Global Spine Pain Market

Global Spine Pain Market Size, Share, and COVID-19 Impact Analysis, By Disease Type (Sub-Acute, Acute, and Chronic), By End-Use (Orthopaedic Clinics, Hospitals, Ambulatory Surgery Centres, and Others), and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2025-2035

CAGR

5.32%

REVENUE 2024

USD Billion 7.45

FORECAST 2035

USD Billion 13.17

REPORT COVERAGE

Global

Global Spine Pain Market Size Insights Forecasts to 2035

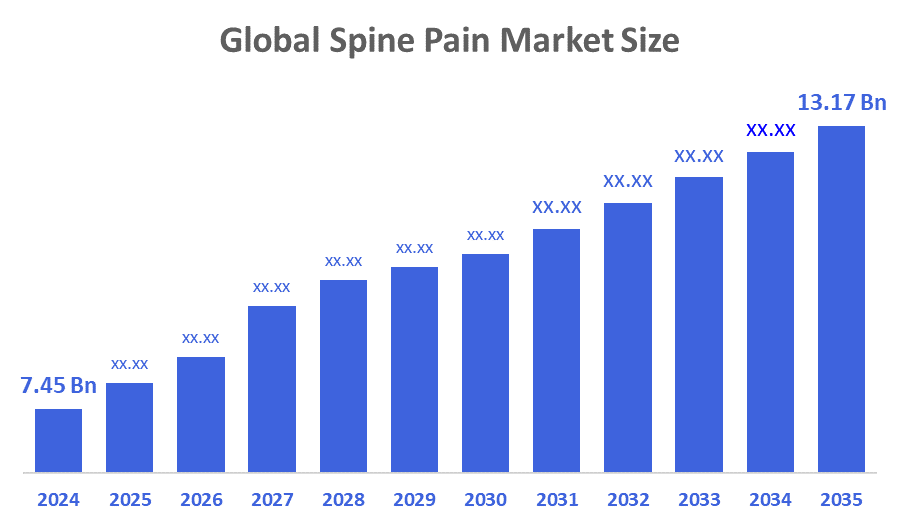

- The Global Spine Pain Market Size Was Estimated at USD 7.45 Billion in 2024

- The Market Size is Expected to Grow at a CAGR of around 5.32 % from 2025 to 2035

- The Worldwide Spine Pain Market Size is Expected to Reach USD 13.17 Billion by 2035

- Europe is expected to grow the fastest during the forecast period.

According to a research report published by Decisions Advisors and Consulting, The Global Spine Pain Market Size Was Worth Around USD 7.45 Billion In 2024 And Is Predicted To Grow To Around USD 13.17 Billion By 2035 With A Compound Annual Growth Rate (CAGR) Of 5.32 % From 2025 To 2035. The growth of the market for spine pain is primarily due to more cases of neurological disorders and an increase in the elderly population. Additionally, sedentary behaviour, increased health awareness in both industrialised and developing countries, and higher disposable income will also help promote growth in the spine pain market.

Market Overview

Spine pain, commonly called back pain, is discomfort or pain in the spinal area. It can stem from many causes, such as muscle strain, injuries, herniated discs, or underlying conditions like osteoarthritis and spinal stenosis. The market for managing spine pain covers a broad range of products and services for diagnosing, treating, and easing symptoms. This includes medical devices, pharmaceuticals, physical therapy, and other healthcare interventions. The development of artificial intelligence and predictive analytics holds real promise. These tools can sift through patient data to boost diagnostic accuracy, forecast surgical outcomes, tailor treatment plans, and streamline inventory for spinal devices. The shift toward value-based care pushes for solutions that deliver better long-term outcomes and lower costs. That creates fertile ground for truly innovative products that meet these changing needs. It can range from an annoying ache to something that really knocks down. The usual suspects for low back pain are muscle strains and sprains. They carry weight, twist, bend, move—all that action leaves them open to trouble. A sprain messes with the ligaments, those tough bands that hold your bones together. Lots of back pain just disappears on its own, but in some cases linger for months or even years. The muscles that keep your spine upright are layered. Some stretch all the way from the base of your skull down to your pelvis, while others just cover shorter stretches, depending on what part of your back they’re supporting—neck, upper, or lower.

The University of Michigan Medical School’s Department of Anesthesiology has received a $16.5 million grant from the NIH’s National Institute of Arthritis and Musculoskeletal and Skin Diseases (NIAMS). The funding is part of the NIH HEAL (Helping to End Addiction Long-term) Initiative and will support a project focused on personalised treatment for chronic lower back pain. The initiative aims to match interventions to individual patient characteristics, medical history, and life experiences, moving away from one-size-fits-all approaches.

Report Coverage

This research report categorizes the spine pain market based on various segments and regions, forecasts revenue growth, and analyzes trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the spine pain market. Recent market developments and competitive strategies, such as expansion, product launch, development, partnership, merger, and acquisition, have been included to draw the competitive landscape in the market. The report strategically identifies and profiles the key market players and analyzes their core competencies in each sub-segment of the spine pain market.

Driving Factors

The spine pain market keeps picking up speed, mostly because more people are dealing with degenerative spinal problems, there are more injuries, and the world’s population is getting older. Lower back pain gets a lot of attention in medical journals and health reports these days, and for good reason—it’s now the top cause of disability around the globe. Money keeps flowing into new medical tech, pushing forward both surgical and non-surgical treatments. Lately, there’s a big push for minimally invasive procedures that help people recover faster and get better results. A few things are really driving this growth: more older adults, plus more people spending their days sitting still, both of which mean more spinal issues. The global burden of disease study spells it out clearly—low back pain affects hundreds of millions and tops the list of disabling conditions worldwide. Some major trends stand out, like the quick rise of minimally invasive surgeries and new non-opioid options for pain relief. Big companies are making moves, too. Take Medtronic, for example—they keep expanding their lineup with cutting-edge tech like the Mazor X Stealth Edition robotic guidance system, pushing the market forward.

Restraining Factors

The spine pain industry has several difficult obstacles, such as regulatory barriers as well as reimbursement for new devices; increased competition as a result of market saturation, leading to pressure on pricing; lack of confidence in products due to safety and efficacy concerns; and the economic fallout from COVID-19, which has delayed elective surgeries and decreased patient volume. All of these factors combined are limiting growth and profits within the industry.

Market Segmentation

The spine pain market share is classified into disease type and end use.

- The chronic segment accounted for the largest share in 2024 and is anticipated to grow at a significant CAGR during the forecast period.

Based on the disease type, the spine pain market is divided into sub-acute, acute, and chronic. Among these, the chronic segment accounted for the largest share in 2024 and is anticipated to grow at a significant CAGR during the forecast period. The chronic segment is dealing with nerve issues, and the population is getting older. According to the National Institute of Neurological Disorders and Stroke, around 80% of adults end up with lower back pain at some point.

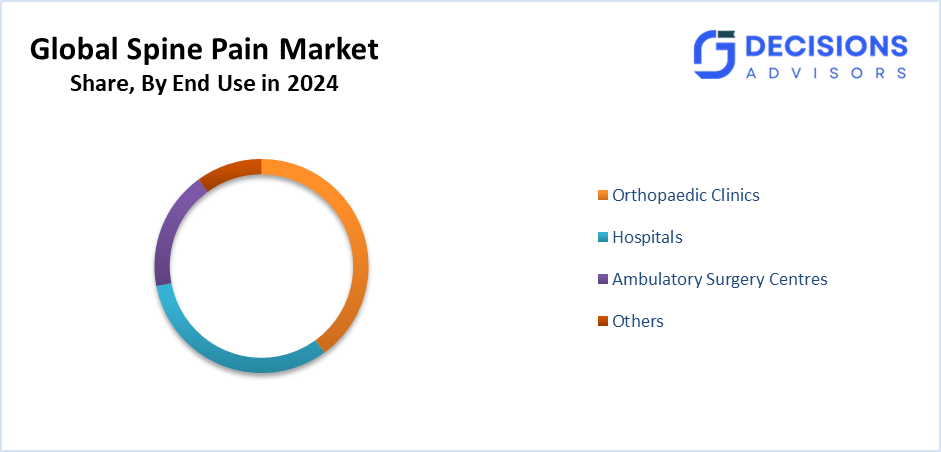

- The orthopaedic clinics segment accounted for the highest market revenue in 2024 and is anticipated to grow at a significant CAGR during the forecast period.

Based on the end use, the spine pain market is divided into orthopaedic clinics, hospitals, ambulatory surgery centres, and others. Among these, the orthopaedic clinics segment accounted for the highest market revenue in 2024 and is anticipated to grow at a significant CAGR during the forecast period. Orthopaedic physicians can deliver long-term comfort from back pain by using various methods for pain reduction, including injections, medication, and physical therapy. Many orthopaedic physicians are also orthopaedic surgeons.

Regional Segment Analysis of the Spine Pain Market

- North America (U.S., Canada, Mexico)

- Europe (Germany, France, U.K., Italy, Spain, Rest of Europe)

- Asia-Pacific (China, Japan, India, Rest of APAC)

- South America (Brazil and the Rest of South America)

- The Middle East and Africa (UAE, South Africa, Rest of MEA)

Asia Pacific is anticipated to hold the largest share of the spine pain market over the predicted timeframe.

Asia Pacific is anticipated to hold the largest share of the spine pain market over the predicted timeframe. Spine pain management is booming, due to huge populations, more money going into healthcare, and people becoming more aware of spinal problems. The middle class is growing fast, too. China, Japan, and India are leading the charge. The market itself is all over the map. In places like Japan and South Korea, you’ll find high-tech centres using advanced robots and navigation systems. Meanwhile, China and India focus on affordable treatments, since price really matters there. One big shift: global companies are starting to build their products locally. That helps them meet local needs and cut costs. On top of that, governments are putting money into hospitals and clinics, so more people can actually get treated.

Europe is expected to grow at a rapid CAGR in the spine pain market during the forecast period. Europe’s spine pain management market is pretty advanced and crowded. solid hospitals, experienced doctors, and a lot of older folks dealing with spinal issues. The European Medicines Agency and the CE marking process keep things strict—products need to actually work and be safe. Each country does its own thing when it comes to healthcare rules and what they’ll pay for. Germany and France, for example, are ahead of the curve when it comes to using the latest spinal tech. Companies need to come up with smarter solutions, mixing medical devices with digital tools to cover patients before and after surgery.

Competitive Analysis:

The report provides an in-depth analysis of the key organisations and companies involved in the spine pain market, along with a comparative evaluation based on their product offerings, business overviews, geographic presence, business strategies, segment market shares, and SWOT analyses. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes product development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

List of Key Companies

- Astellas Pharma Inc.

- BioWave Corporation

- Boston Scientific Corporation

- CELGENE CORPORATION

- Dr Reddy's Laboratories Ltd.

- Endo Pharmaceuticals Inc.

- Johnson & Johnson Private Limited

- Koninklijke Philips N.V.

- Medtronic

- Merck & Co Inc.

- Pfizer Inc

- Sanofi

- SpineThera Inc.

- Teva Pharmaceutical Industries Ltd.

- Others

Key Target Audience

- Market Players

- Investors

- End-users

- Government Authorities

- Consulting and Research Firm

- Venture capitalists

- Value-Added Resellers (VARs)

Recent Development

- In February 2026, Soin Neuroscience and Lilac Biosciences announced a collaboration to study RNA signatures in pain and neuromodulation. The partnership will explore how RNA expression patterns can serve as biomarkers for pain states and therapeutic responses, aiming to move beyond subjective patient reporting toward more objective, molecular-level measures of pain.

- In November 2025, North American Spine and Pain introduced a new clinical approach to back pain management. The model integrates advanced injection-based therapies (such as epidural steroid injections, facet joint injections, radiofrequency ablation, and trigger point injections) with image-guided diagnostics to treat both chronic and acute spinal conditions.

- In July 2024, Boston Scientific presented positive five-year pooled clinical data at the 2024 American Society of Pain & Neuroscience (ASPN) Conference in Miami Beach. The results, drawn from three clinical trials, highlighted the effectiveness of the Intracept™ Intraosseous Nerve Ablation System in treating vertebrogenic low back pain.

Market Segment

This study forecasts revenue at global, regional, and country levels from 2020 to 2035. Decisions Advisors has segmented the spine pain market based on the below-mentioned segments:

Global Spine Pain Market, By Disease Type

- Sub-Acute

- Acute

- Chronic

Global Spine Pain Market, By End Use

- Orthopaedic Clinics

- Hospitals

- Ambulatory Surgery Centres

- Others

Global Spine Pain Market, By Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa

Frequently Asked Questions (FAQ)

- What is the projected size and growth rate of the global spine pain market?

The market was valued at USD 7.45 billion in 2024 and is expected to reach USD 13.17 billion by 2035, growing at a CAGR of 5.32% from 2025 to 2035, driven by ageing populations and rising spinal disorders.

- What is spine pain, and what are its common causes?

Spine pain (often back pain) involves discomfort in the spinal area from muscle strains, sprains, herniated discs, osteoarthritis, spinal stenosis, injuries, or degenerative issues. It ranges from mild aches to debilitating pain affecting daily life.

- Which disease type segment dominates the market?

Chronic spine pain holds the largest share in 2024 and is projected to grow at a significant CAGR. It affects about 80% of adults at some point, linked to ageing, nerve issues, and sedentary lifestyles.

- What end-use segment leads in revenue?

Orthopaedic clinics accounted for the highest revenue in 2024 and are expected to grow at a significant CAGR. They offer specialised treatments like injections, medications, physical therapy, and surgery for long-term pain relief.

- Which regions are leading or growing fastest in the market?

Asia-Pacific is anticipated to hold the largest share due to massive populations, healthcare investments, and awareness in China, Japan, and India. Europe will grow at the fastest CAGR, supported by advanced tech and high prevalence.

- What are the primary drivers of market growth?

Increasing elderly populations, degenerative spinal conditions, sedentary behaviours, trauma injuries, and investments in minimally invasive surgeries and non-opioid therapies like robotics (e.g., Medtronic's Mazor X) fuel expansion.

- What challenges or restraining factors affect the market?

Regulatory hurdles, reimbursement issues for new devices, market saturation leading to pricing pressure, safety concerns, and COVID-19 delays in elective surgeries limit growth, especially in competitive landscapes.

- What recent developments are shaping the market?

Key advances include a $16.5M NIH grant to University of Michigan for personalised chronic back pain treatments; Soin Neuroscience-Lilac collaboration on RNA biomarkers (Feb 2026); North American Spine's injection therapies (Nov 2025); and Boston Scientific's five-year data on Intracept™ for vertebrogenic pain (Jul 2024).

Check Licence

Choose the plan that fits you best: Single User, Multi-User, or Enterprise solutions tailored for your needs.

We Have You Covered

- 24/7 Analyst Support

- Clients Across the Globe

- Tailored Insights

- Technology Tracking

- Competitive Intelligence

- Custom Research

- Syndicated Market Studies

- Market Overview

- Market Segmentation

- Growth Drivers

- Market Opportunities

- Regulatory Insights

- Innovation & Sustainability

Report Details

| Scope | Global |

| Pages | 240 |

| Delivery | PDF & Excel via Email |

| Language | English |

| Release | Feb 2026 |

| Access | Download from this page |