Global Prostate Cancer Market

Global Prostate Cancer Market Size, Share, and COVID-19 Impact Analysis, By Drug Class (Hormonal ADT, AR-Directed Therapies, Cytotoxic Agents, Bone Metastases, Therapeutic Vaccines, Parp Inhibitors, Kinase Inhibitors, and PSMA-Targeted Radioligands), By Treatment (Hormonal Therapy, Chemotherapy, Immunotherapy, Targeted Therapy, and Others), and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2025 - 2035

CAGR

9.45%

REVENUE 2025

USD Billion 17.35

FORECAST 2035

USD Billion 47.26

REPORT COVERAGE

Global

Global Prostate Cancer Market Size Insights Forecasts to 2035

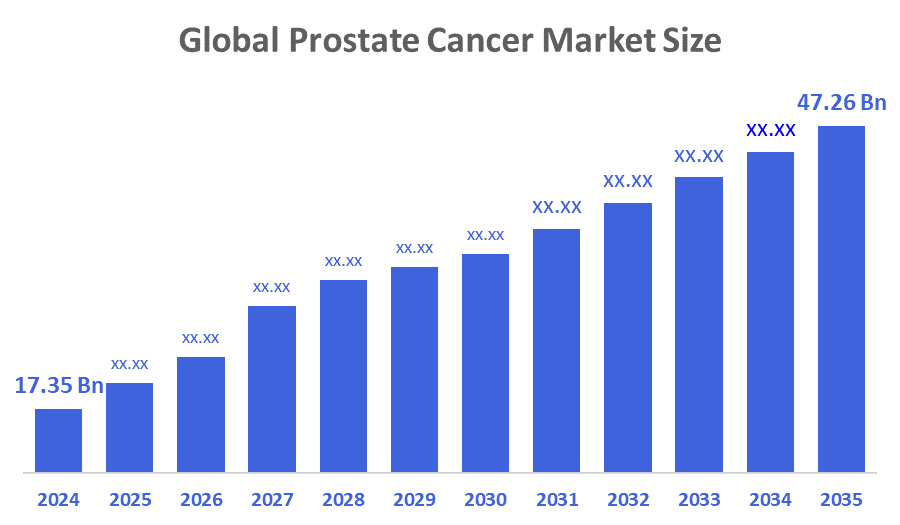

- The Global Prostate Cancer Market Size Was Estimated at USD 17.35 Billion in 2024

- The Market Size is Expected to Grow at a CAGR of around 9.54% from 2025 to 2035

- The Worldwide Prostate Cancer Market Size is Expected to Reach USD 47.26 Billion by 2035

- Europe is expected to Grow the fastest during the forecast period.

According to a Research Report Published by Decisions Advisors and Consulting, The Global Prostate Cancer Market Size was worth around USD 17.35 Billion in 2024 and is predicted to Grow to around USD 47.26 Billion by 2035 with a compound annual growth rate (CAGR) of 9.54% from 2025 to 2035. The increasing number of prostate cancer cases, improvements in screening and diagnostic techniques, and government programs promoting novel treatments are some of the causes driving this development. Modern technologies like computational biology and bioinformatics are helping to create new treatments. Proteome profiling and genome sequencing are two methods that market participants are using for developing better therapies.

Market Overview

The prostate cancer market includes the worldwide network of diagnostics, treatments, and supportive care options focused on preventing, identifying, and managing prostate cancer. The market is influenced by results from clinical trials, regulatory authorisations, reimbursement systems, and the acceptance of new treatment methods. It encompasses research institutions, hospitals, speciality clinics, and biopharmaceutical firms, with expansion fueled by the increasing prevalence of diseases, ageing demographics, and advancements in precision medicine. Prostate cancer claims the lives of one out of every forty-one men, second only to lung cancer. Although prostate cancer is a serious illness, the majority of men who receive a diagnosis do not pass away from it. Black males who are not Hispanic and older men are more likely to develop prostate cancer. The average age at which males receive a prostate cancer diagnosis is 66. The prostate cancer therapeutic market is influenced by the increasing incidence of cancer, the use of new screening methods and diagnostic technologies, and government initiatives for innovative prostate cancer treatments. Therapeutic adoption is anticipated to rise in tandem with the use of diagnostic technology. Bioinformatics and computational biology technologies are used in recent therapeutic advances to assist in obtaining the best possible care.

The National Cancer Institute (NCI) has awarded Weill Cornell Medicine a projected $4 million grant to fund a clinical trial testing advanced imaging for prostate cancer. The study will evaluate whether PSMA-PET CT scans can reduce the need for invasive biopsies during active surveillance.

The University of Queensland (UQ) is joining a $18 million national initiative led by radiopharmaceutical company AdvanCell to develop targeted alpha therapies for prostate cancer. UQ researchers will contribute their expertise in imaging and diagnostics to help deliver highly potent radiation directly to cancer cells while sparing healthy tissue.

Report Coverage

This research report categorises the prostate cancer market based on various segments and regions, forecasts revenue growth, and analyzes trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the prostate cancer market. Recent market developments and competitive strategies, such as expansion, product launch, development, partnership, merger, and acquisition, have been included to draw the competitive landscape in the market. The report strategically identifies and profiles the key market players and analyzes their core competencies in each sub-segment of the prostate cancer market.

Driving Factors

The need for efficient treatment solutions has increased due to the rising incidence of prostate cancer, especially in older populations. Patient outcomes have greatly improved thanks to advancements in targeted medicines, such as androgen receptor inhibitors and radioligand therapy. Additionally, early detection rates have increased due to the incorporation of artificial intelligence into diagnostic processes. Government programs and financing for cancer research support market growth even more. Another important development driver is the move toward personalised medicine, which emphasises therapies based on each patient's unique genetic profile. The market for prostate cancer is expected to grow significantly due to advances in technology and rising healthcare spending. Leading companies in the prostate cancer industry are actively working to expand their product lines and create novel treatments.

The UK launched TRANSFORM, a £42 million landmark prostate cancer screening trial, the largest of its kind in a generation. It will recruit up to test new screening methods, aiming to pave the way for a national programme that could save thousands of lives.

Restraining Factors

The prostate cancer market is hampered by high treatment costs, reimbursement barriers, and restricted access in developing areas, despite considerable innovation momentum. Patient compliance is impacted by safety concerns, side effects, and regulatory delays, which hinder the implementation of novel therapies. PSMA PET imaging infrastructure deficiencies and pricing pressure from generics and biosimilars further limit market growth.

Market Segmentation

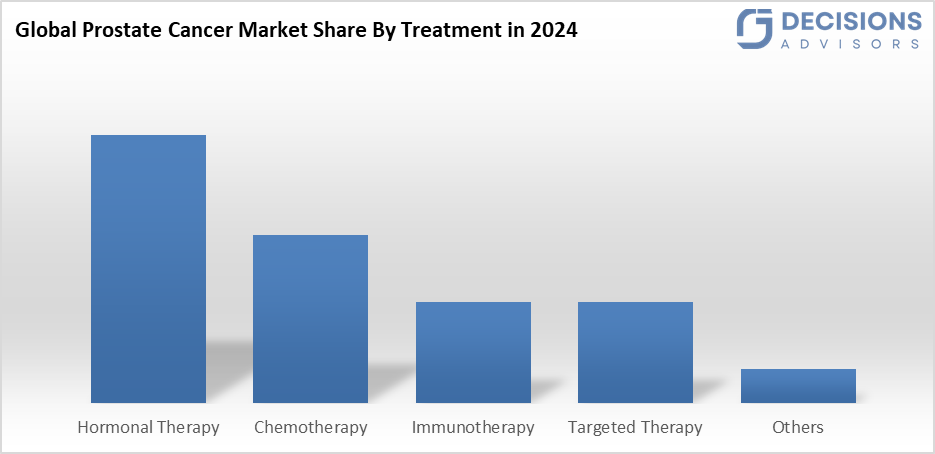

The prostate cancer market share is classified into drug class and treatment.

- The AR-directed therapies segment accounted for the largest share in 2024 and is anticipated to grow at a significant CAGR during the forecast period.

Based on the drug class, the prostate cancer market is segmented into hormonal ADT, AR-directed therapies, cytotoxic agents, bone metastases, therapeutic vaccines, PARP inhibitors, kinase inhibitors, and PSMA-targeted radioligands. Among these, the AR-directed therapies segment accounted for the largest share in 2024 and is anticipated to grow at a significant CAGR during the forecast period. This is due to drugs such as apalutamide and enzalutamide being the top-selling medications in the prostate cancer market. The segment growth will be driven by the increasing use of apalutamide and enzalutamide in already approved situations as well as the expected label expansions in hormone-sensitive settings.

- The hormonal therapy segment dominated the market in 2024 and is anticipated to grow at a significant CAGR during the forecast period.

Based on the treatment, the prostate cancer market is divided into hormonal therapy, chemotherapy, immunotherapy, targeted therapy, and others. Among these, the hormonal therapy segment dominated the market in 2024 and is anticipated to grow at a significant CAGR during the forecast period. This dominance has been associated with the ability of LHRH agonists, antagonists, and anti-androgens to slow the progression of the disease. The use of hormonal medications in first-line treatment regimens has strengthened the preference for them. The segment's dominance in clinical oncology practice has been further fueled by treatment uniformity and patient tolerability.

Regional Segment Analysis of the Prostate Cancer Market

- North America (U.S., Canada, Mexico)

- Europe (Germany, France, U.K., Italy, Spain, Rest of Europe)

- Asia-Pacific (China, Japan, India, Rest of APAC)

- South America (Brazil and the Rest of South America)

- The Middle East and Africa (UAE, South Africa, Rest of MEA)

Asia Pacific is anticipated to hold the largest share of the prostate cancer market over the predicted timeframe.

Asia Pacific is anticipated to hold the largest share of the prostate cancer market over the predicted timeframe. Cost-effective therapy, customised medications, technical developments, a wide range of treatment options, and the increasing prevalence of prostate cancer are all contributing factors to the market's growth. Japan's excellent healthcare institutions and ageing population make it a major player in the Asia-Pacific market. One of the top three cancers that affects men is prostate cancer. This is due to greater detection from screening programs around the country; its incidence is increasing. Japan is anticipated to sustain a strong growth rate over the next years due to expanding partnerships with foreign biotech firms and the broader use of precision diagnostics.

Europe is expected to grow at a rapid CAGR in the prostate cancer market during the forecast period. This is supported by an established oncology care infrastructure and a significant illness load. Growth in the area has been fueled by a number of national screening initiatives, universal healthcare, and easy access to cutting-edge diagnostics. Furthermore, the quick acceptance of innovation in these important markets is made possible by good reimbursement policies in major markets like the UK, Germany, and France, as well as regulatory harmonisation through the European Medicines Agency (EMA). Its sophisticated healthcare infrastructure and strong reimbursement rules under its statutory insurance system, Germany is a significant European hub for prostate cancer treatment and diagnostics. The nation's wide screening coverage of PSA testing results in high rates of early detection and prompt treatment.

Competitive Analysis:

The report offers the appropriate analysis of the key organizations/companies involved within the prostate cancer market, along with a comparative evaluation primarily based on their product offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes product development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

List of Key Companies

- Astellas Pharma Inc.

- AstraZeneca

- Bausch Health Companies Inc.

- Bayer AG

- Bristol-Myers Squibb Company

- Clovis Oncology, Inc.

- Eli Lilly and Company

- Exelixis, Inc.

- Ferring Pharmaceuticals Inc.

- GlaxoSmithKline Plc

- Ipsen Pharma

- Johnson & Johnson Services, Inc.

- Pfizer Inc.

- Sanofi

- Others

Key Target Audience

- Market Players

- Investors

- End-users

- Government Authorities

- Consulting and Research Firm

- Venture capitalists

- Value-Added Resellers (VARs)

Recent Development

- In December 2025, A major international trial for prostate cancer treatment was launched at the Royal Free London. It was a test of a robotic, AI-driven therapy called Aquablation that could offer a less invasive alternative to traditional surgery.

- In October 2025, Pfizer Inc. and Astellas Pharma U.S. Inc. released the final overall survival (OS) data from the Phase 3 EMBARK trial, which assessed XTANDI (enzalutamide) in combination with leuprolide and as monotherapy. There were no additional safety signals found, and XTANDI's safety profile matched that of the initial EMBARK analysis.

- In June 2025, Novartis announced that Pluvicto (lutetium Lu 177 vipivotide tetraxetan). It is achieved a statistically significant and clinically meaningful improvement in radiographic progression-free survival (rPFS) in patients with PSMA-positive metastatic hormone-sensitive prostate cancer (mHSPC), from the Phase 3 PSMAddition trial.

Market Segment

This study forecasts revenue at global, regional, and country levels from 2020 to 2035. Decisions Advisors has segmented the prostate cancer market based on the below-mentioned segments:

Global Prostate Cancer Market, By Drug Class

- Hormonal ADT

- AR-Directed Therapies

- Cytotoxic Agents

- Bone Metastases

- Therapeutic Vaccines

- Parp Inhibitors

- Kinase Inhibitors

- PSMA-Targeted Radioligands

Global Prostate Cancer Market, By Treatment

- Hormonal Therapy

- Chemotherapy

- Immunotherapy

- Targeted Therapy

- Others

Global Prostate Cancer Market, By Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa

Frequently Asked Questions (FAQ)

- What is the projected size and growth rate of the global prostate cancer market?

The market was valued at USD 17.35 billion in 2024 and is expected to reach USD 47.26 billion by 2035, growing at a CAGR of 9.54% from 2025 to 2035.

- What are the main segments of the prostate cancer market by drug class?

The market segments by drug class include: Hormonal ADT, AR-Directed Therapies, Cytotoxic Agents, Bone Metastases, Therapeutic Vaccines, PARP Inhibitors, Kinase Inhibitors, and PSMA-Targeted Radioligands. AR-Directed Therapies held the largest share in 2024 and are poised for significant growth, driven by drugs like apalutamide and enzalutamide.

- Which treatment segment dominates the market?

Hormonal Therapy dominated in 2024 and is expected to grow at a significant CAGR. It includes LHRH agonists, antagonists, and anti-androgens, favoured for slowing disease progression and strong patient tolerability in first-line regimens.

- What drives growth in the prostate cancer market?

Key drivers include rising incidence (especially in older populations), advancements in targeted therapies like AR inhibitors and radioligand therapy, AI-enhanced diagnostics for early detection, government funding for research, and a shift toward personalised medicine.

- What are the main challenges or restraining factors?

High treatment costs, reimbursement barriers in developing regions, side effects impacting compliance, regulatory delays, and infrastructure gaps for technologies like PSMA PET imaging hinder growth.

- Which region holds the largest market share, and which is growing fastest?

Asia-Pacific is anticipated to hold the largest share, fueled by cost-effective therapies, rising prevalence, and strong markets like Japan. Europe is expected to grow at the fastest CAGR, supported by advanced infrastructure, screening programs, and favourable reimbursements in countries like Germany, the UK, and France.

- What does the report cover in terms of data and analysis?

It provides historical data (2020-2023), base year 2024 forecasts to 2035, segment analysis, regional breakdowns, growth drivers, challenges, competitive landscapes, and recent news like partnerships and trials.

- Introduction

- Objectives of the Study

- Market Definition

- Research Scope

- Research Methodology and Assumptions

- Executive Summary

- Premium Insights

- Porter’s Five Forces Analysis

- Value Chain Analysis

- Top Investment Pockets

- Market Attractiveness Analysis By Drug Class

- Market Attractiveness Analysis By Treatment

- Market Attractiveness Analysis By Region

- Industry Trends

- Market Dynamics

- Market Evaluation

- Drivers

- Modern technologies like computational biology and bioinformatics

- Restraints

- High treatment costs, reimbursement barriers, and restricted access in developing areas

- Opportunities

- The increasing number of prostate cancer cases, improvements in screening and diagnostic techniques, and government programs

- Challenges

- Patient compliance is impacted by safety concerns, side effects, and regulatory delays

- Global Prostate Cancer Market Analysis and Projection, By Drug Class

- Segment Overview

- Hormonal ADT

- AR-Directed Therapies

- Cytotoxic Agents

- Bone Metastases

- Therapeutic Vaccines

- Parp Inhibitors

- Kinase Inhibitors

- PSMA-Targeted Radioligands

- Global Prostate Cancer Market Analysis and Projection, By Treatment

- Segment Overview

- Hormonal Therapy

- Chemotherapy

- Immunotherapy

- Targeted Therapy

- Others

- Global Prostate Cancer Market Analysis and Projection, By Regional Analysis

- Segment Overview

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Asia-Pacific

- Japan

- China

- India

- South America

- Brazil

- Middle East and Africa

- UAE

- South Africa

- Global Prostate Cancer Market-Competitive Landscape

- Overview

- Market Share of Key Players in the Prostate Cancer Market

- Global Company Market Share

- North America Company Market Share

- Europe Company Market Share

- APAC Company Market Share

- Competitive Situations and Trends

- Coverage Launches and Developments

- Partnerships, Collaborations, and Agreements

- Mergers & Acquisitions

- Expansions

- Company Profiles

- Astellas Pharma Inc

- Business Overview

- Company Snapshot

- Company Market Share Analysis

- Company Coverage Portfolio

- Recent Developments

- SWOT Analysis

- AstraZeneca

- Business Overview

- Company Snapshot

- Company Market Share Analysis

- Company Coverage Portfolio

- Recent Developments

- SWOT Analysis

- Bausch Health Companies Inc.

- Business Overview

- Company Snapshot

- Company Market Share Analysis

- Company Coverage Portfolio

- Recent Developments

- SWOT Analysis

- Bayer AG

- Business Overview

- Company Snapshot

- Company Market Share Analysis

- Company Coverage Portfolio

- Recent Developments

- SWOT Analysis

- Bristol-Myers Squibb Company

- Business Overview

- Company Snapshot

- Company Market Share Analysis

- Company Coverage Portfolio

- Recent Developments

- SWOT Analysis

- Clovis Oncology, Inc.

- Business Overview

- Company Snapshot

- Company Market Share Analysis

- Company Coverage Portfolio

- Recent Developments

- SWOT Analysis

- Eli Lilly and Company

- Business Overview

- Company Snapshot

- Company Market Share Analysis

- Company Coverage Portfolio

- Recent Developments

- SWOT Analysis

- Exelixis, Inc.

- Business Overview

- Company Snapshot

- Company Market Share Analysis

- Company Coverage Portfolio

- Recent Developments

- SWOT Analysis

- Ferring Pharmaceuticals Inc.

- Business Overview

- Company Snapshot

- Company Market Share Analysis

- Company Coverage Portfolio

- Recent Developments

- SWOT Analysis

- GlaxoSmithKline Plc

- Business Overview

- Company Snapshot

- Company Market Share Analysis

- Company Coverage Portfolio

- Recent Developments

- SWOT Analysis

- Ipsen Pharma

- Business Overview

- Company Snapshot

- Company Market Share Analysis

- Company Coverage Portfolio

- Recent Developments

- SWOT Analysis

- Johnson & Johnson Services, Inc.

- Business Overview

- Company Snapshot

- Company Market Share Analysis

- Company Coverage Portfolio

- Recent Developments

- SWOT Analysis

- Pfizer Inc.

- Business Overview

- Company Snapshot

- Company Market Share Analysis

- Company Coverage Portfolio

- Recent Developments

- SWOT Analysis

- Sanofi

- Business Overview

- Company Snapshot

- Company Market Share Analysis

- Company Coverage Portfolio

- Recent Developments

- SWOT Analysis

- Others

- Business Overview

- Company Snapshot

- Company Market Share Analysis

- Company Coverage Portfolio

- Recent Developments

- SWOT Analysis

- Astellas Pharma Inc

List of Table

- Global Prostate Cancer Market, By Drug Class, 2024-2035(USD Billion)

- Global Hormonal ADT, Prostate Cancer Market, By Region, 2024-2035(USD Billion)

- Global AR-Directed Therapies, Prostate Cancer Market, By Region, 2024-2035(USD Billion)

- Global Cytotoxic Agents, Prostate Cancer Market, By Region, 2024-2035(USD Billion)

- Global Bone Metastases, Prostate Cancer Market, By Region, 2024-2035(USD Billion)

- Global Therapeutic Vaccines, Prostate Cancer Market, By Region, 2024-2035(USD Billion)

- Global PARP Inhibitors, Prostate Cancer Market, By Region, 2024-2035(USD Billion)

- Global Kinase Inhibitors, Prostate Cancer Market, By Region, 2024-2035(USD Billion)

- Global PSMA-Targeted Radioligands, Prostate Cancer Market, By Region, 2024-2035(USD Billion)

- Global Prostate Cancer Market, By Treatment, 2024-2035(USD Billion)

- Global Hormonal Therapy, Prostate Cancer Market, By Region, 2024-2035(USD Billion)

- Global Chemotherapy, Prostate Cancer Market, By Region, 2024-2035(USD Billion)

- Global Immunotherapy, Prostate Cancer Market, By Region, 2024-2035(USD Billion)

- Global Targeted Therapy, Prostate Cancer Market, By Region, 2024-2035(USD Billion)

- Global Others, Prostate Cancer Market, By Region, 2024-2035(USD Billion)

- North America Prostate Cancer Market, By Drug Class, 2024-2035(USD Billion)

- North America Prostate Cancer Market, By Treatment, 2024-2035(USD Billion)

- U.S. Prostate Cancer Market, By Drug Class, 2024-2035(USD Billion)

- U.S. Prostate Cancer Market, By Treatment, 2024-2035(USD Billion)

- Canada Prostate Cancer Market, By Drug Class, 2024-2035(USD Billion)

- Canada Prostate Cancer Market, By Treatment, 2024-2035(USD Billion)

- Mexico Prostate Cancer Market, By Drug Class, 2024-2035(USD Billion)

- Mexico Prostate Cancer Market, By Treatment, 2024-2035(USD Billion)

- Europe Prostate Cancer Market, By Drug Class, 2024-2035(USD Billion)

- Europe Prostate Cancer Market, By Treatment, 2024-2035(USD Billion)

- Germany Prostate Cancer Market, By Drug Class, 2024-2035(USD Billion)

- Germany Prostate Cancer Market, By Treatment, 2024-2035(USD Billion)

- France Prostate Cancer Market, By Drug Class, 2024-2035(USD Billion)

- France Prostate Cancer Market, By Treatment, 2024-2035(USD Billion)

- U.K. Prostate Cancer Market, By Drug Class, 2024-2035(USD Billion)

- U.K. Prostate Cancer Market, By Treatment, 2024-2035(USD Billion)

- Italy Prostate Cancer Market, By Drug Class, 2024-2035(USD Billion)

- Italy Prostate Cancer Market, By Treatment, 2024-2035(USD Billion)

- Spain Prostate Cancer Market, By Drug Class, 2024-2035(USD Billion)

- Spain Prostate Cancer Market, By Treatment, 2024-2035(USD Billion)

- Asia Pacific Prostate Cancer Market, By Drug Class, 2024-2035(USD Billion)

- Asia Pacific Prostate Cancer Market, By Treatment, 2024-2035(USD Billion)

- Japan Prostate Cancer Market, By Drug Class, 2024-2035(USD Billion)

- Japan Prostate Cancer Market, By Treatment, 2024-2035(USD Billion)

- China Prostate Cancer Market, By Drug Class, 2024-2035(USD Billion)

- China Prostate Cancer Market, By Treatment, 2024-2035(USD Billion)

- India Prostate Cancer Market, By Drug Class, 2024-2035(USD Billion)

- India Prostate Cancer Market, By Treatment, 2024-2035(USD Billion)

- South America Prostate Cancer Market, By Drug Class, 2024-2035(USD Billion)

- South America Prostate Cancer Market, By Treatment, 2024-2035(USD Billion)

- Brazil Prostate Cancer Market, By Drug Class, 2024-2035(USD Billion)

- Brazil Prostate Cancer Market, By Treatment, 2024-2035(USD Billion)

- The Middle East and Africa Prostate Cancer Market, By Drug Class, 2024-2035(USD Billion)

- The Middle East and Africa Prostate Cancer Market, By Treatment, 2024-2035(USD Billion)

- UAE Prostate Cancer Market, By Drug Class, 2024-2035(USD Billion)

- UAE Prostate Cancer Market, By Treatment, 2024-2035(USD Billion)

- South Africa Prostate Cancer Market, By Drug Class, 2024-2035(USD Billion)

- South Africa Prostate Cancer Market, By Treatment, 2024-2035(USD Billion)

List of Figures

- Global Prostate Cancer Market Segmentation

- Prostate Cancer Market: Research Methodology

- Market Size Estimation Methodology: Bottom-Up Approach

- Market Size Estimation Methodology: Top-down Approach

- Data Triangulation

- Porter’s Five Forces Analysis

- Value Chain Analysis

- Top investment pocket in the Prostate Cancer Market

- Top Winning Strategies, 2024-2035

- Top Winning Strategies, By Development, 2024-2035(%)

- Top Winning Strategies, By Company, 2024-2035

- Moderate Bargaining power of Buyers

- Moderate Bargaining power of Suppliers

- Moderate Bargaining power of New Entrants

- Low threat of Substitution

- High Competitive Rivalry

- Top Player Positioning, 2024

- Market Share Analysis, 2024

- Restraint and Drivers: Prostate Cancer Market

- Prostate Cancer Market Segmentation, By Drug Class

- Prostate Cancer Market For Hormonal ADT, By Region, 2024-2035 ($ Billion)

- Prostate Cancer Market For AR-Directed Therapies, By Region, 2024-2035 ($ Billion)

- Prostate Cancer Market For Cytotoxic Agents, By Region, 2024-2035 ($ Billion)

- Prostate Cancer Market For Bone Metastases, By Region, 2024-2035 ($ Billion)

- Prostate Cancer Market For Therapeutic Vaccines, By Region, 2024-2035 ($ Billion)

- Prostate Cancer Market For Parp Inhibitors, By Region, 2024-2035 ($ Billion)

- Prostate Cancer Market For Kinase Inhibitors, By Region, 2024-2035 ($ Billion)

- Prostate Cancer Market For PSMA-Targeted Radioligands, By Region, 2024-2035 ($ Billion)

- Prostate Cancer Market Segmentation, By Treatment

- Prostate Cancer Market For Hormonal Therapy, By Region, 2024-2035 ($ Billion)

- Prostate Cancer Market For Chemotherapy, By Region, 2024-2035 ($ Billion)

- Prostate Cancer Market For Immunotherapy, By Region, 2024-2035 ($ Billion)

- Prostate Cancer Market For Targeted Therapy, By Region, 2024-2035 ($ Billion)

- Prostate Cancer Market For Others, By Region, 2024-2035 ($ Billion)

- Astellas Pharma Inc: Net Sales, 2024-2035 ($ Billion)

- Astellas Pharma Inc: Revenue Share, By Segment, 2024 (%)

- Astellas Pharma Inc: Revenue Share, By Region, 2024 (%)

- AstraZeneca: Net Sales, 2024-2035 ($ Billion)

- AstraZeneca: Revenue Share, By Segment, 2024 (%)

- AstraZeneca: Revenue Share, By Region, 2024 (%)

- Bausch Health Companies Inc.: Net Sales, 2024-2035 ($ Billion)

- Bausch Health Companies Inc.: Revenue Share, By Segment, 2024 (%)

- Bausch Health Companies Inc.: Revenue Share, By Region, 2024 (%)

- Bayer AG: Net Sales, 2024-2035 ($ Billion)

- Bayer AG: Revenue Share, By Segment, 2024 (%)

- Bayer AG: Revenue Share, By Region, 2024 (%)

- Bristol-Myers Squibb Company: Net Sales, 2024-2035 ($ Billion)

- Bristol-Myers Squibb Company: Revenue Share, By Segment, 2024 (%)

- Bristol-Myers Squibb Company: Revenue Share, By Region, 2024 (%)

- Clovis Oncology, Inc.: Net Sales, 2024-2035 ($ Billion)

- Clovis Oncology, Inc.: Revenue Share, By Segment, 2024 (%)

- Clovis Oncology, Inc.: Revenue Share, By Region, 2024 (%)

- Eli Lilly and Company: Net Sales, 2024-2035 ($ Billion)

- Eli Lilly and Company: Revenue Share, By Segment, 2024 (%)

- Eli Lilly and Company: Revenue Share, By Region, 2024 (%)

- Exelixis, Inc.: Net Sales, 2024-2035 ($ Billion)

- Exelixis, Inc.: Revenue Share, By Segment, 2024 (%)

- Exelixis, Inc.: Revenue Share, By Region, 2024 (%)

- Ferring Pharmaceuticals Inc: Net Sales, 2024-2035 ($ Billion)

- Ferring Pharmaceuticals Inc: Revenue Share, By Segment, 2024 (%)

- Ferring Pharmaceuticals Inc: Revenue Share, By Region, 2024 (%)

- GlaxoSmithKline Plc: Net Sales, 2024-2035 ($ Billion)

- GlaxoSmithKline Plc: Revenue Share, By Segment, 2024 (%)

- GlaxoSmithKline Plc: Revenue Share, By Region, 2024 (%)

- Ipsen Pharma: Net Sales, 2024-2035 ($ Billion)

- Ipsen Pharma: Revenue Share, By Segment, 2024 (%)

- Ipsen Pharma: Revenue Share, By Region, 2024 (%)

- Johnson & Johnson Services, Inc.: Net Sales, 2024-2035 ($ Billion)

- Johnson & Johnson Services, Inc.: Revenue Share, By Segment, 2024 (%)

- Johnson & Johnson Services, Inc.: Revenue Share, By Region, 2024 (%)

- Pfizer Inc.: Net Sales, 2024-2035 ($ Billion)

- Pfizer Inc.: Revenue Share, By Segment, 2024 (%)

- Pfizer Inc.: Revenue Share, By Region, 2024 (%)

- Sanofi: Net Sales, 2024-2035 ($ Billion)

- Sanofi: Revenue Share, By Segment, 2024 (%)

- Sanofi: Revenue Share, By Region, 2024 (%)

- Others: Net Sales, 2024-2035 ($ Billion)

- Others: Revenue Share, By Segment, 2024 (%)

- Others: Revenue Share, By Region, 2024 (%)

Check Licence

Choose the plan that fits you best: Single User, Multi-User, or Enterprise solutions tailored for your needs.

We Have You Covered

- 24/7 Analyst Support

- Clients Across the Globe

- Tailored Insights

- Technology Tracking

- Competitive Intelligence

- Custom Research

- Syndicated Market Studies

- Market Overview

- Market Segmentation

- Growth Drivers

- Market Opportunities

- Regulatory Insights

- Innovation & Sustainability

Report Details

| Scope | Global |

| Pages | 281 |

| Delivery | PDF & Excel via Email |

| Language | English |

| Release | Dec 2025 |

| Access | Download from this page |