Global Passive Fire Protection Market Size 2025 - 2035

Global Passive Fire Protection Market Size, Share, and COVID-19 Impact Analysis, By Product (Cementitious Materials, Intumescent Coating, Fireproofing Cladding, Others), By Application (Oil & Gas, Construction, Industrial Plants, Warehousing, Other), and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2025 - 2035

CAGR

7.9%

REVENUE 2023

USD Billion 4.32

FORECAST 2031

USD Billion 7.94

REPORT COVERAGE

Global

Global Passive Fire Protection Market Overview

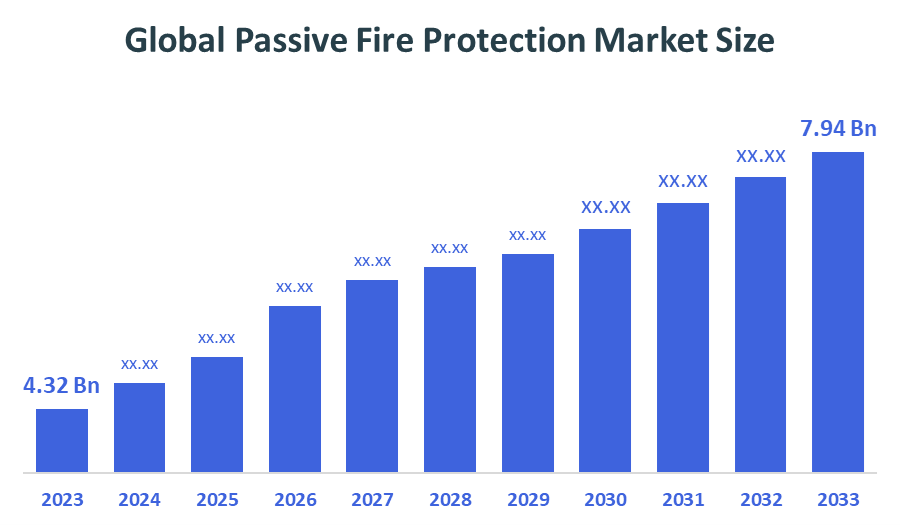

- The global passive fire protection market was valued at approximately USD 4.32 billion in 2023 and is projected to reach around USD 7.94 billion by 2031, growing at a compound annual growth rate (CAGR) of 7.9% during the forecast period from 2024 to 2031.

- This growth is driven by stringent fire safety regulations, increased construction activities, and heightened awareness of fire safety standards across various industries.

Major vendors in the Global Passive Fire Protection Market

Lloyd Insulations (India) Limited, 3M, Sharpfibre Limited, Hempel A/S, The Sherwin-Williams Company, and Others.

Market Segment

This study forecasts revenue at global, regional, and country levels from 2024 to 2032. Decision Advisor has segmented the Global Passive Fire Protection Market based on the below-mentioned segments:

Global Passive Fire Protection Market, By Product:

- Cementitious Materials

- Intumescent Coatings

- Fireproofing Cladding

- Others

Global Passive Fire Protection Market, By Application:

- Oil and Gas

- Construction

- Industrial

- Transportation

- Warehousing

- Others

Global Passive Fire Protection Market, By End-User:

- Residential

- Commercial

- Industrial

Global Passive Fire Protection Market, By Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa

Check Licence

Choose the plan that fits you best: Single User, Multi-User, or Enterprise solutions tailored for your needs.

We Have You Covered

- 24/7 Analyst Support

- Clients Across the Globe

- Tailored Insights

- Technology Tracking

- Competitive Intelligence

- Custom Research

- Syndicated Market Studies

- Market Overview

- Market Segmentation

- Growth Drivers

- Market Opportunities

- Regulatory Insights

- Innovation & Sustainability

Report Details

| Scope | Global |

| Pages | 200 |

| Delivery | PDF & Excel via Email |

| Language | English |

| Release | Aug 2025 |

| Access | Download from this page |