Global In-Chassis Cooling Market

Global In-Chassis Cooling Market Size, Share, By Cooling Type (Air-Based In-Chassis Cooling, Liquid-Based In-Chassis Cooling, and Phase Change Cooling) By Chassis Type (Server Racks, Desktop PCs, Industrial Enclosures, and Networking Equipment) By End User (IT and Telecom, Manufacturing, Automotive, Healthcare, and Consumer Electronics) and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa), Analysis and Forecast 2026 - 2035

CAGR

8.92%

REVENUE 2025

USD Billion 3.15

FORECAST 2035

USD Billion 7.4

REPORT COVERAGE

Global

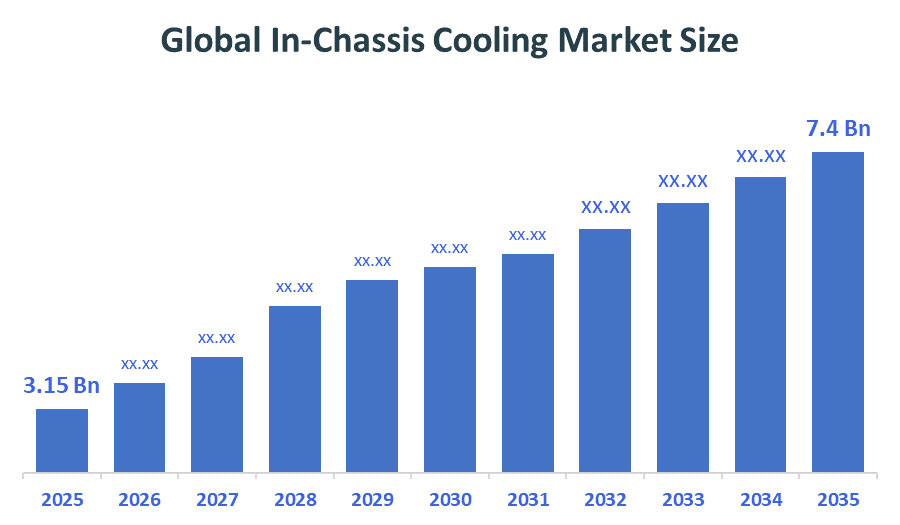

The Global In-Chassis Cooling Market Size was predicted to grow from USD 3.15 Billion in 2025 and is projected to reach around USD 7.4 Billion by 2035. According to Decision Advisors, a detailed research report on the in-chassis cooling market shows that the liquid-based in-chassis cooling technology trend dominates the global market, holding approximately 50-60% of the total share worldwide. Vertiv Holdings Co. leads the market with an annual revenue of approximately USD 10.23 billion in 2025, making it one of the primary market drivers for shaping the industry landscape.

Market Snapshot

- Global In-Chassis Cooling Market Size (2025): USD 3.15 Billion

- Global In-Chassis Cooling Projected Market Size (2035): USD 7.4 Billion

- Global In-Chassis Cooling Compound Annual Growth Rate (CAGR): 8.92%

- Largest Regional Market: Asia-Pacific

- Fastest Growing Region: North America

- 3rd Largest Region: Europe

- Base Year: 2025

- Historical Period: 2021 to 2024

- Forecast Period: 2026 to 2035

Market Overview / Introduction

In-chassis cooling refers to specialised thermal management systems integrated directly within an equipment enclosure to maintain optimal internal temperatures. These systems serve as a critical localised defence against component overheating, sitting between traditional external ventilation and complex immersion systems. By utilising advanced heat pipes, high-static pressure fans, and internal liquid loops, in-chassis cooling ensures that heat generated by CPUs, GPUs, and power supplies is extracted immediately before it can affect surrounding hardware.

Modern in-chassis cooling designs have evolved from simple internal fans to intelligent, modular thermal units equipped with variable speed controllers and vibration-dampening technology. These systems are vital for maintaining the structural integrity and operational longevity of hardware in compact environments. As industries move toward edge computing and high-density AI processing, the ability to manage heat within the chassis itself has become a fundamental requirement for energy efficiency and system reliability.

- The IT and Data Center segments contribute to approximately 68% of the application-based use in the market, driven by the shift toward high-density blade servers and the need for precision internal airflow management.

- In-chassis thermal protection in the industrial sector is experiencing substantial growth, with a CAGR forecasted to surpass 10% due to the rising deployment of automated control systems in harsh manufacturing environments where external dust and heat pose risks to sensitive electronics.

Notable Insights: -

- Liquid-based in-chassis modules make up about 48.5% of the total market share. These solutions are gaining massive traction in the gaming and workstation sectors, where compact form factors require high thermal conductivity that air cooling cannot provide.

- Applications of in-chassis cooling in the telecommunications sector account for almost 39.5% of demand, particularly within 5G base station enclosures that require robust thermal management in outdoor environments.

- About 45.2% of the market value belongs to the Asia-Pacific region in 2026. Rapid industrialisation and the expansion of digital infrastructure in China and India are the primary catalysts for this regional dominance.

What is the Role of Technology in Shaping the Market?

Technological progress is driving a paradigm shift in how heat is managed within closed environments. The integration of micro-channel cold plates and advanced vapor chamber technology has allowed for much higher heat flux density management within the same physical footprint. Furthermore, the rise of smart thermal sensors allows in-chassis systems to communicate with the motherboard, adjusting cooling intensity in real-time based on specific component workloads rather than general internal air temperature.

How are Recent Developments Helping the Market?

Recent innovations include the development of leak-proof quick-disconnect couplings for internal liquid loops and the use of graphene-enhanced thermal interface materials. These advancements have greatly boosted market confidence in deploying liquid cooling inside the chassis. Additionally, the move toward "Tool-less" modular cooling units allows data centre technicians to replace or upgrade internal fans and heat sinks without shutting down entire systems, significantly reducing maintenance downtime and improving the overall ROI for enterprises.

Market Drivers

Market demand for global in-chassis cooling systems is rising due to the surge in high-performance computing (HPC) and the widespread adoption of AI-capable hardware. These components generate unprecedented levels of heat that standard room air conditioning cannot effectively mitigate. Additionally, the drive for "Green Data Centres" is pushing operators toward in-chassis liquid cooling, as it is significantly more energy-efficient to move heat via fluid loops than by moving massive volumes of air.

Restraints

The growth of the international in-chassis cooling industry is primarily constrained by the high initial cost of specialised internal components and the complexity of integrating liquid loops within existing legacy chassis designs. Concerns regarding potential liquid leaks near sensitive circuits also remain a psychological barrier for some conservative industrial sectors.

Competitive Analysis

The report offers the appropriate analysis of the key organisations/companies involved within the global in-chassis cooling market, along with a comparative evaluation primarily based on their product offerings, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborate analysis focusing on the current news and developments of the companies, which includes product development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

Top 10 Companies in the Global In-Chassis Cooling Market

- Vertiv Holdings Co.

- Schneider Electric SE

- Rittal GmbH & Co. KG

- Cooler Master Technology Inc.

- Delta Electronics, Inc.

- Corsair Components, Inc.

- Asetek, Inc.

- Boyd Corporation

- Noctua (Rascom Computerdistribution Ges.m.b.H.)

- Thermaltake Technology Co., Ltd.

Government Initiatives

|

Country |

Key Government Initiatives |

|

US |

Under the Advanced Research Projects Agency-Energy (ARPA-E), the COOLERCHIPS program continues to provide funding for in-chassis cooling innovations that aim to lower PUE (Power Usage Effectiveness) in high-density computing environments. |

|

EU |

The Ecodesign for Sustainable Products Regulation (ESPR) has introduced new standards for server energy efficiency, indirectly mandating the use of more effective internal cooling to reduce overall power draw. |

|

China |

The Guiding Opinions on Accelerating the Construction of Green Data Centres encourages the adoption of liquid-cooled racks and in-chassis thermal management to meet national carbon intensity targets. |

Study on the Supply, Demand, Distribution, and Market Environment

The success of the in-chassis cooling industry depends on the supply chain of high-quality copper and aluminum for heat sinks, as well as the availability of specialized non-conductive coolants. The market environment is currently shifting from a "component-first" approach to a "system-first" approach, where vendors provide end-to-end thermal solutions tailored to specific chassis dimensions and heat profiles.

Price Analysis and Consumer Behaviour Analysis

Pricing for in-chassis cooling varies significantly. Basic air-cooled fan units remain affordable for general consumer use, while high-end internal liquid cooling loops with AI-driven pumps are positioned at a premium. Consumer behaviour shows a clear trend: enterprise buyers are increasingly willing to pay a higher upfront cost for "Self-Contained" cooling units that guarantee 99.99% uptime and lower long-term energy bills.

Market Segmentation

The Global In-Chassis Cooling Market share is classified into cooling type, chassis type, application, and end user.

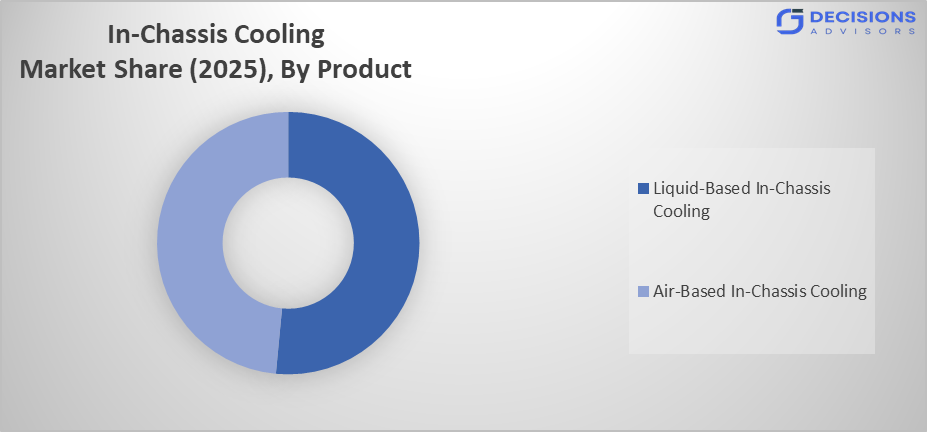

The Liquid-Based In-Chassis Cooling segment holds the largest share, contributing approximately 48-55% of the market in 2025.

Based on the Cooling Type, the global in-chassis cooling market is divided into Air-Based In-Chassis Cooling and Liquid-Based In-Chassis Cooling. Among these, the Liquid-Based In-Chassis Cooling segment holds the largest share, contributing approximately 48-55% of the market in 2025. The reason for this dominance lies in its superior thermal conductivity and efficiency in managing high-wattage components within confined spaces. This technology minimises energy loss in high-performance computing without requiring the massive airflow and physical footprint associated with traditional air-cooled alternatives.

The Server Rack In-Chassis Cooling segment accounts for the largest share, representing over 62% of the global market in 2025.

Based on the Chassis Type, the global in-chassis cooling market is divided into Server Rack In-Chassis Cooling, Desktop PC In-Chassis Cooling, and Industrial Enclosure Cooling. Among these, the Server Rack In-Chassis Cooling segment accounts for the largest share, representing over 62% of the global market in 2025. These systems are critical for maintaining hardware health in enterprise data centers, providing high-reliability cooling that can be automated through standard rack management software. On the other hand, the Industrial Enclosure Cooling segment has emerged as a rapidly growing sector, thanks to the increasing adoption of edge computing nodes in harsh manufacturing environments.

Data Centers dominate the global market, accounting for approximately 52% of the total revenue in 2025.

Based on the Application, the global in-chassis cooling market is divided into Data Centers, Industrial Automation, Automotive Electronics, Consumer Gadgets, and Telecommunications. Among these, Data Centers dominate the global market, accounting for approximately 52% of the total revenue in 2025. This segment is preferred by operators who require high-density thermal management for AI and cloud infrastructure. The Automotive Electronics category is seeing a steady increase in use, especially in the cooling of autonomous driving modules, where localized, high-precision cooling is required to maintain system safety.

The IT and Telecom segment dominates the global market, accounting for approximately 45% of the total revenue in 2025.

Based on the End User, the global in-chassis cooling market is divided into IT and Telecom, Manufacturing, Automotive, Aerospace & Defense, and Healthcare. Among these, the IT and Telecom segment dominates the global market, accounting for approximately 45% of the total revenue in 2025. This segment is preferred by architects who require integrated cooling units that fit within standard telecom enclosures and 5G base stations. The Manufacturing segment is seeing a sharp increase in use, especially by companies implementing Industry 4.0 standards that value the dust-proof and moisture-resistant nature of advanced in-chassis liquid loops.

Strategies to Implement for Growth of the Market in Non-Leading Regions

The possibilities of growth for the in-chassis cooling industry in the emerging regions can be enhanced through the creation of localized assembly facilities for modular cooling units, specifically designed for use by local hardware integrators and telecommunications providers. Government initiatives focused on digital transformation and localized data sovereignty play a major role in creating demand in regions that face high shipping costs for pre-integrated cooling hardware. The additional assistance of investment in the training of local thermal management engineers, together with regional testing labs for hardware stress-testing, will help achieve this.

Regional Segment Analysis of the Global In-Chassis Cooling Market

- North America (U.S., Canada, Mexico)

- Europe (Germany, France, U.K., Italy, Spain, Rest of Europe)

- Asia-Pacific (China, Japan, India, South Korea, Rest of APAC)

- Latin America (Brazil and the Rest of Latin America)

- The Middle East and Africa (UAE, South Africa, Rest of MEA)

Asia-Pacific is projected to be the largest region over the forecast period. This region is anticipated to witness a growth rate of around 15.09% CAGR, maintaining a dominant market share within the global industry. In 2025, the Asia-Pacific region will already accounts for approximately 35.2% of global revenue. This is owing to the fast-developing consumer electronics manufacturing hubs, coupled with the growing demand for local server farms in countries such as China, India, and Vietnam. Other reasons for the same include greater investments toward smart city projects, state-supported indigenous R&D for semiconductor cooling, and widespread adoption of high-efficiency green data center standards.

North America is expected to hold a significant share of the in-chassis cooling market during the forecast period. This region holds approximately 26.8% share of global revenue in 2025, thanks to its highly sophisticated tech sector, along with the extensive adoption of liquid-to-chip technology in both national research labs and high-value industrial applications. The largest part of this region’s revenues comes from the United States, as there is a lot of spending at the corporate level in upgrading legacy data centers, along with local research related to advanced phase-change cooling materials.

Europe is anticipated to hold a substantial share, contributing approximately 22.4% of the global market share. There is a competitive advantage in the region owing to clusters of automotive and industrial engineering innovation and financing for sustainable infrastructure, as well as thermal efficiency research. There is also a comparative advantage with countries like Germany and the UK, which are highly skilled at precision engineering for high-performance enclosures. Moreover, the rigorous environmental standards regarding carbon footprints and power usage effectiveness further give them a competitive advantage.

Recent Developments

- In June 2025, the European Union announced plans to tighten energy performance standards for data centers, significantly driving the demand for in-chassis cooling modules that reduce total facility power draw. [AS5]

- In March 2024, leading manufacturers introduced new "leak-proof" quick-disconnect couplings specifically designed for in-chassis liquid loops, addressing a major safety concern for enterprise hardware.

- In November 2022, the European Union updated its energy consumption reduction targets, pushing industries to adopt advanced thermal management systems to meet stricter efficiency requirements.

- In July 2021, global investments in sustainable industrial systems accelerated, with in-chassis cooling technologies playing a key role in reducing localized hardware failure rates by 25%. [AS7]

Market Segmentation

This study forecasts revenue at global, regional, and country levels from 2021 to 2035. The Global In-Chassis Cooling Market is segmented based on the following categories:

Global In-Chassis Cooling Market, By Cooling Type

- Air-Based In-Chassis Cooling

- Liquid-Based In-Chassis Cooling

Global In-Chassis Cooling Market, By Chassis Type

- Server Rack In-Chassis Cooling

- Desktop PC In-Chassis Cooling

- Industrial Enclosure Cooling

Global In-Chassis Cooling Market, By Application

- Data Centers

- Industrial Automation

- Automotive Electronics

- Consumer Gadgets

- Telecommunications

Global In-Chassis Cooling Market, By End User

- IT and Telecom

- Manufacturing

- Automotive

- Aerospace & Defense

- Healthcare

Global In-Chassis Cooling Market, By Regional Analysis

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- United Arab Emirates

- Saudi Arabia

- Qatar

- South Africa

- Rest of Middle East & Africa

Frequently Asked Questions (FAQ)

What is the significance of leak-detection sensors in modern in-chassis cooling?

As liquid cooling moves directly into the equipment chassis, the risk of moisture damaging sensitive circuits increases. Modern systems incorporate smart leak-detection sensors linked to the system's emergency shut-off. This technique is necessary for protecting high-value components in data centers and industrial control units, ensuring that any breach in the coolant loop is identified before hardware damage occurs.

How does the transition to high-density AI chips affect in-chassis cooling specifications?

The shift toward processors with TDP (Thermal Design Power) exceeding 400W creates intense heat loads that traditional air-cooled fans cannot handle. This shift requires the use of in-chassis liquid loops with micro-channel cold plates that sit directly on the chip. Car and server manufacturers are adopting these precision cooling solutions to prevent thermal throttling and maintain maximum processing speeds.

What role do synthetic dielectric fluids play in in-chassis cooling manufacturing?

Synthetic dielectric fluids are engineered to be non-conductive, meaning they do not cause short circuits even if a leak occurs within the chassis. In high-frequency operations, these fluids offer superior heat transfer while providing a safety net for the surrounding electronics. This makes them ideal for in-chassis loops in mission-critical aerospace and defense equipment.

What are the primary differences in the application of air-based versus liquid-based in-chassis cooling in 2026?

While air-based cooling remains the standard for general-purpose desktop PCs and low-power industrial panels due to its simplicity, liquid-based in-chassis cooling is seeing a massive surge in high-performance computing and electric vehicle power electronics. Liquid's ability to move heat 25 times faster than air makes it the preferred choice for space-constrained, high-performance hardware where a compact thermal footprint is mandatory.

Check Licence

Choose the plan that fits you best: Single User, Multi-User, or Enterprise solutions tailored for your needs.

We Have You Covered

- 24/7 Analyst Support

- Clients Across the Globe

- Tailored Insights

- Technology Tracking

- Competitive Intelligence

- Custom Research

- Syndicated Market Studies

- Market Overview

- Market Segmentation

- Growth Drivers

- Market Opportunities

- Regulatory Insights

- Innovation & Sustainability

Report Details

| Scope | Global |

| Pages | 210 |

| Delivery | PDF & Excel via Email |

| Language | English |

| Release | Apr 2026 |

| Access | Download from this page |