Global Robotic Endoscopy Devices Market Size, Share

Robotic Endoscopy Devices Market Size, Share, By Product Type (Robotic Endoscopy Systems, Capsule Endoscopy Devices, Visualization & Imaging Systems, Accessories), By Application (Gastroenterology, Pulmonology, Urology, Gynaecology, Others), By End User (Hospitals, Ambulatory Surgical Centers, Specialty Clinics), By Region (North America, Europe, Asia-Pacific, Latin America, Middle East & Africa), Analysis and Forecast 2026-2035.

CAGR

9.01%

REVENUE 2025

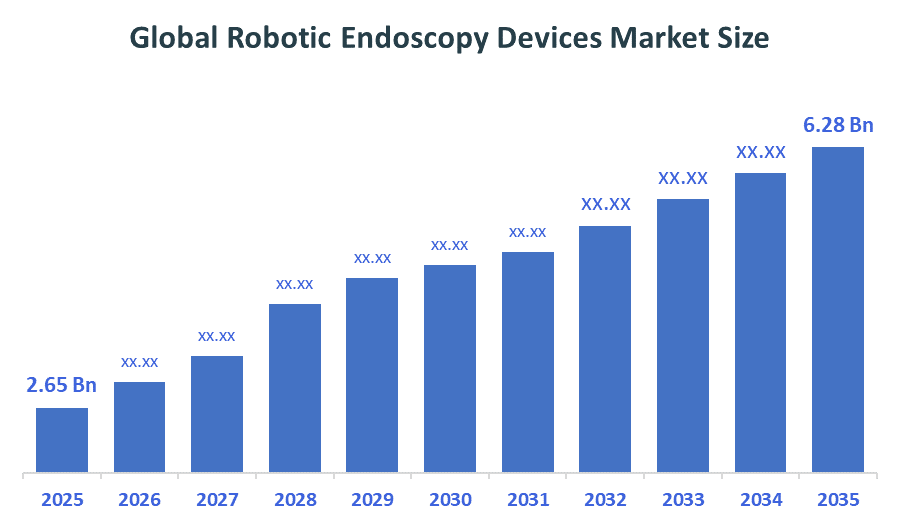

USD Billion 2.65

FORECAST 2035

USD Billion 6.28

REPORT COVERAGE

Global

The Global Robotic Endoscopy Devices Market Size is foreseen to grow from USD 2.65 Billion in 2025 and is govern to reach around USD 6.28 Billion by 2035. According to Decision Advisors, a detailed research report on the Global Robotic Endoscopy Devices Market is boosted by the integration of Artificial Intelligence (AI) and Machine Learning, accounting for nearly 50-60% share of the total share worldwide. Intuitive Surgicel is the prime player in the market with approximately USD 10.06 Billion in annual turnover and a 30-32% market share, positioning it as the primary driver of the global robotic endoscopy devices market.

Market Snapshot

- Global Robotic Endoscopy Devices Market Size (2025): USD 2.65 Billion

- Projected Global Robotic Endoscopy Devices Market Size (2035): USD 6.28 Billion

- Global Robotic Endoscopy Devices Market Compound Annual Growth Rate (CAGR): 9.01%

- Largest Growing Region: North America

- Fastest Regional Market: Asia Pacific

- 3rd Largest Region: Europe

- Base Year: 2025

- Historical Period: 2021–2024

- Forecast Period: 2026–2035

Market Overview/ Introduction

The Global Robotic Endoscopy Devices Market is a high-growth sector within medical technology that utilises computer-assisted programming to run diagnostic and therapeutic SOP within the body's internal organs. This market is all about replacing the traditional, hand-held scopes doctors use to look inside the body with sophisticated robotic systems. These robots don't replace doctors, they act like a high-precision extension of their hands, using flexible tubes, 3D cameras, and AI-powered GPS to reach deep into areas like the lungs or colon with incredible accuracy. Right now, the industry is propelled because it makes surgery much less scary for patients. Instead of large incisions, these robots allow for tiny entry points, which means less pain and a much faster trip home. It's growing fast at about 14.65% each year. While big hospitals are the main buyers, smaller outpatient clinics are starting to adopt them too. From a business perspective, it’s a shift from simple tools to smart platforms, led by companies like Intuitive Surgical, where the goal isn't just to see inside the body, but to treat it with more precision than ever before.

- In December 2025, CMR Surgical received U.S. FDA 510(k) clearance for its Versius Plus robotic system for gallbladder removal procedures, strengthening its position in minimally invasive robotic surgery.

- India’s RDI and PLI schemes promote robotics development and medical device manufacturing.

- The UK’s Robotics Adoption Programme encourages hospital adoption of robotic technologies.

- The EU’s Horizon Europe programme funds research in medical robotics and AI.

- U.S. SBIR and NIH programs support early-stage development and commercialisation.

Notable Insights: -

- North America is anticipated to hold approximately 38% share of the Global Robotic Endoscopy Devices Market over the predicted timeframe.

- Asia Pacific is the fastest-growing region in the Global Robotic Endoscopy Devices Market during the forecast period, holding approximately 30% share.

- By product type, the robotic endoscopy systems segment dominated the market and holds approximately 45% share in 2025 and is projected to grow at a substantial CAGR during the forecast period.

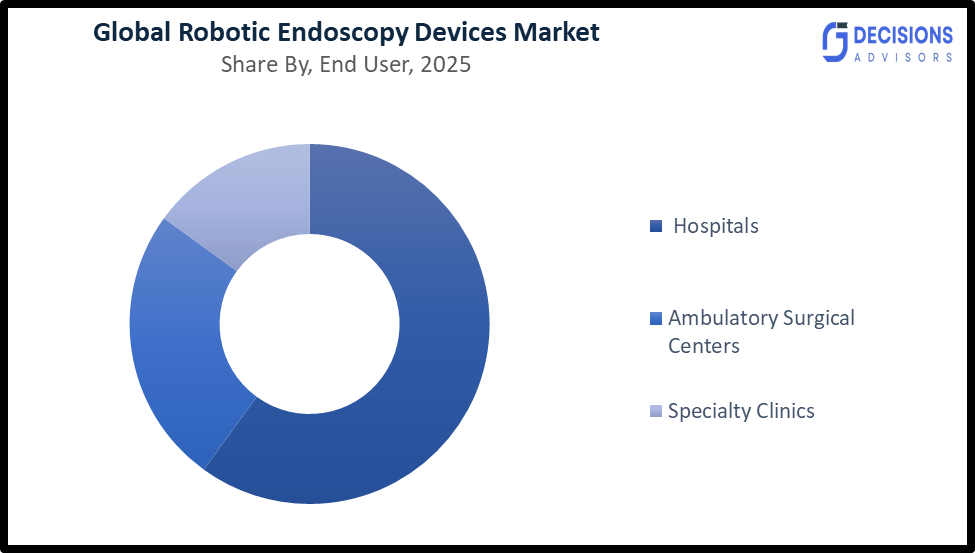

- By end user, the hospitals segment dominated the market and holds approximately 55% share in 2025 and is projected to grow at a substantial CAGR during the forecast period.

- The compound annual growth rate of the global robotic endoscopy devices market is 9.01%.

- The market is likely to achieve a valuation of USD 6.28 Billion by 2035.

What is the role of technology in grooming the market?

Technology plays a crucial role in shaping the robotic endoscopy devices market by significantly enhancing precision, visualization, and procedural efficiency. Advanced innovations such as AI-assisted navigation, 3D high-definition imaging, and robotic articulation systems enable physicians to perform complex minimally invasive procedures with greater accuracy and control. These technologies reduce human error, improve diagnostic capabilities, and shorten recovery times for patients. Additionally, integration with digital platforms and data analytics allows real-time monitoring and better clinical decision-making, further accelerating the adoption of robotic endoscopy systems across healthcare facilities.

Market Drivers

The real engine behind this market is a shift in how we think about surgery, it's becoming less about the big operation and more about precision and recovery. Patients today expect to get back to their lives quickly, and robotic endoscopy makes that possible by replacing huge cuts with tiny, steady movements that reduce pain and hospital stays. This human demand is meeting a perfect storm of technology, where AI and smart navigation act like a high-tech co-pilot for doctors, helping them spot minute signs of cancer or disorders that might have been missed by the human eye alone. At the same time, the market is seeing a drastic demographic shift. As the global population ages, the need for regular screenings for things like colon or lung health is skyrocketing. To keep up, healthcare is trending out of giant, crowded hospitals and into smaller, local outpatient clinics, which are snatching up these robots to make SOP faster and safer. Finally, there's a huge focus on safety, the Shift toward single-use, disposable parts means patients don't have to worry about the cleanliness of the equipment, making the whole experience feel more modern, reliable, and tailored to the individual.

Restrain

The robotic endoscopy devices market faces several restraints, primarily due to the high cost of robotic systems and their maintenance, which limits adoption in cost-sensitive regions. Additionally, the need for specialized training and skilled professionals to operate these advanced systems can slow implementation. Regulatory approval processes are often complex and time-consuming, delaying product launches.

Competitive Analysis:

The report offers the appropriate analysis of the key organisations/companies involved within the global robotic endoscopy devices market, along with a comparative evaluation primarily based on their product of offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborate analysis focusing on the current news and developments of the companies, which includes product development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

Top Companies in the Global Robotic Endoscopy Devices Market

- Intuitive Surgical, Inc.

- Medtronic Plc

- Johnson & Johnson (Auris Health / Ethicon)

- Olympus Corporation

- Boston Scientific Corporation

- Fujifilm Holdings Corporation

- Stryker Corporation

- KARL STORZ SE & Co. KG

- Asensus Surgical, Inc.

- Medrobotics Corporation

Government Initiatives

|

Country |

Key Government Initiatives |

|

India |

|

|

US |

The National Institutes of Health (NIH) awarded USD 1.8 million (SBIR Phase II grant) to Virtuoso Surgical for developing a robotic endoscopic surgical system. |

|

UK |

The NHS funded approximately £4 million investment at The Christie Hospital for upgrading to advanced da Vinci robotic systems, improving cancer treatment and minimally invasive procedures. |

Study on the Supply, Demand, Distribution, and Market Environment of the Global Robotic Endoscopy Devices Market

The global robotic endoscopy devices market operates within a technologically advanced healthcare ecosystem where demand is driven by the rising prevalence of chronic diseases, increasing preference for minimally invasive procedures, and growing adoption of robotic-assisted surgeries in hospitals. Supply is primarily managed by leading medical device manufacturers with strong R&D capabilities and global distribution networks, ensuring availability through hospitals, speciality clinics, and surgical centres. Distribution is concentrated in developed regions, while emerging markets are gradually expanding through partnerships and healthcare investments. The market environment is highly regulated, with strict approval standards to ensure safety, precision, and clinical effectiveness, which play a critical role in shaping product innovation and market entry.

Price Analysis and Consumer Behaviour Analysis

The price analysis of the robotic endoscopy devices market indicates a premium pricing structure, with advanced robotic systems costing 2–5 times higher than conventional endoscopy systems, often ranging from USD 500,000 to over USD 2 million, depending on capabilities. This high cost creates moderate price sensitivity, particularly in developing regions. From a consumer behaviour perspective, hospitals and large healthcare institutions are the primary buyers, prioritising long-term clinical benefits over upfront costs. Notably, over 60% of tertiary care hospitals in developed regions are increasingly investing in robotic-assisted technologies, reflecting a growing preference for precision, improved patient outcomes, and reduced post-operative complications despite the higher initial investment.

Market Segmentation

The Global Robotic Endoscopy Devices Market is classified into product type, application, and end user.

- The robotic endoscopy systems segment dominated the market and holds approximately 45% share in 2025 and is projected to grow at a substantial CAGR during the forecast period.

Based on the product type, the global robotic endoscopy devices market is divided into robotic endoscopy systems, capsule endoscopy devices, visualisation & imaging systems, and accessories. Among these, the robotic endoscopy systems segment dominated the market and holds approximately 45% share in 2025 and is projected to grow at a substantial CAGR during the forecast period. This dominance is attributed to their advanced capabilities, including enhanced precision, flexible navigation, and real-time 3D visualisation, making them highly effective for complex minimally invasive procedures. These systems are widely used in hospitals for gastrointestinal and pulmonary interventions. For instance, robotic-assisted platforms developed by leading companies such as Intuitive Surgical and Medtronic are increasingly adopted for improved clinical outcomes and reduced procedural risks, supporting segment growth.

- The gastroenterology segment accounted for the largest share of approximately 50% in 2025 and is anticipated to grow at a significant CAGR during the forecast period.

Based on the application, the global robotic endoscopy devices market is divided into gastroenterology, pulmonology, urology, gynaecology, and others. Among these, the gastroenterology segment accounted for the largest share of approximately 50% in 2025 and is anticipated to grow at a significant CAGR during the forecast period. This is primarily due to the rising prevalence of gastrointestinal disorders such as colorectal cancer, inflammatory bowel disease, and gastrointestinal bleeding, which require accurate diagnosis and minimally invasive treatment. Robotic endoscopy devices are extensively used for procedures such as colonoscopy, biopsy, and tumour removal. For example, robotic-assisted colonoscopy systems are increasingly utilised for early cancer detection and precise lesion targeting, significantly boosting demand in this segment.

- The hospitals segment dominated the market and holds approximately 55% share in 2025 and is projected to grow at a substantial CAGR during the forecast period.

Based on the end user, the global robotic endoscopy devices market is divided into hospitals, ambulatory surgical centers, and specialty clinics. Among these, the hospitals segment dominated the market and holds approximately 55% share in 2025 and is projected to grow at a substantial CAGR during the forecast period, owing to the availability of advanced infrastructure, skilled professionals, and higher patient inflow for complex procedures. Hospitals are the primary adopters of robotic endoscopy systems due to their ability to handle high-cost equipment and perform specialised surgeries. Additionally, the increasing number of minimally invasive procedures performed in hospital settings further supports segment growth. For instance, large multi-speciality hospitals globally are integrating robotic endoscopy platforms to enhance surgical precision and patient outcomes.

Strategies to Implement for Growth of the Market in Non-Leading Regions

To drive growth in non-leading regions, companies in the robotic endoscopy devices market should focus on developing cost-effective and scalable robotic solutions to improve affordability. Strategic partnerships with local hospitals, distributors, and government bodies can enhance market penetration and accessibility. Expanding training programs and skill development initiatives for healthcare professionals is essential to overcome operational barriers. Additionally, increasing awareness about the benefits of minimally invasive procedures and investing in healthcare infrastructure will support adoption. Offering flexible financing models and after-sales support can further encourage hospitals in emerging markets to adopt robotic endoscopy technologies.

Regional Segment Analysis of the Global Robotic Endoscopy Devices Market

- North America (U.S., Canada, Mexico)

- Europe (Germany, France, U.K., Italy, Spain, Rest of Europe)

- Asia-Pacific (China, Japan, India, Rest of APAC)

- South America (Brazil and the Rest of South America)

- The Middle East and Africa (UAE, South Africa, Rest of MEA)

North America is anticipated to hold approximately 38% share of the Global Robotic Endoscopy Devices Market over the predicted timeframe.

North America is anticipated to hold approximately 38% share of the global robotic endoscopy devices market over the predicted timeframe. it maintains a dominant market position due to advanced healthcare infrastructure, high adoption of robotic-assisted surgical technologies, and the strong presence of key market players. The United States is the key contributor, supported by the increasing prevalence of gastrointestinal disorders and high healthcare expenditure. For instance, hospitals across the U.S. widely use robotic endoscopy systems for minimally invasive procedures such as colonoscopy and tumour removal. Additionally, recent developments such as increased investments in robotic platforms by companies like Intuitive Surgical and Medtronic are further strengthening the region’s leadership.

Asia Pacific is the fastest-growing region in the Global Robotic Endoscopy Devices Market during the forecast period, holding approximately 30% share.

Asia Pacific is the fastest-growing region in the global robotic endoscopy devices market during the forecast period, holding approximately 30% share. This growth is driven by rising healthcare investments, increasing patient population, and growing awareness of minimally invasive procedures in countries such as China, India, and Japan. The region is witnessing strong adoption of robotic endoscopy devices for early diagnosis and treatment of chronic diseases. For example, hospitals in China and India are increasingly adopting robotic-assisted endoscopy systems for gastrointestinal and pulmonary procedures. Additionally, government initiatives to modernise healthcare infrastructure and expand access to advanced medical technologies are accelerating market growth.

Europe is expected to hold approximately 22% share and is the third-largest region in the Global Robotic Endoscopy Devices Market during the forecast period.

Europe is expected to hold approximately 22% share and is the third-largest region in the global robotic endoscopy devices market during the forecast period. The region’s growth is supported by strong regulatory frameworks, increasing adoption of minimally invasive procedures, and growing investments in healthcare innovation. Countries such as Germany, France, and the United Kingdom are leading the market due to rising demand for advanced diagnostic and surgical technologies. For instance, healthcare facilities across Europe are increasingly integrating robotic endoscopy systems to improve procedural accuracy and patient outcomes. Additionally, ongoing research and product innovation by key medical device companies are contributing to market expansion.

Future Market Trends in the Global Robotic Endoscopy Devices Market:

1. Integration of AI and Advanced Imaging Technologies

The market is witnessing rapid integration of artificial intelligence, machine learning, and high-definition/3D imaging systems to enhance diagnostic accuracy and procedural precision. These technologies enable real-time data analysis, improved lesion detection, and better navigation during complex procedures, significantly improving clinical outcomes.

2. Rising Adoption of Minimally Invasive and Outpatient Procedures

There is a strong shift toward minimally invasive surgeries (MIS) due to benefits such as faster recovery, reduced complications, and shorter hospital stays. This trend is also driving the transition toward outpatient and ambulatory surgical settings, increasing the demand for compact and efficient robotic endoscopy systems.

3. Expansion of Therapeutic Applications Beyond Diagnostics

Robotic endoscopy is evolving from purely diagnostic use to advanced therapeutic interventions such as tumour resection, biopsy, and stent placement. This expansion is creating new revenue opportunities and increasing the clinical value of robotic systems across gastroenterology, pulmonology, and oncology.

Recent Development

- In December 2025, Medtronic secured FDA clearance for its Hugo soft tissue robotic system, marking a major step toward expanding its robotic-assisted surgery footprint in the U.S. market.

- In September 2025, Olympus Corporation commercially launched its OLYSENSE AI-powered endoscopy platform across the U.S. and Europe, enabling real-time lesion detection and improved diagnostic accuracy in gastrointestinal procedures.

- In July 2025, Olympus Corporation partnered with Revival Healthcare Capital to co-found Swan EndoSurgical, focusing on the development of advanced endoluminal robotic systems for minimally invasive GI treatments, with potential funding up to $458 million.

- In October 2024, Olympus received CE approval for cloud-based AI endoscopy solutions (CADDIE, CADU, SMARTIBD), marking a major step toward building an intelligent robotic endoscopy ecosystem integrating AI and data-driven diagnostics.

Market Segment

This study forecasts revenue at global, regional, and country levels from 2020 to 2035. Decision Advisors has segmented the global robotic endoscopy devices market based on the below-mentioned segments:

Global Robotic Endoscopy Devices Market, By Product Type

- Robotic Endoscopy Systems

- Capsule Endoscopy Devices

- Visualization & Imaging Systems

- Accessories

Global Robotic Endoscopy Devices Market, By Application

- Gastroenterology

- Pulmonology

- Urology

- Gynecology

- Others

Global Robotic Endoscopy Devices Market, By End User

- Hospitals

- Ambulatory Surgical Centers

- Specialty Clinics

Global Robotic Endoscopy Devices Market, By Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa

Frequently Asked Questions (FAQ)

Q1. What is the average lifespan of robotic endoscopy devices?

A. The lifespan of robotic endoscopy systems typically ranges from 7 to 10 years, depending on usage, maintenance, and technological upgrades.

Q2. How much training is required for surgeons to operate robotic endoscopy systems?

A. Surgeons usually require specialized training programs that can last from a few weeks to several months, including simulation-based practice and supervised procedures.

Q3. Are robotic endoscopy devices covered under health insurance or reimbursement policies?

A. Coverage varies by country and healthcare system, but many developed regions are increasingly including robotic-assisted procedures under reimbursement frameworks due to improved patient outcomes.

Q4. What are the key maintenance requirements for robotic endoscopy systems?

A. These systems require regular software updates, calibration, sterilization of components, and periodic servicing, often supported through annual maintenance contracts.

Q5. How do robotic endoscopy devices impact procedure time compare to traditional methods?

A. While initial setup time may be longer, robotic endoscopy can reduce overall procedure time in complex cases due to improved precision, control, and reduced need for repeat interventions.

Check Licence

Choose the plan that fits you best: Single User, Multi-User, or Enterprise solutions tailored for your needs.

We Have You Covered

- 24/7 Analyst Support

- Clients Across the Globe

- Tailored Insights

- Technology Tracking

- Competitive Intelligence

- Custom Research

- Syndicated Market Studies

- Market Overview

- Market Segmentation

- Growth Drivers

- Market Opportunities

- Regulatory Insights

- Innovation & Sustainability

Report Details

| Scope | Global |

| Pages | 210 |

| Delivery | PDF & Excel via Email |

| Language | English |

| Release | Apr 2026 |

| Access | Download from this page |