement therapy for hemophilia A, demonstrating strong bleed protection with a convenient once-weekly dosing regimen. In May 2024, the FDA updated its label to include full results from the Phase 3 XTEND-Kids study.

How is Recent Developments Helping the Market?

Recent developments are significantly improving the Global Factor VIII Deficiency Treatment Market for Hemophilia A by enhancing treatment efficacy, safety, and accessibility. The introduction of extended half-life factor VIII products reduces infusion frequency and improves patient adherence, making long-term prophylaxis more convenient. Breakthrough gene therapies are emerging as potential one-time treatments, offering sustained factor production and reducing lifelong treatment burden. Advanced recombinant technologies have improved product purity and reduced infection risks. Additionally, digital health tools and AI-based monitoring systems are enabling personalized dosing and better bleeding risk prediction. Improved clinical trial outcomes and regulatory approvals are accelerating product commercialization. Together, these innovations are lowering treatment burden, increasing patient quality of life, and expanding market growth by encouraging wider adoption across developed and emerging healthcare systems globally.

Market Segment

This study forecasts revenue at global, regional, and country levels from 2020 to 2035. Decision Advisors has segmented the Factor VIII Deficiency Treatment Market based on the below-mentioned segments:

Global Factor VIII Deficiency Treatment Market, By Treatment Type

- Recombinant Factor VIII Products

- Plasma-Derived Factor VIII Products

Global Factor VIII Deficiency Treatment Market, By Molecular Weight

- Low Molecular Weight

- High Molecular Weight

Global Factor VIII Deficiency Treatment Market, By End-User

- Hospitals

- Specialty Clinics

Global Factor VIII Deficiency Treatment Market, By Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa

Frequently Asked Questions (FAQ)

Q. What are inhibitors in Hemophilia A treatment, and why do they pose a challenge?

A. Inhibitors are neutralizing antibodies that some patients develop against Factor VIII therapies, making treatment less effective or ineffective. They complicate disease management by increasing bleeding risk and requiring alternative bypassing agents or immune tolerance therapy. This leads to higher treatment costs, longer hospitalization, and reduced response to standard recombinant or plasma-derived Factor VIII products.

Q. How does real-world evidence (RWE) impact treatment decisions in this market?

A. Real-world evidence provides insights from actual patient outcomes outside clinical trials, helping physicians compare long-term safety, dosing frequency, and effectiveness of different Factor VIII therapies. It supports regulatory decisions, improves treatment guidelines, and helps payers evaluate cost-effectiveness. RWE is especially important for newer gene and extended half-life therapies where long-term data is still evolving.

Q. Why is personalized dosing becoming important in Factor VIII deficiency management?

A. Personalized dosing tailors Factor VIII administration based on a patient’s weight, bleeding pattern, pharmacokinetics, and lifestyle. This approach improves bleeding control while avoiding over- or under-treatment. It enhances patient adherence, reduces unnecessary drug usage, and lowers overall treatment burden, especially with advanced recombinant and extended half-life therapies.

Q. How does plasma donation infrastructure affect the availability of treatments?

A. Plasma-derived Factor VIII production depends heavily on a stable and safe plasma donation network. Strong infrastructure ensures consistent raw material supply, while weak donation systems can lead to shortages. Countries with well-organized plasma collection programs tend to have better treatment availability and lower dependency on imports, improving access and market stability.

Check Licence

Choose the plan that fits you best: Single User, Multi-User, or Enterprise solutions tailored for your needs.

We Have You Covered

- 24/7 Analyst Support

- Clients Across the Globe

- Tailored Insights

- Technology Tracking

- Competitive Intelligence

- Custom Research

- Syndicated Market Studies

- Market Overview

- Market Segmentation

- Growth Drivers

- Market Opportunities

- Regulatory Insights

- Innovation & Sustainability

Report Details

| Scope | Global |

| Pages | 210 |

| Delivery | PDF & Excel via Email |

| Language | English |

| Release | Apr 2026 |

| Access | Download from this page |