Global Residential and Commercial Smart Glass Market

Global Residential and Commercial Smart Glass Market Size, Share, By Product (Electrochromic Glass, Thermochromic Glass, Photochromic Glass, Suspended Particle Device (SPD) Glass and Liquid Crystal Glass) By Application (Residential, Commercial, Automotive, Aerospace and Others), By Technology (Active Technology and Passive Technology) and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2026 ? 2035.

REPORT COVERAGE

Global

Market Snapshot

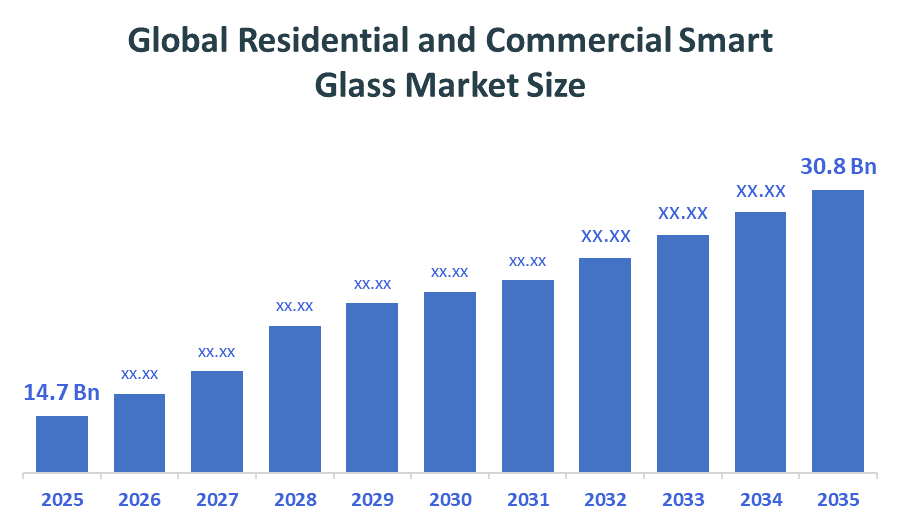

- Market Size (2025): USD 14.7 Billion

- Projected Market Size (2035): USD 30.8 Billion

- Compound Annual Growth Rate (CAGR): 7.68%

- Largest Regional Market: North America

- Fastest Growing Region: Asia Pacific

- 3rd Largest Region: Europe

- Base Year: 2025

- Historical Period: 2021–2025

- Forecast Period: 2026–2035

According to Decision Advisors, the global residential and commercial smart glass market size is expected to grow from USD 14.7 Billion in 2025 to USD 30.8 Billion by 2035, at a CAGR of 7.68% during the forecast period 2026-2035. Global residential and commercial smart glass market is projected to grow significantly over the next decade due to increasing demand for energy-efficient buildings, smart home automation, green building regulations, urbanization, aesthetic and privacy considerations, and technology advancements in electrochromic smart glass, thermochromic smart glass, and SPD smart glass.

Market Overview/ Introduction

The Global Residential and Commercial Smart Glass Market refers to the industry involved in the research, development, manufacturing, and commercialization of smart glass solutions for residential, commercial, and industrial applications. The products of this category include electrochromic devices, photochromic devices, thermochromic devices, and suspended particle devices which provide users with control over light, heat and privacy. The market experiences growth due to energy efficiency requirements are increasing and green building practices are becoming more common; people want solutions to control glare and ultraviolet radiation. The development of technology has enabled smart homes, offices, hospitals and retail spaces to adopt new systems through shorter switching times, bigger panel dimensions and their ability to work with building automation technologies.

- In June 2026, United States has tax deductions for smart glass and energy-efficient building projects apply only to constructions starting on or before June 30, 2026, ongoing projects may still claim benefits, and retrofits can be claimed every 3–4 years.

- The Energy Conservation Building Code (ECBC) mandates U-factor and SHGC standards for commercial buildings, promoting smart glass use to achieve ECBC/Super-ECBC compliance and reduce energy consumption

- The Smart Readiness Indicator (SRI) under the Energy Performance of Buildings Directive promotes smartness in buildings such as automation, dynamic envelope control, and energy management systems to optimise energy efficiency, occupant comfort, and grid responsiveness

Notable Insights: -

- Asia Pacific is the fastest growing region market share approximately 10% in the global residential and commercial smart glass market.

- North America holds the largest regional market share approximately 38% in the global residential and commercial smart glass market.

- By product, the electrochromic glass segment held a dominant position approximately 9.1% in terms of market share in 2025.

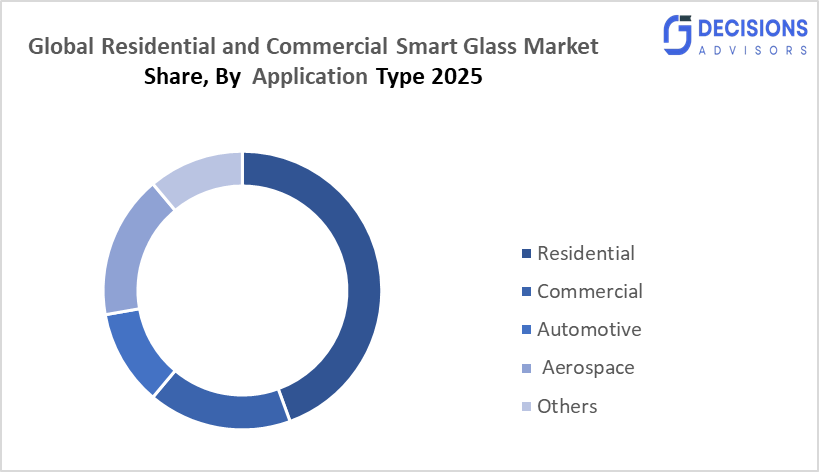

- By Application, Commercial segment is the dominating accounting for approximately 8.5% of the global market share in 2025.

- The compound annual growth rate of the Global Residential And Commercial Smart Glass Market is 12.51%.

- The market is likely to achieve a valuation of 30.8 Billion by 2035.

What is role of technology in grooming the market?

The global residential and commercial smart glass market experiences its main growth due to of technological advancements which provide dynamic light control together with energy efficient systems and building automation solutions. The latest electrochromic and thermochromics panels achieve state changes within 20 to 30 seconds which enables commercial towers to decrease their cooling requirements by 25%. The Internet of Things (IoT) systems enable users to monitor their operations in real time while they connect with HVAC systems and lighting controls which results in annual energy savings of 18% for each building. The architectural field benefits from large-format panels which extend their size beyond 3 square meters. AI-based predictive control systems adjust opacity according to weather conditions and occupancy levels and solar angles which results in improved comfort for building occupants while buildings achieve annual carbon emission reductions of approximately 2,800 kilograms of CO?.

Market Drivers

The global residential and commercial smart glass market is driven by rising demand for energy-efficient buildings, green certifications like LEED and BREEAM, and stricter building energy codes. The commercial and residential markets see increased adoption of electrochromic devices, thermochromics devices, and suspended particle devices which provide daylight control and glare reduction of 40% and privacy solutions. The electrochromic panels now reach 90% solar modulation which results in a 17% reduction of cooling requirements in commercial office spaces. The average return on investment from large commercial retrofits reaches between 5 to 7 years. Daylight-responsive glazing systems benefit 60% of monitored spaces by improving occupant comfort through glare reduction. The healthcare sector and educational institutions and high-rise residential buildings drive increased adoption of the technology.

Restrain

The Global Residential And Commercial Smart Glass Market faces multiple constraints due to its high installation costs which range between USD 120 and USD 350 for each square foot and the installation difficulties that arise when trying to connect to existing building automation systems and the product's inability to perform under extreme weather conditions and the architects and developers who work in this industry do not know about the product and the market is already occupied by low-emissivity coatings and electrochromic films and standard glazing products.

Competitive Analysis:

The report offers the appropriate analysis of the key organizations/companies involved within the global residential and commercial smart glass market, along with a comparative evaluation primarily based on their product of offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes product development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and more. This allows for the evaluation of the overall competition within the market.

Top Companies in Global Residential and Commercial Smart Glass Market

- Saint?Gobain

- AGC Inc.

- View, Inc.

- Gentex Corporation

- Corning Incorporated

- Guardian Industries Holdings

- Halio Inc.

- Gauzy Ltd.

- Research Frontiers Inc.

- Polytronix, Inc.

- Smartglass International Limited

- RavenWindow

- Pleotint LLC

- Vision Systems

- Kinestral Technologies, Inc.

Government Initiatives

|

Country |

Key Government Initiatives |

|

Europe |

In EU the Energy Performance of Buildings Directive (EPBD) enforces stricter energy efficiency standards across member states, encouraging high-performance glazing and smart glass adoption to reduce energy use and enhance thermal performance. |

|

US |

The International Energy Conservation Code (IECC 2024) and state-level standards, including California Title 24 (2025), increase glazing performance requirements, promoting electrochromic and dynamic smart glass for improved U-factor and Solar Heat Gain Coefficient compliance |

|

China |

The government’s urban smart building initiatives in Tier?1 cities, including Shanghai and Beijing, promote smart glass adoption in commercial towers, with studies showing energy savings of up to 347?MJ/m²?year in HVAC systems, accelerating market growth. |

Study on the Supply, Demand, Distribution, and Market Environment of Residential and Commercial Smart Glass Market

The residential and commercial smart glass market shows changing patterns which arise from its supply capabilities, user demand, distribution methods and environmental conditions. Specialized manufacturers create electrochromic, thermochromic, photochromic and suspended particle devices which produce most of the supply while North America maintains about 35% of global market production capacity. Demand is rising most notably in retrofit projects which show a 22% yearly increase in smart glass usage for existing commercial buildings due to of energy code compliance. The distribution system utilizes direct OEM partnerships which make up about 58% of its operations, digital B2B channels while HVAC and façade integrators handle about 30% of their business operations. The market environment faces main pressures which include changing raw material expenses that affect rare earth oxides used in switchable coatings and which experienced an 18% price change in 2025 and which need more lifecycle sustainability reporting in commercial specifications.

Price Analysis and Consumer Behaviour Analysis

Smart glass pricing differs according to its technological features and product dimensions. The basic suspended particle devices start at USD 90 to 150 per square foot while advanced electrochromic systems cost between USD 300 and 500 per square foot for large panels. Commercial offices show 40% higher retrofit adoption rates than residential buildings. Survey data indicates that approximately 55% of architects prioritize lifecycle cost over upfront price while 48% of buyers consider building automation integration as an important factor in their purchasing decisions.

Market Segmentation

The Residential and Commercial Smart Glass Market share is classified into therapeutic modality, product form, and distribution channel

- The electrochromic glass segment dominated the market in 2024, and is projected to grow at a substantial CAGR of approximately 9.1% during the forecast period.

Based on the product, the residential and commercial smart glass market is divided into electrochromic glass, thermochromic glass, photochromic glass, suspended particle device (SPD) glass and liquid crystal glass. Among these, the electrochromic glass segment dominated the market in 2024, and is projected to grow at a substantial CAGR of approximately 9.1% during the forecast period. The electrochromic glass segment dominates the market due to it generates approximately 8.5% of global revenue through its ability to switch quickly, its capacity to scale across large panels and its energy savings that reach 25% and its common use in commercial offices hospitals and high-end residential projects.

- The commercial segment accounted for the largest share in 2024, and is anticipated to grow at a significant CAGR of approximately 8.5 % during the forecast period.

Based on the application, the residential and commercial smart glass market is divided into residential, commercial, automotive, aerospace and others. Among these, the commercial segment accounted for the largest share in 2024, and is anticipated to grow at a significant CAGR of approximately 8.5 % during the forecast period. The commercial segment dominates due to businesses increasingly adopt smart glass for energy efficiency, glare reduction, and privacy in large-scale projects. Advanced electrochromic and SPD systems enable buildings to achieve 23% energy savings while their operational performance improves through automated building management systems which offices, healthcare facilities, and hotels are adopting at higher rates.

- The active technologysegment dominated the market in 2024, and is projected to grow at a substantial CAGR approximately 38.5% during the forecast period.

Based on the technology, the residential and commercial smart glass market is divided into active technology and passive technology. Among these, the active technology segment dominated the market in 2024, and is projected to grow at a substantial CAGR approximately 9.1% during the forecast period. Active technology dominated the market in 2024 because it generated approximately 65% of global revenue. Active smart glass, which includes electrochromic, SPD, and liquid crystal technologies, provides dynamic light and heat control capabilities that allow for energy savings of up to 25% and improve occupant comfort and building automation system integration, which results in greater usage of the technology in both commercial and high-end residential spaces.

Strategies to Implement for Growth of the Market in Non-Leading Regions

The companies need to establish local production facilities which will decrease their operational expenses by 18% and they should create partnerships with construction companies to conduct test projects in commercial buildings and premium residential properties. People will adopt new technologies more successfully when governments use incentive awareness campaigns while training programs for installers will enable them to accomplish maintenance work with 25% greater efficiency. The market will benefit from modular smart glass panels which have dimensions of 1 to 2 square meters and provide switching capabilities that take less than 20 seconds and initial prices between 350 and 450 US dollars per unit. The building sector in emerging markets will experience growth through international projects which include Southeast Asia and Latin America due to these regions implement energy-efficient building codes that will develop into a market 12.51% annual growth until 2035.

Regional Segment Analysis of the Global residential and commercial smart glass market

- North America (U.S., Canada, Mexico)

- Europe (Germany, France, U.K., Italy, Spain, Rest of Europe)

- Asia-Pacific (China, Japan, India, Rest of APAC)

- South America (Brazil and the Rest of South America)

- The Middle East and Africa (UAE, South Africa, Rest of MEA)

North America is anticipated to hold the largest share approximately 38% of the residential and commercial smart glass market over the predicted timeframe.

The residential and commercial smart glass market in North America will lead the market due to it will capture approximately 38% of total worldwide market share during the forecast period. The market experiences strong growth due to businesses construct new buildings while customers demand energy-saving building products and government programs support environmental construction standards which include LEED and ENERGY STAR certifications. The use of smart glass technology in office buildings medical facilities and luxury home developments is increasing because modern building control systems and Internet of Things networks enable this technology. The U.S. market holds 75% of the total market while Canada contributes 15% and Mexico begins to develop its market presence. The region experiences economic growth because both retrofit projects and sustainability regulations increase in the area.

Asia Pacific is expected to grow at a rapid CAGR approximately 10% in the residential and commercial smart glass marketduring the forecast period.

The residential and commercial smart glass market in Asia Pacific will experience fast growth with a compound annual growth rate between 10% during the forecast period. The urban population growth and the construction of tall commercial buildings and smart city projects in China, Japan and India drive this market expansion. The rising energy costs and government energy-efficient building material incentives and growing sustainability awareness drive the adoption of energy-efficient products. The region experiences growth in dynamic glazing system adoption through both rising investment in high-end residential developments and the implementation of intelligent building control technologies.

Europe is the 3rd largest region to grow in the residential and commercial smart glass market during the region.

Europe is the 3rd largest region in the residential and commercial smart glass market due to strict energy-efficiency regulations, growing green building certifications, and high adoption of smart building technologies. Countries like Germany, France, and the UK are investing in dynamic glazing systems to reduce HVAC energy consumption by 20–25% in commercial and residential projects. The integration of IoT-connected electrochromic and SPD glass in offices, hospitals, and public buildings enhances daylight management, occupant comfort, and sustainability compliance. Additionally, government subsidies and incentive programs for energy-efficient construction accelerate deployment.

Future Market Trends in Global Residential and Commercial Smart Glass Market: -

- Rapid Growth of IoT?Integrated Smart Glass

The market for smart glass systems which use IoT and AI control platforms will expand between 2023 and 2035 at a compound annual growth rate between 12.51%. The connected smart glass systems together with their sensor networks will produce approximately 18% more HVAC energy savings than non-connected systems

- Expansion of Retrofit Projects

The rate of retrofit adoption shows strong growth due to smart glass retrofits will make up more than 40% of all installation projects by 2030 which represents an increase from approximately 28% in 2024. The aging commercial building stock drives this trend because it needs energy efficiency upgrades which will decrease cooling loads by 18% in subtropical regions.

- Large?Format Smart Glazing Adoption

The current technology enables architects to use larger than 4 square meter panel sizes which enhance the visual design of atriums and high-rise building façades. Large-format dynamic glazing installations will experience annual growth of approximately 24% due to they enable better daylight entry into buildings which decreases glare from 38%.

Recent Development

- In November 2025, Research Frontiers and AIT Group launched the Thermolite RetroWAL SPD?SmartGlass retrofit system at GlassBuild America?2025, enabling instant dynamic tint upgrades to existing façades without full replacement, reducing solar heat gain and boosting energy efficiency in buildings

- In July 2025, Gauzy and partners delivered the industry’s first multi?zone SPD dimmable roof for the Cadillac?CELESTIQ, the largest in automotive production, enabling independent zonal control and cutting HVAC energy use by up to 40% in EVs.

- In March?2025, Saint?Gobain launched advanced electrochromic smart glass with enhanced durability and faster switching, targeting 30?% energy reduction in buildings, bolstering its product portfolio and construction materials through strategic acquisitions while holding a meaningful global market share.

- In January 2025, Gauzy showcased black SPD smart glass at CES 2025 with neutral dark tint, fast switching, 99% light blocking, and energy/heat control, plus solar-powered LCG combining PDLC/SPD with transparent solar cells for self-powered automotive, architectural, and aeronautical applications.

How is Recent Developments Helping the Market?

Recent developments are helping the global residential and commercial smart glass market by accelerating adoption through innovation, retrofit solutions, and broader applications. New product launches like faster switching SPD/electrochromic glass, retrofit systems for existing façades, and self?powered smart glass improve performance and cost?effectiveness, driving energy efficiency and sustainability. Faster switching SPD/electrochromic glass, retrofit solutions for existing façades, and self-powered systems reduce energy consumption by 20–40?%. Energy regulations, incentives from green building certifications (such as LEED and BREEAM), and integration with IoT-enabled building automation systems are driving the increased adoption of smart glass in both residential and commercial construction.

Market Segment

This study forecasts revenue at global, regional, and country levels from 2020 to 2035. Decision Advisors has segmented the residential and commercial smart glass market based on the below-mentioned segments:

Global residential and commercial smart glass market, By Product

- Electrochromic Glass

- Thermochromic Glass

- Photochromic Glass

- Suspended Particle Device (SPD) Glass

- Liquid Crystal Glass

Global residential and commercial smart glass market, By Application

- Residential

- Commercial

- Automotive

- Aerospace

- Others

Global residential and commercial smart glass market, By Technology

- Active Technology

- Passive Technology.

Global residential and commercial smart glass market, By Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa

Frequently Asked Questions (FAQ)

Q1. How do large-format smart glass panels impact energy efficiency in commercial buildings?

A: Large-format panels over 4?m² allow better daylight penetration and reduce glare by up to 38%, enabling commercial buildings to lower cooling loads and achieve annual energy savings of approximately 18% when integrated with building automation.

Q2. What role do retrofit SPD smart glass solutions play in older buildings?

A: Retrofit SPD systems, like Thermolite RetroWAL, enable dynamic tint upgrades without full façade replacement. Retrofit adoption is projected to account for more than 40% of smart glass installations by 2030, particularly in aging commercial stock needing energy-efficiency improvements.

Q3. How is IoT integration enhancing smart glass performance?

A: IoT-enabled smart glass connects with HVAC and lighting systems, providing real-time monitoring and AI-based predictive control. Buildings can achieve up to 18% additional energy savings and optimize occupant comfort while reducing annual CO? emissions by 2,800?kg per building.

Q4. Which regions are driving the fastest market growth and why?

A: Asia Pacific is the fastest-growing region due to rapid urbanization, smart city projects, rising energy costs, and government incentives for energy-efficient building materials. North America leads 38% market share, driven by green building regulations and high adoption in office and healthcare sectors.

- Introduction

- Objectives of the Study

- Market Definition

- Research Scope

- Research Methodology and Assumptions

- Executive Summary

- Premium Insights

- Porter’s Five Forces Analysis

- Value Chain Analysis

- Top Investment Pockets

- Market Attractiveness Analysis By Product

- Market Attractiveness Analysis By Application

- Market Attractiveness Analysis By Technology

- Market Attractiveness Analysis By Region

- Industry Trends

- Market Dynamics

- Market Evaluation

- Drivers

- Increase in health consciousness

- Restraints

- Strict adherence to regulations required for sugar substitute products

- Opportunities

- Increased investment in R&D activities by manufacturers

- Challenges

5.5.1. Product labeling and claims issues

- Global Residential and Commercial Smart Glass Market Analysis and Projection, By Product

- Segment Overview

- Electrochromic Glass

- Thermochromic Glass

- Photochromic Glass

- Suspended Particle Device (SPD) Glass

- Liquid Crystal Glass

- Global Residential and Commercial Smart Glass Market Analysis and Projection, By Application

- Segment Overview

- Residential

- Commercial

- Automotive

- Automotive

- Others

- Global Residential and Commercial Smart Glass Market Analysis and Projection, By Technology

- Segment Overview

- Active Technology

- Passive Technology.

- Global Residential and Commercial Smart Glass Market Analysis and Projection, By Regional Analysis

- Segment Overview

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Asia-Pacific

- Japan

- China

- India

- South America

- Brazil

- Middle East and Africa

- UAE

- South Africa

- Global Residential and Commercial Smart Glass Market-Competitive Landscape

- Overview

- Market Share of Key Players in the Residential and Commercial Smart Glass Market

- Global Company Market Share

- North America Company Market Share

- Europe Company Market Share

- APAC Company Market Share

- Competitive Situations and Trends

- Coverage Launches and Developments

- Partnerships, Collaborations, and Agreements

- Mergers & Acquisitions

- Expansions

- Company Profiles

- Saint-Gobain

- Business Overview

- Company Snapshot

- Company Market Share Analysis

- Company Coverage Portfolio

- Recent Developments

- SWOT Analysis

- AGC Inc.

- Business Overview

- Company Snapshot

- Company Market Share Analysis

- Company Coverage Portfolio

- Recent Developments

- SWOT Analysis

- View, Inc.

- Business Overview

- Company Snapshot

- Company Market Share Analysis

- Company Coverage Portfolio

- Recent Developments

- SWOT Analysis

- Gentex Corporation

- Business Overview

- Company Snapshot

- Company Market Share Analysis

- Company Coverage Portfolio

- Recent Developments

- SWOT Analysis

- Corning Incorporated

- Business Overview

- Company Snapshot

- Company Market Share Analysis

- Company Coverage Portfolio

- Recent Developments

- SWOT Analysis

- Guardian Industries Holdings

- Business Overview

- Company Snapshot

- Company Market Share Analysis

- Company Coverage Portfolio

- Recent Developments

- SWOT Analysis

- Halio Inc.

- Business Overview

- Company Snapshot

- Company Market Share Analysis

- Company Coverage Portfolio

- Recent Developments

- SWOT Analysis

- Gauzy Ltd.

- Business Overview

- Company Snapshot

- Company Market Share Analysis

- Company Coverage Portfolio

- Recent Developments

- SWOT Analysis

- Research Frontiers Inc.

- Business Overview

- Company Snapshot

- Company Market Share Analysis

- Company Coverage Portfolio

- Recent Developments

- SWOT Analysis

- Polytronix, Inc.

- Business Overview

- Company Snapshot

- Company Market Share Analysis

- Company Coverage Portfolio

- Recent Developments

- SWOT Analysis

- Smartglass International Limited

- Business Overview

- Company Snapshot

- Company Market Share Analysis

- Company Coverage Portfolio

- Recent Developments

- SWOT Analysis

- RavenWindow

- Business Overview

- Company Snapshot

- Company Market Share Analysis

- Company Coverage Portfolio

- Recent Developments

- SWOT Analysis

- Pleotint LLC

- Business Overview

- Company Snapshot

- Company Market Share Analysis

- Company Coverage Portfolio

- Recent Developments

- SWOT Analysis

- Vision Systems

- Business Overview

- Company Snapshot

- Company Market Share Analysis

- Company Coverage Portfolio

- Recent Developments

- SWOT Analysis

- Kinestral Technologies, Inc.

- Business Overview

- Company Snapshot

- Company Market Share Analysis

- Company Coverage Portfolio

- Recent Developments

- SWOT Analysis

- Saint-Gobain

List of Table

- Global Residential and Commercial Smart Glass Market, By Product, 2024-2035(USD Billion)

- Global Electrochromic Glass, Residential and Commercial Smart Glass Market, By Region, 2024-2035(USD Billion)

- Global Thermochromic Glass, Residential and Commercial Smart Glass Market, By Region, 2024-2035(USD Billion)

- Global Photochromic Glass, Residential and Commercial Smart Glass Market, By Region, 2024-2035(USD Billion)

- Global Suspended Particle Device (SPD) Glass, Residential and Commercial Smart Glass Market, By Region, 2024-2035(USD Billion)

- Global Liquid Crystal Glass, Residential and Commercial Smart Glass Market, By Region, 2024-2035(USD Billion)

- Global Residential and Commercial Smart Glass Market, By Application, 2024-2035(USD Billion)

- Global Residential, Residential and Commercial Smart Glass Market, By Region, 2024-2035(USD Billion)

- Global Commercial, Residential and Commercial Smart Glass Market, By Region, 2024-2035(USD Billion)

- Global Automotive, Residential and Commercial Smart Glass Market, By Region, 2024-2035(USD Billion)

- Global Automotive, Residential and Commercial Smart Glass Market, By Region, 2024-2035(USD Billion)

- Global Others, Residential and Commercial Smart Glass Market, By Region, 2024-2035(USD Billion)

- Global Residential and Commercial Smart Glass Market, By Technology, 2024-2035(USD Billion)

- Global Active Technology, Residential and Commercial Smart Glass Market, By Region, 2024-2035(USD Billion)

- Global Passive Technology., Residential and Commercial Smart Glass Market, By Region, 2024-2035(USD Billion)

- North America Residential and Commercial Smart Glass Market, By Product, 2024-2035(USD Billion)

- North America Residential and Commercial Smart Glass Market, By Application, 2024-2035(USD Billion)

- North America Residential and Commercial Smart Glass Market, By Technology, 2024-2035(USD Billion)

- U.S. Residential and Commercial Smart Glass Market, By Product, 2024-2035(USD Billion)

- U.S. Residential and Commercial Smart Glass Market, By Application, 2024-2035(USD Billion)

- U.S. Residential and Commercial Smart Glass Market, By Technology, 2024-2035(USD Billion)

- Canada Residential and Commercial Smart Glass Market, By Product, 2024-2035(USD Billion)

- Canada Residential and Commercial Smart Glass Market, By Application, 2024-2035(USD Billion)

- Canada Residential and Commercial Smart Glass Market, By Technology, 2024-2035(USD Billion)

- Mexico Residential and Commercial Smart Glass Market, By Product, 2024-2035(USD Billion)

- Mexico Residential and Commercial Smart Glass Market, By Application, 2024-2035(USD Billion)

- Mexico Residential and Commercial Smart Glass Market, By Technology, 2024-2035(USD Billion)

- Europe Residential and Commercial Smart Glass Market, By Product, 2024-2035(USD Billion)

- Europe Residential and Commercial Smart Glass Market, By Application, 2024-2035(USD Billion)

- Europe Residential and Commercial Smart Glass Market, By Technology, 2024-2035(USD Billion)

- Germany Residential and Commercial Smart Glass Market, By Product, 2024-2035(USD Billion)

- Germany Residential and Commercial Smart Glass Market, By Application, 2024-2035(USD Billion)

- Germany Residential and Commercial Smart Glass Market, By Technology, 2024-2035(USD Billion)

- France Residential and Commercial Smart Glass Market, By Product, 2024-2035(USD Billion)

- France Residential and Commercial Smart Glass Market, By Application, 2024-2035(USD Billion)

- France Residential and Commercial Smart Glass Market, By Technology, 2024-2035(USD Billion)

- U.K. Residential and Commercial Smart Glass Market, By Product, 2024-2035(USD Billion)

- U.K. Residential and Commercial Smart Glass Market, By Application, 2024-2035(USD Billion)

- U.K. Residential and Commercial Smart Glass Market, By Technology, 2024-2035(USD Billion)

- Italy Residential and Commercial Smart Glass Market, By Product, 2024-2035(USD Billion)

- Italy Residential and Commercial Smart Glass Market, By Application, 2024-2035(USD Billion)

- Italy Residential and Commercial Smart Glass Market, By Technology, 2024-2035(USD Billion)

- Spain Residential and Commercial Smart Glass Market, By Product, 2024-2035(USD Billion)

- Spain Residential and Commercial Smart Glass Market, By Application, 2024-2035(USD Billion)

- Spain Residential and Commercial Smart Glass Market, By Technology, 2024-2035(USD Billion)

- Asia Pacific Residential and Commercial Smart Glass Market, By Product, 2024-2035(USD Billion)

- Asia Pacific Residential and Commercial Smart Glass Market, By Application, 2024-2035(USD Billion)

- Asia Pacific Residential and Commercial Smart Glass Market, By Technology, 2024-2035(USD Billion)

- Japan Residential and Commercial Smart Glass Market, By Product, 2024-2035(USD Billion)

- Japan Residential and Commercial Smart Glass Market, By Application, 2024-2035(USD Billion)

- Japan Residential and Commercial Smart Glass Market, By Technology, 2024-2035(USD Billion)

- China Residential and Commercial Smart Glass Market, By Product, 2024-2035(USD Billion)

- China Residential and Commercial Smart Glass Market, By Application, 2024-2035(USD Billion)

- China Residential and Commercial Smart Glass Market, By Technology, 2024-2035(USD Billion)

- India Residential and Commercial Smart Glass Market, By Product, 2024-2035(USD Billion)

- India Residential and Commercial Smart Glass Market, By Application, 2024-2035(USD Billion)

- India Residential and Commercial Smart Glass Market, By Technology, 2024-2035(USD Billion)

- South America Residential and Commercial Smart Glass Market, By Product, 2024-2035(USD Billion)

- South America Residential and Commercial Smart Glass Market, By Application, 2024-2035(USD Billion)

- South America Residential and Commercial Smart Glass Market, By Technology, 2024-2035(USD Billion)

- Brazil Residential and Commercial Smart Glass Market, By Product, 2024-2035(USD Billion)

- Brazil Residential and Commercial Smart Glass Market, By Application, 2024-2035(USD Billion)

- Brazil Residential and Commercial Smart Glass Market, By Technology, 2024-2035(USD Billion)

- The Middle East and Africa Residential and Commercial Smart Glass Market, By Product, 2024-2035(USD Billion)

- The Middle East and Africa Residential and Commercial Smart Glass Market, By Application, 2024-2035(USD Billion)

- The Middle East and Africa Residential and Commercial Smart Glass Market, By Technology, 2024-2035(USD Billion)

- UAE Residential and Commercial Smart Glass Market, By Product, 2024-2035(USD Billion)

- UAE Residential and Commercial Smart Glass Market, By Application, 2024-2035(USD Billion)

- UAE Residential and Commercial Smart Glass Market, By Technology, 2024-2035(USD Billion)

- South Africa Residential and Commercial Smart Glass Market, By Product, 2024-2035(USD Billion)

- South Africa Residential and Commercial Smart Glass Market, By Application, 2024-2035(USD Billion)

- South Africa Residential and Commercial Smart Glass Market, By Technology, 2024-2035(USD Billion)

List of Figures

- Global Residential and Commercial Smart Glass Market Segmentation

- Residential and Commercial Smart Glass Market: Research Methodology

- Market Size Estimation Methodology: Bottom-Up Approach

- Market Size Estimation Methodology: Top-down Approach

- Data Triangulation

- Porter’s Five Forces Analysis

- Value Chain Analysis

- Top investment pocket in the Residential and Commercial Smart Glass Market

- Top Winning Strategies, 2024-2035

- Top Winning Strategies, By Development, 2024-2035(%)

- Top Winning Strategies, By Company, 2024-2035

- Moderate Bargaining power of Buyers

- Moderate Bargaining power of Suppliers

- Moderate Bargaining power of New Entrants

- Low threat of Substitution

- High Competitive Rivalry

- Top Player Positioning, 2024

- Market Share Analysis, 2024

- Restraint and Drivers: Residential and Commercial Smart Glass Market

- Residential and Commercial Smart Glass Market Segmentation, By Product

- Residential and Commercial Smart Glass Market For Electrochromic Glass, By Region, 2024-2035 ($ Billion)

- Residential and Commercial Smart Glass Market For Thermochromic Glass, By Region, 2024-2035 ($ Billion)

- Residential and Commercial Smart Glass Market For Photochromic Glass, By Region, 2024-2035 ($ Billion)

- Residential and Commercial Smart Glass Market For Suspended Particle Device (SPD) Glass, By Region, 2024-2035 ($ Billion)

- Residential and Commercial Smart Glass Market For Liquid Crystal Glass, By Region, 2024-2035 ($ Billion)

- Residential and Commercial Smart Glass Market Segmentation, By Application

- Residential and Commercial Smart Glass Market For Residential, By Region, 2024-2035 ($ Billion)

- Residential and Commercial Smart Glass Market For Commercial, By Region, 2024-2035 ($ Billion)

- Residential and Commercial Smart Glass Market For Automotive, By Region, 2024-2035 ($ Billion)

- Residential and Commercial Smart Glass Market For Automotive, By Region, 2024-2035 ($ Billion)

- Residential and Commercial Smart Glass Market For Others, By Region, 2024-2035 ($ Billion)

- Residential and Commercial Smart Glass Market Segmentation, By Technology

- Residential and Commercial Smart Glass Market For Active Technology, By Region, 2024-2035 ($ Billion)

- Residential and Commercial Smart Glass Market For Passive Technology., By Region, 2024-2035 ($ Billion)

- Saint-Gobain: Net Sales, 2024-2035 ($ Billion)

- Saint-Gobain: Revenue Share, By Segment, 2024 (%)

- Saint-Gobain: Revenue Share, By Region, 2024 (%)

- AGC Inc.: Net Sales, 2024-2035 ($ Billion)

- AGC Inc.: Revenue Share, By Segment, 2024 (%)

- AGC Inc.: Revenue Share, By Region, 2024 (%)

- View, Inc.: Net Sales, 2024-2035 ($ Billion)

- View, Inc.: Revenue Share, By Segment, 2024 (%)

- View, Inc.: Revenue Share, By Region, 2024 (%)

- Gentex Corporation: Net Sales, 2024-2035 ($ Billion)

- Gentex Corporation: Revenue Share, By Segment, 2024 (%)

- Gentex Corporation: Revenue Share, By Region, 2024 (%)

- Corning Incorporated: Net Sales, 2024-2035 ($ Billion)

- Corning Incorporated: Revenue Share, By Segment, 2024 (%)

- Corning Incorporated: Revenue Share, By Region, 2024 (%)

- Guardian Industries Holdings: Net Sales, 2024-2035 ($ Billion)

- Guardian Industries Holdings: Revenue Share, By Segment, 2024 (%)

- Guardian Industries Holdings: Revenue Share, By Region, 2024 (%)

- Halio Inc.: Net Sales, 2024-2035 ($ Billion)

- Halio Inc.: Revenue Share, By Segment, 2024 (%)

- Halio Inc.: Revenue Share, By Region, 2024 (%)

- Gauzy Ltd.: Net Sales, 2024-2035 ($ Billion)

- Gauzy Ltd.: Revenue Share, By Segment, 2024 (%)

- Gauzy Ltd.: Revenue Share, By Region, 2024 (%)

- Research Frontiers Inc..: Net Sales, 2024-2035 ($ Billion)

- Research Frontiers Inc..: Revenue Share, By Segment, 2024 (%)

- Research Frontiers Inc..: Revenue Share, By Region, 2024 (%)

- Polytronix, Inc.: Net Sales, 2024-2035 ($ Billion)

- Polytronix, Inc.: Revenue Share, By Segment, 2024 (%)

- Polytronix, Inc.: Revenue Share, By Region, 2024 (%)

- Smartglass International Limited: Net Sales, 2024-2035 ($ Billion)

- Smartglass International Limited: Revenue Share, By Segment, 2024 (%)

- Smartglass International Limited: Revenue Share, By Region, 2024 (%)

- RavenWindow: Net Sales, 2024-2035 ($ Billion)

- RavenWindow: Revenue Share, By Segment, 2024 (%)

- RavenWindow: Revenue Share, By Region, 2024 (%)

- Pleotint LLC: Net Sales, 2024-2035 ($ Billion)

- Pleotint LLC: Revenue Share, By Segment, 2024 (%)

- Pleotint LLC: Revenue Share, By Region, 2024 (%)

- Vision Systems: Net Sales, 2024-2035 ($ Billion)

- Vision Systems: Revenue Share, By Segment, 2024 (%)

- Vision Systems: Revenue Share, By Region, 2024 (%)

- Kinestral Technologies, Inc.: Net Sales, 2024-2035 ($ Billion)

- Kinestral Technologies, Inc.: Revenue Share, By Segment, 2024 (%)

- Kinestral Technologies, Inc.: Revenue Share, By Region, 2024 (%)

Check Licence

Choose the plan that fits you best: Single User, Multi-User, or Enterprise solutions tailored for your needs.

We Have You Covered

- 24/7 Analyst Support

- Clients Across the Globe

- Tailored Insights

- Technology Tracking

- Competitive Intelligence

- Custom Research

- Syndicated Market Studies

- Market Overview

- Market Segmentation

- Growth Drivers

- Market Opportunities

- Regulatory Insights

- Innovation & Sustainability

Report Details

| Scope | Global |

| Pages | 210 |

| Delivery | PDF & Excel via Email |

| Language | English |

| Release | Apr 2026 |

| Access | Download from this page |