Global Hemophilia Market

Global Hemophilia Market Size, Share by Disease Type (Hemophilia A, Hemophilia B, Others), By Treatment Type (Replacement Therapy, Gene Therapy, Non-Factor Therapy, Others), By Therapy Type (Prophylactic Treatment, On-Demand Treatment), By End User (Hospitals, Specialty Clinics, Homecare Settings), and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East & Africa), Analysis and Forecast 2026-2035

CAGR

7.5%

REVENUE 2025

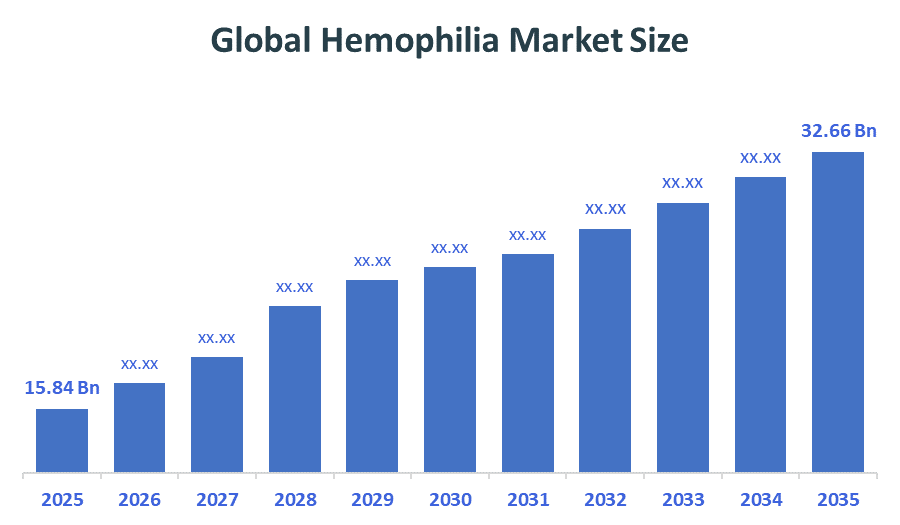

USD Billion 15.84

FORECAST 2035

USD Billion 32.66

REPORT COVERAGE

Global

The Hemophilia Market Size is foreseen to grow from USD 15.84 Billion in 2025 and is expected to reach around USD 32.66 Billion by 2035. According to Decision Advisors, a detailed research report on the Global Hemophilia Market is driven by the increasing prevalence of inherited bleeding disorders, rising adoption of recombinant clotting factor therapies, and rapid advancements in gene therapy technologies. Replacement therapy accounted for approximately 54% share in 2025 due to its widespread clinical use in long-term bleeding management and prophylactic treatment. In addition, Roche reported Hemlibra revenue exceeding USD 4.5 billion in 2024, strengthening its position in innovative hemophilia treatment solutions.

Market Snapshot

- Hemophilia Market Size (2025): USD 15.84 Billion

- Projected Hemophilia Market Size (2035): USD 32.66 Billion

- Hemophilia Market Compound Annual Growth Rate (CAGR): 7.5%

- Largest Regional Market: North America

- Fastest Growing Region: Asia Pacific

- 2nd Largest Region: Europe

- Base Year: 2025

- Historical Period: 2021-2024

- Forecast Period: 2026-2035

Market Overview/ Introduction

The Global Hemophilia Market is a rapidly growing segment in the rare diseases and hematology sector, focused on the diagnosis, treatment, and management of bleeding disorders caused by deficient clotting factors. Primarily driven by Hemophilia A (Factor VIII deficiency), which accounts for the majority of cases worldwide, the market is witnessing strong growth due to rising awareness, increasing adoption of prophylactic therapies, and significant technological advancements in gene therapy, extended half-life clotting factors, and non-factor replacement treatments. With improving healthcare infrastructure, establishment of specialized hemophilia treatment centers, and robust R&D investments, the market is expected to expand steadily as patients shift from on-demand to preventive care, ultimately reducing joint damage and enhancing quality of life.

Notable Insights: -

- North America is expected to maintain the largest share, accounting for around 42% of the global hemophilia market, backed by advanced healthcare infrastructure and favourable reimbursement policies.

- Asia Pacific is expected to grow at the fastest CAGR in the global Hemophilia market during the forecast period.

- By treatment type, the replacement therapy segment led the market in 2025 with nearly 54% share and is projected to grow at a substantial CAGR as patients shift toward preventive care.

- By disease type, the Hemophilia A segment dominated the market in 2025 with approximately 78% share, and is projected to grow at a substantial CAGR during the forecast period.

- The compound annual growth rate of the Hemophilia Market is 7.5%.

- The market is likely to achieve a valuation of USD 32.66 Billion by 2035.

What is the role of technology in grooming the market?

Hemophilia treatment is rapidly evolving through three transformative technology categories include extended half-life clotting factors that reduce infusion frequency from weekly to monthly dosing, gene therapy platforms utilizing AAV vectors offering multi-year disease modification, and non-factor therapies like emicizumab providing superior bleeding prevention. Digital health integration accelerates this transformation as AI-powered diagnostics improve screening accuracy by 94%, while wearable sensors and telehematology platforms enable real-time monitoring and predictive intervention. These connected care systems reduce bleeding episodes by 97% and treatment delays by 60% in underserved regions. The convergence of advanced therapeutics with intelligent monitoring reshapes hemophilia from an acute-care-intensive condition into a preventable, managed disease, collectively supporting better long-term patient outcomes and approximately 35% cost reductions across five-year treatment cycles globally.

Market Drivers

The global hemophilia market is growing due to the rising prevalence of inherited bleeding disorders and increasing adoption of prophylactic treatment approaches worldwide. Growing awareness regarding early diagnosis, preventive care, and long-term disease management is driving demand for recombinant clotting factor concentrates, non-factor replacement therapies, and advanced gene therapy solutions. In addition, increasing healthcare expenditure, favourable reimbursement policies, and expansion of specialized hemophilia treatment centres are supporting market development. Technological advancements in extended half-life therapies, personalized medicine, and digital patient monitoring platforms are improving treatment outcomes and patient adherence. Furthermore, ongoing clinical trials, rising investments in rare disease therapeutics, and regulatory approvals for innovative biologics are expected to create strong growth opportunities for the hemophilia market during the forecast period.

Restrain

The hemophilia market will confront certain obstacles owing to the costly nature of recombinant clotting factors therapy, gene therapies, and prophylactic treatment administration, especially in regions that cannot provide reimbursement for treatments in less-developed countries. Moreover, complications that can arise during the course of treatment, such as inhibitors against clotting factors, are known to undermine the effectiveness of the therapy administered. Additional restrictions in terms of the regulatory requirement and lack of availability of specialized hematology infrastructure may pose barriers to the market in the future.

Competitive Analysis:

The report offers the appropriate analysis of the key organizations/companies involved within the Hemophilia Market, along with a comparative evaluation primarily based on their product of offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes product development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

Top Companies in the Hemophilia Market

- Roche

- Pfizer Inc.

- Takeda Pharmaceutical Company

- Novo Nordisk

- CSL Behring

- Sanofi

- BioMarin Pharmaceutical Inc.

- Bayer AG

- Octapharma AG

- Grifols S.A.

Government Initiatives

|

Country |

Key Government Initiatives |

|

Japan |

Japan’s Ministry of Health, Labour and Welfare promotes rare disease management programs and investment in advanced hematology treatment infrastructure. |

|

US |

The Centres for Disease Control and Prevention (CDC) supports hemophilia surveillance programs and the expansion of specialized hemophilia treatment centres. |

|

Europe |

The European Medicines Agency (EMA) supports accelerated approvals for advanced biologics and gene therapies targeting rare bleeding disorders. |

Study on the Supply, Demand, Distribution, and Market Environment of the Hemophilia Market

The global hemophilia market demonstrates strong coordination between supply, demand, distribution channels, and healthcare infrastructure, though dynamics vary by region. On the supply side, leading biopharmaceutical firms including Roche, Pfizer, and Takeda continue advancing recombinant factors, gene therapies, and non-factor biologics. Demand remains robust due to increasing hemophilia prevalence, growing aging populations with acquired bleeding disorders, and rising adoption of prophylactic care. Distribution relies on hospital pharmacies, specialty hemophilia treatment centers, and homecare settings, which improve treatment access and adherence. Regulatory approvals, reimbursement policies, R&D investments, and advances in diagnostic and drug delivery systems collectively support steady market growth and wider therapy adoption.

Price Analysis and Consumer Behaviour Analysis

Price analysis in the hemophilia market confirms treatment costs remain significantly high due to premium pricing of recombinant clotting factor therapies, non-factor therapies, and gene therapy solutions. Long-term prophylactic and personalized biologic therapies command higher prices because they improve bleeding control, reduce hospitalization, and enhance quality of life. From a consumer behavior perspective, patients and providers prioritize therapies that minimize bleeding episodes and infusion frequency while simplifying disease management. Growing awareness of prophylactic treatment, home-based infusion, and innovative gene therapies is driving global adoption of advanced hemophilia solutions, reshaping pricing strategies and treatment accessibility across both developed and emerging markets.

Market Segmentation

The Hemophilia Market share is classified into product type, route of administration, animal type, application and end user.

- The replacement therapy segment dominated the market in 2025 with approximately 54% share, and is projected to grow at a substantial CAGR during the forecast period.

Based on the treatment type, the Hemophilia Market is divided into replacement therapy, gene therapy, non-factor therapy, and others. Among these, the replacement therapy segment dominated the market in 2025 with approximately 54% share, and is projected to grow at a substantial CAGR during the forecast period, owing to the widespread use of recombinant clotting factor concentrates for long-term bleeding management. For instance, factor VIII and factor IX replacement products are commonly prescribed for prophylactic treatment and prevention of severe bleeding episodes in hemophilia patients. The non-factor therapy segment also held a significant share due to increasing adoption of monoclonal antibody-based treatments.

- The Hemophilia A segment accounted for the largest share in 2025 with approximately 78%, and is anticipated to grow at a significant CAGR during the forecast period.

Based on the disease type, the Hemophilia Market is divided Hemophilia A, Hemophilia B, and others. Among these, the Hemophilia A segment accounted for the largest share in 2025 with approximately 78%, and is anticipated to grow at a significant CAGR during the forecast period, driven by y the high global prevalence of factor VIII deficiency and increasing adoption of advanced biologic therapies. For example, Hemophilia A patients frequently require long-term prophylactic treatment with recombinant factor VIII products and non-factor therapies to reduce bleeding complications and joint damage.

- The prophylactic treatment segment dominated the market in 2025 with approximately 61% share, and is projected to grow at a substantial CAGR during the forecast period.

Based on the therapy type, the Hemophilia Market is divided into prophylactic treatment and on-demand treatment. Among these, the prophylactic treatment segment dominated the market in 2025 with approximately 61% share, and is projected to grow at a substantial CAGR during the forecast period, owing to increasing clinical preference for preventive bleeding management and improved long-term patient outcomes. Prophylactic therapies significantly reduce spontaneous bleeding episodes, hospitalizations, and joint complications in patients with severe hemophilia disorders.

Strategies to Implement for Growth of the Market in Non-Leading Regions

- Increase awareness regarding inherited bleeding disorders through public healthcare campaigns, rare disease education programs, and early screening initiatives.

- Expand access to affordable recombinant clotting factor therapies, non-factor therapies, and prophylactic treatment solutions in developing economies.

- Strengthen partnerships with hospitals, hematology centers, and specialty clinics to improve accessibility and distribution of advanced hemophilia treatment products.

Regional Segment Analysis of the Hemophilia Market

- North America (U.S., Canada, Mexico)

- Europe (Germany, France, U.K., Italy, Spain, Rest of Europe)

- Asia-Pacific (China, Japan, India, Rest of APAC)

- South America (Brazil and the Rest of South America)

- The Middle East and Africa (UAE, South Africa, Rest of MEA)

North America is anticipated to hold the largest share, approximately 42% of the Hemophilia Market over the predicted timeframe.

North America is anticipated to hold the largest share, approximately 42% of the Hemophilia Market over the predicted timeframe. The region dominates due to advanced hematology healthcare infrastructure, strong adoption of recombinant clotting factor therapies, and increasing implementation of prophylactic treatment approaches in the United States and Canada. The increasing awareness regarding rare bleeding disorders, favorable reimbursement frameworks, and increasing adoption of gene therapy solutions are significantly driving regional market growth. Additionally, the presence of major biopharmaceutical companies and specialized hemophilia treatment centers further strengthens the market landscape.

Asia Pacific is expected to grow at the fastest CAGR in the Hemophilia Market during the forecast period.

Asia Pacific is expected to grow at the fastest CAGR in the Hemophilia Market during the forecast period. The growth is driven by increasing awareness regarding inherited bleeding disorders, expanding healthcare infrastructure, and improving access to advanced hematology care in countries such as China, Japan, India, and South Korea. Rising healthcare expenditure, growing adoption of prophylactic therapies, and government support for rare disease management programs are accelerating regional market development. Furthermore, increasing diagnosis rates and expansion of specialty hematology clinics are contributing to strong market growth across the region.

Europe is the second largest region in the Hemophilia Market during the forecast period.

Europe is the second largest region in the Hemophilia Market during the forecast period. The region is characterised by advanced healthcare systems, increasing adoption of recombinant biologics, and strong demand for innovative non-factor therapies, particularly in countries such as Germany, the UK, and France. High awareness regarding prophylactic treatment approaches and increasing implementation of personalized medicine are supporting market expansion. Furthermore, favorable reimbursement policies and technological advancements in gene therapy are contributing to the steady expansion of the market across Europe.

Future Market Trends in the Hemophilia Market: -

- Increasing Adoption of Gene Therapy Solutions

Gene therapy is gaining strong traction due to its potential to provide long-term bleeding control and reduce dependency on frequent factor replacement therapy.

- Rising Demand for Non-Factor Therapies

Non-factor therapies are expanding rapidly because they improve treatment convenience, reduce infusion frequency, and enhance patient adherence in hemophilia management.

- Expansion of Personalized Hemophilia Care

Personalized treatment approaches based on patient genetics and bleeding patterns are improving long-term disease management and therapeutic outcomes.

- Growing Integration of Digital Patient Monitoring Systems

Digital infusion tracking platforms and wearable monitoring technologies are improving treatment adherence, remote care management, and bleeding episode monitoring.

Recent Development

- In March 2026, the European Commission approved the first interchangeable biosimilar clotting factor for hemophilia A, potentially reducing treatment costs and improving patient access across member states.

- In January 2026, Octapharma expanded its manufacturing facility in Austria to increase global supply of recombinant clotting factor concentrates by 40%, addressing shortages in emerging Asia-Pacific markets.

- In November 2025, regulatory authorities in Japan and South Korea jointly approved a home-based gene therapy administration protocol, eliminating the need for hospital-based infusion facilities.

- In September 2025, Sanofi received breakthrough therapy designation from the FDA for its novel bispecific antibody mimicking factor VIII function, accelerating development for patients with inhibitor complications.

Market Segment

This study forecasts revenue at global, regional, and country levels from 2020 to 2035. Decision Advisors has segmented the Hemophilia Market based on the below-mentioned segments:

Hemophilia Market, By Disease Type

- Hemophilia A

- Hemophilia B

- Others

Hemophilia Market, By Treatment Type

- Replacement Therapy

- Gene Therapy

- Non-Factor Therapy

- Others

Hemophilia Market, By Therapy Type

- Prophylactic Treatment

- On-Demand Treatment

Hemophilia Market, By End User

- Hospitals

- Specialty Clinics

- Homecare Settings

Hemophilia Market, By Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa

Frequently Asked Questions (FAQ)

Q1. What is the projected market size of the Hemophilia Market by 2035?

A. The Hemophilia Market is projected to reach approximately USD 32.66 Billion by 2035.

Q2. What is the expected CAGR of the Hemophilia Market during the forecast period?

A. The market is expected to grow at a CAGR of 7.5% during the forecast period from 2026 to 2035.

Q3. Which treatment type dominated the Hemophilia Market in 2025?

A. The replacement therapy segment dominated the market in 2025 with approximately 54% share due to widespread adoption of recombinant clotting factor concentrates.

Q4. Which disease type accounted for the largest share in the Hemophilia Market?

A. The Hemophilia A segment accounted for approximately 78% market share in 2025 owing to the high prevalence of factor VIII deficiency globally.

Q5. Which therapy type dominated the Hemophilia Market?

A. The prophylactic treatment segment dominated the market with approximately 61% share in 2025 due to increasing preference for preventive bleeding management.

Q6. What factors are driving the growth of the Hemophilia Market?

A. Key growth drivers include rising prevalence of inherited bleeding disorders, increasing adoption of gene therapy and non-factor therapies, and growing awareness regarding preventive treatment approaches.

Q7. Which region dominates the Hemophilia Market?

A. North America dominates the market due to advanced hematology healthcare infrastructure, strong adoption of recombinant therapies, and favorable reimbursement policies.

Check Licence

Choose the plan that fits you best: Single User, Multi-User, or Enterprise solutions tailored for your needs.

We Have You Covered

- 24/7 Analyst Support

- Clients Across the Globe

- Tailored Insights

- Technology Tracking

- Competitive Intelligence

- Custom Research

- Syndicated Market Studies

- Market Overview

- Market Segmentation

- Growth Drivers

- Market Opportunities

- Regulatory Insights

- Innovation & Sustainability

Report Details

| Scope | Global |

| Pages | 200 |

| Delivery | PDF & Excel via Email |

| Language | English |

| Release | May 2026 |

| Access | Download from this page |