Global Obesity Surgery Devices Market

Global Obesity Surgery Devices Market Size, Share, By Device Type (Minimally Invasive Surgical Devices, and Non-Invasive / Implantable Devices), By Procedure Type (Sleeve gastrectomy, Gastric bypass, Adjustable gastric banding, Mini-gastric bypass, Revision bariatric surgery, Biliopancreatic diversion with duodenal switch and Non-invasive bariatric procedures), By Functional Category (Stapling devices, Gastric bands, Gastric balloons, Energy-based devices, Suturing & closure devices, and Access devices)By End User (Hospitals, Ambulatory Surgical Centres, Specialty bariatric clinics, and Surgical centres), and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2026-2035.

CAGR

6.39%

REVENUE 2025

USD Billion 1.97

FORECAST 2035

USD Billion 3.66

REPORT COVERAGE

Global

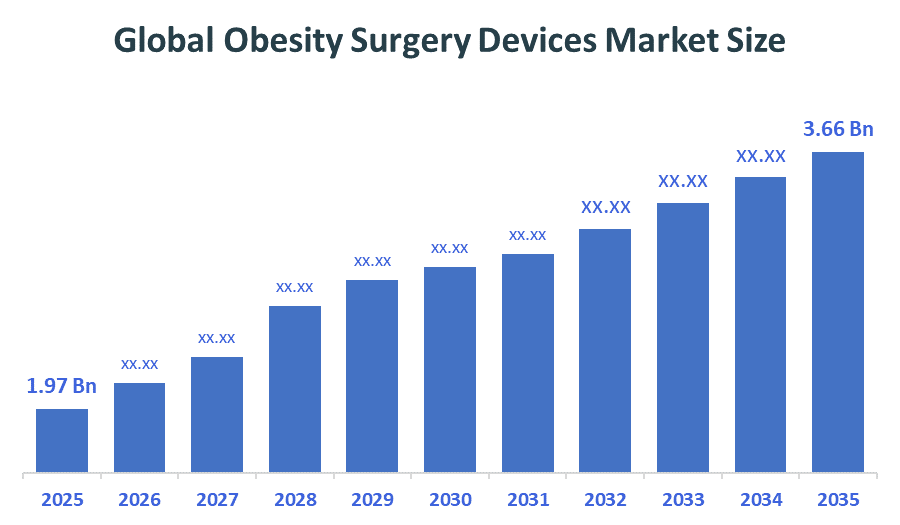

The Global Obesity Surgery Devices Market Size is projected USD 1.97 Billion in 2025 and is forecasted to reach around USD 3.66 Billion by 2035. According to Decision Advisors, a detailed report on analysis of the Global Obesity Surgery Devices Market indicates that the Minimally invasive bariatric surgery adoption trend dominates the Market, accounting for approx. 64.1% of the total global demand worldwide. Medtronic plc dominates the Global Obesity Surgery Devices Market, supported by revenue of approx. USD 32–33 billion, due to technological leadership in minimally invasive surgical devices, strong clinical outcomes, and extensive global hospital adoption worldwide.

Market Snapshot

- Global Obesity Surgery Devices Market Size (2025): USD 1.97 Billion

- Projected Global Obesity Surgery Devices Market Size (2035): USD 3.66 Billion

- Global Obesity Surgery Devices Market Compound Annual Growth Rate (CAGR): 6.39%

- Largest Regional Market: Asia pacific

- Fastest Growing Region: North America

- 3rd Largest Region: Europe

- Base Year: 2025

- Historical Period: 2021–2024

- Forecast Period: 2026–2035

Market Overview/ Introduction

Obesity surgery devices market is defined as the global industry that revolves around the development, manufacturing, distribution, and sale of medical devices for conducting surgical operations aimed at treating obesity. Examples of such devices include stapling systems, gastric bands, gastric balloons, suturing and closure devices, energy-based surgical devices, and access devices. Such devices are primarily used in obesity surgeries, including sleeve gastrectomy, gastric bypass, and adjustable gastric banding surgeries. These procedures can assist obese individuals in losing excessive weight through minimal invasions in the case where conventional approaches fail to provide any improvements. The primary purpose of using obesity surgery devices is to minimize the volume of an individual's stomach or prevent them from consuming large amounts of food. There are high growth prospects in the market as a result of increasing cases of global obesity. The estimated number of obese people in the world today is more than 1 billion people. Technological innovations have made bariatric surgeries easier with improved accuracy. Technologies include staplers, energy-based surgical sealers, and minimally invasive robotic systems among others. Single incision laparoscopic surgery is another technology contributing to growth in the market. In addition, the government has played an active role in ensuring that the market continues to expand. Reimbursement of medical expenses by insurance companies is common practice in countries such as the US and other European countries. Emerging countries have adopted public health policies for bariatric surgeries.

- In March 2026, patent expiry of semaglutide, India's PLI scheme is accelerating domestic generic production, significantly lowering obesity treatment costs and disrupting the traditional surgical device market landscape.

- In February 2026, The All India Institute of Ayurveda provides holistic obesity management services using Ayurveda, yoga, diet control, and lifestyle therapy, supporting non-surgical weight management and metabolic health improvement in India.

- In December 2025, Quality Council of India promotes healthcare accreditation standards that enhance safety and quality in bariatric and obesity surgery centres, supporting improved clinical outcomes in surgical obesity management in India.

Notable Insights: -

- Asia-Pacific holds the largest regional Market share approximately 38% in the Global Obesity Surgery Devices Market.

- North America is the fastest growing region Market share approximately 32% in the Global Obesity Surgery Devices Market.

- By Device Type, the Minimally Invasive Surgical Devices segment held a dominant position with 76% in terms of Market share in 2025.

- By Procedure Type, Sleeve gastrectomy segment is the dominating accounting for Market is approximately 48%.

- By End User, Hospitals segment held a dominant position Market is approximately 58%.

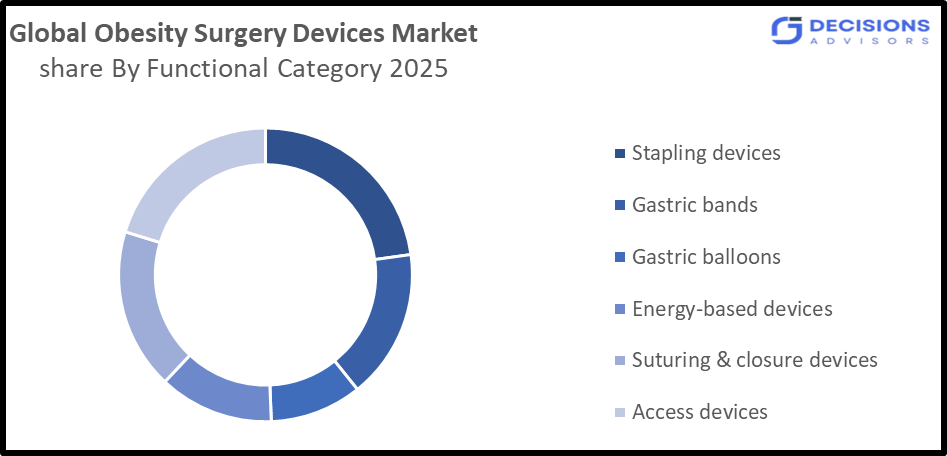

- By Functional Category, Stapling devices segment held a dominant position Market is approximately 43%.

- The Market is likely to achieve a valuation of USD 3.66 Billion by 2035.

What is role of technology in grooming the Market?

Technology is critical in shaping the Global Obesity Surgery Devices Market through safety enhancement, precision, and improved clinical results for weight loss surgeries. With the introduction of modern minimally invasive laparoscopic devices, surgical staplers, and energy-based devices for sealant purposes, the occurrence of medical errors during operations has decreased, making this procedure highly acceptable among both doctors and patients. The application of robotic surgery technology to perform weight loss surgeries has improved the accuracy of medical professionals, allowing them to perform their duties with ease. Artificial intelligence and digital imaging have also been incorporated in this market, enabling better pre-planning and real-time decision-making processes.

How is Recent Developments Helping the Market?

Emerging trends have been greatly benefiting the Global Obesity Surgery Devices Market by increasing the accuracy, safety, and uptake of minimally invasive surgeries and robotic surgeries. For example, in 2025–2026, manufacturers such as Medtronic introduced advanced bariatric surgery devices that had high-precision sensors and staplers with high accuracy levels to ensure the safety of patients and improved outcomes. Similarly, in January 2026, Johnson & Johnson filed a request with the FDA to test its new OTTAVA Robotic Surgical System as part of the move towards robotic-assisted bariatric surgery. Such trends help in catering to the demand arising from the increasing prevalence of obesity globally, where it has been predicted that there would be over 1 billion obese individuals across the world (according to the WHO). Also, according to reports, in 2025, minimally invasive surgeries were seen to hold a market share of more than 60% in the bariatric surgeries market owing to reduced risks and lower hospitalization costs. Besides, with growth in robotic platforms, single-use instruments, and AI-powered pre-operative surgical planning tools, the uptake and use of such technologies have grown exponentially.

Market Drivers

The Global Obesity Surgery Devices Market growth drivers include an increase in the global prevalence of obesity, where more than 1 billion individuals are expected to become obese by 2025, as estimated by WHO. The growing usage of minimally invasive surgery devices such as the gastric sleeve surgery and gastric bypass surgery is creating significant demand for obesity surgery devices. Advances in technology such as stapler power devices, robotic surgery devices, and energy sealers, among others, have greatly contributed towards improving surgical accuracy and results. Rising incidences of diabetes and heart diseases as obesity co-morbidities are driving surgical interventions.

Restrain

The factors that prevent the market from growing include high procedural expenses, insufficient compensation in developing nations, and potential surgical hazards including complications and infections. Furthermore, the lack of bariatric surgeons in poor areas is another aspect that hinders market growth. Finally, there is an option for patients who prefer not to go for surgical weight loss.

Competitive Analysis:

The report offers the appropriate analysis of the key organizations/companies involved within the Obesity Surgery Devices Market, along with a comparative evaluation primarily based on their Product of offering, business overviews, geographic presence, enterprise strategies, segment Market share, and SWOT analysis. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes Product development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and Others. This allows for the evaluation of the overall competition within the Market.

Top Companies in Global Obesity Surgery Devices Market

- Medtronic plc

- Johnson & Johnson (Ethicon Inc.)

- Intuitive Surgical, Inc.

- Olympus Corporation

- Boston Scientific Corporation

- B. Braun Melsungen AG

- Conmed Corporation

- Apollo Endosurgery, Inc.

- ReShape Lifesciences, Inc.

- Stryker Corporation

Government Initiatives

|

Country |

Key Government Initiatives |

|

U.S.

|

In April 2026, Governments in developed and developing countries are increasing funding for obesity management programs, expanding prevention, treatment, and clinical care initiatives, supporting broader access to obesity-related healthcare services. |

|

India |

In April 2026, Government and medical bodies are promoting non-invasive and endoscopic obesity treatment techniques to reduce hospital stays, complications, and infection risks, supporting growth of minimally invasive obesity care solutions. |

Study on the Supply, Demand, Distribution, and Market Environment of Obesity Surgery Devices Market

The global obesity surgery devices market shows a balanced but rapidly expanding supply-demand environment driven by rising obesity rates and increasing bariatric procedures. Demand is highest in North America and Europe due to high obesity prevalence, advanced healthcare infrastructure, and strong reimbursement policies. Supply is dominated by key manufacturers such as Medtronic and Johnson & Johnson, ensuring steady availability of stapling systems, energy devices, and minimally invasive tools. Distribution occurs mainly through direct hospital contracts, medical device distributors, and specialized surgical suppliers. The market environment is highly competitive, innovation-driven, and regulated, with growing adoption of robotic-assisted and minimally invasive technologies improving procedural efficiency and expanding global access to obesity treatment solutions.

Price Analysis and Consumer Behaviour Analysis

The Global Obesity Surgery Devices Market is known for its high prices due to device and procedure costs, playing a significant role in pricing trends. Depending on the country, type of hospital, and technology employed, the cost of bariatric surgeries is estimated at USD 7,000-25,000 per patient. The cost of robotic surgery, for instance, is 2-3 times higher than traditional laparoscopic surgery, which makes it difficult to penetrate price-sensitive markets. High costs associated with stapling and energy-based devices account for an essential portion of the procedure cost, thanks to their high precision. As for consumer behaviour, there is an observable trend in favour of safe, fast and less-invasive procedures, as seen in over 60% choosing laparoscopic surgeries in 2025. Consumers in developed countries tend to use health insurance extensively, whereas those in developing countries face the problem of affordability.

Market Segmentation

The Global Obesity Surgery Devices Market share is classified into mounting device type, procedure type, and end user

- The Minimally Invasive Surgical Devices segment dominated the Market in 2025, and is projected to grow at a substantial CAGR of approximately 7.2% during the forecast period.

Based on the device type, the global obesity surgery devices market is divided into minimally invasive surgical devices, and non-invasive / implantable devices. Among these, Minimally Invasive Surgical Devices dominate the Global Obesity Surgery Devices Market. In 2025, this segment is estimated to account for around 70–80% of total market revenue, driven by high adoption of laparoscopic bariatric procedures such as sleeve gastrectomy and gastric bypass. The segment is also projected to grow at a CAGR of approximately 6–8%, supported by shorter hospital stays, reduced complications, and increasing preference for advanced stapling and energy-based surgical technologies worldwide.

The Sleeve gastrectomy segment accounted for the largest share in 2025, and is anticipated to grow at a significant CAGR of approximately 8.6% during the forecast period.

Based on the procedure type, the global obesity surgery devices market is divided into sleeve gastrectomy, gastric bypass, adjustable gastric banding, mini-gastric bypass, revision bariatric surgery, biliopancreatic diversion with duodenal switch, and non-invasive bariatric procedures. Among these, Sleeve gastrectomy is the leading segment in the Global Obesity Surgery Devices Market. In 2025, it is estimated to account for approximately 45–50% of total market revenue, driven by its simplicity, lower complication rates, and strong clinical outcomes compared to other bariatric procedures. The segment is projected to grow at a CAGR of around 7–9% (2025–2035), supported by rising obesity prevalence, increasing patient preference for minimally invasive surgery, and expanding hospital adoption globally.

The Hospitals segment dominated the Market in 2025, and is projected to grow at a substantial CAGR of approximately 5.3% during the forecast period.

Based on the end user, the global obesity surgery devices market is divided into hospitals, ambulatory surgical centres, specialty bariatric clinics, and surgical centres. Among these, Hospitals dominate the Global Obesity Surgery Devices Market. In 2025, this segment is estimated to hold around 55–60% of total market revenue, driven by high patient inflow, availability of advanced bariatric surgical infrastructure, and presence of skilled surgeons. Hospitals are projected to grow at a CAGR of approximately 5–7% (2025–2035), supported by increasing obesity-related admissions and complex bariatric procedures requiring multidisciplinary care and advanced minimally invasive surgical technologies.

- The Pharmaceuticals segment dominated the Market in 2025, and is projected to grow at a substantial CAGR of approximately 7.6% during the forecast period.

Based on the functional category, the global obesity surgery devices market is divided into stapling devices, gastric bands, gastric balloons, energy-based devices, suturing & closure devices, and access devices. Among these, Stapling devices dominate the Global Obesity Surgery Devices Market. In 2025, this segment is estimated to account for around 35–45% of total market revenue, driven by its critical role in major bariatric procedures such as sleeve gastrectomy and gastric bypass. The segment is projected to grow at a CAGR of approximately 6–8% (2025–2035), supported by rising adoption of minimally invasive surgeries, technological advancements in surgical staplers, and increasing global obesity-related surgical volumes.

Strategies to Implement for Growth of the Market in Non-Leading Regions

Innovations to boost the market growth in non-leading markets including APAC, Latin America, and some Middle Eastern nations can be achieved by various measures. Affordable expansion of bariatric surgeries and implementation of minimally invasive and cost-efficient medical devices will contribute greatly to achieving this aim. Collaboration with local manufacturers and technology licensing will enable reduction of cost of medical devices by 20–30%. The development of healthcare infrastructure and establishment of bariatric surgeon training courses will ensure an adequate number of trained specialists. Moreover, governments of the leading countries suffering from the obesity epidemic can promote the growth through their programs to cover the cost of operations and encourage citizens to get obesity treatment. In recent years, adult obesity incidence rate rose by over 5–8% annually in Indian and Chinese cities.

Regional Segment Analysis of the Obesity Surgery Devices Market

- North America (U.S., Canada, Mexico)

- Europe (Germany, France, U.K., Italy, Spain, Rest of Europe)

- Asia-Pacific (China, Japan, India, Rest of APAC)

- South America (Brazil and the Rest of South America)

- The Middle East and Africa (UAE, South Africa, Rest of MEA)

Asia pacific is anticipated to hold the largest share of the Obesity Surgery Devices Market over the predicted timeframe.

Asia Pacific is anticipated to hold the largest share of the Obesity Surgery Devices Market due to rapidly rising obesity prevalence, expanding healthcare infrastructure, and increasing adoption of minimally invasive bariatric procedures in countries like China, India, and Japan. Growing medical tourism and improving reimbursement policies further support demand. In 2025, the region accounts for approximately 38% market revenue share, with a projected CAGR of around 11.5% (2025–2035). Rising awareness of obesity-related diseases and affordability of advanced surgical technologies are key growth drivers.

North America is expected to grow at a rapid CAGR in the Obesity Surgery Devices Market during the forecast period. North America is expected to grow at a rapid CAGR in the Obesity Surgery Devices Market due to high obesity prevalence, strong healthcare infrastructure, advanced adoption of minimally invasive and robotic bariatric surgeries, and favorable insurance reimbursement policies. The region benefits from continuous technological innovation and early adoption of premium surgical devices. In 2025, North America accounts for approximately 32% market revenue share, with a projected CAGR of around 10.2% (2025–2035). Rising awareness of obesity-related comorbidities and increasing surgical procedure volumes further drive market expansion across the region.

Europe is the 3rd largest region to grow in the Obesity Surgery Devices Market during the region. Europe is the third-largest region in the Obesity Surgery Devices Market due to rising obesity prevalence, strong public healthcare systems, and wide insurance coverage for bariatric procedures. Countries like Germany, France, and the UK show high adoption of minimally invasive and laparoscopic surgeries supported by advanced hospital infrastructure. In 2025, Europe holds approximately 27% market revenue share, with a projected CAGR of around 9.4% (2025–2035). Increasing government focus on obesity management and growing preference for safe surgical weight-loss solutions further support regional market growth.

Future Market Trends in Global Obesity Surgery Devices Market: -

- Shift Toward Minimally Invasive and Robotic-Assisted Surgery

The Global Obesity Surgery Devices Market is increasingly moving toward minimally invasive and robotic-assisted procedures. Surgeons prefer laparoscopic and robotic systems due to improved precision, reduced blood loss, and faster recovery times. This trend is boosting demand for advanced stapling, suturing, and energy-based devices. Rising patient preference for less painful procedures and shorter hospital stays is accelerating adoption. Hospitals are also investing in robotic platforms to improve surgical outcomes and handle growing bariatric surgery volumes efficiently.

2. Rising Adoption of Advanced Stapling and Smart Surgical Devices

Technological innovation in stapling devices is a key future trend. Manufacturers are developing smart staplers with better tissue compression, real-time feedback, and enhanced safety features to reduce complications. These advancements improve surgical accuracy in procedures like sleeve gastrectomy and gastric bypass. Integration of digital technologies and ergonomic designs is making surgeries more efficient. As bariatric procedures increase globally, demand for high-performance, reliable, and cost-effective stapling systems is expected to grow significantly.

- Expanding Bariatric Surgery Access in Emerging Markets

Emerging economies are becoming major growth hubs for obesity surgery devices due to rising obesity rates and improving healthcare infrastructure. Countries in Asia-Pacific and Latin America are expanding access to bariatric procedures through private hospitals and government healthcare initiatives. Increasing medical tourism is also supporting market expansion. Lower procedure costs and growing awareness of obesity-related health risks are driving demand. This expansion is encouraging global manufacturers to strengthen distribution networks and partnerships in developing regions.

Recent Development

- In April 2026, FDA, United States continues to regulate and approve advanced obesity treatment devices including intragastric balloon systems like ORBERA, supporting growth of minimally invasive bariatric procedures and medical device innovation.

- In April 2025, Johnson & Johnson MedTech completed first clinical cases using the OTTAVA robotic surgical system in Roux-en-Y gastric bypass procedures, advancing precision in bariatric surgery innovation.

Market Segment

This study forecasts revenue at Global, regional, and country levels from 2021 to 2035. Decision Advisors has segmented the Global Obesity Surgery Devices Market based on the below-mentioned segments:

Global Obesity Surgery Devices Market, By Device Type

- Minimally Invasive Surgical Devices

- Non-Invasive / Implantable Devices

Global Obesity Surgery Devices Market, By Procedure Type

- Sleeve gastrectomy

- Gastric bypass

- Adjustable gastric banding

- Mini-gastric bypass

- Revision bariatric surgery

- Biliopancreatic diversion with duodenal switch

- Non-invasive bariatric procedures

Global Obesity Surgery Devices Market, By Functional Category

- Stapling devices

- Gastric bands

- Gastric balloons

- Energy-based devices

- Suturing & closure devices

- Access devices

Global Obesity Surgery Devices Market, By End User

- Hospitals

- Ambulatory Surgical centres

- Specialty bariatric clinics

- Surgical centres

Global Obesity Surgery Devices Market, By Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa

Frequently Asked Questions (FAQ)

1. What are the key technological innovations shaping the future of obesity surgery devices?

The market is witnessing rapid advancements in robotic-assisted surgery platforms, AI-integrated surgical systems, and next-generation smart stapling devices. These innovations enhance precision, reduce surgical errors, and improve patient recovery outcomes. Additionally, single-port laparoscopic systems and advanced energy-based sealing technologies are improving procedural efficiency. Continuous R&D investments by leading manufacturers are further accelerating innovation, making bariatric surgeries safer and more predictable across healthcare facilities globally.

2. How do reimbursement policies influence the adoption of obesity surgery devices?

Reimbursement frameworks play a critical role in determining patient access to bariatric procedures. In regions with strong insurance coverage, such as developed economies, higher procedure uptake is observed due to reduced out-of-pocket expenses. Conversely, limited reimbursement in developing regions restricts adoption. Expansion of public and private insurance coverage for obesity treatments is expected to significantly improve market penetration and encourage hospitals to invest in advanced surgical device technologies.

3. What role does medical tourism play in the growth of the obesity surgery devices market?

Medical tourism significantly contributes to market expansion by increasing cross-border bariatric procedures. Patients from high-cost healthcare regions often travel to countries offering affordable yet high-quality obesity surgeries. This trend boosts demand for surgical devices in destination countries and encourages healthcare facilities to upgrade their surgical infrastructure. As a result, medical tourism supports equipment utilization rates and drives investments in minimally invasive and advanced surgical technologies.

4. What challenges do manufacturers face in the obesity surgery devices market?

Manufacturers face challenges such as stringent regulatory approval processes, high product development costs, and the need for continuous technological upgrades. Ensuring device safety, durability, and clinical effectiveness requires extensive testing and compliance with global standards. Additionally, pricing pressure from healthcare providers and competition among established players limit profit margins. Supply chain disruptions and raw material cost fluctuations also create operational challenges for device manufacturers worldwide.

5. How is patient awareness influencing the demand for obesity surgery devices?

Rising awareness of obesity-related health risks such as cardiovascular diseases, diabetes, and metabolic disorders is significantly increasing patient inclination toward surgical interventions. Educational campaigns, digital health platforms, and physician consultations are improving understanding of bariatric surgery benefits. This growing awareness is encouraging early treatment adoption and expanding the patient pool eligible for surgical procedures, thereby driving sustained demand for advanced obesity surgery devices globally.

Check Licence

Choose the plan that fits you best: Single User, Multi-User, or Enterprise solutions tailored for your needs.

We Have You Covered

- 24/7 Analyst Support

- Clients Across the Globe

- Tailored Insights

- Technology Tracking

- Competitive Intelligence

- Custom Research

- Syndicated Market Studies

- Market Overview

- Market Segmentation

- Growth Drivers

- Market Opportunities

- Regulatory Insights

- Innovation & Sustainability

Report Details

| Scope | Global |

| Pages | 240 |

| Delivery | PDF & Excel via Email |

| Language | English |

| Release | Apr 2026 |

| Access | Download from this page |