Global Liquid Cold Plates Market

Global Liquid Cold Plates Market Size, Share, By Material (Aluminum, Copper, and Stainless Steel) By Type (Standard Tube Cold Plates, Vacuum Brazed Cold Plates, and Friction Stir Welded Cold Plates) By Application (Data Centers, Electric Vehicles, Aerospace & Defense, Industrial Electronics, and Medical Equipment) By End User (IT and Telecom, Automotive, Healthcare, and Manufacturing) and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa), Analysis and Forecast 2026-2035

CAGR

5.38%

REVENUE 2025

USD Billion 1.99

FORECAST 2035

USD Billion 3.36

REPORT COVERAGE

Global

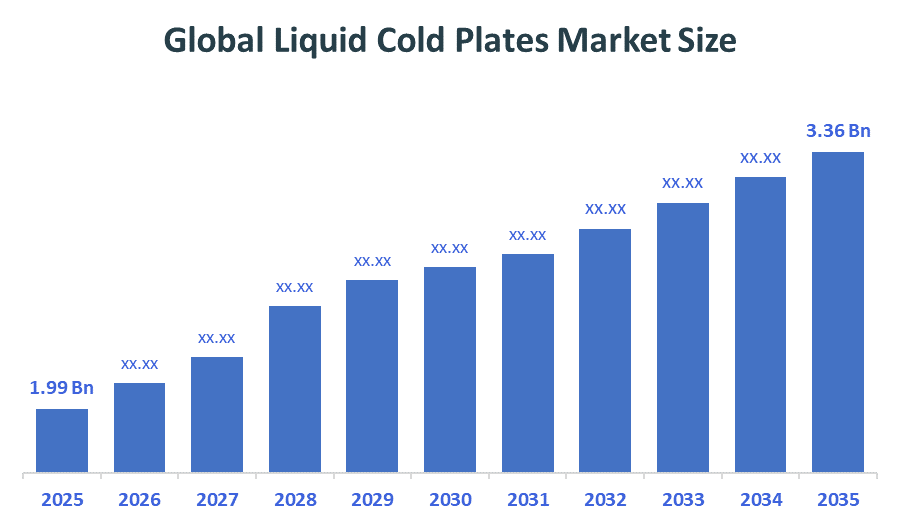

The Global Liquid Cold Plates Market Size was predicted to grow from USD 1.99 billion in 2025 and is projected to reach around USD 3.36 billion by 2035. According to Decision Advisors, a detailed research report on the liquid cold plates market shows that the copper-based cold plate trend dominates the global market, holding approximately 48.6% of the total share worldwide. Boyd Corporation leads the market with approximately 24% of the global market share. Reported full-year 2025 revenue of $3.14 billion USD, making it one of the major market drivers for shaping the industry.

Market Snapshot

- Global Liquid Cold Plates Market Size (2025): USD 1.99 Billion

- Global Liquid Cold Plates Projected Market Size (2035): USD 3.36 Billion

- Global Liquid Cold Plates Compound Annual Growth Rate (CAGR): 5.38%

- Largest Regional Market: Asia-Pacific

- Fastest Growing Region: North America

- 3rd Largest Region: Europe

- Base Year: 2025

- Historical Period: 2021 to 2024

- Forecast Period: 2026 to 2035

Market Overview / Introduction

The liquid cold plates are high-performance thermal management components that work towards localised heat extraction for power semiconductors, CPUs, and battery cells. The liquid cold plates serve as a vital intermediate phase between traditional heat sinks and full immersion cooling, using internal fluid pathways and high-conductivity materials for rapid heat dispersal with minimal space requirements. Modern liquid cold plates possess features such as serpentine tube configurations and microfluidic channels to ensure consistent performance levels while lowering the possibility of thermal throttling in high-density electronics. The liquid cold plates were formerly basic, drilled blocks but have been upgraded into complex, thin-profile thermal management systems with precision-engineered flow paths and integration within high-power AI and server environments. The increased adoption of liquid cold plates is attributed to the rise in demand for electric vehicle battery thermal management and heat management in hyperscale data centers. Liquid cold plates help protect critical hardware from degradation and failure due to their ability to maintain stable operating temperatures in compact enclosures.

- The data center and high-performance computing segments contribute to approximately 45% of the application-based use in the market, driven by the increasing demand for AI-driven server cooling and the transition to high-density rack configurations.

- Battery thermal management technology in the automotive sector is experiencing substantial growth, with a CAGR forecasted to remain above 14% on account of the increasing adoption of high-power charging stations and the advanced generation of long-range electric vehicles.

Notable Insights: -

- Copper liquid cold plates make up about 48.6% of the total market share of this sector. They have gained a reputation in mission-critical operations, particularly in aerospace avionics, defense electronics, and supercomputing clusters.

- About 68% of liquid cooling installations utilize direct-to-chip cold plates. These investments are stimulated mainly by high levels of investment into AI infrastructure and high-power industrial automation because many enterprises experience performance bottlenecks from air-cooled hardware.

- Applications of cold plates in the sphere of renewable energy inverters account for almost 22% of all demand. The rapid development of high-capacity solar farms, alongside increased worries about power semiconductor longevity, has become one of the main drivers of using these advanced plates.

- About 52.3% of the market value belongs to the Asia-Pacific region in 2026. Many countries within this region, like China and India, invest considerable amounts of money in semiconductor fabrication and localised EV production in order to address the growing needs of their technology sectors.

What is the Role of Technology in Shaping the Market?

Technological progress is making some groundbreaking modifications within the thermal management industry with respect to fluid dynamics, weight reduction, and manufacturing precision. The present generation of cold plate platforms has ceased to be simple metal blocks, but now they are complex micro-engineered cooling interfaces capable of self-optimisation for prolonged periods of time owing to their capacity to utilize vacuum-brazing techniques, additive manufacturing (3D printing), and real-time leak detection integration.

How are Recent Developments Helping the Market?

These innovations include the implementation of microfluidic cooling channels, the incorporation of advanced dielectric fluid compatibility, and friction stir welding for leak-proof joints. These innovations have significantly aided in promoting development and growth within the market. Innovations have included the creation of modular cold plates that are capable of safeguarding a variety of high-power IGBT modules, which may range from railway traction systems to multi-kilowatt power supplies, all without fail. Using automated manufacturing mechanics, such innovations will enable precise management of coolant flow through the utilisation of high-performance internal fins without any form of manufacturing defect or system failure occurring.

Market Drivers

Market demand for global liquid cold plates is rising owing to the increased funding of tech giants and automotive firms towards high-density power electronics and energy-efficient server architectures that can satisfy PUE targets in the present times. The modern cold plates have gained considerable popularity in the market on account of their benefits associated with incorporating several features, including uniform temperature distribution, high-pressure resistance, and low-profile design in one robust and maintenance-free solution. Conversely, the emergence of multi-chip modules has led to an increased need for specialised thermal solutions that can help cater to the trend of extreme heat flux densities where the application of standard air-cooled heat sinks is becoming physically impossible.

Restraints

The growth of the international market for the liquid cold plate industry is constrained by the high upfront infrastructure costs and the complexities of ensuring long-term material compatibility with various coolants to prevent internal corrosion.

Competitive Analysis:

The report offers the appropriate analysis of the key organisations/companies involved within the liquid cold plates market, along with a comparative evaluation primarily based on their product offerings, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborate analysis focusing on the current news and developments of the companies, which includes product development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

Top 10 Companies in the Global Liquid Cold Plates Market

- Boyd Corporation

- Lytron (Danfoss)

- Wakefield-Vette

- Wieland MicroCool

- Advanced Thermal Solutions, Inc. (ATS)

- Mikros Technologies

- CoolIT Systems

- Asetek, Inc.

- Fujikura Ltd.

- Rittal GmbH & Co. KG

Government Initiatives

|

Country |

Key Government Initiatives |

|

EU |

The EU 2030 Climate Target Plan set stricter energy efficiency targets for high-power industrial machinery, aiming to reduce industrial energy wastage by 11.7%, significantly influencing the adoption of liquid cold plates in power electronics. |

|

India |

In the Union Budget 2025, the Indian government granted infrastructure status to high-tech manufacturing, facilitating capital expansion for the Make in India initiative for EV components, specifically targeting localised battery cooling plate production. |

|

US |

In alignment with the CHIPS and Science Act, the federal government has intensified funding for domestic semiconductor cooling research. This initiative supports the development of high-efficiency cold plate technologies to secure the local supply chain for AI hardware. |

Study on the Supply, Demand, Distribution, and Market Environment

The success of the liquid cold plate industry depends on finding the sweet spot between the ability to operate with maximum thermal conductivity and the growing need for leak-proof, high-pressure reliability. The supply of liquid cold plates comes from a focus on producing high-purity aluminum and copper alloys and specialized brazing processes capable of delivering instantaneous temperature stabilization without the excessive space requirements associated with legacy air-cooling hardware.

Price Analysis and Consumer Behaviour Analysis

The pricing for liquid cold plates varies depending on the heat flux capacity, manufacturing technology (e.g., vacuum brazed vs. tubed), and material choice. Higher-end products using copper microchannels and equipped with state-of-the-art manifold connections are more expensive. However, standard aluminum tubed plates for consumer electronics and industrial chargers are less costly and provide an ideal opportunity for localized thermal management. Consumers have clearly demonstrated a preference toward long-term reliability and energy efficiency; hence, companies are expected to favor products that ensure operational autonomy, zero-leak integrity, and precise temperature positioning for long periods of time.

Market Segmentation

The Global Liquid Cold Plates Market share is classified into material, type, application, and end user.

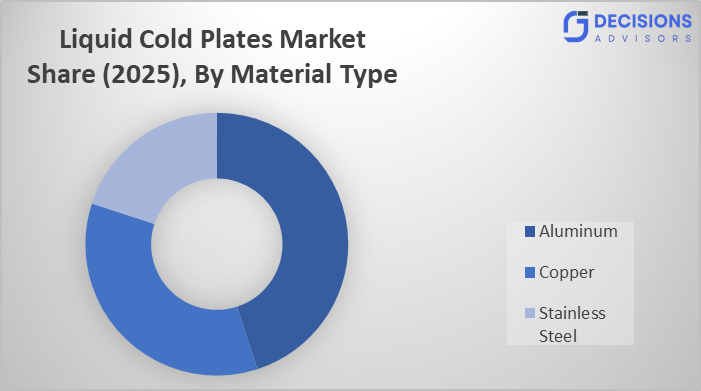

- The Aluminum segment holds the largest volume share, contributing approximately 45% of the market in 2025.

Based on the Material, the global liquid cold plates market is divided into Aluminum, Copper, and Stainless Steel. Among these, The Aluminum segment holds the largest volume share, contributing approximately 45% of the market in 2025. The reason for this dominance lies in its ideal balance of thermal conductivity, low weight, and cost-effectiveness for mass-market applications like electric vehicles.

- The Vacuum Brazed segment accounts for the largest revenue share, representing over 40% of the global market in 2025.

Based on the Type, the global liquid cold plates market is divided into Standard Tube Cold Plates, vacuum brazed cold plates, and friction stir-welded cold plates. Among these, the Vacuum Brazed segment accounts for the largest revenue share, representing over 40% of the global market in 2025. These designs are critical for maintaining high-pressure resistance and intricate internal geometry for mission-critical supercomputing and aerospace electronics.

- Data Centers dominate the global market, accounting for approximately 45% of the total revenue in 2025.

Based on the Application, the global liquid cold plates market is divided into Data Centers, Electric Vehicles, Aerospace & Defense, Industrial Electronics, and Medical Equipment. Among these, Data Centers dominate the global market, accounting for approximately 45% of the total revenue in 2025. This segment is preferred by operators who require direct-to-chip integrated solutions for managing the intense heat of AI and GPU clusters. The Electric Vehicle category is seeing a sharp increase in use, especially in battery cooling systems for luxury and performance EVs.

- The IT and Telecom segment dominates the global market, accounting for approximately 52% of the total revenue in 2025.

Based on the End User, the global liquid cold plates market is divided into IT and Telecom, Automotive, Healthcare, and Manufacturing. Among these, the IT and Telecom segment dominates the global market, accounting for approximately 52% of the total revenue in 2025. This segment is preferred by planners who require large-scale integrated solutions and professional thermal engineering for 5G network expansion and hyperscale cloud infrastructure.

Strategies to Implement for Growth of the Market in Non-Leading Regions

The potential for growth within the liquid cold plate industry in emerging regions could be increased through the deployment of efficient modular thermal platforms for local industrial developers and local agencies tasked with 5G infrastructure management. Programs aimed at achieving semiconductor self-sufficiency by governments contribute substantially toward demand within regions with expanding tech sectors. Further support through increasing investments in training local thermal engineering technicians will facilitate the adoption of sustainable climate control and smart thermal response solutions.

Regional Segment Analysis of the Global Liquid Cold Plates Market

- North America (U.S., Canada, Mexico)

- Europe (Germany, France, U.K., Italy, Spain, Rest of Europe)

- Asia-Pacific (China, Japan, India, South Korea, Rest of APAC)

- Latin America (Brazil and the Rest of Latin America)

- The Middle East and Africa (UAE, South Africa, Rest of MEA)

Asia-Pacific is projected to be the largest region in the liquid cold plates market over the forecast period. In 2025, the region accounted for approximately 38.4% of global revenue, valued at USD 1.46 billion. This dominance is attributed to the presence of major electronics manufacturing hubs and the rapid expansion of the electric vehicle (EV) industry in China, India, and South Korea. Furthermore, significant investments in hyperscale data centres and the widespread adoption of 5G infrastructure are fueling the demand for high-performance liquid cooling solutions to manage increasing heat fluxes in AI-driven workloads.

North America is expected to maintain a significant market share, holding approximately 33.4% of global revenue in 2025. The region's growth is primarily driven by its leadership in the aerospace and defence sectors, alongside a robust ecosystem for high-performance computing (HPC) and artificial intelligence. The United States leads the regional market due to substantial corporate spending on liquid-cooled server architectures for generative AI and the integration of advanced thermal management in next-generation radar and electronic warfare systems.

Europe is anticipated to hold a substantial share, contributing approximately 22.4% of the global market. The region benefits from a strong foundation in automotive engineering, particularly in Germany and Italy, where the transition to 800V EV architectures is driving the demand for precision-machined aluminium cold plates. Additionally, rigorous European Union standards regarding energy efficiency and the "Circular Economy" have accelerated the adoption of closed-loop liquid cooling systems in industrial automation and renewable energy inverters.

Recent Developments

- In February 2026, Boyd Corporation announced a strategic partnership with a North American hyperscale cloud operator to supply over 500,000 direct liquid cooling cold plate assemblies for AI server rack deployments scheduled for 2026-2027.

- In January 2026, CoolIT Systems launched its Rack DLC 3.0 platform, featuring cold plate manifolds specifically engineered for the NVIDIA Blackwell GB200 architecture, achieving a 22% improvement in coolant-side thermal resistance.

- In June 2025, Asia Vital Components Co., Ltd. (AVC) unveiled the AVC-LC Series of aluminum cold plates, designed for 800V EV battery packs with high-pressure ratings of 200 psi and bionic serpentine channel geometries for superior temperature uniformity.

- In March 2025, Mikros Technologies completed a USD 42 million Series B funding round to scale the production of its proprietary micro-channel copper cold plates used in quantum computing cryostats and high-power defense electronics.

Market Segmentation

This study forecasts revenue at global, regional, and country levels from 2021 to 2035. The Global Liquid Cold Plates Market is segmented based on the following categories:

Global Liquid Cold Plates Market, By Type

- Machined Channel Cold Plates

- Tubed Cold Plates

- Vacuum-Brazed Cold Plates

- Friction Stir Welded (FSW) Cold Plates

Global Liquid Cold Plates Market, By Material

- Aluminum

- Copper

- Stainless Steel

Global Liquid Cold Plates Market, By Application

- Data Centers

- Electric Vehicle (EV) Batteries

- Power Electronics

- Industrial Electronics

- Aerospace & Defense

Global Liquid Cold Plates Market, By Regional Analysis

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- United Arab Emirates

- Saudi Arabia

- Qatar

- South Africa

- Rest of Middle East & Africa

Frequently Asked Questions (FAQ)

What is the significance of temperature uniformity in EV battery cold plates?

Keeping temperatures consistent across a battery pack is vital for long-term vehicle health. When some cells are significantly hotter than others, they age much faster, which eventually forces the entire battery pack to perform at the level of its weakest, most degraded cell. High-performance liquid cooling is designed to maintain a very tight temperature range that traditional air cooling simply cannot achieve.

How does vacuum brazing improve cold plate performance?

Vacuum brazing is a high-precision joining process that bonds components together without using extra chemicals like flux. This results in a "clean" internal build and incredibly strong structural integrity. This strength allows for complex internal designs that can handle extreme pressure, making it a go-to choice for high-stakes environments like aerospace and supercomputing.

Why is aluminium the preferred material for liquid cold plates in the automotive sector?

Aluminium is the gold standard for electric vehicles because it hits the "sweet spot" of performance and practicality. It is lightweight, which is essential for maximising a car's driving range, yet it conducts heat very effectively. Additionally, it is cost-effective and stands up well against corrosion when mixed with standard cooling fluids.

What role does Microchannel technology play in cooling AI processors?

As AI processors become more powerful, they generate an immense amount of heat that standard cooling methods can no longer manage. Microchannel technology solves this by using incredibly narrow paths for coolant to flow through. This drastically increases the surface area available to pull heat away, allowing these chips to run at peak performance without overheating.

Check Licence

Choose the plan that fits you best: Single User, Multi-User, or Enterprise solutions tailored for your needs.

We Have You Covered

- 24/7 Analyst Support

- Clients Across the Globe

- Tailored Insights

- Technology Tracking

- Competitive Intelligence

- Custom Research

- Syndicated Market Studies

- Market Overview

- Market Segmentation

- Growth Drivers

- Market Opportunities

- Regulatory Insights

- Innovation & Sustainability

Report Details

| Scope | Global |

| Pages | 210 |

| Delivery | PDF & Excel via Email |

| Language | English |

| Release | May 2026 |

| Access | Download from this page |