Global Immunoassay Interference Blocker Market

Global Immunoassay Interference Blocker Market Size, Share, and COVID-19 Impact Analysis, Impact of Tariff and Trade War Analysis, By Product Type (Heterophilic Blocking Reagents, Rheumatoid Factor (RF) Blockers, and Human Anti-Mouse Antibody (HAMA) Blockers), By End User (Diagnostic Laboratories, Hospitals & Clinics, and Academic & Research Institutes), and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2025-2035

REPORT COVERAGE

Global

Immunoassay Interference Blocker Market Summary, Size & Emerging Trends

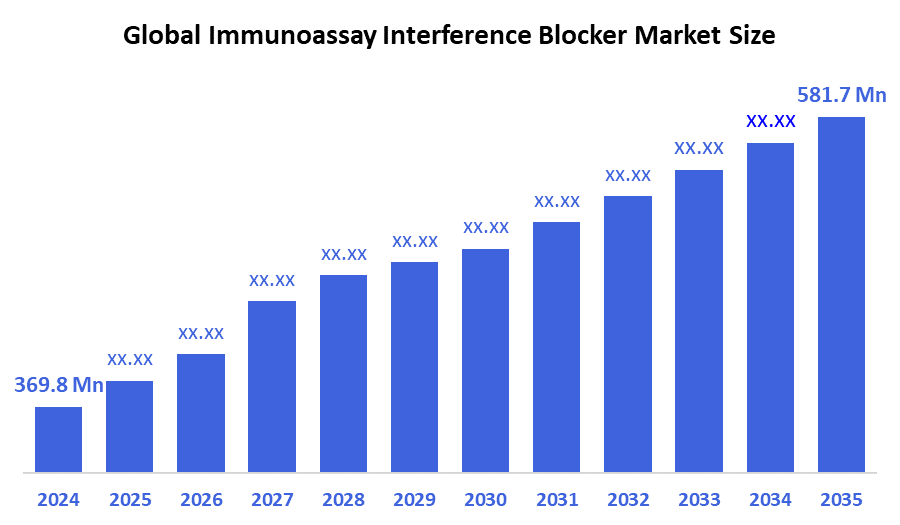

According to Decision Advisor, the Global Immunoassay Interference Blocker Market Size is expected to grow from USD 369.8 Million in 2024 to USD 581.7 Million by 2035, at a CAGR of 4.2% during the forecast period 2025-2035. Rising demand for high-precision diagnostic assays and the increasing prevalence of false positives due to assay interference are key drivers boosting the adoption of immunoassay interference blockers.

Key Market Insights

- North America is expected to dominate the market in 2024, due to advanced diagnostic infrastructure.

- Heterophilic blocking reagents lead the product segment due to their broad utility across immunoassays.

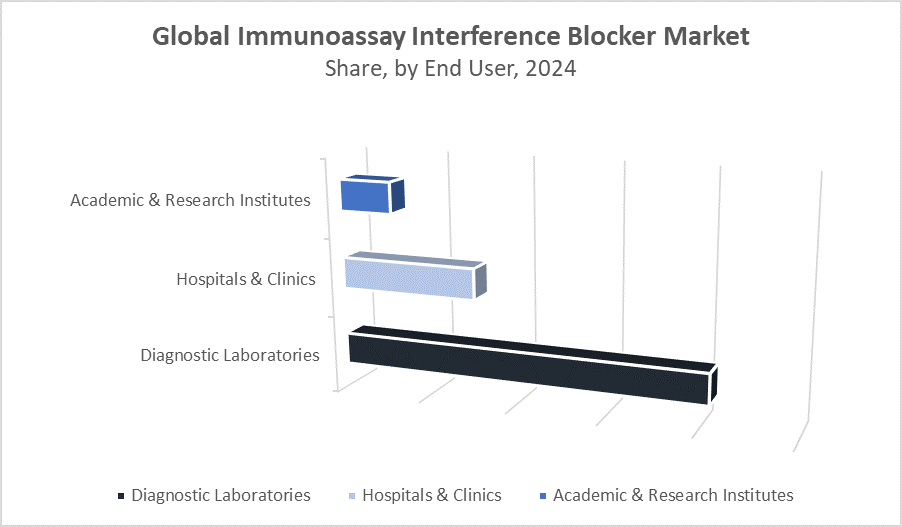

- Diagnostic laboratories hold the largest market share among end users.

Global Market Forecast and Revenue Outlook

- 2024 Market Size: USD 369.8 Million

- 2035 Projected Market Size: USD 581.7 Million

- CAGR (2025-2035): 4.2%

- North America: Largest market in 2024

- Asia Pacific: Fastest growing market

Immunoassay Interference Blocker Market

The immunoassay interference blocker market centers on reagents that neutralize interfering substances such as heterophilic antibodies, rheumatoid factors, and human anti-mouse antibodies (HAMA which can cause false results in diagnostic assays. These blockers are essential for improving the accuracy and reliability of immunoassay-based tests widely used in detecting infectious diseases, cancers, hormonal disorders, and chronic illnesses. With the growing shift toward automated, high-throughput, and highly sensitive diagnostic platforms, the demand for interference blockers is rising sharply. Increasing awareness among clinicians and lab professionals about the risks of assay interference is driving adoption. Additionally, stringent regulatory standards for diagnostic accuracy and a growing number of tests affected by cross-reactivity contribute to market growth. As healthcare systems emphasize reliable diagnostics to guide treatment decisions, interference blockers are becoming a critical component in the global clinical diagnostics landscape.

Immunoassay Interference Blocker Market Trends

- Increasing integration of blockers into diagnostic test kits by OEMs

- Rising R&D investment to develop universal interference blocking reagents

- Strategic partnerships between diagnostic manufacturers and reagent suppliers

Immunoassay Interference Blocker Market Dynamics

Driving Factors: Growing demand for accurate diagnostics and rising test volumes

The push for diagnostic accuracy is intensifying as healthcare systems worldwide emphasise early disease detection and precision treatment planning. Immunoassays are widely used in diagnosing conditions like cancer, infections, endocrine disorders, and autoimmune diseases. However, the reliability of these tests can be compromised by endogenous antibodies such as heterophilic antibodies or human anti-mouse antibodies (HAMA), which may bind non-specifically and cause false-positive or false-negative results. This issue is particularly critical in high-stakes environments like oncology or prenatal testing. As diagnostic testing becomes more automated and high-throughput, especially in centralised laboratories and reference centers, small inconsistencies can lead to large-scale diagnostic errors. Interference blockers are becoming an indispensable solution to uphold test integrity across large volumes, supporting better clinical decision-making, minimising misdiagnoses, and avoiding unnecessary treatments. The overall increase in global testing volume, accelerated by pandemic-driven investments, further fuels the demand.

Restrain Factors: High cost and complexity of customised interference solutions

Despite their clinical value, immunoassay interference blockers are not universally accessible. Advanced blockers are often expensive to develop and require fine-tuning to match specific assay platforms or reagents. In settings where diagnostic systems are not standardised, integrating blockers effectively becomes technically complex and cost-prohibitive. Furthermore, many developing countries face systemic barriers such as inadequate lab infrastructure, a lack of skilled personnel, and limited awareness of assay interference issues. These factors restrict the consistent use of interference blockers, even in situations where they could significantly improve diagnostic outcomes. Budget constraints in smaller labs or public hospitals can lead to the use of less effective reagents or even bypassing blockers altogether, risking diagnostic accuracy.

Opportunity: Expansion in personalised medicine and companion diagnostics

The rise of personalised medicine is redefining diagnostics, making accuracy and specificity more critical than ever. In targeted therapy areas such as oncology, rare diseases, and pharmacogenomics, diagnostic errors can have severe consequences. This is where interference blockers gain strategic relevance. With more companion diagnostics being approved alongside therapeutics, there is a growing need for ultra-precise immunoassays that are free from false readings caused by antibody interference. Manufacturers that can create blocker solutions optimised for these advanced diagnostics, particularly those used in monoclonal antibody therapies or gene-based treatments, can capitalise on this emerging demand.

Challenges: Lack of standardisation and regulatory variations

One of the most significant challenges facing this market is the lack of global standardization for interference blocker validation and performance assessment. Different diagnostic platforms and assay formats require different blocker chemistries and dosing, which complicates product development and scalability. In addition, regulatory agencies across regions (e.g., FDA in the U.S., EMA in Europe, CDSCO in India) have varying requirements for blocker validation, stability testing, and clinical utility demonstration. This fragmentation leads to delays in product approvals, increased R&D costs, and challenges in marketing products globally.

Global Immunoassay Interference Blocker Market Ecosystem Analysis

The global immunoassay interference blocker market ecosystem comprises raw material suppliers, reagent formulators, diagnostic device manufacturers, and end users such as hospitals and laboratories. Leading companies prioritise creating highly specific, stable blockers and collaborate with assay developers to ensure seamless compatibility. Regulatory agencies play a critical role by enforcing stringent quality standards, promoting innovation, and ensuring the accuracy and reliability of diagnostic tests across various healthcare settings worldwide.

Global Immunoassay Interference Blocker Market, By Product Type

The heterophilic blocking reagents segment dominated the global immunoassay interference blocker market, accounting for approximately 48% of total revenue. These reagents are highly valued for their broad-spectrum ability to block heterophilic antibody interference, which commonly causes false positives in various diagnostic assays. Their versatility makes them essential across multiple diagnostic platforms, enhancing test accuracy and reliability.

The rheumatoid factor (RF) blockers segment holds about 28% of the market share. These blockers specifically target interference caused by rheumatoid factors, especially in patients with autoimmune diseases. RF blockers are critical in minimizing false-positive results in immunoassays used to detect thyroid conditions, viral infections, and tumor markers, thus ensuring more precise diagnostic outcomes.

Global Immunoassay Interference Blocker Market, By End User

Diagnostic laboratories represent the largest segment, accounting for around 50% of the immunoassay interference blocker market revenue. These labs process vast numbers of patient samples daily, performing various immunoassays that are susceptible to interference from antibodies like heterophilic antibodies and rheumatoid factors. The high testing volume and critical need for precise, reproducible results make interference blockers indispensable in these settings. Laboratories increasingly adopt advanced blockers to minimize false positives and negatives, ensuring diagnostic accuracy that directly influences patient treatment decisions and outcomes.

Hospitals and clinics hold approximately 32% of the market share. These facilities perform a range of diagnostic tests in-house, including immunoassays critical for rapid diagnosis and patient monitoring. Interference blockers are essential here to maintain test integrity, especially in urgent care environments like emergency rooms and intensive care units, where timely and accurate results can be life-saving. Additionally, hospitals benefit from blockers by reducing misdiagnoses linked to assay interference, which supports better clinical decision-making. Increasing investments in point-of-care testing and hospital-based diagnostic services further contribute to the growth of this segment.

North America holds a commanding lead with approximately 42% of the global market share as of 2024

fueled by several factors: the presence of key global diagnostic and pharmaceutical companies that develop and manufacture cutting-edge interference blockers; robust healthcare infrastructure with widespread access to advanced diagnostic laboratories; and stringent regulatory oversight from agencies like the FDA and Health Canada. These regulations ensure high standards for diagnostic accuracy, pushing laboratories and hospitals to adopt reliable interference blockers to minimize false results. Additionally, a large patient population with rising incidences of cancer, autoimmune diseases, and infectious diseases drives the need for precise immunoassays. Continuous investment in R&D and technological innovations further strengthen North America’s market position.

Europe accounts for roughly 26% of the immunoassay interference blocker market.

Countries like Germany, France, and the UK lead adoption due to their advanced healthcare systems and strong emphasis on early disease detection, which requires highly reliable diagnostic testing. The region is characterized by extensive public and private healthcare spending, supportive government initiatives promoting diagnostic accuracy, and a well-established network of diagnostic laboratories. Moreover, the aging population and increasing prevalence of chronic diseases such as cancer and autoimmune disorders heighten demand for immunoassays and corresponding interference blockers. European regulatory agencies also enforce strict quality controls, ensuring that only validated interference blockers are used, thus maintaining market growth.

Asia Pacific is the fastest-growing region, with a forecasted CAGR of 9.1%.

Rapid economic development, expanding healthcare infrastructure, and increasing healthcare expenditure in countries such as China, India, Japan, and Southeast Asian nations are the primary growth drivers. The rise in public and private diagnostic laboratories, coupled with growing awareness about the importance of diagnostic accuracy among clinicians and patients, propels demand for immunoassay interference blockers. In emerging economies, government initiatives aimed at improving healthcare access and quality are creating a favorable environment for diagnostic advancements. Additionally, the high burden of infectious diseases and chronic conditions in this region accelerates the need for precise immunoassay testing. Despite challenges like infrastructure gaps and regulatory variability, the region’s expanding healthcare landscape presents vast opportunities for market players.

WORLDWIDE TOP KEY PLAYERS IN THE IMMUNOASSAY INTERFERENCE BLOCKER MARKET INCLUDE

- Thermo Fisher Scientific

- Bio-Rad Laboratories

- Siemens Healthineers

- Abbott Laboratories

- PerkinElmer, Inc.

- F. Hoffmann-La Roche AG

- Bio-Techne Corporation

- Quidel Corporation

- Randox Laboratories

- DiaSorin S.p.A.

- Others

Product Launches in Immunoassay Interference Blocker Market

- In February 2024, Thermo Fisher Scientific launched a new line of multi-target blocking reagents specifically designed for next-generation immunoassays. These reagents improve compatibility across various diagnostic platforms and sample types, helping to reduce interference from multiple sources simultaneously. This innovation supports more accurate and reliable immunoassay results, especially important as diagnostic testing becomes increasingly complex and automated.

- In July 2023, Bio-Rad Laboratories expanded its portfolio of Human Anti-Mouse Antibody (HAMA) blockers by introducing a reagent that targets interference from new monoclonal antibody therapies. This advancement enhances diagnostic precision for oncology patients, where monoclonal antibody treatments can cause assay interference, potentially leading to false results. Bio-Rad’s updated HAMA blockers help ensure that cancer diagnostics are more accurate and dependable.

Market Segment

This study forecasts revenue at global, regional, and country levels from 2020 to 2035. Decision Advisor has segmented the immunoassay interference blocker market based on the below-mentioned segments:

Global Immunoassay Interference Blocker Market, By Product Type

- Heterophilic Blocking Reagents

- Rheumatoid Factor (RF) Blockers

- Human Anti-Mouse Antibody (HAMA) Blockers

Global Immunoassay Interference Blocker Market, By End User

- Diagnostic Laboratories

- Hospitals & Clinics

- Academic & Research Institutes

Global Immunoassay Interference Blocker Market, By Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa

FAQs

Q: What is the market size of the Global Immunoassay Interference Blocker Market in 2025?

A: The Global Immunoassay Interference Blocker Market size is projected to be approximately USD 384.3 million in 2025.

Q: What is the forecasted CAGR of the Global Immunoassay Interference Blocker Market from 2025 to 2035?

A: The market is expected to grow at a CAGR of 4.2% during the period 2025–2035.

Q: What is the revenue potential of immunoassay interference blockers in Asia Pacific by 2035?

A: Asia Pacific is projected to generate over USD 170 million in revenue by 2035, driven by expanding diagnostics infrastructure and high disease burden.

Q: Who are the top 10 companies operating in the Global Immunoassay Interference Blocker Market?

A: Key players include Thermo Fisher Scientific, Bio-Rad Laboratories, Siemens Healthineers, Abbott Laboratories, PerkinElmer Inc., F. Hoffmann-La Roche AG, Bio-Techne Corporation, Quidel Corporation, Randox Laboratories, and DiaSorin S.p.A.

Q: Which startups or innovations are disrupting the immunoassay interference blocker market?

A: Innovations from major players like Thermo Fisher’s multi-target blocking reagents and Bio-Rad’s enhanced HAMA blockers for oncology diagnostics are setting new industry standards.

Q: Can you provide company profiles for leading immunoassay blocker manufacturers?

A: Yes. For example, Thermo Fisher Scientific introduced advanced blockers compatible with next-gen immunoassays in 2024, while Bio-Rad Laboratories expanded its HAMA blocker product line to reduce diagnostic errors in cancer testing.

Q: What are the main drivers of growth in the immunoassay interference blocker market?

A: Increasing diagnostic volumes, demand for test accuracy, rising incidence of chronic and infectious diseases, and automation in laboratories are key growth drivers.

Q: What challenges are limiting the adoption of immunoassay interference blockers?

A: High costs, lack of standardization, limited awareness in developing markets, and integration complexities with non-standardized assay platforms are major restraints.

Check Licence

Choose the plan that fits you best: Single User, Multi-User, or Enterprise solutions tailored for your needs.

We Have You Covered

- 24/7 Analyst Support

- Clients Across the Globe

- Tailored Insights

- Technology Tracking

- Competitive Intelligence

- Custom Research

- Syndicated Market Studies

- Market Overview

- Market Segmentation

- Growth Drivers

- Market Opportunities

- Regulatory Insights

- Innovation & Sustainability

Report Details

| Scope | Global |

| Pages | 220 |

| Delivery | PDF & Excel via Email |

| Language | English |

| Release | Oct 2025 |

| Access | Download from this page |