Global Pulsed Laser Deposition Systems Market

Global Pulsed Laser Deposition Systems Market Size, Share, By Product Type (Nanosecond Pulsed Laser Deposition Systems, Femtosecond Pulsed Laser Deposition Systems, and Picosecond Pulsed Laser Deposition Systems) By Application (Semiconductors, Thin Film Coatings, Optoelectronics, Energy Storage Devices, and Research and Development) By End User (Electronics and Semiconductor Industry, Academic and Research Institutes, Energy and Power Sector, and Industrial Manufacturing) and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2026-2035

REPORT COVERAGE

Global

Market Snapshot

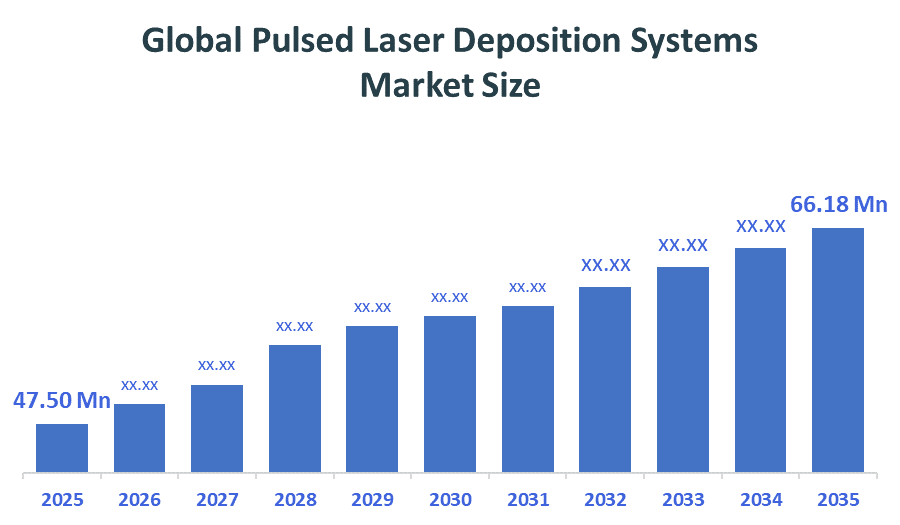

- Market Size (2025): USD 47.50 Million

- Projected Market Size (2035): USD 66.18 Million

- Compound Annual Growth Rate (CAGR): 3.37%

- Largest Regional Market: North America

- Fastest Growing Region: Asia-Pacific

- 3rd Largest Region: Europe

- Base Year: 2025

- Historical Period: 2021–2024

- Forecast Period: 2026–2035

According to Decision Advisors, the Global Pulsed Laser Deposition Systems Market Size is expected to grow from USD 47.50 million in 2025 to USD 66.18 million by 2035, with a CAGR of 3.37% during the forecast period from 2026 to 2035. The market is projected to experience steady growth as high-precision thin-film fabrication technologies become more integrated into specialised industrial applications. This expansion is mainly fuelled by the increased demand for complex oxide films, as well as pulsed laser deposition's growing use in high-temperature superconducting tapes. Innovations in laser source stability and vacuum chamber design are also significantly contributing to this expansion. Sophisticated systems with enhanced capabilities for stoichiometric transfer, thickness, and varied target materials are now considered essential for advanced research and semiconductor development.

Market Overview / Introduction

The increasing emphasis on ensuring efficiency in high-precision film deposition in thin film technology and material synthesis, especially in modern semiconductor technology and energy research, is one of the major growth drivers for the global pulsed laser deposition systems market. Pulsed laser deposition systems refer to advanced physical deposition technology involving high-energy laser beams aimed at a material target, which creates a plasma plume for film deposition on a material substrate with extreme stoichiometric precision. From its specialized origins in physics labs, this technology has advanced into highly sophisticated technology characterised by high film quality, atomic layer thickness control, and the capability for synthesising multi-layer films of materials like oxides, nitrides, and superconductors. Pulsed laser deposition systems have a crucial function in ensuring efficiency in high-performance technology, especially in situations where engineers and researchers apply this technology for high-density film deposition compared to conventional sputtering and chemical vapor deposition technology. The increased importance given to nanotechnology and ceramics has led to the inclusion of automated PLD systems that provide increased flexibility in adverse working conditions, including the production of high-temperature superconducting tapes, solid-state batteries, and the latest generation of microelectronics

- North America holds over 35% to 40% of global revenue, supported by strong R&D spending in aerospace, defence, and quantum computing, along with a high concentration of advanced laser technology companies and national laboratories.

- Semiconductor and electronics applications account for nearly 50% of total demand, driven by increasing use of pulsed laser deposition in ferroelectric memory devices, wide-bandgap semiconductors, and advanced optical coatings.

Notable Insights: -

- North America accounts for approximately 38% of the global Pulsed Laser Deposition Systems market share in 2025. This can be attributed to high investments in defence materials and high-performance computing.

- Asia-Pacific is projected to register the fastest growth, with its market share expected to reach around 34% by the end of the forecast period. The growth in the region can be attributed to the expansion of semiconductor manufacturing facilities in South Korea, Taiwan, and China, along with increased government spending in nanotechnology research.

- By application, electronics and specialised optics dominate the market, contributing nearly 42% of the total share. The use of these systems for creating functional thin films in sensors and integrated circuits solidified this segment's lead in the industry.

- By laser type, excimer laser-based systems hold the leading position with an estimated market share of about 46%. As industrial requirements for high-energy ultraviolet pulses become more common.

- The global pulsed laser deposition systems market is expanding at a Compound Annual Growth Rate CAGR of 3.37% through 2035.

What is the role of technology in shaping the market?

Technology is playing a transformative role in the pulsed laser deposition systems market by enhancing ablation consistency, plume monitoring, and overall deposition uniformity. Modern deposition units are evolving from manual laboratory setups into fully automated industrial systems equipped with in-situ monitoring tools like Reflection High-Energy Electron Diffraction (RHEED), advanced vacuum control, and seamless compatibility with multi-target synchronisation. This shift allows engineers and researchers to streamline material discovery, reduce substrate contamination, and maintain consistent operational accuracy across different material classes from polymers to complex ceramics.

How are Recent Developments Helping the Market?

Recent developments, including continuous laser source innovation, digital automation integration, and the advancement of combinatorial PLD techniques, are significantly driving the growth of the global pulsed laser deposition systems market. Manufacturers are introducing modern deposition chambers with programmable substrate heating, integrated load-locks for high throughput, and improved laser beam homogenisers, enabling more efficient and precise film growth. The growing shift toward high-power electronics and quantum materials is increasing demand for systems that seamlessly integrate with robotic target handling, allowing smoother workflow transitions and enhanced material purity.

Market Drivers

The global pulsed laser deposition systems market is growing with the increasing investments of technology providers in advanced material infrastructure to improve the performance of devices and precision in the manufacturing process. Modern PLD systems are gaining strong preference in the market with the advantage of integrating multiple capabilities such as high-purity material growth, intricate multilayer stacking, and flexible target switching in one compact system. The regional market is dominated by North America, with the high adoption of technologically advanced defence research equipment in the region. At the same time, the increasing trend of miniaturised electronic devices is driving the market with the need for advanced pulsed laser deposition systems that can enhance the functionality of devices, along with their reliability in harsh conditions. The awareness of advanced energy storage is motivating companies to upgrade their equipment with high-temperature substrate heaters and oxygen-compatible vacuum systems.

Restraints

The growth of the global pulsed laser deposition systems market is restricted by the high cost associated with high-power laser sources and vacuum system components. Additional cost factors for clean-room installation and target materials also affect the implementation cost of such systems in the normal production process.

Competitive Analysis:

The report offers the appropriate analysis of the key organisations/companies involved within the pulsed laser deposition systems market, along with a comparative evaluation primarily based on their product offerings, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborate analysis focusing on the current news and developments of the companies, which includes product development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

Top 10 Companies in the Pulsed Laser Deposition Systems Market

- PVD Products, Inc.

- Neocera, LLC

- Coherent Corp.

- Scienta Omicron

- The Kurt J. Lesker Company

- SVT Associates, Inc.

- AdNaNoTek Corporation

- Blue Wave Semiconductors, Inc.

- SolMateS B.V.

- SURFACE systems + technology GmbH & Co. KG

Government Initiatives

|

Country |

Key Government Initiatives |

|

US |

In the United States, advanced material fabrication and thin-film research are heavily supported through the CHIPS and Science Act, which authorises approximately USD 52.7 billion to revitalize domestic semiconductor manufacturing and R&D. |

|

Japan |

In Japan, the government is aggressively pursuing a chip renaissance by allocating 0.71% of its GDP (approximately USD 25.7 billion) toward the semiconductor and AI industrial sectors. Through the Ministry of Economy, Trade and Industry (METI), Japan is funding the Rapidus project with over USD 6.1 billion to achieve domestic mass production of 2nm chips by 2027. |

|

India |

In India, the India Semiconductor Mission (ISM) 2.0, announced in the Union Budget 2026–27, continues the momentum of a ?76,000 crore (approx. USD 9.1 billion) incentive framework. The government offers fiscal support of up to 50% of project costs for setting up compound semiconductor fabs and sensor manufacturing facilities. |

Study on the Supply, Demand, Distribution, and Market Environment

The pulsed laser deposition systems market is influenced by a balanced interaction between supply, demand, distribution channels, and the overall market environment. On the supply side, manufacturers are focusing on producing technologically advanced and cost-efficient PLD units to meet the evolving needs of semiconductor and material science professionals. This includes the development of high-repetition-rate laser sources and automated multi-target carousels that allow for continuous thin-film growth without breaking the vacuum. The main driving forces behind the demand for the technology are the increased usage of complex oxide films in microelectronics, the rising incidence of solid-state batteries, and the increased awareness of the combinatorial PLD technology. Concerning the distribution aspect, the market depends on a mix of industrial direct sales, scientific equipment approved distributors, and nanotechnology platforms, which are enhancing the accessibility of the products to both developed and emerging research centers.

Price Analysis and Consumer Behaviour Analysis

The cost of the pulsed laser deposition system is subject to variation depending on factors like the complexity of the system, whether the system is integrated with a laser source, and the level of automation. Advanced systems with in-situ analysis tools like RHEED (Reflection High-Energy Electron Diffraction) and ultrafast lasers are priced on the higher end due to their high level of accuracy and ability to create atom-perfect crystal lattices, while nanosecond-based nano PLD is priced lower.

Market Segmentation

The pulsed laser deposition systems market share is classified into product type, application type,

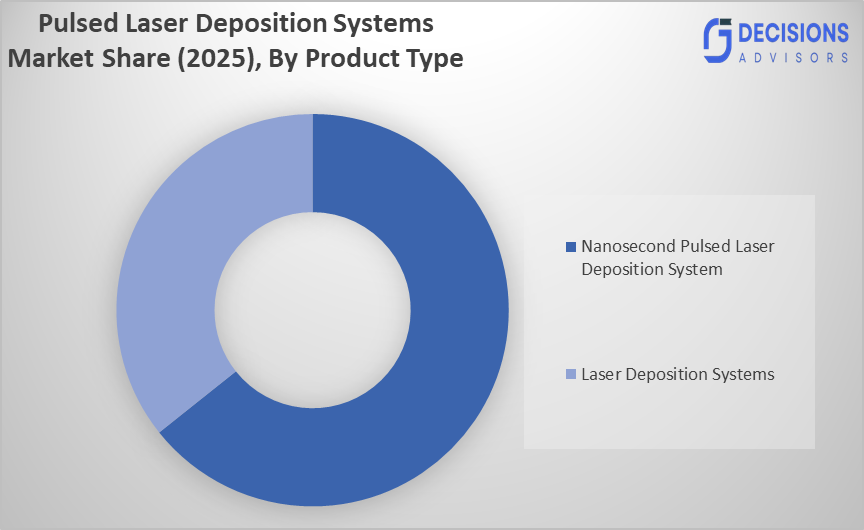

By product type, nanosecond pulsed laser deposition systems dominate the global pulsed laser deposition systems market, accounting for approximately 47% of the total market share in 2025.

Based on the product type, the pulsed laser deposition systems market is segmented into nanosecond pulsed laser deposition systems, femtosecond pulsed laser deposition systems, and picosecond pulsed laser deposition systems. By product type, nanosecond pulsed laser deposition systems dominate the global pulsed laser deposition systems market, accounting for approximately 47% of the total market share in 2025. The nanosecond segment dominated the market in 2024 and is expected to grow at a steady CAGR of around 3.4% during the forecast period. This dominance is mainly attributed to their wide adoption in thin film fabrication, material research, and industrial coating processes due to their cost-effectiveness, operational stability, and suitability for large-scale deposition requirements.

By application, semiconductors hold the largest share, contributing approximately 44% of the market in 2025.

The pulsed laser deposition systems market is segmented into semiconductors, thin film coatings, optoelectronics, energy storage devices, and research and development. By application, semiconductors hold the largest share, contributing approximately 44% of the market in 2025. The semiconductor segment accounted for the largest share of the market in 2024. The segment is expected to grow at a steady rate as demand for advanced electronic components and miniaturised devices continues to rise. The dominance of this segment is largely driven by the increasing use of pulsed laser deposition systems in fabricating high-precision thin films, integrated circuits, and next-generation electronic materials.

By end user, the electronics and semiconductor industry dominates the global pulsed laser deposition systems market, accounting for approximately 46% of the total market share in 2025.

Based on the end user, the pulsed laser deposition systems market is segmented into electronics and semiconductor industry, academic and research institutes, energy and power sector, and industrial manufacturing. By end user, the electronics and semiconductor industry dominates the global pulsed laser deposition systems market, accounting for approximately 46% of the total market share in 2025. The electronics and semiconductor segment dominated the market in 2024 and is expected to grow at a steady CAGR of around 3.6% during the forecast period. This dominance is mainly attributed to the increasing demand for advanced microelectronics, thin film devices, and high-performance materials used in integrated circuits, sensors, and next generation electronic components.

Strategies to Implement for Growth of the Market in Non-Leading Regions

The growth rate in the pulsed laser deposition system market in non-leading regions can be further increased by implementing the following strategies in the non-leading regions. First and foremost, the best strategy to boost the growth rate in the non-leading regions would be to introduce entry-level pulse laser deposition systems to the universities and startups in the non-leading regions. Secondly, the R&D funds and the government's nano-technology mission would also boost the growth rate in the non-leading regions. Thirdly, more funds would be required to be spent on the education and training of engineers in the field of vacuum technology and laser safety. Strengthening distribution channels through partnerships with global scientific equipment suppliers and utilising digital procurement technologies can help to improve access to specialised targets and laser gases in remote industrial locations. Partnerships between laser manufacturers and local material science centres can also enable customised deposition systems based on specific regional research needs.

Regional Segment Analysis of the Pulsed Laser Deposition Systems Market

- North America (U.S., Canada, Mexico)

- Europe (Germany, France, U.K., Italy, Spain, Rest of Europe)

- Asia-Pacific (China, Japan, India, South Korea, Rest of APAC)

- Latin America (Brazil and the Rest of Latin America)

- The Middle East and Africa (UAE, South Africa, Rest of MEA)

North America is expected to hold the largest share of the pulsed laser deposition systems market during the forecast period. The region accounts for approximately 38% of the global revenue share, backed by highly advanced infrastructure in material sciences and high adoption rates for PLD technology in defence and quantum computing applications. The majority of the revenue in this region comes from the United States due to high federal spending on research for functional ceramics and superconductors. The constant upgrade in optical coatings and early adoption of combinatorial PLD for fast discovery are contributing to demand for the technology in this region.

Asia-Pacific is projected to be the fastest-growing region over the forecast period. The region is expected to grow at a CAGR of approximately 4.5% while accounting for nearly 30% of the global market share. This can be attributed to the improvement in infrastructure for semiconductor processing and the ever-expanding electronics assembly plants in China, South Korea, and India. Additional factors include increased investments in local chip self-sufficiency, nanotechnology initiatives taken by various countries’ governments, and a massive increase in solar cell manufacturing facilities.

Europe is anticipated to hold the third-largest share, contributing approximately 24% of the global market share. The region is in a good position owing to the established research clusters in photonics and consistent investment in sustainable energy materials. Countries like Germany, France, and the UK are important players due to their high level of knowledge about advanced manufacturing and the implementation of clean energy projects like the Quantum Technologies Flagship. Moreover, the existence of major vacuum equipment producers and the modernisation of research facilities are contributing to the gradual uptake of pulsed laser deposition.

Future Market Trends in the Global Pulsed Laser Deposition Systems Market

1. Increasing Adoption of In-Situ Monitoring and Automated Control

A clear trend away from manual deposition equipment and towards fully integrated PLD systems with real-time diagnostic tools such as Reflection High-Energy Electron Diffraction (RHEED) is evident. Such sophisticated equipment has the potential to improve film quality and consistency by up to 25% through precise plume monitoring.

2. Rising Demand for Large-Area Industrial Production Systems

High-tech industries are now shifting their research and development from small-wafer R&D to large-area pulsed laser deposition. This is causing an increased demand for scanning laser beams and rotating substrate heater systems to accommodate wafers up to 200mm or larger.

3. Expansion of Combinatorial PLD for Rapid Material Discovery

The market is currently seeing rapid growth in the use of Combinatorial PLD systems, which enable the simultaneous deposition of different material gradients on a single substrate. This approach greatly accelerates the prototyping phase of new functional materials, especially in the quest for solid-state electrolytes and quantum materials.

Recent Developments

- In June 2025, Coherent Corp. unveiled the LEAP 600C, a specialised 600 W excimer laser system designed for high-throughput Pulsed Laser Deposition. The system enables deposition rates improvement of nearly 30% compared to previous models, making it suitable for large-scale production of high-temperature superconducting tapes.

- In early 2025, PVD Products upgraded its Nano PLD series by integrating high-pressure RHEED compatibility into entry-level systems. This enhancement allows real-time atomic layer monitoring while reducing system costs by approximately 20%, improving accessibility for research institutions and small-scale laboratories.

- In 2024, Scienta Omicron expanded its modular deposition platform with a dedicated laser MBE module. This development improved vacuum efficiency by nearly 20% and enhanced thin film purity levels, supporting advanced quantum material and nanotechnology research applications.

- In late 2024, a strategic collaboration between SolMateS and semiconductor manufacturers led to the standardisation of PLD processes for PZT thin films on 8-inch wafers. This initiative increased production scalability by over 30% and aligned with the rising demand in the MEMS sensor market, which is projected to grow at a CAGR of around 10% over the next few years.

Market Segmentation

This study forecasts revenue at global, regional, and country levels from 2020 to 2035. Decision Advisors has segmented the pulsed laser deposition systems market is segmented based on the following categories:

Global Pulsed Laser Deposition Systems Market, By Product Type

• Nanosecond Pulsed Laser Deposition Systems

• Femtosecond Pulsed Laser Deposition Systems

• Picosecond Pulsed Laser Deposition Systems

Global Pulsed Laser Deposition Systems Market, By Application

• Semiconductors

• Thin Film Coatings

• Optoelectronics

• Energy Storage Devices

• Research and Development

Global Pulsed Laser Deposition Systems Market, By End User

• Electronics and Semiconductor Industry

• Academic and Research Institutes

• Energy and Power Sector

• Industrial Manufacturing

Global Pulsed Laser Deposition Systems Market, By Regional Analysis

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- United Arab Emirates

- Saudi Arabia

- Qatar

- South Africa

- Rest of Middle East & Africa

Frequently Asked Questions (FAQ)

What is a Pulsed Laser Deposition (PLD) system and why is it important?

A Pulsed Laser Deposition system is a highly advanced physical vapour deposition tool used for the deposition of a film on a substrate material by utilising a high-energy laser beam for the deposition of material from a target. This tool is highly significant in the field of material science because it enables the deposition of complex chemical compositions with high precision.

What factors are driving the growth of the PLD systems market?

The market is growing with the increasing demand for high-performance microelectronic devices, the rise in research activities in solid-state batteries, and the growing application of high-temperature superconductors in energy and defence fields.

Which laser source dominates the PLD market?

The excimer lasers have the highest market share. This is because the excimer lasers have a high ultraviolet output, which gives them the high absorption capability necessary for clean ablation of ceramics and oxides used in the study and application of semiconductors.

Which region leads the PLD systems market?

North America is the leader in the market with strong R&D capabilities and high defence spending in advanced materials. The Asia-Pacific market is the fastest-growing market with the expanding semiconductor industry in the region and growing government spending in nanotechnology.

Who are the key end users of these deposition systems?

The primary end users are semiconductor manufacturers, academic research organisations, energy producers working on solar and battery technology, and aerospace organisations. The largest sector for semiconductor and electronics research is driven by the ongoing need for thinner and more functional material layers in new technology.

Check Licence

Choose the plan that fits you best: Single User, Multi-User, or Enterprise solutions tailored for your needs.

We Have You Covered

- 24/7 Analyst Support

- Clients Across the Globe

- Tailored Insights

- Technology Tracking

- Competitive Intelligence

- Custom Research

- Syndicated Market Studies

- Market Overview

- Market Segmentation

- Growth Drivers

- Market Opportunities

- Regulatory Insights

- Innovation & Sustainability

Report Details

| Scope | Global |

| Pages | 210 |

| Delivery | PDF & Excel via Email |

| Language | English |

| Release | Apr 2026 |

| Access | Download from this page |