Global Geysers Market

Global Geysers Market Size, Share, By Product Type (Electric, Gas, Solar) By Technology (Storage, Tankless, Hybrid) By Capacity (Below 30 Liters, 30-100 Liters, 100-250 Liters, 250-400 Liters, above 400 Liters) By Application (Residential, Commercial, Industrial) and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa), Analysis and Forecast 2026-2035

CAGR

5.86%

REVENUE 2025

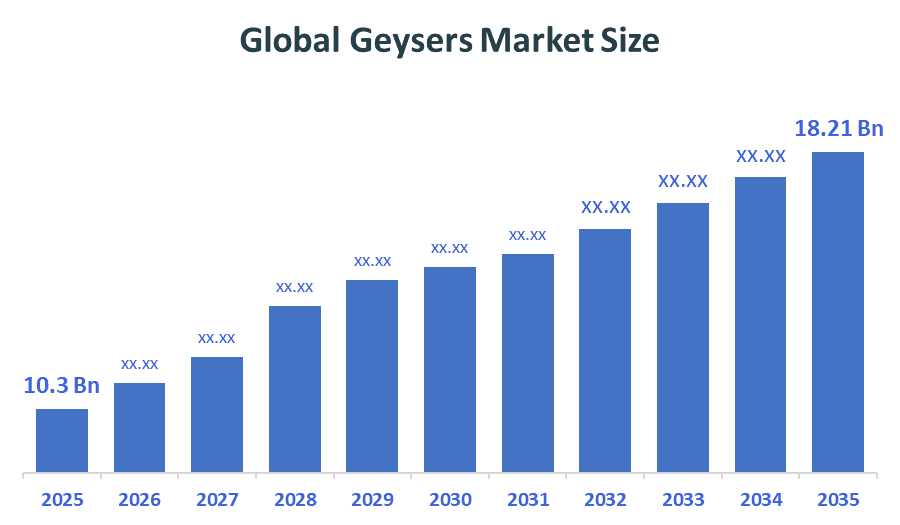

USD Billion 10.3

FORECAST 2035

USD Billion 18.21

REPORT COVERAGE

Global

The Global Geysers Market Size was predicted to grow from USD 10.3 Billion in 2025 and is projected to reach around USD 18.21 Billion by 2035. According to Decision Advisors, a detailed research report on the water heater market shows that the electric geyser segment dominates the global market, holding approximately 51% of the total share worldwide. A.O. Smith Corporation leads the market with a reported total annual revenue of $3.83 Billion in 2025, making it one of the major market drivers for shaping the industry.

Market Snapshot

- Global Geysers Market Size (2025): USD 10.3 Billion

- Global Geysers Projected Market Size (2035): USD 18.21 Billion

- Global Geysers Compound Annual Growth Rate (CAGR): 5.86%

- Largest Regional Market: Asia-Pacific

- Fastest Growing Region: North America

- 3rd Largest Region: Europe

- Base Year: 2025

- Historical Period: 2021 - 2024

- Forecast Period: 2026 - 2035

Market Overview / Introduction

Geysers are specialised water-heating appliances engineered to deliver temperature-controlled water for domestic, commercial, and industrial hygiene, acting as the essential bridge between raw energy sources and high-efficiency thermal delivery. The industry has undergone a significant technological shift, evolving from rudimentary immersion-based heaters to advanced, AI-native smart appliances characterised by plasma-welded, glass-lined tanks, high-density CFC-free insulation, and IoT-enabled predictive maintenance. These systems are now primarily deployed in high-demand residential environments and specialised commercial sectors like hospitality and healthcare, where precision heating is critical for operational efficiency. To accelerate the transition toward sustainability, 2026 has seen pivotal government interventions, such as the U.S. Department of Energy’s (DOE) October 2026 mandate requiring all new commercial water heaters to meet a 95% condensing efficiency standard, alongside India’s expanded Jal Jeevan Mission, which continues to drive plumbing infrastructure to 100% of rural households. The combined impact of these regulations and innovations has fundamentally transformed the market into a smart ecosystem, protecting consumers from rising utility costs through 20-30% energy reductions while ensuring long-term climate resilience through cleaner, decarbonised heating cycles.

- The residential segment contributes to approximately 54.4% of the application-based use in the market, driven by the increasing demand for urban housing, improved living standards, and the adoption of modern bathroom fixtures.

- There is an exponential rise in the development of solar-powered geysers in the commercial sector, and the CAGR is predicted to remain robust because of the growing application of renewable energy in hotels and hospitals to offer optimized operational costs.

Notable Insights: -

- Electric geyser modules make up about 51% of the total market share of this sector. They have gained a reputation for ease of installation, particularly in urban apartments, small businesses, and rental properties.

- Storage-based systems account for almost 54.5% of all demand. The widespread availability of various tank capacities allows these units to remain the standard choice for households requiring high volumes of hot water simultaneously.

- Smart IoT-enabled geysers show an annual increase above 6.5%. The rise in smart home adoption and frequent occurrences of energy conservation mandates encourage enterprises to invest more money in connected water heating solutions.

What is the Role of Technology in Shaping the Market?

The advancements in technology have made some major changes in the water heating industry regarding heating efficiency, tank longevity, and user safety. Geyser technology of the current generation has evolved beyond being mere heating coils to smart thermal devices that can operate with minimal energy waste because they are able to use nano-polymer coatings, plasma-welded tanks, and AI algorithms for usage pattern recognition.

How are Recent Developments Helping the Market?

They involve the use of heat pump technology, anti-bacterial coating systems, and multi-stage safety valves. These innovations have played an important role in facilitating growth and development within the market. There have been innovations involving the development of geysers that are able to resist hard water corrosion, which are able to protect all types of heating elements used in household goods to industrial-grade systems. Such innovations would facilitate the production of compact, high-performance units using the insulation properties of modern materials, without losing heat or experiencing premature tank failure.

Market Drivers

The market demand for global geysers is on the rise due to higher investments by consumers and governments into energy-efficient home appliances and green building infrastructure capable of meeting climate goals. Modern geysers have enjoyed significant market popularity because of their advantages of combining multiple properties in one durable system, such as high thermal stability, digital temperature control, and effective pressure handling. On the other hand, the establishment of smart city projects has brought about greater demands for water heating solutions to address the trend of shifting from conventional low-efficiency heaters to smart-grid compatible geysers.

Restraints

However, the development of the global market for the geyser industry is limited by the complexities involved in maintaining the stability of the price of raw materials such as stainless steel and specialized insulation foam, considering that the market may be characterized by fluctuations that lead to price hikes for the end consumer.

Competitive Analysis:

The report offers the appropriate analysis of the key organisations/companies involved within the geysers market, along with a comparative evaluation primarily based on their product offerings, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborate analysis focusing on the current news and developments of the companies, which includes product development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

Top 10 Companies in the Global Geysers Market

- A.O. Smith Corporation

- Rheem Manufacturing Company

- Ariston Holding N.V.

- Bosch Thermotechnology Corp.

- Rinnai Corporation

- Bradford White Corporation

- Bajaj Electricals Ltd.

- Haier Smart Home Co., Ltd.

- Havells India Ltd.

- Noritz Corporation

Government Initiatives

|

Country |

Key Government Initiatives |

|

China |

Under the 15th Five-Year Plan (2026-2030), the government has prioritised the expansion of natural gas pipelines to rural areas, driving the adoption of gas-based tankless geysers in previously underserved regions. |

|

India |

The Jal Jeevan Mission, extended into 2026 with a budget of ?67,670 Crore, focuses on providing tap water connections to 100% of rural households, significantly expanding the potential consumer base for water heaters. |

|

US |

The Department of Energy has updated energy conservation standards for residential water heaters in 2026, mandating a shift toward heat pump technology for larger capacity units to reduce national energy demand. |

Study on the Supply, Demand, Distribution, and Market Environment

The geyser market in 2026 operates at a critical intersection where manufacturers must balance high-performance thermal efficiency with a growing consumer demand for affordable, long-lasting hardware. Supply chains have become increasingly vertically integrated to buffer against price swings in essential raw materials like copper and high-grade stainless steel. Production now centers on using specialised anti-corrosive alloys and ultra-high-density, CFC-free insulation that ensures sustained heat retention, effectively eliminating the energy waste common in older designs. Distribution has shifted toward a hybrid-omnichannel model, where digital sales now account for over 40% of the market in several regions, supported by localised service networks that ensure rapid installation. This environment is particularly robust in the Asia-Pacific region, where government-led rural electrification and rapid urbanisation continue to outpace supply, creating a fertile ground for manufacturers who can deliver value-engineered units that do not compromise on durability or safety.

Price Analysis and Consumer Behaviour Analysis

Pricing for geysers is increasingly dictated by a cost-per-efficiency logic, influenced by tank capacity, Energy Star ratings, and the depth of integrated smart features. Premium models utilise expensive, sophisticated materials such as titanium-shielded elements and plasma-welded tanks to offer superior protection against hard-water scaling, commanding a higher price point for long-term reliability. Conversely, the market for standard electric storage geysers remains highly competitive and affordable, providing a low-barrier entry for consumers replacing ageing immersion or legacy systems. Behaviourally, modern consumers are becoming efficiency-first buyers; data indicates that nearly 60% of market leaders are investing in smart controls as users move toward appliances that offer active energy monitoring. This shift demonstrates a clear preference for products that are not only easy to install but also provide transparent, real-time data on electricity consumption, allowing households to manage their utility bills more effectively.

Market Segmentation

The Global Geysers Market share is classified into product type, technology, capacity, and application.

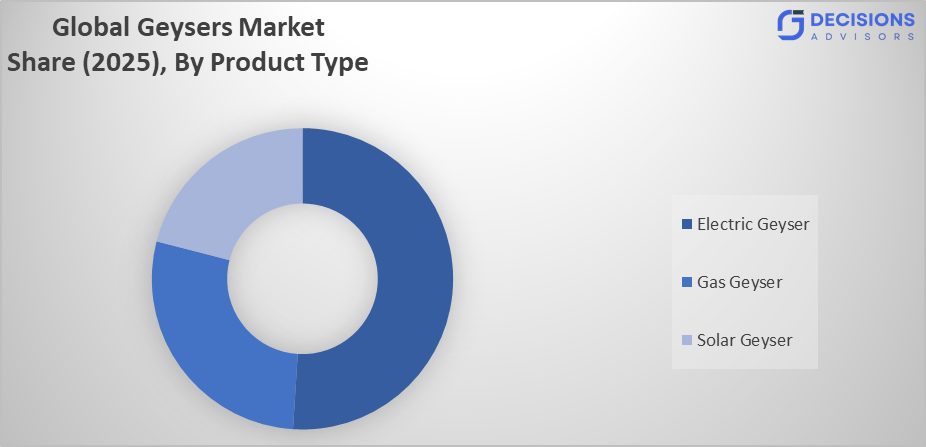

The Electric Geyser segment holds the largest share, contributing approximately 51% of the market in 2025.

Based on the Product Type, the global geysers market is divided into electric, gas, and solar. Among these, the Electric Geyser segment holds the largest share, contributing approximately 51% of the market in 2025. The reason for this dominance lies in the widespread availability of electrical infrastructure and the low initial cost of installation compared to solar or gas-piped alternatives.

The Storage segment accounts for the largest share, representing over 54.5% of the global market in 2025.

Based on the Technology, the global geysers market is divided into storage, tankless, and hybrid. Among these, the Storage segment accounts for the largest share, representing over 54.5% of the global market in 2025. These units are critical for residential applications, providing high-volume water supply and high-speed delivery through the adoption of standard pressurised tank designs. On the other hand, the Tankless segment has emerged as a rapidly growing sector, thanks to the increasing adoption of space-saving heating units in compact urban apartments.

The 30-100 Litres segment dominates the global market, accounting for approximately 42% of the total revenue in 2025.

Based on the Capacity, the global geysers market is divided into below 30 Litres, 30-100 Liters, 100-250 Liters, 250-400 Liters, and above 400 Liters. Among these, the 30-100 Litres segment dominates the global market, accounting for approximately 42% of the total revenue in 2025. This segment is preferred by residential households that require reliable performance and sufficient capacity for daily family needs. The Above 400 Litres category is seeing a steady increase in use, especially in the industrial sector, where high-capacity water heating is required for large-scale operations.

The Residential segment dominates the global market, accounting for approximately 54.4% of the total revenue in 2025.

Based on the Application, the global geysers market is divided into residential, commercial, and industrial. Among these, the Residential segment dominates the global market, accounting for approximately 54.4% of the total revenue in 2025. This segment is preferred by planners who require reliable hot water for daily domestic activities and modern living standards. The Automotive segment is seeing a sharp increase in use, especially by manufacturers who value the high-temperature resistance and efficiency of advanced heating systems for industrial cleaning and processing.

Strategies to Implement for Growth of the Market in Non-Leading Regions

The possibilities of growth for the geyser industry in the emerging regions can be enhanced through the creation of efficient localised assembly lines for the use of local machinery manufacturers, as well as local bodies responsible for managing the electrification process of the rural regions. The initiatives from the government focused on self-sufficiency for the industries, together with an increase in the manufacture of appliances, play a major role in creating a demand in those regions that face difficulties regarding the importation of high-quality heating appliances. The additional assistance of investment in the training of local thermal engineers, together with regional quality control labs, will help achieve this.

Regional Segment Analysis of the Global Geysers Market

- North America (U.S., Canada, Mexico)

- Europe (Germany, France, U.K., Italy, Spain, Rest of Europe)

- Asia-Pacific (China, Japan, India, South Korea, Rest of APAC)

- Latin America (Brazil and the Rest of Latin America)

- The Middle East and Africa (UAE, South Africa, Rest of MEA)

Asia-Pacific is projected to be the largest region over the forecast period. This region is anticipated to witness a growth rate of around 6.15% CAGR, maintaining a dominant market share within the global industry. In 2025, the Asia-Pacific region will already account for approximately 37.7% of global revenue. This is owing to the fast-developing electronics manufacturing hubs, coupled with the growing demand for industrial machinery in countries such as China, India, and Vietnam. Other reasons for the same include greater investments made toward infrastructure development in the region, state-supported indigenous manufacturing projects for electrical equipment, and widespread adoption of high-efficiency appliance standards.

North America is expected to hold a significant share of the geyser market during the forecast period. This region holds approximately 18.5% share of global revenue in 2025, thanks to its highly sophisticated residential sector, along with the extensive adoption of energy-efficient technology in both national energy goals and high-value industrial applications. The largest part of this region’s revenues comes from the United States, as there is a lot of spending at the corporate level in modernization programs for aging infrastructure, along with local research related to advanced heating materials.

Europe is anticipated to hold a substantial share, contributing approximately 22.4% of the global market share. There is a competitive advantage in the region owing to clusters of engineering innovation and financing for sustainable industrial transitions, as well as electrical efficiency research. There is also a comparative advantage with countries like Germany and Italy, which are highly skilled at precision manufacturing for high-performance heating units. Moreover, the rigorous environmental standards regarding material recyclability and energy waste further give them a competitive advantage.

Recent Developments

- In February 2026, Hammond Power Solutions announced a definitive agreement to acquire AEG Power Solutions in an all-cash transaction valued at approximately USD 263 million, marking a significant consolidation in the power equipment sector.

- In October 2025, Premier Energies approved the acquisition of a 51% stake in Transcon Industries. This strategic investment signifies the company's diversification into specialised power equipment and industrial heating manufacturing.

- In May 2024, Superior Essex successfully completed the full buyout of the Essex Furukawa joint venture. This consolidation allows for unified production assets and streamlined R&D for sustainable, high-efficiency heating and conductor materials.

- In November 2021, Furukawa Electric launched the BRACE X blue-IR hybrid laser system, a technological breakthrough that improves welding efficiency in electrical components, reducing manufacturing power consumption by 30%.

Market Segmentation

This study forecasts revenue at global, regional, and country levels from 2021 to 2035. The Global Geysers Market is segmented based on the following categories:

Global Geysers Market, By Product Type

- Electric

- Gas

- Solar

Global Geysers Market, By Technology

- Storage

- Tankless

- Hybrid

Global Geysers Market, By Capacity

- Below 30 Litres

- 30-100 Litres

- 100-250 Litres

- 250-400 Litres

- Above 400 Litres

Global Geysers Market, By Application

- Residential

- Commercial

- Industrial

Global Geysers Market, By Regional Analysis

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- United Arab Emirates

- Saudi Arabia

- Qatar

- South Africa

- Rest of Middle East & Africa

Frequently Asked Questions (FAQ)

What is the significance of corona-resistant insulation in modern geyser components?

Advanced water heaters often utilize inverter-fed systems which can face problems associated with voltage spikes. Corona-resistant insulation in the internal wiring and heating elements is necessary for extending the service life of geysers applied in modern smart-home automation systems and frequency-controlled drive applications.

How does the transition to smart-grid architectures affect geyser specifications?

The adoption of high-voltage smart systems requires the use of special internal designs that can withstand variable electrical loads. Modern geysers are now designed with high thermal class ratings (H or C) to handle the increased dielectric pressure, ensuring that high-efficiency units remain stable during peak grid usage.

What role does oxygen-free copper (OFC) play in high-performance geyser manufacturing?

Oxygen-free copper leads to improved conductivity and increased ductility in the heating elements. For geysers requiring rapid heating or miniaturized internal components, OFC offers the necessary mechanical strength to avoid damage during high-intensity thermal operations.

What are the primary differences in the application of electric versus solar geysers in 2026?

While electric geysers remain the standard for high-efficiency and space-constrained urban applications, solar geysers are seeing increased adoption in standalone residential homes and commercial developments. Solar units significantly reduce long-term operational costs, making them ideal for weight-sensitive or cost-driven projects where a larger physical footprint for panels can be accommodated

Check Licence

Choose the plan that fits you best: Single User, Multi-User, or Enterprise solutions tailored for your needs.

We Have You Covered

- 24/7 Analyst Support

- Clients Across the Globe

- Tailored Insights

- Technology Tracking

- Competitive Intelligence

- Custom Research

- Syndicated Market Studies

- Market Overview

- Market Segmentation

- Growth Drivers

- Market Opportunities

- Regulatory Insights

- Innovation & Sustainability

Report Details

| Scope | Global |

| Pages | 210 |

| Delivery | PDF & Excel via Email |

| Language | English |

| Release | Apr 2026 |

| Access | Download from this page |