Global Inductor Market

Global Inductor Market Size, Share, By Inductor Type (Power, RF/High-Frequency, Coupled, and More), Core Material (Air/Ceramic, Ferrite, and More), End-User Vertical (Automotive, Aerospace and Defense, and More), and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2026-2035

REPORT COVERAGE

Global

Market Snapshot

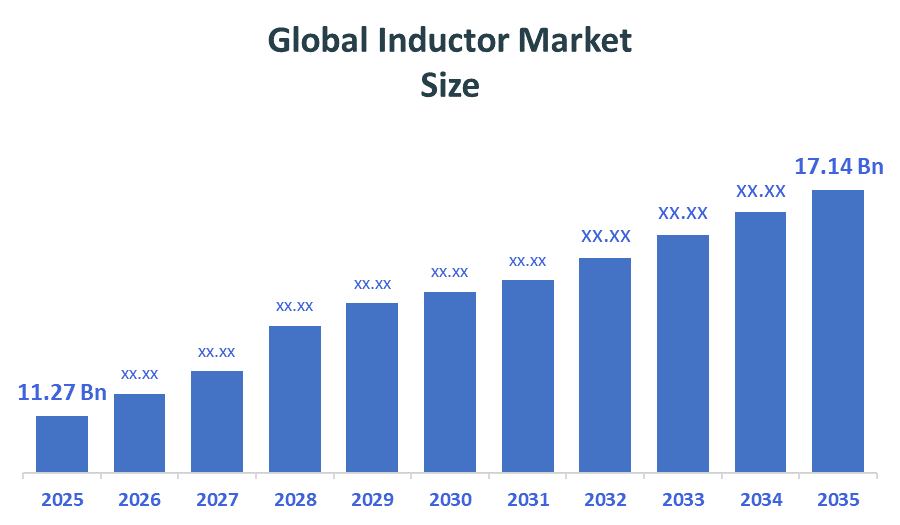

- Market Size (2025): USD 11.27Billion

- Projected Market Size (2035): USD 17.14 Billion

- Compound Annual Growth Rate (CAGR): 4.28%

- Largest Regional Market: North America

- Fastest Growing Region: Asia-Pacific

- 3rd Largest Region: Europe

- Base Year: 2025

- Historical Period: 2021–2024

- Forecast Period: 2025-2035

According to Decision Advisors, the Global inductor market Size is expected to grow from USD 11.27 Billion in 2025 to USD 17.14 Billion by 2035, at a CAGR of 4.28% during the forecast period 2025-2035. The global inductor market is driven by rising demand for consumer electronics, rapid 5G deployment, increasing electric vehicle adoption, growth in renewable energy systems, expansion of IoT devices, and advancements in power management technologies, enhancing efficiency, miniaturization, and performance across multiple industrial applications worldwide.

Market Overview/ Introduction

The global inductors market refers to the industry of passive electronic components that store energy in a magnetic field and regulate current in circuits across electronics, automotive, and telecom sectors. The market expands because consumer electronics, which represent more than 30% to 35% of total market demand, continue to grow and electric vehicles and 5G infrastructure become more widely used. The industry experiences operational improvements because companies develop advanced technologies that enable miniaturization and create high-frequency inductors and thin-film technology, which results in a 4.5% to 5% annual growth for thin-film inductors. The latest research shows that R&D funding increased 24% to create small inductors that use less energy. The automotive industry shows strong growth with more than 7% annual compound growth rate while EVs and renewable energy systems and IoT devices create more business opportunities.

- In March 2026, China’s Five-Year Plans prioritize industrial upgrading by supporting high-tech manufacturing, including electronic components, through R&D investment, policy incentives, and supply chain localization, aiming to reduce import dependence and strengthen domestic production capabilities and global competitiveness

- In March 2025, global EV incentives across Europe and North America, including subsidies and tax benefits, accelerate EV adoption, increasing demand for automotive-grade power inductors used in efficient power management and electronic systems

- In January 2025, governments across APAC and the Middle East, including China, UAE, and Saudi Arabia, are investing in 5G and industrial modernization, increasing demand for high-frequency and common-mode inductors in advanced electronic infrastructure.

Notable Insights: -

- North America holds the largest regional market share approximately 33% in the global inductor market

- Asia Pacific is the fastest growing region in the global inductor market with a CAGR of approximately 8%.

- By inductor, the power segment held a dominant position with approximately 8% in terms of market share in 2025.

- By core material, ferrite segment is the dominating accounting for over 7% of the global market share in 2025.

- The compound annual growth rate of the global inductor market is 4.28%.

- The market is likely to achieve a valuation of USD 17.14billion by 2035.

What is role of technology in grooming the market?

The global inductors market relies on technology which drives performance improvements, efficiency enhancements and expands application possibilities. Permanent miniaturization research has achieved continuous progress which enables inductors to become smaller while maintaining their capacity to deliver high power output for modern devices such as smartphones and wearables which represent more than 30% of market demand. Modern materials including nanocrystalline and ferrite core components enable 15% to 20% power loss reduction while they enhance energy efficiency. Market demand for high-frequency thin-film inductors will grow at a rate between 4.5% and 5% CAGR because these devices enable the development of 5G and IoT networks. The combination of automated manufacturing combined with precision design tools results in production efficiency improvements that exceed 20% while enabling manufacturers to create high-quality components at large scale. The combination of technological progress with market expansion and application development enables businesses to grow in their respective markets.

Market Drivers

The global inductors market is driven by the rapid expansion of consumer electronics and automotive electrification and advanced communication technologies. The demand for consumer electronics products accounts for more than 30%–35% of total market requirements because smartphones and laptops and wearable devices need power management components that operate with high efficiency. The increasing use of electric vehicles drives the market because inductors serve as essential components inside battery management systems and power converters which automotive applications require. The deployment of 5G networks creates an increased need for high-frequency inductors because telecom markets experience substantial growth across all regions. The demand for renewable energy systems such as solar inverters and wind power electronics continues to rise, which results in increased market demand. The market experiences worldwide growth because urbanization and rising disposable income and the increasing use of IoT devices drive expansion.

Restrain

Even though there is strong worldwide demand for the global inductors market, multiple restrictions will impede its development. The industry faces its biggest obstacle through its unstable raw material costs that especially affect copper and ferrite core prices, which lead to production cost increases that decrease manufacturer profit margins. The design process of modern electronic devices becomes more difficult because engineers need to find ways to create small inductors that can sustain their original performance standards. The most important limitation of the market exists because Asian manufacturers engage in fierce price competition, which directly affects their ability to maintain profit margins. The production process experiences disruptions because of supply chain interruptions and the company's need to obtain components from particular geographic areas.

Competitive Analysis:

The report offers the appropriate analysis of the key organizations/companies involved within the Global inductor market, along with a comparative evaluation primarily based on their product of offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes product development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

Top Companies in the Global inductor market

- TDK Corporation

- Murata Manufacturing Co., Ltd.

- Vishay Intertechnology, Inc.

- Taiyo Yuden Co., Ltd.

- Panasonic Corporation

- Coilcraft, Inc.

- Delta Electronics, Inc.

- Chilisin Electronics Corp.

- Pulse Electronics Corporation

- Shenzhen Sunlord Electronics Co., Ltd.

- Sumida Corporation

- Würth Elektronik Group

- Bourns, Inc.

Government Initiatives

|

Country |

Key Government Initiatives |

|

Europe |

In September 2023, European Union, the European Chips Act allocates €43 billion to strengthen semiconductor capacity, indirectly boosting demand for inductors through expanded electronics manufacturing, supply chain integration, and advanced technology ecosystem development. |

|

US |

In August 2022, United States, the CHIPS and Science Act allocate $52+ billion to boost semiconductor manufacturing, indirectly increasing demand for inductors through supply chain expansion, domestic production incentives, and electronics ecosystem growth. |

|

India

|

In March 2025, India, Production Linked Incentive (PLI) schemes boosted electronics output from ?2.13 lakh crore to ?5.45 lakh crore, indirectly increasing demand for inductors through ecosystem expansion and domestic component manufacturing growth. |

Study on the Supply, Demand, Distribution, and Market Environment Global inductor market

The global inductor market operates through a structured system which exists because supply chains function effectively and market demand increases together with shifting market trends. Asia-Pacific produces 54% of worldwide output because major manufacturing centers in China and Japan and South Korea drive the industry. More than 60% of market share belongs to leading companies which maintain steady large-scale production but face challenges from raw material price changes which affect about 28% of their manufacturing operations. Consumer electronics hold the highest demand in the market with approximately 34% of total reaching this sector while automotive and telecommunications industries follow because of rising electrification and 5G technology use. The worldwide demand maintains its upward trend because people increasingly use smartphones together with electric vehicles and Internet of Things devices. The surface-mount technology system (SMT) provides over 68 to 85% of installation needs, which enables precise integration into small electronic systems. Original equipment manufacturer partnerships and electronics supply networks create a global system which distributes products worldwide. The market environment develops through technological progress and trade policy changes together with supply chain transformations. The market will expand through 2030 at a rate of approximately 5.5% compound annual growth rate because innovation and miniaturization and industrial automation development drive growth.

Price Analysis and Healthcare Facilities Behaviour Analysis

Inductor prices display major variations because different types of inductors have different size requirements and their purpose defines their use. The typical cost of standard inductors for consumer electronics ranges between 0.05 to 2 per unit, while specialized high-frequency and automotive-grade inductors require advanced materials and precision design. OEMs achieve cost savings of approximately 15% to 25% through bulk purchasing, while price increases of 10% to 15% occur because of raw material price changes for copper and ferrite. Medical electronics in healthcare facilities use inductors for their various applications in imaging systems, ventilators and monitoring devices. Hospitals choose premium-grade inductors because they need components that deliver high reliability with minimal noise, despite the higher expenses which these components entail. Medical device manufacturers show a preference for customized inductors, which help them maintain stable device performance and ensure patient safety, according to more than 40% of manufacturers. The global demand for high-quality inductors has increased because healthcare infrastructure development and advanced medical electronics adoption have grown in the post-pandemic environment.

Market Segmentation

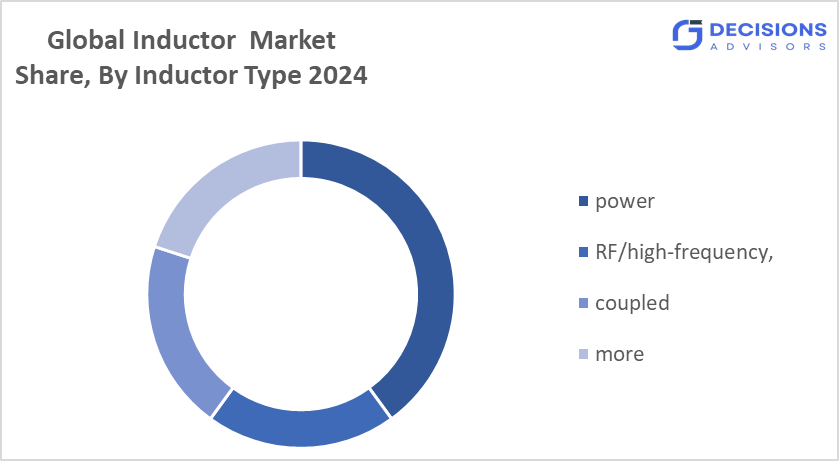

The global inductor market share is classified into solution inductor type, core material, and end user vertical

The power segment dominated the market in 2025, and is projected to grow at a substantial CAGR of approximately 8% during the forecast period.

Based on the inductor type, the global inductor market is divided power, RF/high-frequency, coupled, and more. Among these, the power segment dominated the market in 2025, and is projected to grow at a substantial CAGR of approximately 8% during the forecast period. The power inductor segment leads the market because it functions as a fundamental component which enables power handling and energy distribution for nearly all electronic devices. The market maintains high demand for these inductors because they serve multiple applications which include DC-DC converters and voltage regulators and automotive electronics and renewable energy systems.

- The ferrite segment accounted for the largest share in 2025, and is anticipated to grow at a significant CAGR of approximately 7% during the forecast period.

Based on the core material, the global inductor market is divided into air/ceramic, ferrite, and more. Among these, the ferrite segment accounted for the largest share in 2025, and is anticipated to grow at a significant CAGR of approximately 7% during the forecast period. The ferrite core segment dominates due to high magnetic permeability, low energy loss, and strong high-frequency performance. Its widespread use in consumer electronics, automotive systems, and power supplies, along with cost efficiency and miniaturization benefits, drives growth.

- The automotive segment dominated the market at a CAGR of approximately 6% in 2025, and is projected to grow at a substantial CAGR during the forecast period.

Based on the End-User Vertical, the global inductor market is divided automotive, aerospace and defense, and more. Among these, the automotive segment dominated the market at a CAGR of approximately 6% in 2025, and is projected to grow at a substantial CAGR during the forecast period. The automotive segment dominates due to rising electric vehicle adoption, increasing use of ADAS, and higher electronic content per vehicle. Inductors are essential in power management, battery systems, and infotainment, driving strong and consistent demand growth globally.

Strategies to Implement for Growth of the Market in Non-Leading Regions

Targeted cost management and infrastructure development and awareness programs can boost growth of the global inductor market in non-leading regions. Local manufacturing and assembly units will decrease production and logistics expenses by 20% to 30% which will make inductors more affordable to regional OEMs. The electronics manufacturing sector and EV ecosystem development receive funding from both government entities and private companies because the industry experiences 6% to 8% compound annual growth rate. Market penetration increases through stronger partnerships with local distributors and electronics manufacturers especially in areas where small manufacturers depend on imports for more than 40% of their needs. Technical training and awareness programs will increase adoption of renewable energy and IoT technologies in emerging sectors. The company will enter price-sensitive markets through its low-cost standardized inductors and flexible supply contracts which will also help its long-term business development.

Regional Segment Analysis of the Global Inductor Market

- North America (U.S., Canada, Mexico)

- Europe (Germany, France, U.K., Italy, Spain, Rest of Europe)

- Asia-Pacific (China, Japan, India, Rest of APAC)

- South America (Brazil and the Rest of South America)

- The Middle East and Africa (UAE, South Africa, Rest of MEA)

North America is anticipated to hold the largest share approximately 33% of the global inductor market over the predicted timeframe The forecasted period will see North America maintaining its position as the largest inductor market which will account for 33% of total worldwide sales. The advanced industries which include automotive electronics and aerospace and telecommunications and data centers drive strong demand for this market. The demand for inductors receives additional support from three factors which include the quick establishment of 5G networks and the rising usage of electric vehicles and the substantial funding dedicated to semiconductor production facilities. The region achieves its status as a leader in high-performance electronic components because of its major technology companies and its advanced research and development facilities and its government programs that foster innovation and production.

Asia Pacific is expected to grow at a rapid CAGR approximately 8% in the global inductor market during the forecast period. Asia Pacific is expected to grow at a rapid CAGR of approximately 8% in the global inductor market during the forecast period. This growth is driven by strong electronics manufacturing in countries like China, Japan, South Korea, and India, along with increasing demand for smartphones, EVs, and industrial automation. Rising urbanization and expanding middle-class populations are boosting consumer electronics adoption. Additionally, government initiatives supporting semiconductor and electronics production, along with cost-effective manufacturing and robust supply chains, are accelerating regional market expansion and making Asia Pacific a key growth engine.

Europe is the 3rd largest region to grow in the global inductor market during the region.

Europe is the third-largest region in the global inductor market due to its strong presence in automotive manufacturing, particularly electric vehicles and advanced driver-assistance systems. Countries like Germany, France, and United Kingdom drive demand through industrial automation and renewable energy projects. The region also benefits from strict energy efficiency regulations and increasing investments in smart grids and power electronics. Additionally, a well-established industrial base and growing focus on sustainability and electrification support steady demand for inductors across multiple applications.

Future Market Trends Global inductor market: -

- Miniaturization & High-Efficiency Inductors

demand for compact devices is driving miniaturization, with thin-film inductors growing at around 4.5%–5% CAGR and adoption rising by nearly 25%–30%.

- Rising Demand in Automotive & EV Sector

Inductor usage in electric vehicles and automotive electronics is expanding at approximately 6%–8% CAGR, supported by electrification and advanced driver-assistance systems.

- Growth of 5G & IoT Applications

Expansion of 5G networks and IoT devices is boosting demand for high-frequency inductors, contributing to over 20% increase in telecom-related applications.

Recent Development

- In May, 2025, companies including Sumida Corporation and Hammond Power Solutions launched EV-focused power components, boosting demand for high-efficiency inductors used in charging systems and advanced electrical infrastructure.

- In April, 2025, Bourns, Inc. introduced SRP4021HMCT shielded inductors with metal alloy cores, offering high saturation current and thermal stability, supporting consumer electronics and automotive applications demand.

- In February 2025, Taiyo Yuden commercialized LCQPB series wire-wound ferrite power inductors with full AEC-Q200 qualification, supporting automotive safety systems and enhancing reliability in high-performance electronic and vehicle applications.

- In January 2025, TDK Corporation expanded its ADL4524VL wire-wound inductors for automotive PoC and launched MHQ1005075HA and KLZ2012-A series, supporting high-frequency A2B applications with reliability up to 150°C.

How is Recent Developments Helping the Market?

The global inductor market growth is experiencing a major boost from recent technological advancements which enhance performance, efficiency and expand application possibilities. The new high-frequency multilayer inductors enable 5G and IoT devices to achieve energy efficiency improvements between 15% and 20%. The electric vehicle market is receiving support through product launches and strategic partnerships from key players who introduce automotive-grade inductors and shielded inductors to the market. Inductor usage in electric vehicles is increasing by 30% to 40% with the introduction of new products. The combination of miniaturization progress and surface-mount technology (SMT) advancements allows manufacturers to produce smaller components which maintain better reliability, thus creating a growing demand for consumer electronics products that already make up more than 40% of total market need. The combination of material innovations and automated manufacturing processes leads to better thermal stability and production efficiency improvements which exceed 20%. This development enables manufacturers to establish cost-effective supply systems which help develop their market base.

Market Segment

This study forecasts revenue at global, regional, and country levels from 2020 to 2035. Decision Advisor has segmented the global inductor market based on the below-mentioned segments:

Global inductor market, By Inductor Type

- Power

- RF/High-Frequency

- Coupled

- More

Global inductor market, By Core Material

- Air/Ceramic

- Ferrite

- More

Global inductor market, By End User Vertical

- Automotive

- Aerospace and Defense

- More

Global inductor market, By Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa

Frequently Asked Questions (FAQ)

1. What is the expected growth rate of the market?

The market is expected to grow at a CAGR of 4.28% during the forecast period from 2025 to 2035.

2. What are the key factors driving market growth?

Major drivers include rising demand for consumer electronics, electric vehicles (EVs), 5G infrastructure, renewable energy systems, and IoT devices, along with advancements in power management technologies.

3. Which region dominates the global inductor market?

North America holds the largest market share, accounting for approximately 33% of the global market.

4. Which region is expected to grow the fastest?

The Asia-Pacific region is expected to grow at the fastest rate, with a CAGR of around 8%, driven by strong electronics manufacturing and increasing EV adoption.

Check Licence

Choose the plan that fits you best: Single User, Multi-User, or Enterprise solutions tailored for your needs.

We Have You Covered

- 24/7 Analyst Support

- Clients Across the Globe

- Tailored Insights

- Technology Tracking

- Competitive Intelligence

- Custom Research

- Syndicated Market Studies

- Market Overview

- Market Segmentation

- Growth Drivers

- Market Opportunities

- Regulatory Insights

- Innovation & Sustainability

Report Details

| Scope | Global |

| Pages | 210 |

| Delivery | PDF & Excel via Email |

| Language | English |

| Release | Apr 2026 |

| Access | Download from this page |