Global PD-1 Resistant Head and Neck Cancer Market

Global PD-1 Resistant Head and Neck Cancer Market Size, Share, By Treatment Type (Chemotherapy, Radiation Therapy, Surgery, Targeted Therapy), By Cancer Type (Squamous Cell Carcinoma, Adenocarcinoma, Nasopharyngeal Carcinoma, Throat Cancer), By End User (Hospitals, Cancer Research Centers, Clinics), and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2025 ? 2035.

REPORT COVERAGE

Global

Market Snapshot

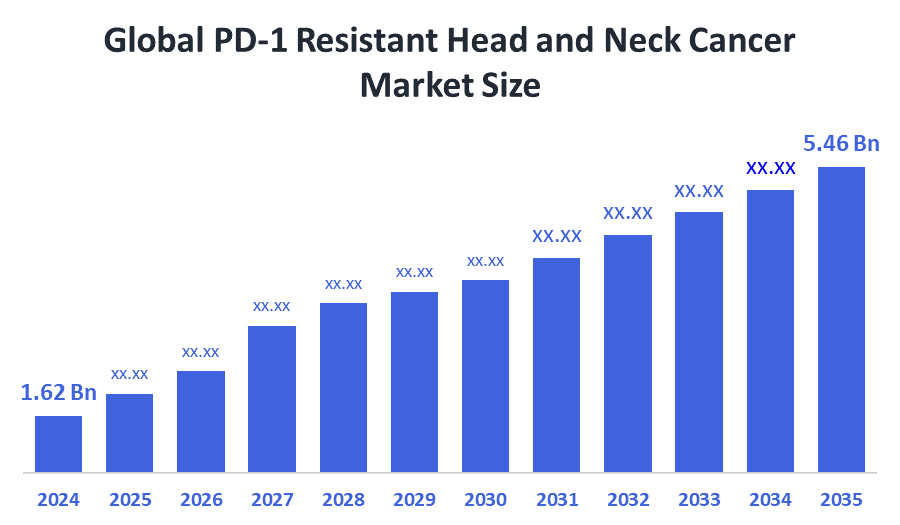

- Market Size (2025): USD 1.62 Billion

- Projected Market Size (2035): USD 5.46 Billion

- Compound Annual Growth Rate (CAGR): 12.92%

- Largest Regional Market: North America

- Fastest Growing Region: Asia-Pacific

- 3rd Largest Region: Europe

- Base Year: 2025

- Historical Period: 2021–2024

- Forecast Period: 2025–2035

According to Decision Advisors, the PD-1 Resistant Head and Neck Cancer Market Size is expected to grow from USD 1.62 billion in 2025 to USD 5.46 billion by 2035, at a CAGR of 12.92% during the forecast period 2025-2035. Fueled by the increase in HPV-related cases, strong research and development of new combinations (such as Monalizumab), and genomic profiling, high unmet need, combination therapies, rising incidence of HPV-related HNSCC, and precision medicine and biomarkers.

Market Overview/ Introduction

The PD-1 resistant head and neck cancer market encompasses the area of oncology dedicated to creating and selling treatments for patients with head and neck cancers who do not respond or who develop resistance to programmed cell death protein-1 (PD-1) inhibitors like Pembrolizumab and Nivolumab. The market's growth is propelled by the rising incidence of head and neck cancers, which sees over 900,000 new global cases annually, and the growing percentage of patients showing primary or acquired resistance to PD-1 blockade, resulting in a considerable unmet clinical need. The primary opportunity lies in combining PD-1 inhibitors with novel agents targeting immune evasion, such as anti-TIGIT antibodies and NK cell activators.

- In November 2024, CEL-SCI Corp received FDA concurrence to incorporate PD-L1 biomarker selection in Multikine studies, with a confirmatory trial planned for 2025, however, the therapy targets newly diagnosed head and neck cancer patients.

- Petosemtamab, an EGFRxLGR5 bispecific antibody, is being evaluated in the Phase III LiGeR-HN2 trial for recurrent/metastatic HNSCC in the second-line or later setting, demonstrating promising response rates in patients previously treated with PD-1 inhibitors.

Notable Insights: -

- North America holds the largest regional market share approximately 42% in the PD-1 resistant head and neck cancer.

- Asia Pacific is the fastest growing region in the PD-1 resistant head and neck cancer with a CAGR of approximately 22%.

- By treatment type, the target therapy segment held a dominant position with approximately 52.4% in terms of market share in 2025.

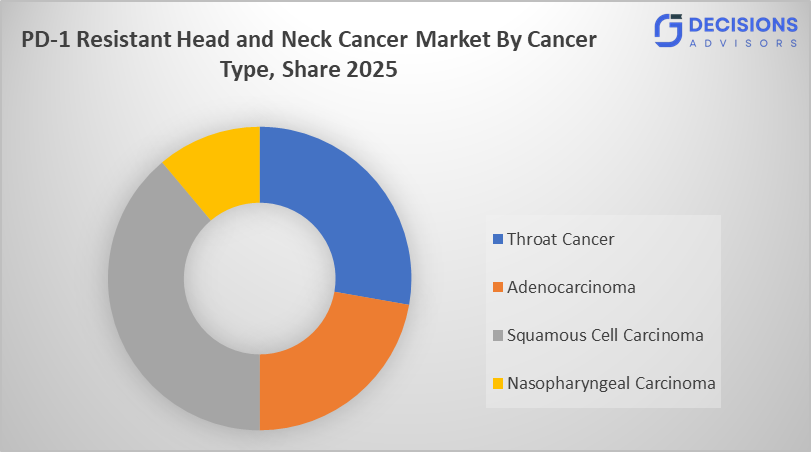

- By cancer type, squamous cell carcinoma is the dominating accounting for over 60% of the global market share in 2025.

- The compound annual growth rate of the PD-1 resistant head and neck cancer is 12.92%.

- The market is likely to achieve a valuation of USD 5.46 billion by 2035.

What is role of technology in grooming the market?

Technology is vital for shaping the PD-1 resistant head and neck cancer market, as it allows for treatment methods that are more precise, effective, and scalable. Progress in artificial intelligence (AI) and big data is enhancing resistance profiling and the identification of new drug targets, thereby speeding up the creation of next-generation treatments like bispecific antibodies and personalized vaccines. AI-driven neoantigen vaccines, for example, have shown disease-free survival rates of up to 100% in early studies, underscoring their transformative potential. Moreover, the use of genomic and biomarker testing technologies is refining patient selection and treatment personalization, leading to better outcomes in resistant cases. Technology facilitates digital clinical trials, real-world data analysis, and tele-oncology, aiding in the expansion of access, acceleration of drug development, and enhancement of overall treatment efficiency in both developed and emerging regions.

How is Recent Developments Helping the Market?

Recent developments are greatly boosting the expansion of the PD-1 resistant head and neck cancer market by enhancing treatment effectiveness and broadening therapeutic choices. Immunotherapy clinical trials, particularly those involving PD-1/PD-L1 inhibitors, have yielded significant advantages; for instance, a major worldwide investigation involving more than 700 patients revealed that combining immunotherapy with standard treatment resulted in a doubling of disease-free survival (approximately 5 years compared to 30 months). Furthermore, innovative targeted treatments like multi-action antibodies have resulted in tumor reduction or disease management in almost 75% of patients with extensive prior treatment, underscoring advancements in overcoming resistance. The development of combination therapies, biomarker-driven methods, and novel drug delivery techniques is resulting in improved patient outcomes, shorter treatment duration, and greater uptake all of which are contributing significantly to the overall growth of the market.

Market Drivers

The market is propelled by various essential elements associated with the increasing burden of disease and clinical needs that remain unmet. The rising occurrence of head and neck cancers worldwide, combined with the prevalent use of immunotherapies, has resulted in a burgeoning group of patients who develop resistance, thus generating a significant need for alternative treatments. It is important to point out that just 15–20% of patients exhibit a lasting response to immune checkpoint inhibitors, underscoring the considerable unfulfilled need for effective second-line therapies. Furthermore, the advancement of biomarker-driven diagnostics, individualized treatment approaches, and next-gen therapies like bispecific antibodies is driving innovation. The market growth is further driven by escalating R&D investments, heightened clinical trial activities, and a better comprehension of tumor immune resistance mechanisms, as stakeholders seek to improve survival outcomes and address therapy limitations.

Restrain

The head and neck cancer market resistant to PD-1 has various constraining elements, among which is the limited overall effectiveness of checkpoint inhibitors. This underscores a major unmet need. Moreover, intricate tumor microenvironments impede the efficacy of drugs, contributing to elevated rates of clinical trial failures. More than 60% of patients experience serious adverse events related to treatment, and high therapy costs combined with limited availability in developing areas hinder market expansion.

Competitive Analysis:

The report offers the appropriate analysis of the key organizations/companies involved within the PD-1 resistant head and neck cancer market, along with a comparative evaluation primarily based on their product of offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes product development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

Top Companies in PD-1 Resistant Head and Neck Cancer Market

- Merck & Co.

- Bristol-Myers Squibb

- AstraZeneca

- Pfizer

- Roche Holding AG

- Regeneron Pharmaceuticals

- Incyte Corporation

- Amgen Inc.

- Rakuten Medical

- BioNTech SE

- ALX Oncology

- RAPT Therapeutics

- Adaptimmune Therapeutics

- Cel-Sci Corporation, GSK

- Boehringer Ingelheim

- Sotio Biotech

- Exelixis

- Bicara Therapeutics

- Merus

- Adlai Nortye Biopharma

Government Initiatives

|

Country |

Key Government Initiatives |

|

UK |

The Cancer Vaccine Launch Pad (CVLP), led by NHS England in partnership with BioNTech, is a national initiative designed to accelerate patient recruitment into cancer vaccine trials, including advanced head and neck cancer studies across approximately 15 NHS hospitals. |

|

Germany |

The Society for Immunotherapy of Cancer (SITC) convened experts from academia, industry, and government to develop consensus definitions for resistance to immune checkpoint inhibitors, particularly in combination therapies, to standardize clinical trial design and improve evaluation of treatment outcomes. |

|

China |

Government and publicly funded research organizations are supporting clinical trials evaluating anti-PD-1 therapies in combination with other immunomodulatory agents, such as TIGIT inhibitors, and targeted therapies to overcome resistance, particularly in recurrent or treatment-resistant head and neck cancer settings. |

Market Segmentation

The PD-1 resistant head and neck cancer market share is classified into treatment type, cancer type, and end user

- The targeted therapy segment dominated the market in 2025, and is projected to grow at a substantial CAGR of approximately 52.4% during the forecast period.

Based on the treatment type, the PD-1 resistant head and neck cancer market is divided into chemotherapy, radiation therapy, surgery, targeted therapy. Among these, the targeted therapy segment dominated the market in 2025, and is projected to grow at a substantial CAGR of approximately 52.4% during the forecast period. Targeted therapy, including EGFR inhibitors like Cetuximab, addresses the specific molecular pathways that cause resistance to PD-1/PD-L1 inhibitors, making it crucial for patients who have failed immunotherapy.

- The squamous cell carcinoma segment accounted for the largest share in 2025, and is anticipated to grow at a significant CAGR of approximately 60% during the forecast period.

Based on the cancer type, the PD-1 resistant head and neck cancer market is divided squamous cell carcinoma, adenocarcinoma, nasopharyngeal carcinoma, throat cancer. Among these, the squamous cell carcinoma segment accounted for the largest share in 2025, and is anticipated to grow at a significant CAGR of approximately 60 % during the forecast period. It constitutes the largest systemic-therapy pool and serves as the main focus for pharmaceutical companies creating therapies to address resistance, including combination approaches involving CTLA-4, LAG-3, or ADC agents.

The hospitals segment dominated the market at a CAGR of approximately 57.85% in 2025, and is projected to grow at a substantial CAGR during the forecast period.

Based on the end user, the PD-1 resistant head and neck cancer market is divided into hospitals, cancer research centers, clinics. Among these, the hospitals segment dominated the market at a CAGR of approximately 57.85% in 2025, and is projected to grow at a substantial CAGR during the forecast period. Hospitals offer advanced facilities for complex cancer diagnosis and treatment, including specialized oncology departments, which are crucial for managing PD-1 resistant cases that often necessitate intravenous chemotherapy, combination therapies, or advanced imaging.

Strategies to Implement for Growth of the Market in Non-Leading Regions

Growth of the PD-1 resistant head and neck cancer market in non-leading regions such as Latin America, and Middle East and Africa can be accelerated through cost-effective pricing models, expansion of regional clinical trials, and adoption of combination immunotherapies. Improving access to biomarker testing and strengthening local manufacturing can further enhance treatment availability, especially as over 60% of global head and neck cancer cases occur in developing regions. Additionally, increasing awareness, early diagnosis programs, and public private partnerships can significantly expand the eligible patient pool, while digital health and tele-oncology solutions help bridge infrastructure gaps and improve overall treatment reach.

Regional Segment Analysis of the PD-1 resistant head and neck cancer market

- North America (U.S., Canada, Mexico)

- Europe (Germany, France, U.K., Italy, Spain, Rest of Europe)

- Asia-Pacific (China, Japan, India, Rest of APAC)

- South America (Brazil and the Rest of South America)

- The Middle East and Africa (UAE, South Africa, Rest of MEA)

North America is anticipated to hold the largest share of the PD-1 resistant head and neck cancer market over the predicted timeframe. North America is anticipated to hold the largest share of the PD-1–resistant head and neck cancer market, accounting for approximately 42% during the forecast period, driven by the strong presence of leading pharmaceutical companies, high adoption of advanced immunotherapies, robust clinical trial activity, favorable reimbursement policies, and well-established healthcare infrastructure in the United States and Canada, along with increasing prevalence of head and neck cancers, early access to novel therapies, strong regulatory support, and rising investments in oncology research and precision medicine.

Asia Pacific is expected to grow at a rapid CAGR in the PD-1 resistant head and neck cancer market during the forecast period. Asia Pacific is expected to grow at a rapid CAGR of approximately 22% in the PD-1–resistant head and neck cancer market during the forecast period, driven by rising cancer incidence in countries like China and India, improving healthcare infrastructure, increasing adoption of advanced immunotherapies, expanding clinical trials, rising government healthcare investments, growing medical tourism, enhanced early diagnosis rates, and the presence of emerging local biopharmaceutical companies accelerating treatment access.

Europe is the 3rd largest region to grow in the PD-1 resistant head and neck cancer market during the region. Europe is the third-largest region in the PD-1–resistant head and neck cancer market, accounting for approximately 28% share during the forecast period, driven by strong healthcare systems, increasing adoption of immunotherapies, rising cancer incidence, supportive government funding, and active clinical research across countries like Germany, France.

Future Market Trends in PD-1 Resistant Head and Neck Cancer: -

- Rise of Combination Therapies:

To overcome resistance, the market is shifting toward combining immunotherapy with other agents. Key assets include novel combinations, such as potential inhibitors that target different stages of immune exhaustion or tumor angiogenesis.

- Targeted Precision Medicine:

Development is moving away from a one-size-fits-all approach toward personalized medicine, specifically identifying biomarkers that indicate when a patient will fail to respond to PD-1 inhibitors.

Recent Development

- In February 2026, the FDA granted Breakthrough Therapy Designation to subcutaneous amivantamab and hyaluronidase-lpuj (Rybrevant Faspro) as monotherapy for HPV-unrelated recurrent or metastatic head and neck cancer patients who progressed after platinum-based chemotherapy and PD-1/PD-L1 inhibitors.

- In May 2023, Monalizumab (AstraZeneca/Innate Pharma), a first-in-class NKG2A inhibitor, was evaluated in the Phase III INTERLINK-1 trial (NCT04590963) for PD-1–resistant head and neck cancer; however, the study was discontinued after failing to demonstrate overall survival benefit in treated patients.

Market Segment

This study forecasts revenue at global, regional, and country levels from 2020 to 2035. Decision Advisor has segmented the PD-1 resistant head and neck cancer market based on the below-mentioned segments:

PD-1 Resistant Head and Neck Cancer Market, By Treatment Type

- Chemotherapy

- Radiation Therapy

- Surgery

- Targeted Therapy

PD-1 Resistant Head and Neck Cancer Market, By cancer Type

- Squamous Cell Carcinoma

- Adenocarcinoma

- Nasopharyngeal Carcinoma

- Throat Cancer

PD-1 Resistant Head and Neck Cancer Market, By End User

- Hospitals

- Cancer Research Centers

- Clinics

PD-1 Resistant Head and Neck Cancer Market, By Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa

Frequently Asked Questions (FAQ)

1. What are the primary biological mechanisms driving resistance to PD-1 inhibitors in head and neck cancers?

Resistance to PD-1 inhibitors is largely attributed to complex tumor microenvironment factors, including immune evasion via T-cell exhaustion, upregulation of alternative immune checkpoints (e.g., TIGIT, LAG-3), loss of antigen presentation, and immunosuppressive cytokine activity. These mechanisms limit the efficacy of monotherapy, necessitating multi-targeted therapeutic strategies.

2. How are combination immunotherapy approaches reshaping treatment paradigms in PD-1 resistant cases?

Combination therapies integrating PD-1/PD-L1 inhibitors with agents targeting CTLA-4, VEGF, or NK cell pathways are significantly improving response rates. These approaches enhance immune activation, overcome resistance pathways, and are increasingly becoming the cornerstone of next-generation oncology treatment frameworks.

3. What role do biomarker-driven strategies play in optimizing treatment outcomes?

Biomarker-based approaches, including PD-L1 expression, tumor mutational burden (TMB), and genomic profiling, are critical in identifying patients likely to benefit from specific therapies. This precision medicine approach reduces trial-and-error treatment and enhances clinical efficacy while optimizing healthcare resource utilization.

4. How is the clinical trial landscape evolving for PD-1 resistant head and neck cancer therapies?

The clinical trial ecosystem is rapidly expanding, with a focus on adaptive trial designs, global patient recruitment, and evaluation of novel modalities such as bispecific antibodies and cell therapies. Increased participation from emerging markets is also improving data diversity and accelerating regulatory approvals.

5. What are the key barriers to commercialization of novel therapies in this market?

Major challenges include high development costs, stringent regulatory requirements, limited long-term efficacy data, and reimbursement complexities. Additionally, variability in healthcare infrastructure across regions affects the scalability and accessibility of advanced treatments.

Check Licence

Choose the plan that fits you best: Single User, Multi-User, or Enterprise solutions tailored for your needs.

We Have You Covered

- 24/7 Analyst Support

- Clients Across the Globe

- Tailored Insights

- Technology Tracking

- Competitive Intelligence

- Custom Research

- Syndicated Market Studies

- Market Overview

- Market Segmentation

- Growth Drivers

- Market Opportunities

- Regulatory Insights

- Innovation & Sustainability

Report Details

| Scope | Global |

| Pages | 210 |

| Delivery | PDF & Excel via Email |

| Language | English |

| Release | Apr 2026 |

| Access | Download from this page |