Medical Oxygen Concentrator Market

Global Medical Oxygen Concentrator Market Size, Share, and COVID-19 Impact Analysis, By Modality (Portable and Stationary), By Technology (Pulse Flow and Continuous Flow), By End User (Hospital, Homecare, Ambulatory Surgical Centres), and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2025-2035

CAGR

6.43%

REVENUE 2024

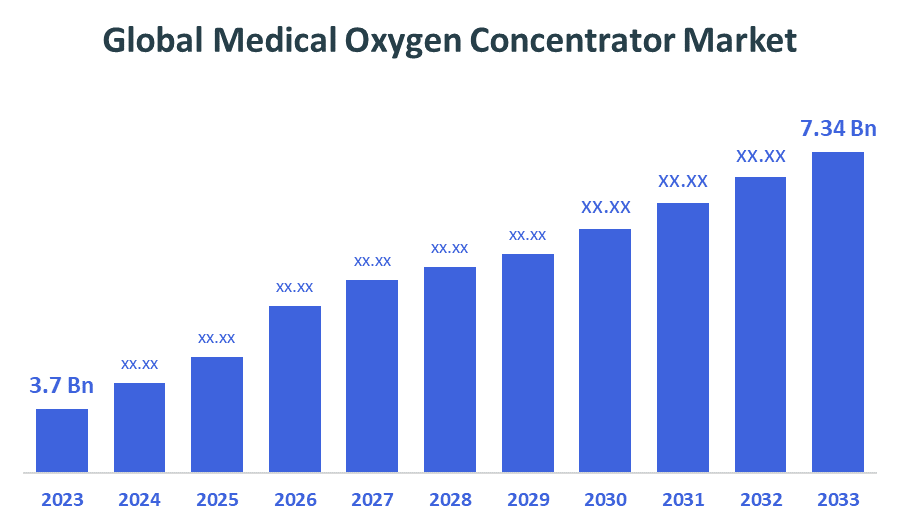

USD Billion 3.7

FORECAST 2035

USD Billion 7.34

REPORT COVERAGE

Global

Global Medical Oxygen Concentrator Market Insights Forecasts to 2035

- The Global Medical Oxygen Concentrator Market Size Was Estimated at USD 3.7 Billion in 2024

- The Market Size is Expected to Grow at a CAGR of around 6.43% from 2025 to 2035

- The Worldwide Medical Oxygen Concentrator Market Size is Expected to Reach USD 7.34 Billion by 2035

- Asia Pacific is expected to grow the fastest during the forecast period.

Medical Oxygen Concentrator Market

Medical oxygen concentrations are devices that extract oxygen centered by ambient air and are concentrated for patients suffering from respiratory disorders such as COPD, asthma, sleep apnea, and pneumonia complications. Portable and stable models serve settings ranging from home care to hospitals and emergency services. The market expanded rapidly, as the demand for oxygen therapy equipment increased. Additionally, the increasing prevalence of chronic respiratory diseases, the aging population, and the growing preference for home-based oxygen therapy are primary development drivers.

Attractive Opportunities in the Medical Oxygen Concentrator Market

- The growing demand for portable oxygen concentrations offers a major opportunity for manufacturers. With increasing preference for home-based care and dynamics-centered respiratory support, compact devices that provide long battery life and are easy to use are becoming necessary. Patients with chronic obstructive pulmonary disease (COPD) and elderly individuals, like portable systems, who do not require continuous refill or continuous electricity.

- The growth of the home healthcare segment provides another attractive opportunity for market expansion. As the infrastructure of the hospital increases pressure and long-term entry costs, more patients are being treated with oxygen therapy at home. Governments and insurance providers in countries like the United States, Japan, and Germany are covering domestic oxygen support under chronic disease management policies.

- Emerging markets also have strong potential, especially in the Asia-Pacific and Latin American regions. With increasing awareness about respiratory disorders, extending high disease burden and access to healthcare, countries such as India, China, and Brazil are seeing increasing demand for oxygen therapy. Local manufacturing assistance, government procurement programs, and partnerships with NGOs are helping to enter these disqualified markets.

Global Medical Oxygen Concentrator Market Dynamics

DRIVER: Rising Prevalence of Respiratory Diseases

The primary driver of the Global Medical Oxygen Concentrator Market is the increasing prevalence of chronic respiratory diseases like COPD, asthma, and sleep apnea. As global air pollution deteriorates and the elderly population increases, more individuals require long-term oxygen therapy in both hospitals and home care settings. In addition, complications have contributed to the increase in demand for respiratory aid equipment, including oxygen concentrations. This growing patient population continues market growth, especially with a high incidence of respiratory diseases in urban areas.

RESTRAINT: High Cost of Devices and Limited Access in Rural Areas

Medical oxygen concentrations, especially the high costs of portable models, consist of an advanced battery and flow system. These devices are not always covered under basic health insurance schemes in developing countries. In many rural or lower-income areas, access to reliable power and maintenance support is limited, making it difficult for patients to use these devices continuously. This cost barrier and infrastructure boundaries slow down citizens in underserved areas.

OPPORTUNITY: Expansion of Home Healthcare Services

The expansion of home healthcare services offers a strong opportunity for market development. Since hospitals aim to reduce inpatient stays and promote outpatient care, there is a growing change towards home-based oxygen therapy. Patients with long-term respiratory conditions prefer home treatment for comfort and convenience. Healthcare providers and insurers are supporting home oxygen care in markets such as the US, UK, Japan, and Germany, causing both stable and portable oxygen concentrations in residential settings.

CHALLENGES: Regulatory and Certification Barriers

Oxygen concentrations are subject to strict regulatory requirements for market device certification and clinical use. Manufacturers should follow standards set by agencies such as the US FDA, European CE, and other national bodies, which can delay product approval and limit global distribution. Additionally, the difference in technical guidelines in countries makes manufacturing and testing processes difficult for companies to streamline, especially when entering new markets with limited regulatory transparency.

Global Medical Oxygen Concentrator Market Ecosystem Analysis

The medical oxygen concentration market operates within a colleague ecosystem that includes device manufacturers, healthcare providers, regulatory agencies, and distribution partners. Leading companies such as Philips Response, Inquire, Innocent, and Drive Devilbis Healthcare develop portable and stable oxygen concentrations used in both hospital and homecare settings. These manufacturers work closely with clinical experts, respiratory physicians, and homecare service providers to ensure accurate prescriptions, setups, and maintenance of equipment. Regulatory bodies such as the US FDA, CE in Europe, and the ISO Authority take care of product approval and compliance with safety standards.

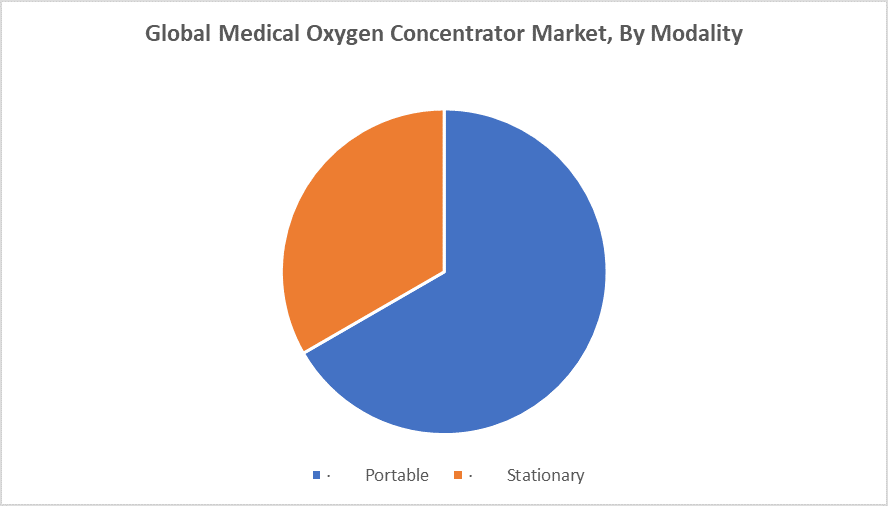

Based on the modality, the portable segment led the market with the leading revenue share over the forecast period

The segment dominance is driven by because of the growing need for home-based oxygen therapy that is suitable, portable, and simple to use. Patients who need continuous oxygen support while doing their everyday activities are drawn to these portable devices. Older patients are using batteries more frequently due to advancements in battery technology and their small design, especially in developed nations like North America and Europe.

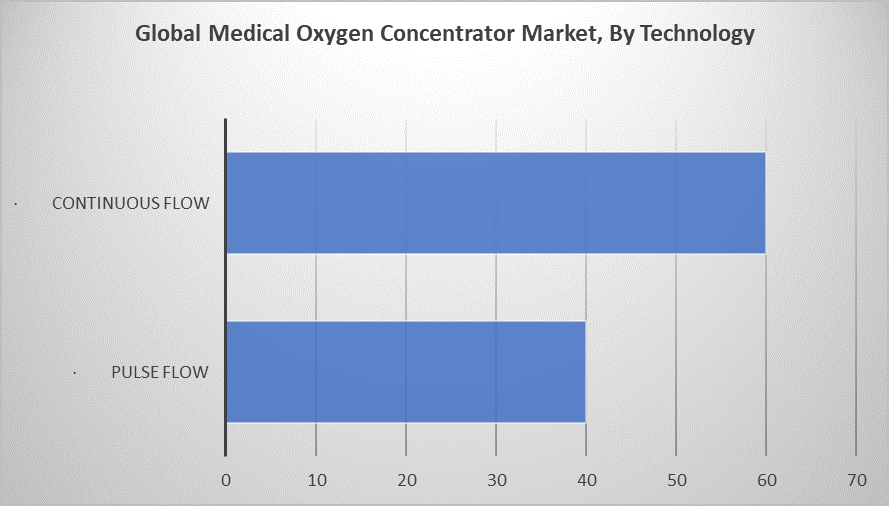

Based on the technology, the continuous flow segment led the market with the major revenue share during the forecast period

The continuous flow segment led the market, holding the largest revenue share during the forecast period. Their extensive application in long-term care and medical settings. For patients who need consistent oxygen assistance during rest and activity, these devices are perfect since they provide a steady delivery of oxygen. Additionally, continuous flow devices are preferred because they work with CPAP and BiPAP machines, particularly for individuals with COPD and sleep apnea.

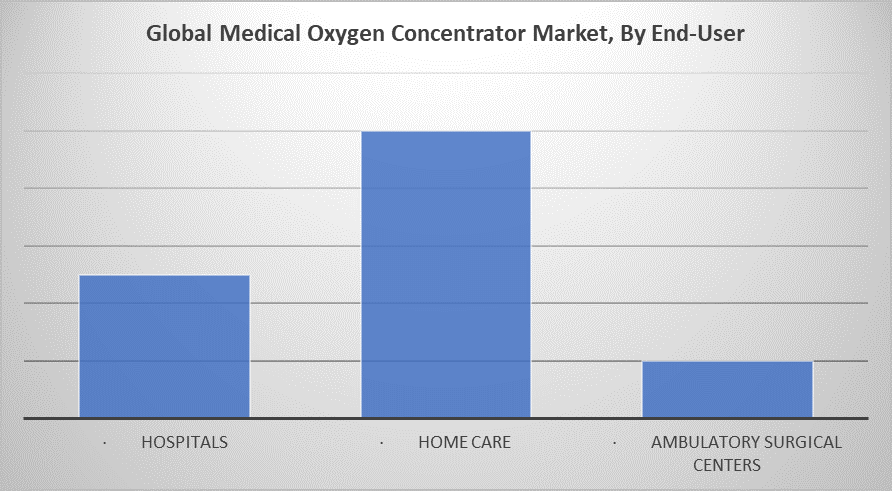

Based on the end-user, the home care segment led the market with the major revenue share during the forecast period

The home care segment led the market, holding the largest revenue share during the forecast period. Increasing preference for in-home respiration support, especially for patients with chronic obstructive pulmonary disease (COPD) and other long-term conditions. The cost of healthcare and the increase in hospital bed deficiency have motivated governments and healthcare providers to adopt home-based oxygen therapy as a cost-effective and patient-friendly alternative. In addition, technological progress in distance monitoring and the easy use of oxygen devices has increased the safety and access to home oxygen solutions.

North America is anticipated to hold the largest market share of the medical oxygen concentrator market during the forecast period

North America is anticipated to hold the largest market share in the medical oxygen concentrator market during the forecast period. Supported by a well-developed healthcare system, a high diagnosis rate of respiratory diseases, and widespread home oxygen therapy. The United States leads the region, with continuous product innovation by companies such as Medicare Support, Strong Supply Series and Innocent, and Philips Respironics. Additionally, a growing elderly population and increasing cases of COPD, sleep apnea complications have contributed to the continuous demand for both portable and stable oxygen concentrations.

Asia Pacific is expected to grow at the fastest CAGR in the medical oxygen concentrator market during the forecast period

Asia Pacific is expected to grow at the fastest CAGR in the medical oxygen concentrator market during the forecast period. Increased rates of respiratory diseases, an increase in health care expenses, and expanding homecare services in countries such as China, India, and Indonesia. The infrastructure of oxygen is required, leading to the government's initiative and local production of oxygen concentrations. Increasing awareness about oxygen therapy and improving access to healthcare in both urban and semi-urban areas are expected to promote the demand for both portable and stable oxygen equipment.

Recent Development

- In March 2024, CAIRE, an oxygen supply manufacturer, started a new state-of-the-art medical technology center in Chengdu, China, to better serve its customers in the Asia Pacific region. The site will manufacture the company’s Eclipse 5 portable oxygen concentrator and the VisionAire 5 stationary oxygen concentrator, along with a range of select AirSep commercial oxygen concentrators.

Key Market Players

KEY PLAYERS IN THE MEDICAL OXYGEN CONCENTRATOR MARKET INCLUDE

- Philips Respironics

- Inogen Inc.

- Invacare Corporation

- Drive DeVilbiss Healthcare

- CAIRE Inc.

- O2 Concepts

- Nidek Medical

- Chart Industries (AirSep)

- Teijin

- Precision Medical, Inc.

- Besco Medical Co., Ltd.

- Others

Market Segment

This study forecasts revenue at global, regional, and country levels from 2020 to 2035. Dicision Advisors has segmented the medical oxygen concentrator market based on the below-mentioned segments:

Global Medical Oxygen Concentrator Market, By Modality

- Portable

- Stationary

Global Medical Oxygen Concentrator Market, By Technology

- Pulse Flow

- Continuous Flow

Global Medical Oxygen Concentrator Market, By End-User

- Hospitals

- Home Care

- Ambulatory Surgical Centers

Global Medical Oxygen Concentrator Market, By Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa

Check Licence

Choose the plan that fits you best: Single User, Multi-User, or Enterprise solutions tailored for your needs.

We Have You Covered

- 24/7 Analyst Support

- Clients Across the Globe

- Tailored Insights

- Technology Tracking

- Competitive Intelligence

- Custom Research

- Syndicated Market Studies

- Market Overview

- Market Segmentation

- Growth Drivers

- Market Opportunities

- Regulatory Insights

- Innovation & Sustainability

Report Details

| Scope | Global |

| Pages | 240 |

| Delivery | PDF & Excel via Email |

| Language | English |

| Release | May 2025 |

| Access | Download from this page |