Global Fiber Optic Connectors Market

Global Fiber Optic Connectors Market Size, Share, By Type (Lucent Connector, Fiber Connector, Straight Tip, Master Unit, Push On/Pull Off, Subscriber Connector, Multi-Fiber Termination, Fiber Distributed Data Interface, Sub-Multi-Assembly) By Application (Datacenter, Telecommunication, Inter-Building, Security System) By Industries (Automotive, IT and Telecom and Consumer Electronics) and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2026-2035

CAGR

9.2%

REVENUE 2025

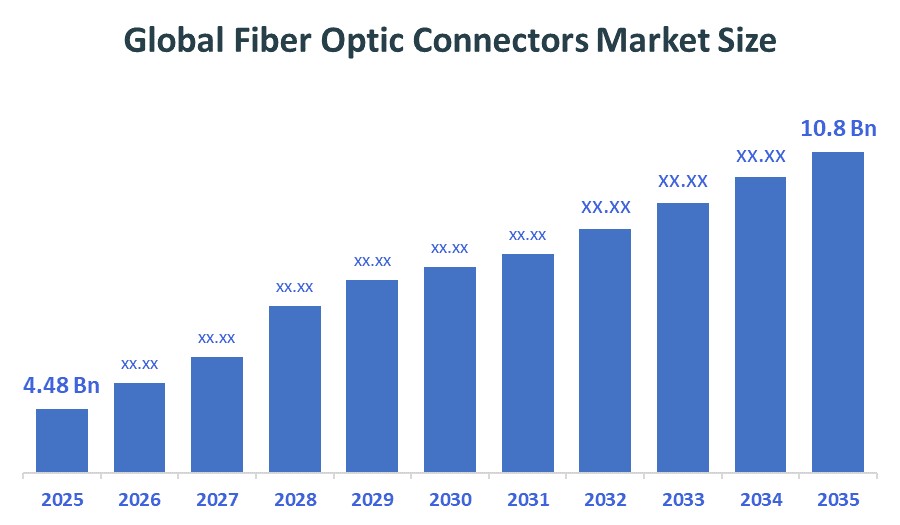

USD Billion 4.48

FORECAST 2035

USD Billion 10.8

REPORT COVERAGE

Global

Market Snapshot

- Global Fiber Optic Connectors Market Size (2025): USD 4.48 Billion

- Projected Global Fiber Optic Connectors Market Size (2035): USD 10.8 Billion

- Compound Annual Growth Rate (CAGR): 9.2%

- Largest Regional Market: Asia-Pacific

- Fastest Growing Region: North America

- 3rd Largest Region: Europe

- Base Year: 2025

- Historical Period: 2021–2024

- Forecast Period: 2026–2035

According to Decision Advisors, The Global Fiber Optic Connectors Market Size is expected to grow from USD 4.48 billion in 2025 to USD 10.8 billion by 2035, at a CAGR of 9.2% during the forecast period 2026-2035. The global fiber optic connectors market growth is driven by 5G expansion, cloud/AI data centers, FTTH rollout, IoT adoption, government initiatives, and advanced low-loss connector technology.

Market Overview/ Introduction

The global fiber optic connectors market refers to the industry that create and produce connectors which link optical fibers to provide fast data transmission through communication networks. The demand for high-bandwidth internet together with the rollout of 5G networks and the growing need for data centers and cloud computing services is fueling economic expansion. The main developments in the industry show that fiber-to-the-home (FTTH) services, high-density connectors for hyperscale data centers are becoming more popular. The market is seeing better performance, better system reliability through the introduction of low-loss connectors and compact LC connectors which will hold 35.43% market share in 2024. Opportunities are expanding with smart city projects and worldwide broadband network development work together to create new business opportunities.

- India’s flagship rural broadband initiative has connected over 2.15 lakh Gram Panchayats (village councils) with optical-fiber infrastructure to expand high-speed internet access across rural areas. The country’s optical-fiber network expanded from 19.35 lakh route km in 2019 to about 42.36 lakh route km by 2025, reflecting massive infrastructure growth.

- December 2020: The PM-WANI Scheme, launched by the Government of India, aims to expand public Wi-Fi access nationwide. It allows small entrepreneurs to set up Public Data Offices without license fees, improving affordable internet connectivity and promoting digital inclusion in rural and underserved areas.

- The National Broadband Mission under the Digital India initiative promotes a “Fiber First” policy, Right of Way (RoW) reforms, and integration with smart cities, 5G, and e-governance services to accelerate broadband infrastructure deployment and last-mile connectivity across the country

Notable Insights: -

- Asia-Pacific holds the largest regional market share approximately 40% in the global fiber optic connectors market

- North America is the fastest growing region CAGR 8% in the global fiber optic connectors market.

- By type, the lucent connector segment held a dominant position with 37% in terms of market share in 2025.

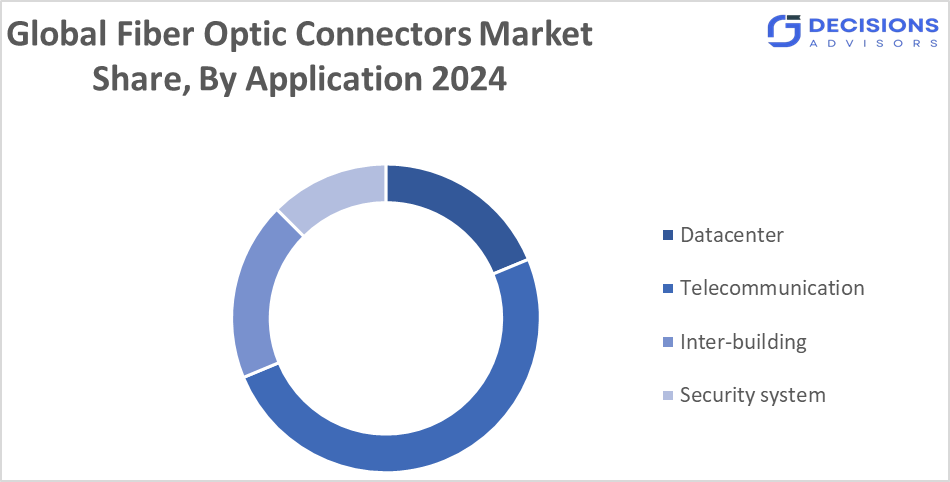

- By application, data center segment is the dominating accounting for over 8% of the global market share in 2025.

- The compound annual growth rate of the Cardiac AI Monitoring and Diagnostics is 9.2%.

- The market is likely to achieve a valuation of USD 10.8 billion by 2035.

What is role of technology in grooming the market?

The global Fiber Optic Connectors market depends on technology because it provides methods for transferring data at high speeds with dependable performance and greater capacity. The rapid expansion of 5G, Cloud Computing, and Internet of Things (IoT) requires dense fiber-optic infrastructure and advanced connector solutions. Now hyperscale data centers use connectors which support 12, 24 or 48 fiber configurations to achieve better bandwidth performance. Global internet traffic will surpass 396 exabytes per month which drives demand for high-speed optical networks. The network performance and reliability and scalability of digital communication systems that require high bandwidth now benefit from innovations which include low-insertion-loss connectors and automated fiber alignment and compact LC and MPO designs. The rising number of nearly 7 billion mobile broadband connections worldwide further drives fiber infrastructure upgrades, boosting connector adoption in telecom and hyperscale data centers.

Market Drivers

The global demand for fiber optic connectors grows due to the expanding 5G infrastructure and the rapid development of cloud computing and the rising adoption of Internet of Things (IoT) devices. The worldwide number of internet users reached 5.4 billion in 2024 which created a greater need for high-speed broadband networks. The Indian government broadband initiatives BharatNet and Digital India have established new fiber infrastructure which better enables the installation of fiber optic connectors in telecommunications systems, enterprise networks and hyperscale data centers. Government programs such as Digital India and BharatNet are expanding fiber networks which results in increased deployment of fiber optic connectors in telecom and broadband projects.

Restrain

The market faces restraints due to fiber-optic networks require high installation and maintenance expenses which exceed those of traditional copper networks. The cost to deploy fiber networks ranges from USD 25000 to USD 60000 for each mile based on the specific terrain and population density of the area. The operational process becomes more difficult because fiber connectors need exact positioning and only qualified technicians can handle their installation. The factors of network damage, connector contamination, and bending sensitivity all impact signal performance which makes the technology unsuitable for deployment in remote areas that have limited budget capacity.

Competitive Analysis:

The report offers the appropriate analysis of the key organizations/companies involved within the fiber optic connectors market, along with a comparative evaluation primarily based on their product of offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes product development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

Top Companies in Global Fiber Optic Connectors Market

- Amphenol Corporation

- TE Connectivity

- Corning Incorporated

- CommScope

- Molex

- Sumitomo Electric Industries

- Furukawa Electric Co., Ltd.

- Fujikura Ltd.

- Sterlite Technologies Ltd.

- 3M

- Broadcom Inc.

- Radiall S.A.

- Rosenberger Group

- AFL Global

- Hirose Electric Co., Ltd

Government Initiatives

|

Country |

Key Government Initiatives |

|

European Union |

In March 2021: The Digital Decade 2030 strategy aims to achieve gigabit connectivity for all households and full 5G coverage across the EU by 2030. The initiative promotes fiber-first policies, public funding, and subsidies to expand broadband infrastructure in rural and underserved regions. |

|

US |

In November 15, 2021: The Broadband Equity, Access, and Deployment (BEAD) Program, created under the Infrastructure Investment and Jobs Act, allocates USD 42.45 billion to expand high-speed broadband in unserved and underserved areas across the U.S., supporting large-scale fiber infrastructure deployment and digital connectivity improvements |

|

India

|

In October 13, 2021: The PM GatiShakti National Master Plan integrates infrastructure sectors such as roads, railways, power, and telecom through a GIS-based platform to accelerate fiber deployment via shared corridors and coordinated planning, improving broadband expansion and nationwide digital connectivity |

Study on the Supply, Demand, Distribution, and Market Environment the Fiber Optic Connectors Market

The study of supply, demand, distribution, and market environment in the global Fiber Optic Connectors market highlights strong growth driven by expanding digital infrastructure. On the demand side, telecom and data-center applications account for a major share, with telecom networks representing over 22% of connector usage globally. Supply chains include manufacturers of connectors, fiber cables, and network hardware distributed through telecom operators and system integrators. Rapid deployment of 5G is a key factor, as 5G networks require 10–20 times more fiber connections than 4G systems. Additionally, global 5G investments exceeded USD 95 billion in 2023, strengthening fiber infrastructure deployment and increasing demand for reliable optical connectivity solutions across telecom and enterprise networks.

Price Analysis and Consumer Behaviour Analysis??

Price dynamics in the fiber optic connectors market show different patterns based on the type of connector, the region of manufacturing and the sector of application. Standard connectors such as LC and SC face intense price competition due to manufacturers in Asia produce the connectors at high volumes which leads to lower market prices. The manufacturing costs will rise due to changes in raw material costs which include metals, ceramics and polymers that make up the production process. From a consumer perspective, telecom operators, data-center companies prioritize performance, durability and low signal loss when they purchase connectors. The LC connector segment holds over 35% market share, which shows that modern networks strongly prefer compact connectors that provide high-density connectivity. Telecom and cloud infrastructure operators drive the demand for reliable optical components due to they need these components to support their expanding broadband networks, high-speed data transmission and increasing global digital traffic.

Market Segmentation

The fiber optic connectors market share is classified into type, application, and Industries

- The lucent connector segment dominated the market in 2025, and is projected to grow at a substantial CAGR of approximately 37% during the forecast period.

Based on the type, the?fiber optic connectors market is divided?into?lucent connector, fiber connector, straight tip, master unit, push on/pull off, subscriber connector, multi-fiber termination, fiber distributed data interface, sub-multi-assembly among these,?the lucent connector segment dominated the market and holds approximately 37%?share in 2025 and is projected to grow at a substantial CAGR during the forecast period. The Lucent connector segment dominates due to compact size, high-density capability, low loss, FTTH/5G adoption, and cost-efficient, scalable deployment.

- The data centre segment accounted for the largest share in 2025, and is anticipated to grow at a significant CAGR of approximately 8% during the forecast period.

Based on the application, the?fiber optic connectors market is divided?into Datacenter, telecommunication, inter-building, security system among these,?the data center segment dominated the market and holds approximately?8%?share in 2025 and is projected to grow at a substantial CAGR during the forecast period. The segment will experience substantial growth during the forecast period because ongoing digital transformation and 5G adoption and increased FTTH deployment drive market demand. The segment will experience a market expansion that will result in annual growth rates 8 % throughout the entire forecast period.

- The Telecommunication segment dominated the market in 2025, and is projected to grow at a substantial CAGR approximately?40% during the forecast period.

Based on the Industries, the?fiber optic connectors market is divided?into Datacenter, Telecommunication, Inter-Building, Security System among these,?the Telecommunication segment dominated the market and holds approximately?40%?share in 2025 and is projected to grow at a substantial CAGR during the forecast period. The segment will experience substantial growth through the forecast period due to digitalization increases and networks require low latency and telecom backbone and metro fiber networks receive ongoing investments. The segment will experience substantial growth through the forecast period due to digitalization increases, networks require low latency, telecom backbone and metro fiber networks receive ongoing investments.

Strategies to Implement for Growth of the Market in Non-Leading Regions

The global fiber optic connectors market expansion strategies for non-leading regions emphasize three main factors which include infrastructure investment, policy support and technology adoption. Governments should increase broadband funding because almost 2.6 billion people worldwide still lack internet access with most users located in developing areas. 5G network expansion through fiber backhaul development will enhance connectivity while generating need for advanced connectors. Public–private partnerships enable faster deployment processes together with cost reduction benefits. Programs which follow the BharatNet model will expand fiber network infrastructure into rural communities. The promotion of local manufacturing together with technician training programs will enable installation cost reductions of 15 to 20% which will strengthen supply chains and drive broader adoption of fiber optic connectivity solutions across developing markets.

Regional Segment Analysis of the Fiber Optic Connectors Market

- North America (U.S., Canada, Mexico)

- Europe (Germany, France, U.K., Italy, Spain, Rest of Europe)

- Asia-Pacific (China, Japan, India, Rest of APAC)

- South America (Brazil and the Rest of South America)

- The Middle East and Africa (UAE, South Africa, Rest of MEA)

Asia Pacific is anticipated to hold the largest share approximately 40%of the fiber optic connectors market over the predicted timeframe.

Asia Pacific is anticipated to hold the largest share approximately 40%of the fiber optic connectors market over the predicted timeframe. The Asia-Pacific region will dominate the global fiber optic connectors market throughout the forecast period. The region maintains its dominant position due to 5G networks are expanding rapidly and countries such as China, India Japan and South Korea are developing extensive fiber broadband networks and building new data centers. The government programs that promote digital infrastructure construction together with the internet access which now reaches 64% of the population create more demand for high-speed optical connectors that telecommunications companies, enterprises and cloud network operators use.

North America is expected to grow at a rapid CAGR 8% in the fiber optic connectors market during the forecast period.

North America is expected to grow at a rapid CAGR 8% in the fiber optic connectors market during the forecast period. Growth is driven by expanding 5G infrastructure, rising hyperscale Cloud Computing data centers, and broadband initiatives such as the Broadband Equity, Access, and Deployment (BEAD) Program, which is investing over USD 42 billion to expand high-speed internet connectivity. Internet penetration in North America exceeds 90% of the population, driving the rapid deployment of fiber optic networks to support high-speed connectivity, AI workloads, and next-generation digital services across the United States and Canada.

Europe is the 3rd largest region to grow in the fiber optic connectors market during the region.

The European market for fiber optic connectors ranks as the third largest worldwide due to substantial investments made toward fiber broadband and digital infrastructure development. The growth of 5G networks together with the increasing adoption of fiber-to-the-home (FTTH) systems serves as primary factors driving market expansion. The major economies of Germany, France and the United Kingdom are constructing advanced high-speed broadband infrastructure. The Digital Decade 2030 initiative establishes a regional goal for gigabit connectivity which serves as a foundation for telecom operators to invest in modern optical networking systems and high-capacity fiber optic connectors.

Future Market Trends in Fiber Optic Connectors Market: -

- Expansion of 5G Infrastructure

The rapid rollout of 5G networks is significantly increasing demand for fiber backhaul. A single 5G base station can require 3–5 times more fiber links than previous networks, and dense urban deployments may require up to 10 fiber connections per site, boosting connector adoption.

- Growth of AI and Cloud Data Centers

The expansion of Artificial Intelligence and Cloud Computing is driving demand for ultra-high-capacity optical networks. Global data center traffic accounts for over 70% of total internet traffic, requiring high-density fiber connectors to support massive data transmission.

- Increasing Fiber-to-the-Home (FTTH) Deployment

The growth of Fiber to the Home (FTTH) is accelerating broadband access. Fiber broadband penetration in many developed economies exceeds 50% of fixed broadband connections, significantly increasing the installation of fiber connectors in residential networks.

Recent Development

- In December 2025, Panduit launched NetKey fiber optic connectors featuring tool-less field termination, reducing installation time by approximately 60%. The solution targets enterprise data centers and 400GBASE-SR8 applications, improving efficiency in high-density optical networks.

- In October 2025, Broadcom Inc. introduced the industry’s first 800G AI Ethernet Network Interface Card (NIC), the Thor Ultra, designed to support ultra?high?speed connectivity in AI data centers and scale large?scale AI workloads with enhanced performance and interoperability.

- In April 2025, Molex launched its VersaBeam Expanded Beam Optical Interconnects, offering high-density fiber connectivity for edge computing and hyperscale data centers. These connectors support up to 144 fibers per interface, improving installation efficiency and network reliability.

- In March 2025, 3M, in partnership with SENKO and Sumitomo Electric, deployed Expanded Beam Optical (EBO) ferrule technology for high-density data centers, enhancing fiber optic connector reliability, reducing maintenance, and improving performance in enterprise and cloud network applications.

How is Recent Developments Helping the Market?

Recent developments are significantly supporting the growth of the global fiber optic connectors market by improving performance, reliability, and scalability of optical networks. Companies are introducing advanced high-density connectors designed for next-generation data centers and telecom infrastructure. For example, in 2025, SENKO Advanced Components, 3M, and Molex collaborated to launch an MPO EBO EZ-WAY connector using expanded-beam optical technology, which improves reliability and reduces maintenance in harsh environments. Additionally, innovations such as 16-fiber MPO connectors supporting 400 G transmission reduce cable congestion by about 35%, enabling efficient high-bandwidth data center connectivity. Furthermore, new connectors designed for 100 Gbps and higher data rates and next-generation 1.6 Tbps optical networks are enhancing network capacity and reliability. These technological partnerships, product launches, and high-speed connector innovations are accelerating adoption of fiber infrastructure, thereby strengthening the global fiber optic connectors market.

Market Segment

This study forecasts revenue at global, regional, and country levels from 2020 to 2035. Decision Advisor has segmented the fiber optic connectors market based on the below-mentioned segments:

Global Fiber Optic Connectors Market, By Type

- Lucent Connector

- Fiber Connector

- Straight Tip

- Master Unit

- Push On/Pull Off

- Subscriber Connector

- Multi-Fiber Termination

- Fiber Distributed Data Interface

- Sub-multi-assembly

Global Fiber Optic Connectors Market, By Application

- Datacenter

- Telecommunication

- Inter-Building

- Security System

Global Fiber Optic Connectors Market, By Industries

- Automotive

- IT and Telecom

- Consumer Electronics

Global Fiber Optic Connectors Market, By Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa

Frequently Asked Questions (FAQ)

Q1. What is a fiber optic connector?

A fiber optic connector is a device that joins optical fibers to enable fast, reliable data transmission in telecom, data center, and enterprise networks.

Q2. Which connector type dominated the market in 2025?

The Lucent Connector (LC) segment dominated, holding approximately 37% market share due to compact size, high density, low loss, and FTTH/5G adoption.

Q3. Which application holds the largest share of the market?

The Data Center segment dominated in 2025, accounting for roughly 8% market share, driven by hyperscale cloud infrastructure, AI workloads, and high-bandwidth requirements.

Q4. Which industry drives the most demand for fiber optic connectors?

The Telecommunication industry dominated with 40% market share, fueled by 5G expansion, fiber-to-the-home (FTTH), and broadband infrastructure investments.

- Introduction

- Objectives of the Study

- Market Definition

- Research Scope

- Research Methodology and Assumptions

- Executive Summary

- Premium Insights

- Porter’s Five Forces Analysis

- Value Chain Analysis

- Top Investment Pockets

- Market Attractiveness Analysis By Type

- Market Attractiveness Analysis By Application

- Market Attractiveness Analysis By Industries

- Market Attractiveness Analysis By Region

- Industry Trends

- Market Dynamics

- Market Evaluation

- Drivers

Expansion of 5G infrastructure

-

- Restraints

- High installation and deployment cost of fiber-optic networks.

- Opportunities

- Smart cities require high-speed

- Challenges

- High deployment cost of fiber optic infrastructure.

- Restraints

- Global Fiber Optic Connectors Market Analysis and Projection, By Type

- Segment Overview

- Lucent Connector

- Fiber Connector

- Straight Tip

- Master Unit

- Push On/Pull Off

- Subscriber Connector

- Multi-Fiber Termination

- Fiber Distributed Data Interface

- Sub-multi-assembly

- Global Fiber Optic Connectors Market Analysis and Projection, By Application

- Segment Overview

- Datacenter

- Telecommunication

- Inter-Building

- Security System

- Global Fiber Optic Connectors Market Analysis and Projection, By Industries

- Segment Overview

- Automotive

- IT and Telecom

- Consumer Electronics

- Global Fiber Optic Connectors Market Analysis and Projection, By Regional Analysis

- Segment Overview

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Asia-Pacific

- Japan

- China

- India

- South America

- Brazil

- Middle East and Africa

- UAE

- South Africa

- Global Fiber Optic Connectors Market-Competitive Landscape

- Overview

- Market Share of Key Players in the Fiber Optic Connectors Market

- Global Company Market Share

- North America Company Market Share

- Europe Company Market Share

- APAC Company Market Share

- Competitive Situations and Trends

- Coverage Launches and Developments

- Partnerships, Collaborations, and Agreements

- Mergers & Acquisitions

- Expansions

- Company Profiles

- Amphenol Corporation

- Business Overview

- Company Snapshot

- Company Market Share Analysis

- Company Coverage Portfolio

- Recent Developments

- SWOT Analysis

- TE Connectivity

- Business Overview

- Company Snapshot

- Company Market Share Analysis

- Company Coverage Portfolio

- Recent Developments

- SWOT Analysis

- Corning Incorporated

- Business Overview

- Company Snapshot

- Company Market Share Analysis

- Company Coverage Portfolio

- Recent Developments

- SWOT Analysis

- CommScope

- Business Overview

- Company Snapshot

- Company Market Share Analysis

- Company Coverage Portfolio

- Recent Developments

- SWOT Analysis

- Molex

- Business Overview

- Company Snapshot

- Company Market Share Analysis

- Company Coverage Portfolio

- Recent Developments

- SWOT Analysis

- Sumitomo Electric Industries

- Business Overview

- Company Snapshot

- Company Market Share Analysis

- Company Coverage Portfolio

- Recent Developments

- SWOT Analysis

- Furukawa Electric Co., Ltd.

- Business Overview

- Company Snapshot

- Company Market Share Analysis

- Company Coverage Portfolio

- Recent Developments

- SWOT Analysis

- Fujikura Ltd.

- Business Overview

- Company Snapshot

- Company Market Share Analysis

- Company Coverage Portfolio

- Recent Developments

- SWOT Analysis

- Sterlite Technologies Ltd.

- Business Overview

- Company Snapshot

- Company Market Share Analysis

- Company Coverage Portfolio

- Recent Developments

- SWOT Analysis

- 3M

- Business Overview

- Company Snapshot

- Company Market Share Analysis

- Company Coverage Portfolio

- Recent Developments

- SWOT Analysis

- Broadcom Inc.

- Business Overview

- Company Snapshot

- Company Market Share Analysis

- Company Coverage Portfolio

- Recent Developments

- SWOT Analysis

- Radiall S.A.

- Business Overview

- Company Snapshot

- Company Market Share Analysis

- Company Coverage Portfolio

- Recent Developments

- SWOT Analysis

- Rosenberger Group

- Business Overview

- Company Snapshot

- Company Market Share Analysis

- Company Coverage Portfolio

- Recent Developments

- SWOT Analysis

- AFL Global

- Business Overview

- Company Snapshot

- Company Market Share Analysis

- Company Coverage Portfolio

- Recent Developments

- SWOT Analysis

- Hirose Electric Co., Ltd

- Business Overview

- Company Snapshot

- Company Market Share Analysis

- Company Coverage Portfolio

- Recent Developments

- SWOT Analysis

- Amphenol Corporation

List of Table

- Global Fiber Optic Connectors Market, By Type , 2024-2035(USD Billion)

- Global Lucent Connector, Fiber Optic Connectors Market, By Region, 2024-2035(USD Billion)

- Global Fiber Connector, Fiber Optic Connectors Market, By Region, 2024-2035(USD Billion)

- Global Straight Tip, Fiber Optic Connectors Market, By Region, 2024-2035(USD Billion)

- Global Master Unit, Fiber Optic Connectors Market, By Region, 2024-2035(USD Billion)

- Global Push On/Pull Off, Fiber Optic Connectors Market, By Region, 2024-2035(USD Billion)

- Global Fiber Optic Connectors Market, By Application, 2024-2035(USD Billion)

- Global Datacenter, Fiber Optic Connectors Market, By Region, 2024-2035(USD Billion)

- Global Telecommunication, Fiber Optic Connectors Market, By Region, 2024-2035(USD Billion)

- Global Inter-Building, Fiber Optic Connectors Market, By Region, 2024-2035(USD Billion)

- Global Security System, Fiber Optic Connectors Market, By Region, 2024-2035(USD Billion)

- Global Fiber Optic Connectors Market, By Industries, 2024-2035(USD Billion)

- Global Automotive, Fiber Optic Connectors Market, By Region, 2024-2035(USD Billion)

- Global IT and Telecom, Fiber Optic Connectors Market, By Region, 2024-2035(USD Billion)

- Global Consumer Electronics, Fiber Optic Connectors Market, By Region, 2024-2035(USD Billion)

- North America Fiber Optic Connectors Market, By Type, 2024-2035(USD Billion)

- North America Fiber Optic Connectors Market, By Application, 2024-2035(USD Billion)

- North America Fiber Optic Connectors Market, By Industries, 2024-2035(USD Billion)

- U.S. Fiber Optic Connectors Market, By Type, 2024-2035(USD Billion)

- U.S. Fiber Optic Connectors Market, By Application, 2024-2035(USD Billion)

- U.S. Fiber Optic Connectors Market, By Industries, 2024-2035(USD Billion)

- Canada Fiber Optic Connectors Market, By Type, 2024-2035(USD Billion)

- Canada Fiber Optic Connectors Market, By Application, 2024-2035(USD Billion)

- Canada Fiber Optic Connectors Market, By Industries, 2024-2035(USD Billion)

- Mexico Fiber Optic Connectors Market, By Type, 2024-2035(USD Billion)

- Mexico Fiber Optic Connectors Market, By Application, 2024-2035(USD Billion)

- Mexico Fiber Optic Connectors Market, By Industries, 2024-2035(USD Billion)

- Europe Fiber Optic Connectors Market, By Type, 2024-2035(USD Billion)

- Europe Fiber Optic Connectors Market, By Application, 2024-2035(USD Billion)

- Europe Fiber Optic Connectors Market, By Industries, 2024-2035(USD Billion)

- Germany Fiber Optic Connectors Market, By Type, 2024-2035(USD Billion)

- Germany Fiber Optic Connectors Market, By Application, 2024-2035(USD Billion)

- Germany Fiber Optic Connectors Market, By Industries, 2024-2035(USD Billion)

- France Fiber Optic Connectors Market, By Type, 2024-2035(USD Billion)

- France Fiber Optic Connectors Market, By Application, 2024-2035(USD Billion)

- France Fiber Optic Connectors Market, By Industries, 2024-2035(USD Billion)

- U.K. Fiber Optic Connectors Market, By Type, 2024-2035(USD Billion)

- U.K. Fiber Optic Connectors Market, By Application, 2024-2035(USD Billion)

- U.K. Fiber Optic Connectors Market, By Industries, 2024-2035(USD Billion)

- Italy Fiber Optic Connectors Market, By Type, 2024-2035(USD Billion)

- Italy Fiber Optic Connectors Market, By Application, 2024-2035(USD Billion)

- Italy Fiber Optic Connectors Market, By Industries, 2024-2035(USD Billion)

- Spain Fiber Optic Connectors Market, By Type, 2024-2035(USD Billion)

- Spain Fiber Optic Connectors Market, By Application, 2024-2035(USD Billion)

- Spain Fiber Optic Connectors Market, By Industries, 2024-2035(USD Billion)

- Asia Pacific Fiber Optic Connectors Market, By Type, 2024-2035(USD Billion)

- Asia Pacific Fiber Optic Connectors Market, By Application, 2024-2035(USD Billion)

- Asia Pacific Fiber Optic Connectors Market, By Industries, 2024-2035(USD Billion)

- Japan Fiber Optic Connectors Market, By Type, 2024-2035(USD Billion)

- Japan Fiber Optic Connectors Market, By Application, 2024-2035(USD Billion)

- Japan Fiber Optic Connectors Market, By Industries, 2024-2035(USD Billion)

- China Fiber Optic Connectors Market, By Type, 2024-2035(USD Billion)

- China Fiber Optic Connectors Market, By Application, 2024-2035(USD Billion)

- China Fiber Optic Connectors Market, By Industries, 2024-2035(USD Billion)

- India Fiber Optic Connectors Market, By Type, 2024-2035(USD Billion)

- India Fiber Optic Connectors Market, By Application, 2024-2035(USD Billion)

- India Fiber Optic Connectors Market, By Industries, 2024-2035(USD Billion)

- South America Fiber Optic Connectors Market, By Type, 2024-2035(USD Billion)

- South America Fiber Optic Connectors Market, By Application, 2024-2035(USD Billion)

- South America Fiber Optic Connectors Market, By Industries, 2024-2035(USD Billion)

- Brazil Fiber Optic Connectors Market, By Type, 2024-2035(USD Billion)

- Brazil Fiber Optic Connectors Market, By Application, 2024-2035(USD Billion)

- Brazil Fiber Optic Connectors Market, By Industries, 2024-2035(USD Billion)

- The Middle East and Africa Fiber Optic Connectors Market, By Type, 2024-2035(USD Billion)

- The Middle East and Africa Fiber Optic Connectors Market, By Application, 2024-2035(USD Billion)

- The Middle East and Africa Fiber Optic Connectors Market, By Industries, 2024-2035(USD Billion)

- Billion)

- UAE Fiber Optic Connectors Market, By Type, 2024-2035(USD Billion)

- UAE Fiber Optic Connectors Market, By Application, 2024-2035(USD Billion)

- UAE Fiber Optic Connectors Market, By Industries, 2024-2035(USD Billion)

- South Africa Fiber Optic Connectors Market, By Type, 2024-2035(USD Billion)

- South Africa Fiber Optic Connectors Market, By Application, 2024-2035(USD Billion)

- South Africa Fiber Optic Connectors Market, By Industries, 2024-2035(USD Billion)

List of Figures

- Global Fiber Optic Connectors Market Segmentation

- Fiber Optic Connectors Market: Research Methodology

- Market Size Estimation Methodology: Bottom-Up Approach

- Market Size Estimation Methodology: Top-down Approach

- Data Triangulation

- Porter’s Five Forces Analysis

- Value Chain Analysis

- Top investment pocket in the Fiber Optic Connectors Market

- Top Winning Strategies, 2024-2035

- Top Winning Strategies, By Development, 2024-2035(%)

- Top Winning Strategies, By Company, 2024-2035

- Moderate Bargaining power of Buyers

- Moderate Bargaining power of Suppliers

- Moderate Bargaining power of New Entrants

- Low threat of Substitution

- High Competitive Rivalry

- Top Player Positioning, 2024

- Market Share Analysis, 2024

- Restraint and Drivers: Fiber Optic Connectors Market

- Fiber Optic Connectors Market Segmentation, By Type

- Fiber Optic Connectors Market For Lucent Connector, By Region, 2024-2035 ($ Billion)

- Fiber Optic Connectors Market For Fiber Connector, By Region, 2024-2035 ($ Billion)

- Fiber Optic Connectors Market For Straight Tip, By Region, 2024-2035 ($ Billion)

- Fiber Optic Connectors Market For Master Unit, By Region, 2024-2035 ($ Billion)

- Fiber Optic Connectors Market For Push On/Pull Off, By Region, 2024-2035 ($ Billion)

- Fiber Optic Connectors Market Segmentation, By Application

- Fiber Optic Connectors Market For Datacenter, By Region, 2024-2035 ($ Billion)

- Fiber Optic Connectors Market For Telecommunication, By Region, 2024-2035 ($ Billion)

- Fiber Optic Connectors Market For Inter-Building, By Region, 2024-2035 ($ Billion)

- Fiber Optic Connectors Market For Security System, By Region, 2024-2035 ($ Billion)

- Fiber Optic Connectors Market Segmentation, By Industries

- Fiber Optic Connectors Market For Automotive, By Region, 2024-2035 ($ Billion)

- Fiber Optic Connectors Market For IT and Telecom, By Region, 2024-2035 ($ Billion)

- Fiber Optic Connectors Market For Consumer Electronics, By Region, 2024-2035 ($ Billion)

- Amphenol Corporation: Net Sales, 2024-2035 ($ Billion)

- Amphenol Corporation: Revenue Share, By Segment, 2024 (%)

- Amphenol Corporation: Revenue Share, By Region, 2024 (%)

- TE Connectivity: Net Sales, 2024-2035 ($ Billion)

- TE Connectivity: Revenue Share, By Segment, 2024 (%)

- TE Connectivity: Revenue Share, By Region, 2024 (%)

- Corning Incorporated: Net Sales, 2024-2035 ($ Billion)

- Corning Incorporated: Revenue Share, By Segment, 2024 (%)

- Corning Incorporated: Revenue Share, By Region, 2024 (%)

- CommScope: Net Sales, 2024-2035 ($ Billion)

- CommScope: Revenue Share, By Segment, 2024 (%)

- CommScope: Revenue Share, By Region, 2024 (%)

- Molex: Net Sales, 2024-2035 ($ Billion)

- Molex: Revenue Share, By Segment, 2024 (%)

- Molex: Revenue Share, By Region, 2024 (%)

- Sumitomo Electric Industries: Net Sales, 2024-2035 ($ Billion)

- Sumitomo Electric Industries: Revenue Share, By Segment, 2024 (%)

- Sumitomo Electric Industries: Revenue Share, By Region, 2024 (%)

- Furukawa Electric Co., Ltd.: Net Sales, 2024-2035 ($ Billion)

- Furukawa Electric Co., Ltd.: Revenue Share, By Segment, 2024 (%)

- Furukawa Electric Co., Ltd.: Revenue Share, By Region, 2024 (%)

- Fujikura Ltd.: Net Sales, 2024-2035 ($ Billion)

- Fujikura Ltd.: Revenue Share, By Segment, 2024 (%)

- Fujikura Ltd.: Revenue Share, By Region, 2024 (%)

- Sterlite Technologies Ltd..: Net Sales, 2024-2035 ($ Billion)

- Sterlite Technologies Ltd..: Revenue Share, By Segment, 2024 (%)

- Sterlite Technologies Ltd..: Revenue Share, By Region, 2024 (%)

- 3M: Net Sales, 2024-2035 ($ Billion)

- 3M: Revenue Share, By Segment, 2024 (%)

- 3M: Revenue Share, By Region, 2024 (%)

- Broadcom Inc.: Net Sales, 2024-2035 ($ Billion)

- Broadcom Inc.: Revenue Share, By Segment, 2024 (%)

- Broadcom Inc.: Revenue Share, By Region, 2024 (%)

- Radiall S.A.: Net Sales, 2024-2035 ($ Billion)

- Radiall S.A.: Revenue Share, By Segment, 2024 (%)

- Radiall S.A.: Revenue Share, By Region, 2024 (%)

- Rosenberger Group: Net Sales, 2024-2035 ($ Billion)

- Rosenberger Group: Revenue Share, By Segment, 2024 (%)

- Rosenberger Group: Revenue Share, By Region, 2024 (%)

- AFL Global: Net Sales, 2024-2035 ($ Billion)

- AFL Global: Revenue Share, By Segment, 2024 (%)

- AFL Global: Revenue Share, By Region, 2024 (%)

- Hirose Electric Co., Ltd: Net Sales, 2024-2035 ($ Billion)

- Hirose Electric Co., Ltd: Revenue Share, By Segment, 2024 (%)

- Hirose Electric Co., Ltd: Revenue Share, By Region, 2024 (%)

Check Licence

Choose the plan that fits you best: Single User, Multi-User, or Enterprise solutions tailored for your needs.

We Have You Covered

- 24/7 Analyst Support

- Clients Across the Globe

- Tailored Insights

- Technology Tracking

- Competitive Intelligence

- Custom Research

- Syndicated Market Studies

- Market Overview

- Market Segmentation

- Growth Drivers

- Market Opportunities

- Regulatory Insights

- Innovation & Sustainability

Report Details

| Scope | Global |

| Pages | 210 |

| Delivery | PDF & Excel via Email |

| Language | English |

| Release | Apr 2026 |

| Access | Download from this page |