Global Glaucoma Surgery Devices Market

The Global Glaucoma Surgery Devices Market Size, Share by Product Type (Glaucoma Drainage Devices, Glaucoma Laser Devices, Minimally Invasive Glaucoma Surgery (MIGS) Devices), by Application (Trabeculectomy, Glaucoma Drainage Implant Surgery, Minimally Invasive Glaucoma Surgery (MIGS)), by End User (Hospitals, Ambulatory Surgical Centers, Specialty Eye Clinics), and by Region (North America, Europe, Asia-Pacific, Latin America, Middle East & Africa), Analysis and Forecast 2026-2035

CAGR

4.85%

REVENUE 2025

USD Billion 1.8

FORECAST 2035

USD Billion 2.89

REPORT COVERAGE

Global

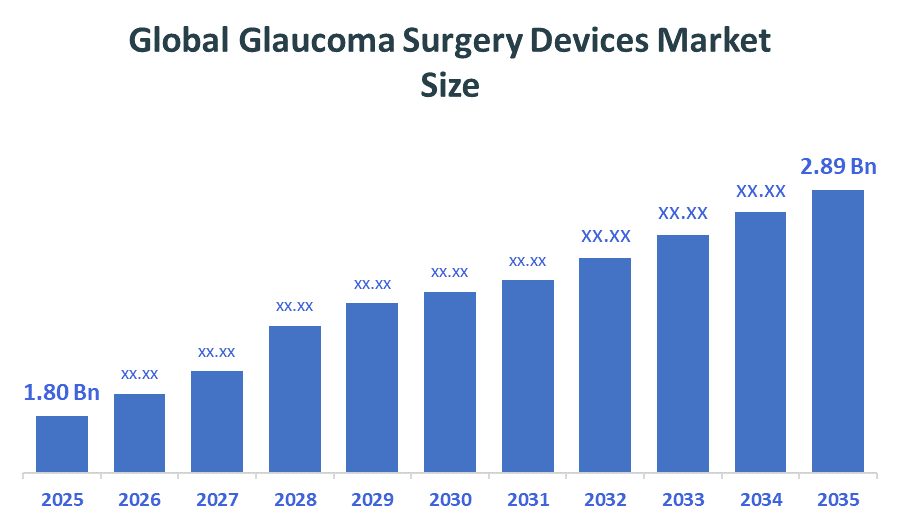

The Global Glaucoma Surgery Devices Market Size is foreseen to grow from USD 1.80 Billion in 2025 and is govern to reach around USD 2.89 Billion by 2035. According to Decision Advisors, a detailed research report on the global glaucoma surgery devices market is boosted by accelerated adoption of Minimally Invasive Glaucoma Surgery (MIGS), accounting for nearly upto the 40-45% share of the total share worldwide. Alcon, Inc is the prime player in the market with approximately 5.8 Billion in annual turnover and a 55-60% market share, positioning it as the primary driver of the global glaucoma surgery devices market.

Market Snapshot

- Global Glaucoma Surgery Devices Market Size (2025): USD 1.80 Billion

- Projected Global Glaucoma Surgery Devices Market Size (2035): USD 2.89 Billion

- Global Glaucoma Surgery Devices Market Compound Annual Growth Rate (CAGR): 4.85%

- Largest Regional Market: North America

- Fastest Growing Region: Asia Pacific

- 2nd Largest Region: Europe

- Base Year: 2025

- Historical Period: 2021–2024

- Forecast Period: 2026–2035

Market Overview/ Introduction

The Glaucoma Surgery Devices Market as a high-tech toolkit designed to save patients sight. Glaucoma is often called the silent thief of sight because it builds up pressure inside the eye, slowly damaging the optic nerve. This market is essentially the global industry that builds the stents, valves, and lasers doctors use to relieve that pressure and stop blindness before it starts. The biggest change happening right now is a move toward gentler medicine. Instead of the old-school, heavy-duty surgeries that required long recovery times, more patients are choosing MIGS (Minimally Invasive Glaucoma Surgery). These procedures use small, microscopic stents to drain fluid, and they’re so safe that doctors often perform them at the same time as a routine cataract surgery. This shift is a huge deal MIGS now makes up nearly half of the entire market. Behind the scenes, companies like Alcon and Glaukos are the heavy hitters propelling the charge. They’re focusing on making surgeries faster and more precise by using AI and advanced lasers. The real reason the market is growing so fast, though, is simply because we’re living longer; as the world's population ages, more of us will need these life-changing tools to keep our vision clear.

Notable Insights: -

- North America is anticipated to hold the largest share, approximately 41% of the global glaucoma surgery devices market over the predicted timeframe.

- Asia Pacific is expected to grow at the fastest CAGR in the global glaucoma surgery devices market during the forecast period, with growth rates estimated at around 10.2% CAGR.

- By product type, the minimally invasive glaucoma surgery (MIGS) devices segment dominated the market in 2025 with approximately 55% share, and is projected to grow at a substantial CAGR during the forecast period.

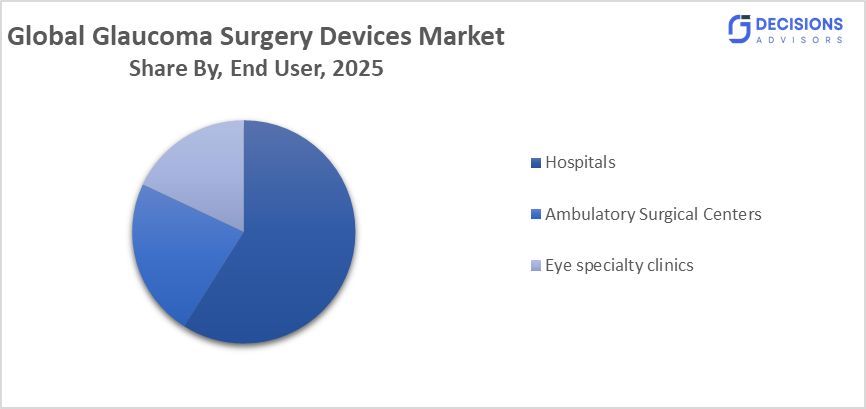

- By end user, the hospitals segment dominated the market in 2025 with approximately 60% share, and is projected to grow at a substantial CAGR during the forecast period.

- The compound annual growth rate of the global glaucoma surgery devices market is 4.85%.

- The market is likely to achieve a valuation of USD 2.89 Billion by 2035.

What is the role of technology in grooming the market?

Technology plays a crucial role in shaping the glaucoma surgery devices market by enabling safer, more precise, and minimally invasive treatment options. Innovations such as minimally invasive glaucoma surgery (MIGS) devices, advanced laser systems, and biocompatible implants help improve intraocular pressure control while reducing complications and recovery time. Additionally, integration of imaging technologies and smart surgical tools enhances accuracy during procedures, leading to better patient outcomes and increased adoption of advanced glaucoma surgical solutions.

Market Drivers

The Thing which really pushing this market forward is a mix of how we’re ageing and a major shift in how we think about health. Since glaucoma is almost entirely a wear-and-tear condition of the eye, the fact that we are living longer than ever before means the number of people needing help is skyrocketing. It’s estimated that by 2030, tens of millions of people will fall into the high-risk age bracket. On top of that, lifestyle diseases like diabetes which are becoming more common double the risk of developing glaucoma, creating a massive, urgent need for new solutions. But there’s also a very human side to this, eye-drop fatigue. For years, the only real way to manage glaucoma was a lifetime of expensive daily drops that can be a hassle to remember and often cause irritation. Now, both doctors and patients are leaning toward one-and-done surgical fixes. Thanks to new, gentler tech like tiny micro-stents (MIGS), surgery isn't the scary, last-resort option it used to be. It’s now a proactive, safe way to protect vision early on, letting people get back to their lives without having to worry about a bottle of eye drops every single morning.

Restrain

The glaucoma surgery devices market faces several restraints, primarily due to the high cost of advanced devices such as MIGS implants and laser systems, which limits adoption in cost-sensitive and developing regions. Additionally, the need for skilled ophthalmic surgeons and specialized training can restrict widespread use. Risks associated with surgical complications and variability in patient outcomes also pose challenges, while limited awareness and access to advanced eye care further hinder market growth.

Competitive Analysis:

The report offers the appropriate analysis of the key organizations/companies involved within the global glaucoma surgery devices market, along with a comparative evaluation primarily based on their product of offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes product development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

Top Companies in the Global Glaucoma Surgery Devices Market

- Alcon Inc.

- Johnson & Johnson Vision

- Glaukos Corporation

- New World Medical Inc.

- Santen Pharmaceutical Co., Ltd.

- Lumenis Ltd.

- BVI Medical (Beaver-Visitec International)

- Sight Sciences Inc.

- Carl Zeiss Meditec AG

- AbbVie Inc. (Allergan)

Government Initiatives

|

Country |

Key Government Initiatives |

|

India |

National Program for Control of Blindness (NPCB): Large-scale screening and early detection programs for glaucoma. VISION 2020: Right to Sight-India (partnership with WHO & IAPB): Awareness campaigns like Eye Donation Fortnight and World Sight Day. Ayushman Bharat: Expanding access to ophthalmic surgeries, including glaucoma treatment, under public health insurance. |

|

China |

WHO & IAPB Partnerships: Programs addressing cataracts and glaucoma through awareness and surgical camps. Made in China 2025: Encouraging domestic manufacturing of ophthalmic devices. NGO Collaboration: Eye health initiatives in Africa supported by international agencies. |

|

Japan |

Expanded Insurance Reimbursement: Coverage for MIGS and laser-based glaucoma surgeries. Government-Led Screening Programs: Early detection initiatives targeting ageing populations. Regulatory Facilitation: Fast-track approvals for advanced glaucoma devices. |

Study on the Supply, Demand, Distribution, and Market Environment of the Global Glaucoma Surgery Devices Market

The global glaucoma surgery devices market shows a strong balance between supply, demand, distribution, and overall market environment, driven by the rising prevalence of glaucoma and increasing preference for surgical treatment. Demand is primarily led by hospitals and ophthalmic clinics due to high surgical volumes, while supply is supported by continuous innovation in MIGS devices, implants, and laser systems. Distribution occurs mainly through direct hospital procurement and specialized medical distributors. Overall, the market environment remains technology-driven and moderately competitive, with increasing focus on minimally invasive procedures and improved patient outcomes.

Price Analysis and Consumer Behaviour Analysis

Price analysis in the glaucoma surgery devices market indicates that advanced solutions such as MIGS implants and laser systems are relatively high-cost, typically ranging from USD 500 to USD 2,000 per device, depending on technology and functionality. From a consumer behaviour perspective, hospitals account for nearly 60% of total demand, as they prioritise clinical effectiveness, safety, and long-term patient outcomes over pricing. Additionally, there is a growing preference among healthcare providers for minimally invasive and technologically advanced devices, reflecting an increasing willingness to invest in premium solutions that reduce complications and improve surgical success rates.

Market Segmentation

The Global Glaucoma Surgery Devices Market share is classified into product type, application, and end user.

- The minimally invasive glaucoma surgery (MIGS) devices segment dominated the market in 2025 with approximately 55% share, and is projected to grow at a substantial CAGR during the forecast period.

Based on the product type, the global glaucoma surgery devices market is divided into glaucoma drainage devices, glaucoma laser devices, and minimally invasive glaucoma surgery (MIGS) devices. Among these, the MIGS devices segment dominated the market in 2025 with approximately 55% share, owing to their safety, reduced surgical time, and faster patient recovery. For instance, MIGS devices such as micro-stents are widely used to lower intraocular pressure with minimal tissue damage. Additionally, advancements in biocompatible materials and implant design (2023–2025) have improved clinical outcomes and adoption rates. Glaucoma drainage and laser devices are expected to witness steady growth due to their continued use in advanced and complex cases.

- The minimally invasive glaucoma surgery (MIGS) segment accounted for the largest share in 2025 with approximately 45%, and is anticipated to grow at a significant CAGR during the forecast period.

Based on the application, the global glaucoma surgery devices market is divided into trabeculectomy, glaucoma drainage implant surgery, and minimally invasive glaucoma surgery (MIGS). Among these, the MIGS segment accounted for the largest share in 2025 with approximately 45%, driven by increasing preference for less invasive procedures and improved safety profiles. For example, MIGS procedures are widely adopted for early to moderate glaucoma treatment due to shorter recovery times and fewer complications. Moreover, increasing awareness and adoption of advanced surgical techniques (2023–2025) are enhancing demand. Trabeculectomy and drainage implant surgeries continue to be used for severe glaucoma cases.

- The hospitals segment dominated the market in 2025 with approximately 60% share, and is projected to grow at a substantial CAGR during the forecast period.

Based on the end user, the global glaucoma surgery devices market is divided into hospitals, ambulatory surgical centers, and specialty eye clinics. Among these, the hospitals segment dominated the market in 2025 with approximately 60% share, due to the availability of advanced ophthalmic infrastructure, skilled surgeons, and high patient inflow. For instance, hospitals are the primary centers for glaucoma surgeries, including complex and high-risk procedures, requiring advanced surgical devices. Furthermore, increasing investments in healthcare infrastructure and ophthalmic equipment (2023–2025) are driving segment growth. Ambulatory surgical centers are expected to grow steadily due to the rising demand for cost-effective and outpatient eye procedures.

Strategies to Implement for Growth of the Market in Non-Leading Regions

To drive growth of the glaucoma surgery devices market in non-leading regions, companies should focus on developing cost-effective MIGS devices and expanding local manufacturing to improve affordability and access. Strengthening partnerships with regional hospitals and training ophthalmologists in advanced surgical techniques can significantly boost adoption. Increasing awareness through screening programs is also critical, as many glaucoma cases remain undiagnosed. For example, India’s National Programme for Control of Blindness (NPCB) has helped expand eye care services and early diagnosis, creating opportunities for surgical device adoption. Additionally, collaborations between global companies and local distributors such as expanding presence in Southeast Asia and Africa—can improve distribution networks and market penetration.

Regional Segment Analysis of the Global Glaucoma Surgery Devices Market

- North America (U.S., Canada, Mexico)

- Europe (Germany, France, U.K., Italy, Spain, Rest of Europe)

- Asia-Pacific (China, Japan, India, Rest of APAC)

- South America (Brazil and the Rest of South America)

- The Middle East and Africa (UAE, South Africa, Rest of MEA)

North America is anticipated to hold the largest share, approximately 41% of the Global Glaucoma Surgery Devices Market over the predicted timeframe.

North America is anticipated to hold the largest share, approximately 41% of the Global Glaucoma Surgery Devices Market over the predicted timeframe. The region dominates due to its advanced ophthalmic healthcare infrastructure and high adoption of technologically advanced surgical devices, particularly in the United States and Canada, where minimally invasive glaucoma surgeries (MIGS) are widely performed. Additionally, the region reports a high prevalence of glaucoma and conducts a large volume of ophthalmic procedures annually, creating strong demand for surgical devices. A key recent development includes the increasing adoption of MIGS implants and laser-based glaucoma treatments between 2023–2025, improving patient outcomes and reducing surgical risks. Strong reimbursement frameworks and continuous technological advancements are further strengthening market dominance.

Asia Pacific is expected to grow at the fastest CAGR in the Global Glaucoma Surgery Devices Market during the forecast period, with growth rates estimated at approximately 10.2% CAGR.

Asia Pacific is expected to grow at the fastest CAGR in the Global Glaucoma Surgery Devices Market during the forecast period, with growth rates estimated at approximately 10.2% CAGR. The region has a rapidly expanding ageing population and increasing prevalence of glaucoma, with countries such as China and India being key contributors. Growth is driven by rising healthcare expenditure, improving eye care infrastructure, and increasing awareness about early diagnosis and treatment. For instance, countries like India and China are investing significantly in ophthalmic care programs and surgical capacity expansion, boosting the adoption of glaucoma surgery devices. Additionally, the expansion of private hospitals and government initiatives supporting vision care are accelerating market growth.

Europe is the second largest region in the Global Glaucoma Surgery Devices Market during the forecast period, holding approximately 28% share.

Europe is the second largest region in the Global Glaucoma Surgery Devices Market during the forecast period, holding approximately 28% share, supported by well-established healthcare systems and increasing adoption of advanced ophthalmic surgical technologies. The region benefits from strong regulatory frameworks and widespread availability of modern medical devices, with countries such as Germany, France, and the UK leading the market. A recent development includes increased adoption of MIGS devices and laser-based glaucoma treatments between 2023–2025, improving surgical outcomes and patient safety. Additionally, the rising ageing population and growing burden of glaucoma have further strengthened demand for surgical devices across the region.

Future Market Trends in the Global Glaucoma Surgery Devices Market: -

1. Rapid Adoption of Minimally Invasive Glaucoma Surgery (MIGS)

The market is strongly shifting toward MIGS devices due to their safer profile, faster recovery, and reduced complications compared to traditional surgeries. The MIGS segment alone is projected to grow steadily, reaching USD 781.2 million by 2030 at approximately 5.3% CAGR, highlighting its increasing clinical acceptance.

2. Integration of Advanced Technologies (AI & Imaging)

Future glaucoma surgeries are increasingly incorporating real-time imaging, AI-based diagnostics, and digital monitoring systems, which improve surgical precision and early detection. These technologies enable more personalised treatment and reduce complication rates, transforming glaucoma management into a more data-driven approach.

3. Development of Next-Generation Implants and Combination Procedures

There is growing innovation in micro-stents, micro-shunts, and biocompatible implants, along with procedures combining glaucoma surgery with cataract treatment. These advancements improve long-term outcomes and reduce the need for repeat surgeries, making them highly attractive for both patients and surgeons

Recent Development

- In April 2026, Alcon Inc. launched the Hydrus Microstent in India, a minimally invasive glaucoma surgery (MIGS) device designed to reduce intraocular pressure and decrease dependence on medication in patients with open-angle glaucoma.

- In April 2025, Sight Sciences launched the OMNI Edge Surgical System, an advanced implant-free MIGS device designed to treat multiple points of resistance in the eye and improve intraocular pressure control.

- In March 2025, Glaukos Corporation partnered with RadiusXR and Topcon Healthcare Inc. to develop advanced visual field diagnostic solutions, enhancing early glaucoma detection and expanding access to digital eye care globally.

- In January 2025, Alcon Inc. collaborated with the Glaucoma Research Foundation to enhance patient awareness, education, and access to advanced glaucoma treatments through global initiatives and outreach programs.

Market Segment

This study forecasts revenue at global, regional, and country levels from 2020 to 2035. Decision Advisors has segmented the global glaucoma surgery devices market based on the below-mentioned segments:

Global Glaucoma Surgery Devices Market, By Product Type

- Glaucoma Drainage Devices

- Glaucoma Laser Devices

- Minimally Invasive Glaucoma Surgery (MIGS) Devices

Global Glaucoma Surgery Devices Market, By Application

- Trabeculectomy

- Glaucoma Drainage Implant Surgery

- Minimally Invasive Glaucoma Surgery (MIGS)

Global Glaucoma Surgery Devices Market, By End User

- Hospitals

- Ambulatory Surgical Centers

- Eye Specialty Clinics

Global Glaucoma Surgery Devices Market, By Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa

Frequently Asked Questions (FAQ)

1. How does patient adherence to post-surgical care impact the success of glaucoma surgery devices?

Post-surgical care, including medication compliance and follow-up visits, plays a critical role in maintaining intraocular pressure and ensuring long-term surgical success.

2. What are the differences in adoption rates of glaucoma surgery devices between urban and rural healthcare settings?

Adoption is significantly higher in urban areas due to better access to advanced ophthalmic infrastructure, while rural regions face limitations in awareness and specialist availability.

3. How do reimbursement policies influence the choice of glaucoma surgical procedures?

Favorable reimbursement policies encourage the use of advanced devices like MIGS, whereas limited coverage may lead to preference for traditional, lower-cost procedures.

4. What role do training and surgeon experience play in the effectiveness of MIGS devices?

Surgeon expertise is crucial, as MIGS procedures require precision and familiarity with new technologies, directly impacting surgical outcomes and adoption rates.

5. How is the integration of glaucoma surgery with cataract procedures affecting market growth?

Combined procedures are gaining popularity as they reduce overall surgical burden, improve patient convenience, and enhance cost-effectiveness, thereby boosting device demand.

Check Licence

Choose the plan that fits you best: Single User, Multi-User, or Enterprise solutions tailored for your needs.

We Have You Covered

- 24/7 Analyst Support

- Clients Across the Globe

- Tailored Insights

- Technology Tracking

- Competitive Intelligence

- Custom Research

- Syndicated Market Studies

- Market Overview

- Market Segmentation

- Growth Drivers

- Market Opportunities

- Regulatory Insights

- Innovation & Sustainability

Report Details

| Scope | Global |

| Pages | 240 |

| Delivery | PDF & Excel via Email |

| Language | English |

| Release | Apr 2026 |

| Access | Download from this page |