Global Solid-State Lasers for Data Storage Market

Global Solid-state lasers for data storage Market Size, Share, By Laser Type (Erbium-Doped Lasers, Titanium-Sapphire Lasers, Neodymium-Doped Yttrium Aluminium Garnet (Nd:YAG) Lasers, and Yttrium Orthovanadate (Nd:YVO?) Lasers), By Wavelength (Infrared Lasers, Visible Lasers, Ultraviolet Lasers, and Multi-Wavelength Systems), By Application (Optical Discs (CD, DVD and Blu-ray), Archival Storage, Holographic Data Storage, and 3D Optical Data Storage), and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2026?2035.

REPORT COVERAGE

Global

Market Snapshot

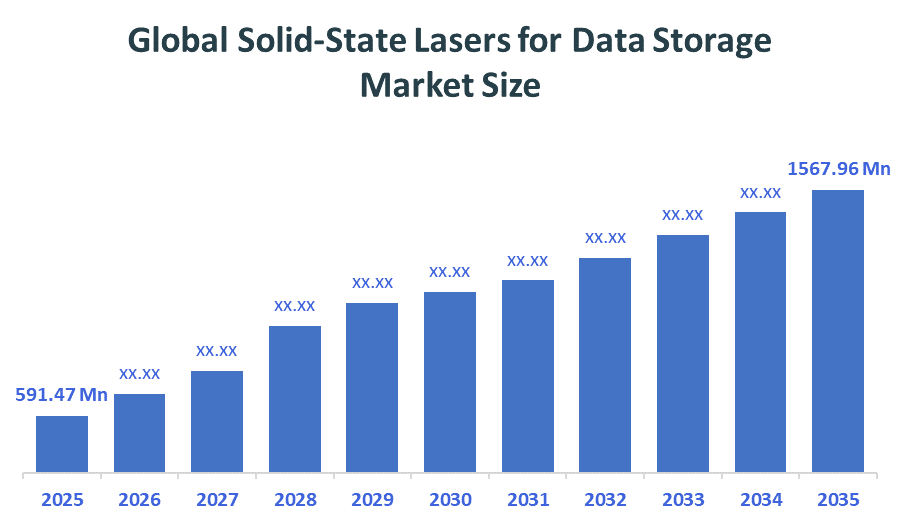

- Market Size (2025): USD 591.47 Million

- Projected Market Size (2035): USD 1567.96 Million

- Compound Annual Growth Rate (CAGR): 10.24%

- Largest Regional Market: Asia Pacific

- Fastest Growing Region: North America

- 3rd Largest Region: Europe

- Base Year: 2025

- Historical Period: 2021–2024

- Forecast Period: 2026–2035

According to Decision Advisors, the Global Solid-State Lasers for Data Storage Market Size is expected to grow from USD 591.47 million in 2025 to USD 1567.96 million by 2035, at a CAGR of 10.24% during the forecast period 2026-2035. Global Solid-state lasers for data storage market are expected to experience substantial growth over the forecast period due to increasing demand for high-speed data storage solutions, advancements in laser technology, miniaturization of devices, and growing adoption across cloud computing and consumer electronics.

Market Overview/ Introduction

The Global Solid-State Lasers for Data Storage Market comprise laser equipment used in optical media to save digital files has been developed that incorporates solid-state technology into the laser mechanisms. Solid-state lasers incorporate solid-state gain media (e.g., crystals and/or glasses exposed to rare-earth ions), which allow the lasers to provide high-coherence light used for saving information digitally. Optical storage devices that use lasers as a means of saving digital files include DVDs, audio CDs and Blu-rays, and they also are commonly used in data centres for storage systems that support very large data sets. The primary driver of growth for solid-state lasers in the digital-storage industry is the continued increase in demand for higher-capacity, faster and more reliable solutions for storing digital files, all of which are required for efficient cloud computing, enterprise data management and consumer electronics. Significant advancements in technology such as blue-violet lasers allowing for ultra-high density of optical storage, multi-wavelength laser systems, miniaturization of lasers with an energy efficiency focus, advancements in cooling systems for lasers, the laser modulation technology, and incorporation of next-generation optical storage architectures all supporting the increased acceptance of laser-based systems. Investment in research and development has also been extremely beneficial to the expanded use of solid-state laser technology, as the major companies that manufacture lasers are working to improve the lasers performance to meet the ever-changing requirements of digital-storage applications globally.

- November 2025, The National Quantum Mission (NQM) launched supports development of indigenous high-precision, compact diode lasers, which are crucial for quantum computing-based high-density data storage, advancing India’s capabilities in solid-state laser technologies and next-generation storage solutions.

- The RDI Scheme, July 2025, with a ?1?lakh?crore outlay, supports commercialization of deep-tech innovations from TRL?4 and above, including laser-based and data storage research, aiming to boost India’s strategic technology development and private-sector R&D capabilities.

- In March 2026, a solid-state laser and photonic beam switching initiative was highlighted, enabling all-optical circuit switching for AI/cloud data centres, supporting ultra-low-latency, energy-efficient storage access, with NVIDIA investing $2B in Coherent for next-gen photonic optics.

Notable Insights: -

- Asia-Pacific holds the largest regional market share approximately 45% in the global Solid-state lasers for data storage market.

- North America is the fastest growing region market share approximately 43% in the global Solid-state lasers for data storage market.

- By laser type, the neodymium-doped yttrium aluminium garnet (Nd:YAG) lasers segment held a dominant position with 28% in terms of market share in 2025.

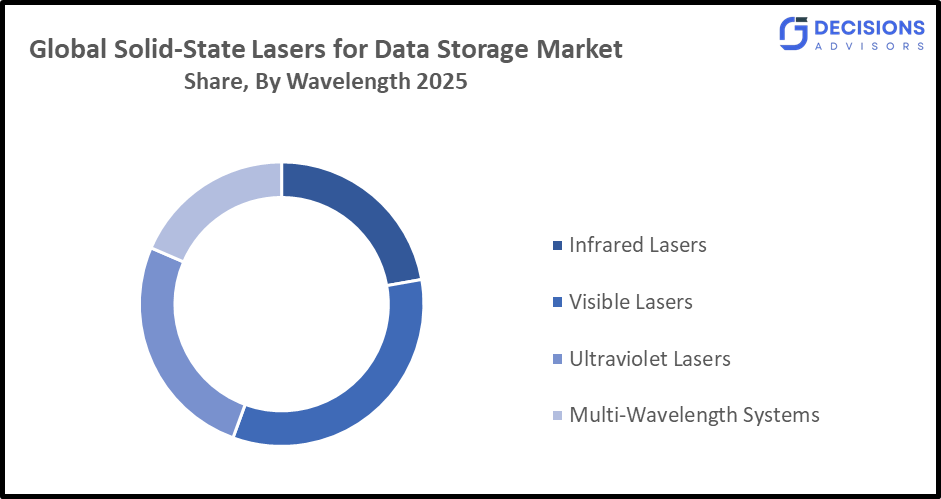

- By wavelength, visible lasers segment is the dominating accounting for over 48% of the global market share in 2025.

- By application, optical discs (CD, DVD and Blu-ray) segment is the dominating accounting for market is approximately 40%.

- The market is likely to achieve a valuation of USD 1567.96 million by 2035.

What is role of technology in grooming the market?

Technology significantly drives the solid?state lasers for data storage market by improving performance, precision and adoption. Advances like compact, energy?efficient laser modules and higher?precision beam control boost data density and speed. Nearly 65?% of new product launches are technology?driven, underscoring its role in innovation. The market, valued at roughly USD?540?million in 2024, is projected to grow to about USD?926?million by 2031 at approximately 8?% CAGR, supported by ongoing miniaturization and optical advancements.

How is Recent Developments Helping the Market?

Recent technological developments are significantly boosting the solid?state lasers for data storage market by enhancing storage capacity, precision, and new applications. Innovations in laser miniaturization and beam accuracy have increased adoption in over 54?% of storage platforms, improving energy efficiency and read/write speeds. Advancements in optical materials and multi?layer recording methods support higher data densities and reliability. Breakthrough optical storage research, including femtosecond lasers for volumetric data encoding, further expands future long?term archival solutions.

Market Drivers

Market drivers currently include the increased demand for both high speed and high-capacity data storage, with more than 62% of data centres deploying solid-state lasers (SSL) to increase performance and reliability for reading and writing. Approximately 54% of advanced storage systems are now using compact and energy-efficient laser modules, 66% of enterprises that require high-speed archival solutions use SSLs for real-time processing. Ongoing advances in technology and continued digital data growth are driving further growth in the marketplace. Technological advancements like blue-violet lasers, multi-wavelength systems, and miniaturized energy-efficient modules enhance storage density and reliability. Rising adoption of optical storage solutions for secure, long-term data retention and increasing investments in research and development to improve laser performance and durability further propel market growth. The shift toward digital transformation globally also fuels strong demand for advanced solid-state laser technologies.

Restrain

Restraints in the solid?state lasers for data storage market include high manufacturing and integration costs, limiting adoption in cost-sensitive segments. Technical challenges such as heat generation, material degradation, and complex cooling requirements can affect performance and lifespan. Additionally, increasing competition from alternative storage technologies, like SSDs and cloud-based solutions, may slow the market’s growth despite technological advancements.

Competitive Analysis:

The report offers the appropriate analysis of the key organizations/companies involved within the Solid-state lasers for data storage market, along with a comparative evaluation primarily based on their product of offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes Application development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

Top Companies in Global Solid-state lasers for data storage Market

- Coherent Inc

- IPG Photonics

- TRUMPF SE

- nLIGHT Inc

- Lumentum Holdings Inc

- Jenoptik AG

- Novanta Inc

- Lumibird SA

- Wuhan Raycus Fiber Laser Technologies Co Ltd

- Hans Laser Technology Industry Group Co Ltd

- Maxphotonics Co Ltd

- EKSPLA

Government Initiatives

|

Country |

Key Government Initiatives |

|

U.S. |

The U.S. CHIPS and Science Act, with $52.7?billion for domestic chip R&D and $39?billion in manufacturing incentives, boosts semiconductor and photonics production, including laser diodes for solid-state lasers in optical storage and data-centre photonics. |

|

USA |

DARPA and U.S. DoD expand solid?state laser research, emphasizing high?power directed energy systems and photonic transceivers under defence programs, focusing on battlefield applications and communications rather than data storage technologies. |

|

China |

China’s National Key R&D Program and NSFC funded femtosecond laser optical storage research, including multi?layer high?capacity 5D storage projects supported under Program No.?2022YFC3310300 and related grants in 2024–2025. |

Study on the Supply, Demand, Distribution, and Market Environment of Energy Management Systems Market

The Solid?state Lasers for Data Storage market is shaped by dynamic supply, demand, and distribution factors within a technology-driven environment. Supply is led by key players like Coherent Inc., IPG Photonics, and TRUMPF SE, providing advanced laser modules through OEM partnerships. Demand is rising due to growing data volumes, cloud computing, and high-density storage, with over 62?% of data centres adopting solid-state lasers. Distribution occurs via OEMs, distributors, and online channels, targeting enterprise and consumer segments. The market environment emphasizes technological innovation, energy-efficient systems, and multi-wavelength lasers, while high costs and competition from SSDs present challenges, aligning indirectly with broader energy management trends.

Price Analysis and Consumer Behaviour Analysis

Price Analysis: Solid?state lasers for data storage are expensive due to advanced materials, precision optics, and complex manufacturing, with high-performance, multi-wavelength, and enterprise-grade modules priced at a premium. Miniaturized modules benefit from cost reductions through scaled production. Consumer Behaviour Analysis: Enterprises and data centres prioritize reliability, speed, and long-term durability over price, driving adoption of premium lasers. OEMs focus on modular, scalable components, while small businesses and research labs prefer affordable, compact modules. Overall, performance and efficiency outweigh cost in purchasing decisions, especially for mission-critical storage applications.

Market Segmentation

The Solid-state lasers for data storage market share are classified into laser type, wavelength, and application.

- The Neodymium-Doped Yttrium Aluminium Garnet (Nd:YAG) Lasers segment dominated the market in 2024, and is projected to grow at a substantial CAGR of approximately 28% during the forecast period.

Based on the Laser type, the Solid-state lasers for data storage market are divided into erbium-doped lasers and titanium-sapphire lasers, neodymium-doped yttrium aluminium garnet (Nd:YAG) lasers, and yttrium orthovanadate (Nd:YVO?). Among these, the neodymium-doped yttrium aluminium garnet (Nd:YAG) Lasers segment dominated the solid?state lasers for data storage market due to their high output power, reliability, and versatility in continuous and pulsed applications. In 2024, the Nd:YAG segment held the largest share of approximately 28?%, reflecting widespread adoption in optical storage systems. Other types like Nd:YVO?, Erbium-doped, and Titanium-Sapphire lasers are used in niche or research applications, but Nd:YAG’s performance and mature supply chain make it the market leader.

- The Visible lasers segment accounted for the largest share in 2024, and is anticipated to grow at a significant CAGR of approximately 48% during the forecast period.

Based on the Wavelength, the Solid-state lasers for data storage market are divided into infrared lasers, visible lasers, and ultraviolet lasers. Among these, visible lasers dominate the solid?state lasers for data storage market due to their ability to achieve higher data density and precision, essential for Blu?ray, DVD, and advanced optical storage systems. Shorter visible wavelengths, particularly blue-violet (~405?nm), enable tighter laser spot focusing, increasing storage capacity. Infrared lasers are mainly used in legacy CD/DVD systems, while ultraviolet lasers remain niche due to cost and complexity. Visible lasers currently account for the largest market share, around 45–50?% in 2024, reflecting widespread adoption.

- The optical discs segment (CD, DVD, Blu-ray) segment dominated the market in 2024, and is projected to grow at a substantial CAGR of approximately 40% during the forecast period.

Based on the Application, the Solid-state lasers for data storage market are divided into optical discs (CD, DVD and Blu-ray), archival storage, holographic data storage, defence, telecommunications, others, pathology & cancer staging. Among these, the Optical Discs segment (CD, DVD, Blu-ray) dominates the solid?state lasers for data storage market due to widespread consumer and enterprise use for media storage, backup, and distribution. Blu-ray adoption, in particular, drives demand for high-precision blue-violet lasers, enabling higher data density. This segment accounted for the largest share of approximately 40?% in 2024, reflecting its established infrastructure, affordability, and compatibility with existing playback devices, while emerging applications like holographic and archival storage are growing but remain smaller in comparison.

Strategies to Implement for Growth of the Market in Non-Leading Regions

To grow the solid?state lasers for data storage market in non-leading regions, companies should focus on strategic partnerships with local OEMs and distributors, enabling wider adoption. Affordable, compact laser modules can attract cost-sensitive customers. Investing in regional R&D and service centers ensures better support and customization. Awareness campaigns and training programs can educate end-users on performance benefits. Additionally, government collaborations and incentives for advanced storage technologies can accelerate penetration, while adapting solutions to local infrastructure and energy efficiency needs enhances market growth.

Regional Segment Analysis of the Solid-state lasers for data storage Market

- North America (U.S., Canada, Mexico)

- Europe (Germany, France, U.K., Italy, Spain, Rest of Europe)

- Asia-Pacific (China, Japan, India, Rest of APAC)

- South America (Brazil and the Rest of South America)

- The Europe (UAE, South Africa, Rest of MEA)

Asia Pacific is anticipated to hold the largest share of the Solid-state lasers for data storage market over the predicted timeframe.

The Asia Pacific region is expected to hold the largest share of the solid?state lasers for data storage market due to rapid industrialization, electronics manufacturing, and data centre expansion, particularly in China, Japan, South Korea, and India. Strong local supply chains and R&D investments further support growth. Across broader solid?state laser industries, Asia Pacific accounts for around 30–46?% of global share and is the fastest?growing region, reflecting superior adoption rates and manufacturing scale.

North America is expected to grow at a rapid CAGR in the Solid-state lasers for data storage market during the forecast period. North America is expected to grow at a rapid CAGR in the solid?state lasers for data storage market due to strong demand from data centres, cloud computing, and research institutions. Advanced technology infrastructure, high R&D investment, and OEM collaborations drive adoption of high-performance laser modules. The market in the region is projected to grow from approximately USD?0.87?billion in 2025 to USD?1.24?billion by 2033, representing a CAGR of approximately 4.5?%, reflecting increasing reliance on precision laser technologies.

Europe are the 3rd largest region to grow in the Solid-state lasers for data storage market during the region. Europe is the third-largest region in the solid?state lasers for data storage market, driven by increasing adoption in telecommunications, research laboratories, and industrial manufacturing. Strong government support for advanced photonics and optical storage technologies, along with rising investments in R&D and energy-efficient systems, boosts growth. Key markets include Germany, France, and the UK. The European market is projected to expand steadily, reflecting a growing focus on high-performance, reliable, and energy-efficient solid-state laser solutions for data storage applications.

Future Market Trends in Global Solid-state lasers for data storage Market: -

- High-Density Storage Solutions

The shift toward high-density optical storage is a major trend, driven by the surging demand for massive data storage in cloud computing, hyperscale data centres, and enterprise applications. Blue-violet solid-state lasers and multi-wavelength systems allow tighter data packing on discs and optical media, increasing storage capacity without expanding physical space. This trend also supports long-term archival solutions and faster writes speeds, enabling organizations to efficiently manage growing data volumes. Companies investing in high-density lasers gain a competitive edge in performance-focused markets.

- Energy-Efficient and Miniaturized Laser Modules

Energy efficiency and miniaturization are transforming solid-state laser design. Compact, low-power modules reduce operational costs while allowing integration into portable devices, edge computing hardware, and small-scale storage systems. Advanced thermal management and optimized materials improve reliability and lifespan. The trend aligns with global sustainability goals and rising demand for eco-friendly storage solutions, particularly in regions with high energy costs. Adoption of miniaturized modules also facilitates scalable deployment in enterprise and consumer electronics markets, accelerating penetration in emerging regions.

- Integration with Advanced Optical Technologies

Future growth will increasingly involve integrating solid-state lasers with holographic, 3D, and volumetric optical storage systems. These combinations enhance data density, precision, and retrieval speeds, opening new applications in research, defense, and high-end enterprise storage. Integration supports multi-layer recording and faster parallel access to stored data. This trend also fosters innovation in hybrid storage architectures, enabling solid-state lasers to coexist with other photonics technologies. Companies leveraging these integrations can offer high-performance, reliable, and scalable solutions to meet evolving global data demands.

Recent Development

- March 2026: Researchers advanced holographic data storage using solid-state lasers, encoding information in 3D with amplitude, phase, and polarization. Achieved storage densities exceeding 10?TB/cm³, marking a significant leap for high-capacity optical data storage technologies.

- August 2025: Startups like SPhotonix advance 5D optical data storage using ultrafast solid-state lasers, inscribing data in fused silica. Achieves densities up to 360?TB per disk, with high durability and energy-efficient, multi-dimensional encoding for next-generation storage.

- March 2025: Scientists developed a compact solid-state deep-UV laser generating 193?nm light with 10–50?mW output using cascaded LBO crystals. This supports semiconductor lithography and high-density data manufacturing, enabling precise microfabrication for next-generation storage technologies.

- Early 2026: Solid-state lasers are integrated into photonic circuits, offering linewidth <100?kHz, 10–50?mW output, and SNR >60?dB, enhancing stability, coherence, and Tbps-scale data transfer, supporting next-generation high-speed data storage and optical computing applications.

Market Segment

This study forecasts revenue at global, regional, and country levels from 2020 to 2035. Decision Advisors has segmented the Solid-state lasers for data storage market based on the below-mentioned segments:

Global Solid-state lasers for data storage Market, By Laser Type

- Erbium-Doped Lasers

- Titanium-Sapphire Lasers

- Neodymium-Doped Yttrium Aluminium Garnet (Nd:YAG) Lasers

- Yttrium Orthovanadate (Nd:YVO?) Lasers

Global Solid-state lasers for data storage Market, By Wavelength

- Infrared Lasers

- Visible Lasers

- Ultraviolet Lasers

- Multi-Wavelength Systems

Global Solid-state lasers for data storage Market, By Application

- Optical Discs (CD, DVD and Blu-ray)

- Archival Storage

- Holographic Data Storage

- 3D Optical Data Storage

Global Solid-state lasers for data storage Market, By Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa

Frequently Asked Questions (FAQ)

1. Question: What is the expected market share of solid-state lasers for data storage in emerging regions like Africa and South America specifically?

Answer: The report mentions these regions generally but does not provide specific market size, growth rate, or market share data for Africa, South America, or other emerging markets.

2. Question: What are the projected costs or pricing trends of different solid-state laser modules over the forecast period?

Answer: While the report notes that solid-state lasers are expensive, it does not provide detailed pricing trends, cost per unit, or expected reductions over 2025–2035.

3. Question: What is the competitive landscape for startups and smaller companies in the solid-state laser market?

Answer: The report lists top companies but does not detail the role, market share, or growth of smaller startups and emerging players, except a brief mention of SPhotonix.

4. Question: How much of the global market is currently used specifically for data centre storage versus consumer optical media?

Answer: The report gives application categories but does not quantify the exact market share of solid-state lasers used in enterprise/cloud data centres compared to consumer devices like DVDs and Blu-ray.

5. Question: What are the environmental or sustainability impacts of solid-state laser production and disposal?

Answer: The report mentions energy-efficient designs but does not provide lifecycle analysis, carbon footprint, or sustainability metrics for production, use, and disposal of solid-state lasers.

Check Licence

Choose the plan that fits you best: Single User, Multi-User, or Enterprise solutions tailored for your needs.

We Have You Covered

- 24/7 Analyst Support

- Clients Across the Globe

- Tailored Insights

- Technology Tracking

- Competitive Intelligence

- Custom Research

- Syndicated Market Studies

- Market Overview

- Market Segmentation

- Growth Drivers

- Market Opportunities

- Regulatory Insights

- Innovation & Sustainability

Report Details

| Scope | Global |

| Pages | 210 |

| Delivery | PDF & Excel via Email |

| Language | English |

| Release | Apr 2026 |

| Access | Download from this page |