Global Retinal Vein Occlusion Market

Global Retinal Vein Occlusion Market Size, Share, and COVID-19 Impact Analysis, By Type (Branch Retinal Vein Occlusion and Central Retinal Vein Occlusion), By Treatment (Anti-vascular Endothelial Growth Factor (Anti-VEGF), Corticosteroid Drugs, Laser Photocoagulation, Vitrectomy and Others) and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2025-2035.

REPORT COVERAGE

Global

Global Retinal Vein Occlusion Market Insights Forecasts to 2035

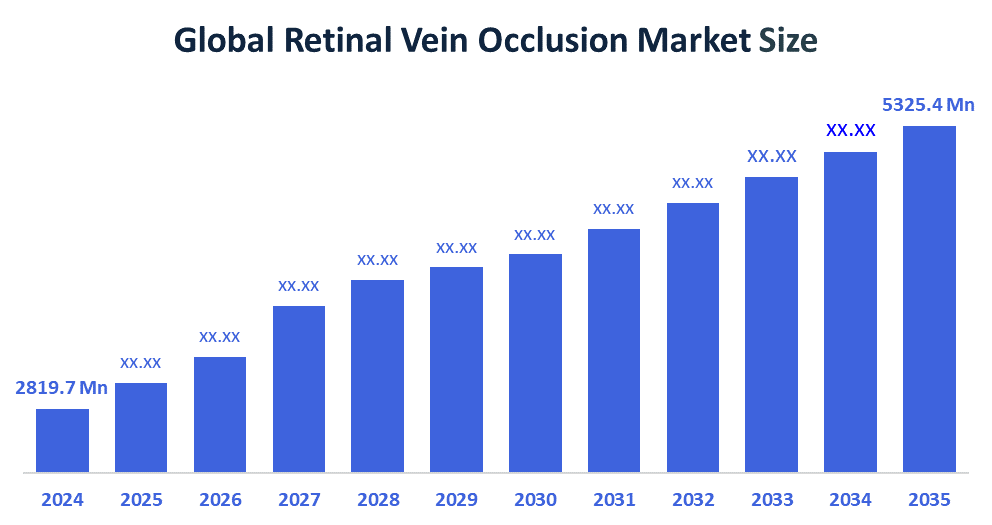

- The Global Retinal Vein Occlusion Market Size Was valued at USD 2819.7 Million in 2024

- The Global Retinal Vein Occlusion Market Size is Expected to Grow at a CAGR of around 5.95% from 2025 to 2035

- The Worldwide Retinal Vein Occlusion Market Size is Expected to Reach USD 5325.4 Million by 2035

- Asia-Pacific is expected to grow the fastest during the forecast period.

According to a research report published by Spherical Insights and Consulting, the global retinal vein occlusion market size was worth around USD 2819.7 Million in 2024 and is predicted to grow to around USD 5325.4 Million by 2035 with a compound annual growth rate (CAGR) of 5.95% from 2025 to 2035. The global retinal vein occlusion market will achieve future growth through advanced anti-VEGF therapies and sustained-release drug delivery systems and AI-based retinal imaging technology and tele-ophthalmology expansion and combination treatment methods and the increasing elderly demographic and better healthcare access in developing markets.

Market Overview

The global retinal vein occlusion market refers to the worldwide industry that handles the detection and treatment of retinal vein occlusion, which is an eye condition that results from blocked retinal veins and causes vision loss. Additionally, the retinal vein occlusion market offers substantial growth potential because of ongoing research into new treatment drugs and diagnostic products. Patients with RVO can benefit from emerging treatments which include gene therapies and new anti-inflammatory drugs. The market currently develops customized medicine solutions which design treatments according to specific patient needs to achieve better results. The increasing number of clinical trials that seek to develop new treatment methods will drive future market growth according to market experts. The recent approval of drugs such as dexamethasone intravitreal implant (Ozurdex) and brolucizumab has created new treatment possibilities which enable pharmaceutical companies to increase their product lines. The retinal vein occlusion market will experience growth because pharmaceutical companies and research institutions will enhance their collaborative efforts to develop and introduce new treatment solutions.

Report Coverage

This research report categorizes the retinal vein occlusion market based on various segments and regions, forecasts revenue growth, and analyzes trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the retinal vein occlusion market. Recent market developments and competitive strategies such as expansion, type launch, development, partnership, merger, and acquisition, have been included to draw the competitive landscape in the market. The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the retinal vein occlusion market.

Driving Factors

The retinal vein occlusion market depends on three main factors which are the rising RVO cases and the growing elder population and the development of new treatment methods. The aging demographic is particularly susceptible to retinal vascular diseases, with people over the age of 60 at a higher risk of developing RVO. The World Health Organization (WHO) estimates that the global population of people aged 60 years or older will reach 2.1 billion by 2050, further escalating the demand for treatments targeting retinal disorders. The market expansion receives additional support from the introduction of advanced diagnostic equipment which includes optical coherence tomography (OCT) and from the launch of new drug treatments which include anti-VEGF injections. Anti-VEGF (vascular endothelial growth factor) therapies, like ranibizumab and aflibercept, have transformed RVO treatment methods because these therapies enable patients to achieve better vision results which has driven market growth worldwide.

Restraining Factors

The main factors that restrict progress include expensive treatment costs, restricted availability of specialized eye care services, dangers associated multiple times of getting intravitreal injections, insufficient knowledge about medical conditions that exist in developing areas, the process of diagnosing patients takes too long and the existing reimbursement systems stop doctors from using new treatment methods.

Market Segmentation

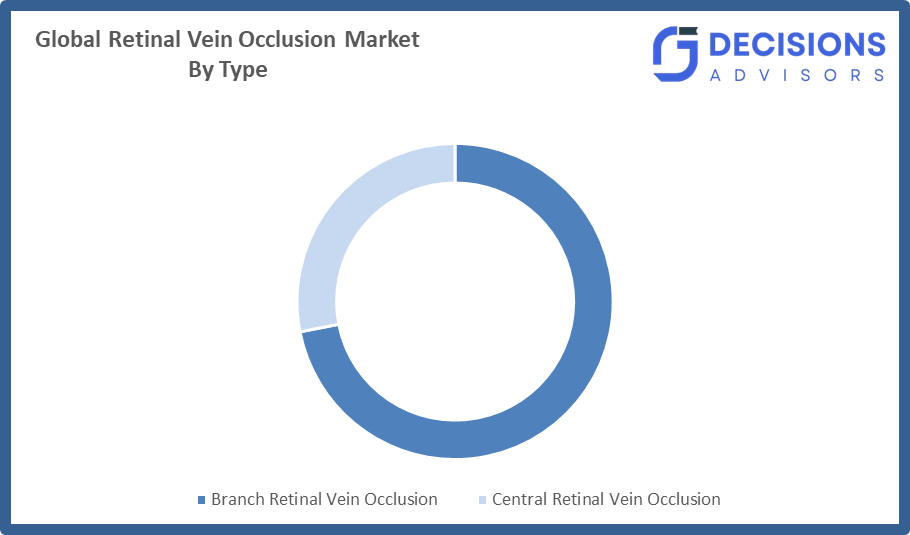

The retinal vein occlusion market share is classified into type and treatment.

- The branch retinal vein occlusion segment dominated the market in 2024, approximately 65% and is projected to grow at a substantial CAGR during the forecast period.

Based on the type, the retinal vein occlusion market is divided into branch retinal vein occlusion, central retinal vein occlusion. Among these, the branch retinal vein occlusion segment dominated the market in 2024, approximately 65% and is projected to grow at a substantial CAGR during the forecast period. The higher incidence of the condition combined with its effective treatment response makes it more prevalent than central occlusion. The method enables doctors to identify and treat patients who have developed specific retinal ailments which occur in particular areas. The high use of anti-VEGF injections together with laser treatments creates a strong need for these services. The segment expansion receives additional support from three factors which include increasing elderly populations, growing diabetes and hypertension rates, and advancements in retinal imaging technologies.

- The anti-vascular endothelial growth factor (Anti-VEGF) segment accounted for the largest share in 2024, approximately 68% and is anticipated to grow at a significant CAGR during the forecast period.

Based on the treatment, the retinal vein occlusion market is divided into anti-vascular endothelial growth factor (Anti-VEGF), corticosteroid drugs, laser photocoagulation, vitrectomy and others. Among these, the anti-vascular endothelial growth factor (Anti-VEGF) segment accounted for the largest share in 2024, approximately 68% and is anticipated to grow at a significant CAGR during the forecast period. The treatment demonstrates effective clinical results which decrease macular edema while enhancing visual acuity. Ophthalmologists prefer the treatment as their primary option because of its effectiveness. The adoption of the product increases because of its continuous product developments and its sustained-release product designs and its ability to treat more patients. The segment experiences growth because of three factors which include increasing retinal disorder cases and aging populations and better access to intravitreal therapies.

Regional Segment Analysis of the Retinal Vein Occlusion Market

- North America (U.S., Canada, Mexico)

- Europe (Germany, France, U.K., Italy, Spain, Rest of Europe)

- Asia-Pacific (China, Japan, India, Rest of APAC)

- South America (Brazil and the Rest of South America)

- The Middle East and Africa (UAE, South Africa, Rest of MEA)

North America is anticipated to hold the largest share of the retinal vein occlusion market over the predicted timeframe.

North America is anticipated to hold the largest share of the retinal vein occlusion market over the predicted timeframe. The combination of advanced ophthalmology infrastructure and high retinal disorder awareness together with their strong diagnostic capabilities creates a complete system which enables effective retinal disorder detection. The system facilitates treatment access because it provides positive reimbursement policies and medical facilities that adopt Anti-VEGF therapies at an early stage. The region maintains its dominant position because of its leading pharmaceutical companies and active clinical research activities and increasing number of senior citizens.

Asia-Pacific is expected to grow at a rapid CAGR in the retinal vein occlusion market during the forecast period. The region experiences development because of three factors which include expanding ophthalmic care infrastructure and rising diabetes and hypertension rates and the growing number of elderly citizens. The region experiences growth because of improved healthcare spending, increased availability of retinal imaging and Anti-VEGF treatments, the presence of many unmet medical needs, and government initiatives and pharmaceutical industry growth.

Competitive Analysis:

The report offers the appropriate analysis of the key organizations/companies involved within the retinal vein occlusion market, along with a comparative evaluation primarily based on their type of offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes type development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

List of Key Companies

- AbbVie

- Hoffmann-La Roche AG

- Regeneron Pharmaceuticals, Inc.

- Taiwan Liposome Company

- Aerie Pharmaceuticals, Inc.

- Graybug Vision

- Outlook Therapeutics

- Kodiak Sciences, Inc.

- Chugai Pharmaceutical Co. Ltd.

- Novartis AG

- Others

Key Target Audience

- Market Players

- Investors

- End-users

- Government Authorities

- Consulting and Research Firm

- Venture capitalists

- Value-Added Resellers (VARs)

Recent Development

- In July 2024, Roche announced y that the European Commission (EC) has approved Vabysmo (faricimab) for the treatment of visual impairment due to macular edema secondary to retinal vein occlusion.

Market Segment

This study forecasts revenue at global, regional, and country levels from 2020 to 2035. Spherical Insights has segmented the retinal vein occlusion market based on the below-mentioned segments:

Global Retinal Vein Occlusion Market, By Type

- Branch Retinal Vein Occlusion

- Central Retinal Vein Occlusion

Global Retinal Vein Occlusion Market, By Treatment

- Anti-vascular Endothelial Growth Factor (Anti-VEGF)

- Corticosteroid Drugs

- Laser Photocoagulation

- Vitrectomy

- Others

Global Retinal Vein Occlusion Market, By Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa

Frequently Asked Questions (FAQ)

1. What factors are driving growth in the Global Retinal Vein Occlusion Market?

A: Rising retinal vein occlusion cases, growing elderly population, increasing diabetes and hypertension prevalence, advanced diagnostic technologies like OCT, and strong adoption of anti-VEGF therapies are key drivers supporting sustained global market expansion.

2. Which type segment leads the market and why?

A: Branch retinal vein occlusion dominates due to higher incidence, better treatment responsiveness, localized retinal damage enabling earlier diagnosis, and strong use of anti-VEGF injections and laser therapies, increasing overall treatment demand.

3. Why does the Anti-VEGF segment hold the largest treatment share?

A: Anti-VEGF therapies lead because they effectively reduce macular edema, improve vision, serve as first-line treatments, gain strong ophthalmologist preference, and benefit from continuous innovation, sustained-release formulations, and expanding patient eligibility.

4. Why is North America the largest regional market?

A: Advanced ophthalmology infrastructure, strong retinal disorder awareness, superior diagnostic systems, favorable reimbursement policies, early Anti-VEGF adoption, leading pharmaceutical presence, active clinical research, and growing elderly population drive regional dominance.

5. Why is Asia-Pacific the fastest-growing region?

A: Asia-Pacific growth is fueled by expanding eye-care infrastructure, rising diabetes and hypertension cases, aging populations, higher healthcare spending, improved retinal imaging access, large untreated patient pools, supportive government programs, and pharmaceutical expansion.

Check Licence

Choose the plan that fits you best: Single User, Multi-User, or Enterprise solutions tailored for your needs.

We Have You Covered

- 24/7 Analyst Support

- Clients Across the Globe

- Tailored Insights

- Technology Tracking

- Competitive Intelligence

- Custom Research

- Syndicated Market Studies

- Market Overview

- Market Segmentation

- Growth Drivers

- Market Opportunities

- Regulatory Insights

- Innovation & Sustainability

Report Details

| Scope | Global |

| Pages | 210 |

| Delivery | PDF & Excel via Email |

| Language | English |

| Release | Mar 2026 |

| Access | Download from this page |