Global Space Battery Market

Global Space Battery Market Size, Share, By Battery Type (Nickel-Based, Lithium-Based, Silver-Zinc, and Others) By Platform (Satellites, Launch Vehicles, Space Stations, and Rovers/Landers) By Application (Communication, Earth Observation, Navigation, and Scientific Research) By End User (Government & Military, and Commercial) and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa), Analysis and Forecast 2026 - 2035

CAGR

4.5%

REVENUE 2025

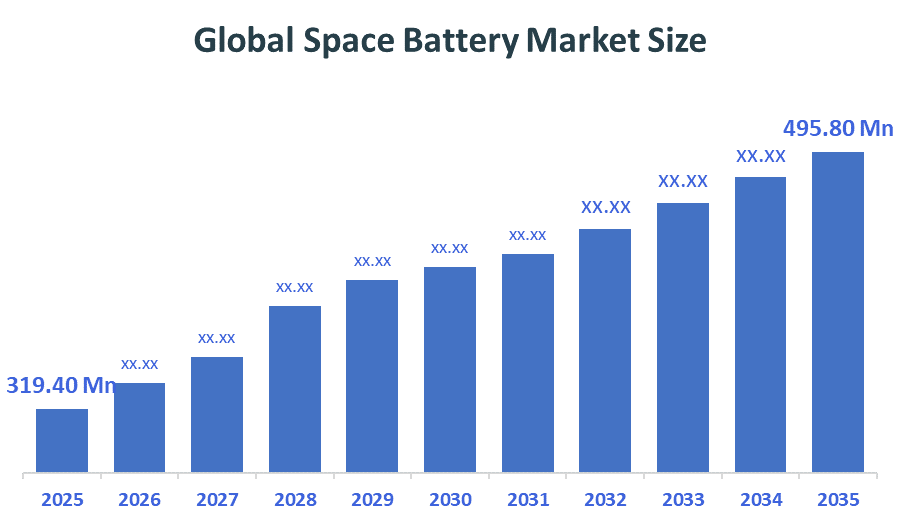

USD Million 319.4

FORECAST 2035

USD Million 495.8

REPORT COVERAGE

Global

The Global Space Battery Market Size was expected to grow from USD 319.40 million in 2025 and is projected to reach around USD 495.80 million by 2035. According to Decision Advisors, a detailed research report on the space battery market shows that the lithium-based technology trend dominates the global space battery market, holding an estimated 30-40% of the total share worldwide. Saft Groupe SAS reported a turnover (revenue) of €1.2 billion in 2025, making it one of the major market drivers for shaping the industry.

Market Snapshot

- Global Space Battery Market Size (2025): USD 319.40 Million

- Global Space Battery Projected Market Size (2035): USD 495.80 Million

- Global Space Battery Compound Annual Growth Rate (CAGR): 4.5%

- Largest Regional Market: North America

- Fastest Growing Region: Asia-Pacific

- 3rd Largest Region: Europe

- Base Year: 2025

- Historical Period: 2021 to 2024

- Forecast Period: 2026 to 2035

Market Overview / Introduction

Space battery systems are energy storage systems designed to facilitate constant power delivery for satellites, orbiters, and lunar exploration equipment. Space batteries act as an essential source of power in eclipse conditions where solar panels fail to deliver any energy, through the use of modern electrochemical cells and thermal vacuum protections to enable constant power delivery without experiencing any form of depletion. The current space battery systems have capabilities like radiation hardening and advanced battery management systems to ensure consistent performance and reduce the risk of critical mission hardware failure. The space battery systems were initially large nickel-cadmium batteries that have since evolved into high-density lithium batteries capable of delivering power through smart monitoring technologies and being integrated within autonomous spacecraft bus systems. There has been an increase in the use of space battery systems due to the growing demand for small satellite constellations and long-range explorations within low-earth orbit and other regions. Space battery systems play an essential role in protecting spacecraft assets from experiencing power losses or other forms of electrical interruptions by ensuring constant voltage without the need for massive legacy battery systems.

- The satellite and telecommunications segments contribute to approximately 70% of the application-based use in the market, driven by the increasing demand for LEO constellations, 5G satellite connectivity, and the safeguarding of essential global positioning utility hubs.

- Advanced energy storage technology in the lunar exploration sector is experiencing substantial growth, with a CAGR forecasted to surpass 10% on account of the increasing adoption of rover power systems as part of the advanced generation of planetary landers for providing optimised energy to scientific instruments and survival heaters.

Notable Insights: -

- Lithium-based battery modules make up about 55.4% of the total market share of this sector. They have gained a reputation in high-performance satellite operations, particularly in communication satellites, military surveillance, and deep space probes.

- About 68.2% of all installations occur in commercial satellite networks and government space agencies. These investments are stimulated mainly by high levels of investment into space tourism projects and global internet coverage initiatives because many spacecrafts experience power bottlenecks that result in the loss of critical telemetry.

- Applications of space batteries in the sphere of Earth observation account for almost 38.7% of all demand. The rapid development of climate monitoring sensors, alongside increased worries about weather patterns and resource management, has become one of the main drivers of using these advanced energy systems.

- About 42.1% of the market value belongs to the North American region in 2026. Many organisations within this region, like NASA and private aerospace giants, invest considerable amounts of money in reusable launch vehicles and satellite manufacturing in order to address the growing needs of their expanding space sectors.

What is the Role of Technology in Shaping the Market?

Innovations made in technology have brought revolutionary changes in the space energy sector with regard to energy density, heat resistance, and life cycles. The current space power systems are no longer mere battery systems; rather, they are sophisticated energy management systems that can operate independently over long durations of time because they are capable of using radiation-proof substances, polymer electrolytes, and health monitoring diagnostics.

How are Recent Developments Helping the Market?

Some of the innovations involved include the integration of silicon anodes, introduction of modern solid-state electrolytes, and thermal bypass technology. Innovation has played an instrumental role in helping the industry grow. Some of the innovations involved the development of modular battery packs that can protect all types of space craft components, ranging from miniature nanosatellites to complete manned space stations without exception. With the use of cell balance techniques, these innovations will make sure that energy discharges are managed in an automated fashion through electrochemical state of health monitoring without any errors on the part of humans.

Market Drivers

The demand for global space batteries has increased due to the increase in the investment by governments and private companies in sustainable space presence and power efficient spacecraft, which would be able to meet the objectives of long-term missions currently. The current space batteries have gained wide acceptance among users because of the many advantages that have been realized from combining these different characteristics in a single system, such as high charge efficiency, radiation protection, and lightweight construction. On the other hand, the development of high energy electric propulsion has meant that there is a growing requirement for better sources of energy that can cope with the shift towards electric propulsion in deep space where traditional sources of power are proving difficult.

Restraints

The growth of the international market for the space battery industry is constrained by the difficulties in ensuring the safety of high energy density cells under extreme launch vibrations and thermal cycling conditions because of the possibility of thermal runaway and vacuum leakage.

Competitive Analysis:

The report offers the appropriate analysis of the key organisations/companies involved within the space battery market, along with a comparative evaluation primarily based on their product offerings, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborate analysis focusing on the current news and developments of the companies, which includes product development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

Top 10 Companies in the Global Space Battery Market

- Saft Groupe SAS

- EaglePicher Technologies

- GS Yuasa Corporation

- EnerSys

- Northrop Grumman Corporation

- Lockheed Martin Corporation

- Boeing

- Mitsubishi Electric Corporation

- Maxell, Ltd.

- NanoAvionics

Government Initiatives

|

Country |

Key Government Initiatives |

|

US |

In alignment with the NASA Space Technology Mission Directorate (STMD) umbrella solicitation for FY 2026, the federal government has intensified funding for the SpaceTech REDDI program. This initiative allocates significant grants to develop high-capacity energy storage and advanced battery chemistries, such as silicon anodes and solid-state cells, to support the Artemis lunar surface power requirements and long-duration deep space exploration. |

|

EU |

Under the Horizon Europe Work Programme 2026-2027, the European Commission has dedicated approximately €4.9 billion to climate and industrial competitiveness actions, which includes specific funding for advanced energy storage and battery research. Additionally, the ESA (European Space Agency) has implemented the Energy Storage Initiative to accelerate the development of European space-based power solutions and ensure strategic autonomy in mission-critical battery hardware. |

|

India |

In the Union Budget 2026-27, the Indian government introduced a Basic Customs Duty (BCD) exemption on capital goods used for manufacturing Lithium-Ion cells. This policy is designed to lower project costs for domestic energy storage ecosystems. Furthermore, the government has increased support for ISRO’s technology transfer programs, facilitating the commercialization of space-grade battery technologies to private Indian aerospace firms to bolster the national space economy. |

Study on the Supply, Demand, Distribution, and Market Environment

Sustainability in the space battery market is all about achieving an equilibrium where performance in terms of optimal electrical reliability matches up to the increased demands for weight reduction in relation to energy management. The production process involved in supplying the space batteries revolves around manufacturing chemical compositions that have maximum capacity and electronic designs that maximise power delivery and stability while remaining lightweight.

Price Analysis and Consumer Behaviour Analysis

Space battery prices are determined based on their capacity, history of flights, and certification of safety. Space batteries utilising the highest-grade solid-state batteries, which are fitted with sophisticated radiation-hardened management sensors along with thermal protection systems, cost more. Nevertheless, conventional lithium-ion batteries, particularly those for CubeSat or micro-satellite use, are relatively affordable and present an excellent platform for inexpensive orbital operations and education-based research in the emerging space market. Customers have shown a preference for high energy density and reliability; therefore, agencies should be expected to opt for space batteries that guarantee operational independence, system compatibility, and accurate power provision.

Market Segmentation

The Global Space Battery Market share is classified into battery type, platform, application, and end user.

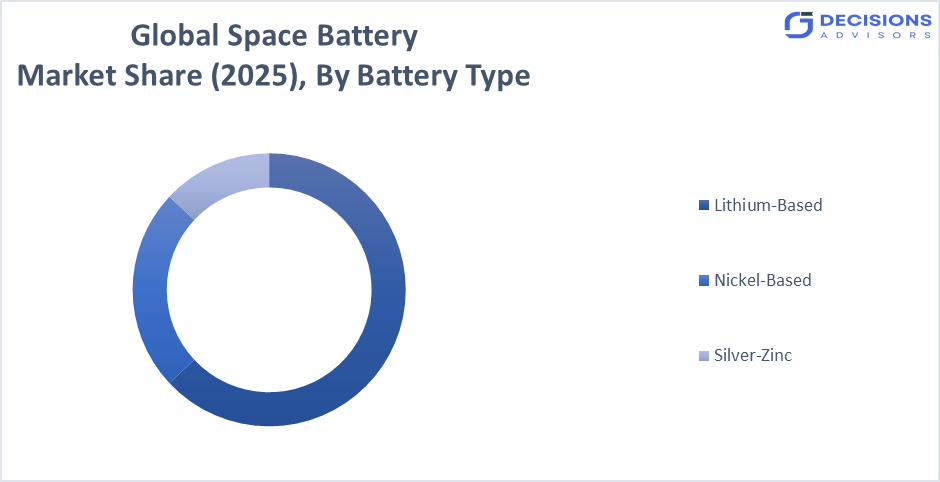

The Lithium-Based segment holds the largest share, contributing approximately 58% of the market in 2025.

Based on the Battery Type, the global space battery market is divided into Nickel-Based, Lithium-Based, Silver-Zinc, and Others. Among these, the Lithium-Based segment holds the largest share, contributing approximately 58% of the market in 2025. The reason for this dominance lies in their ability to perform better in terms of energy-to-weight ratio in mass-sensitive spacecraft and their ability to provide high discharge rates for propulsion and communication subsystems without consuming excessive volume compared to the nickel-cadmium alternatives. The nickel and silver zinc variants represent the other major segments in this market, but they still remain relevant due to their proven safety in specific manned missions.

The Satellites segment accounts for the largest share, representing over 65% of the global market in 2025.

Based on the Platform, the global space battery market is divided into Satellites, Launch Vehicles, Space Stations, and Rovers/Landers. Among these, the Satellites segment accounts for the largest share, representing over 65% of the global market in 2025. These deployments are critical for maintaining the operational continuity of global communication, improving earth monitoring, and reducing the need for frequent replacement through the adoption of modern, long life battery packs. On the other hand, the Rovers/Landers segment has emerged as a rapidly growing sector, thanks to the increasing adoption of lunar and martian exploration missions and the transition to high power instruments for planetary science.

Communication dominates the global market, accounting for approximately 54% of the total revenue in 2025.

Based on the Application, the global space battery market is divided into Communication, Earth Observation, Navigation, and Scientific Research. Among these, Communication dominates the global market, accounting for approximately 54% of the total revenue in 2025. This segment is preferred by operators who require large-scale constellations and professional energy engineering services for complex internet and broadcasting infrastructure. The Earth Observation category is seeing a sharp increase in use, especially in the deployment of high-resolution imaging satellites, where sophisticated power management is required to maintain sensor performance.

The Government & Military segment dominates the global market, accounting for approximately 55% of the total revenue in 2025.

Based on the End User, the global space battery market is divided into Government & Military and Commercial. Among these, the Government & Military segment dominates the global market, accounting for approximately 55% of the total revenue in 2025. This segment is preferred by defense agencies that require high security solutions and professional orbital engineering services for complex surveillance and national security satellites. The Commercial segment is seeing a sharp increase in use, especially by private aerospace firms in the satellite broadband industry who value the efficiency and cost effectiveness of automated energy systems for large constellations.

Strategies to Implement for Growth of the Market in Non-Leading Regions

Growth possibilities for the space battery sector in developing economies may be enhanced through the introduction of effective modular power systems to assist the local space firms, as well as government organizations responsible for managing the satellites. Space sovereignty programs implemented by the government and the growth of small satellite standards make significant contributions towards the demand for the space battery market in developing economies that present considerable difficulties in the establishment of large-scale traditional power plants on the ground. Increased funding for the development of local aerospace engineering specialists, as well as regional test centers, would aid the integration of sustainable power sources and smart batteries.

Regional Segment Analysis of the Global Space Battery Market

- North America (U.S., Canada, Mexico)

- Europe (Germany, France, U.K., Italy, Spain, Rest of Europe)

- Asia-Pacific (China, Japan, India, South Korea, Rest of APAC)

- Latin America (Brazil and the Rest of Latin America)

- The Middle East and Africa (UAE, South Africa, Rest of MEA)

North America is expected to hold a significant share of the space battery market during the forecast period. This region holds approximately 42.1% share of global revenue in 2025, thanks to its highly sophisticated infrastructure related to NASA missions and private space firms, along with the extensive adoption of high energy density technology in both national defense goals and commercial satellite applications. The largest part of this region’s revenues comes from the United States, as there is a lot of spending at the federal level in lunar programs for automated power adoption, along with local research related to solid state space batteries.

Asia-Pacific is projected to be the fastest-growing region over the forecast period. This region is anticipated to witness a growth rate of around 11.45% CAGR, maintaining a rapidly expanding market share within the global industry. In 2025, the Asia-Pacific already accounts for a significant portion of global revenue. This is owing to the fast-developing space infrastructure, coupled with the growing demand for modern satellite protection in countries such as China, India, and Japan. Other reasons for the same include greater investments made toward indigenous satellite manufacturing, state-supported research projects for low-cost lithium modules, and widespread adoption of smart power management strategies.

Europe is anticipated to hold a substantial share, contributing approximately 21.3% of the global market share. There is a competitive advantage in the region owing to clusters of aerospace technology innovation and financing for sustainable space operations, as well as energy risk management research. There is also a comparative advantage with countries like France, Germany, and the UK, which are highly skilled at precision engineering for high-performance space grade energy units. Moreover, the rigorous safety standards regarding orbital debris and energy efficiency further give them a comparative advantage.

Recent Developments

- In September 2025, NASA and Lockheed Martin formalised a strategic collaboration to integrate next-generation solid-state batteries into the Artemis lunar exploration architecture. This partnership aims to leverage high-energy-density cells that offer a 40% reduction in weight compared to current flight-qualified lithium-ion packs.

- In April 2025, EaglePicher Technologies introduced a modular Space Playbook design that reduced battery development-to-launch timelines from an average of 7.5 years to just 25 months.

- In November 2024, Saft Groupe SAS announced a major contract to provide high-performance Li-ion battery systems for a constellation of over 300 Low Earth Orbit (LEO) telecommunication satellites. The agreement highlights the shift toward scalable, high-cycle-life battery architectures for 5G global connectivity.

- In March 2023, GS Yuasa Corporation celebrated a milestone of 20 years of continuous operation of its lithium-ion cells aboard the International Space Station (ISS). This longevity data has set a new industry benchmark for battery degradation rates in vacuum and microgravity environments.

Market Segmentation

This study forecasts revenue at global, regional, and country levels from 2021 to 2035. The Global Space Battery Market is segmented based on the following categories:

Global Space Battery Market, By Battery Type

- Nickel-Based

- Lithium-Based

- Silver-Zinc

- Others

Global Space Battery Market, By Platform

- Satellites

- Launch Vehicles

- Space Stations

- Rovers/Landers

Global Space Battery Market, By Application

- Communication

- Earth Observation

- Navigation

- Scientific Research

Global Space Battery Market, By End User

- Government & Military

- Commercial

Global Space Battery Market, By Regional Analysis

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- United Arab Emirates

- Saudi Arabia

- Qatar

- South Africa

- Rest of Middle East & Africa

Frequently Asked Questions (FAQ)

What is the difference between primary and secondary space batteries?

Primary space batteries are non-rechargeable units that carry all their energy from launch and are discarded once depleted. They are typically used for short-duration tasks, such as launch vehicle stages, missiles, or planetary descent probes, where high power is needed for only a few hours. Secondary batteries are rechargeable and work alongside solar arrays to store energy during sunlight periods for use during the dark eclipse phase of an orbit.

How do space batteries survive the extreme temperature swings in orbit?

Spacecraft experience temperature shifts ranging from -55°C in the shade to over 120°C in direct sunlight. Since traditional convection cooling is impossible in a vacuum, batteries rely on conduction through copper heat sinks and specialised thermal interface materials (TIMs). Most battery packs are also wrapped in Multi-Layer Insulation (MLI) and equipped with internal electric heaters to prevent the electrolyte from freezing during long periods of darkness.

What are the main technical challenges caused by space radiation?

High-energy particles and galactic cosmic rays can cause Single Event Effects (SEE) in the Battery Management System (BMS), leading to data corruption or circuit failure. Over time, cumulative radiation exposure (Total Ionising Dose) degrades the chemical stability of the cells and the efficiency of the protective electronics. To counter this, engineers use radiation-hardened components and aluminium shielding to protect the battery’s sensitive control logic.

What happens to space batteries at the end of a mission?

To mitigate the risk of creating space debris, global regulations require spacecraft to undergo a passivation process at the end of their life. This involves fully discharging the batteries and disconnecting them from the solar arrays to prevent accidental energy buildup. For Low Earth Orbit (LEO) satellites, the batteries must remain intact until the spacecraft performs a controlled re-entry and burns up in the atmosphere.

How are new space batteries tested for the vacuum of space?

Before launch, batteries undergo Thermal Vacuum (TVAC) testing. They are placed in a vacuum chamber that simulates the airless environment of space while being cycled through extreme high and low temperatures. This ensures the battery casing won't leak or outgas (release volatile chemicals) and that the internal electrical connections can withstand the mechanical strain of constant expansion and contraction.

Check Licence

Choose the plan that fits you best: Single User, Multi-User, or Enterprise solutions tailored for your needs.

We Have You Covered

- 24/7 Analyst Support

- Clients Across the Globe

- Tailored Insights

- Technology Tracking

- Competitive Intelligence

- Custom Research

- Syndicated Market Studies

- Market Overview

- Market Segmentation

- Growth Drivers

- Market Opportunities

- Regulatory Insights

- Innovation & Sustainability

Report Details

| Scope | Global |

| Pages | 210 |

| Delivery | PDF & Excel via Email |

| Language | English |

| Release | Apr 2026 |

| Access | Download from this page |