Global STD Diagnostic Market

Global STD Diagnostics Market Size, Share, By Disease Type (Chlamydia, Gonorrhea, Syphilis, HIV, HPV, and HSV) By Technology (Molecular Diagnostics, Immunoassays, and Rapid/POC Tests) By End User (Hospitals, Diagnostic Labs, and Home-care/Self-Testing) and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2025 ? 2035.

REPORT COVERAGE

Global

Market Snapshot

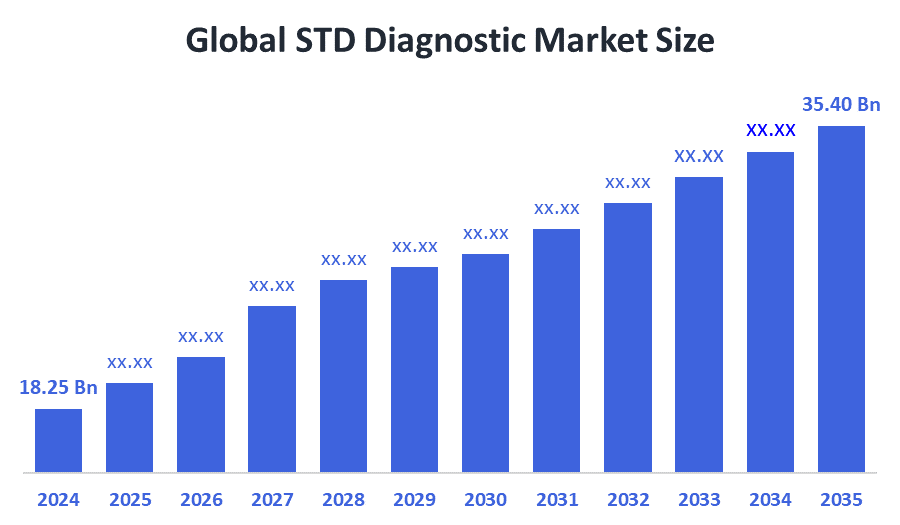

- Market Size (2025): USD 18.25 Billion

- Projected Market Size (2035): USD 35.40 Billion

- Compound Annual Growth Rate (CAGR): 6.85%

- Largest Regional Market: North America

- Fastest Growing Region: Asia-Pacific

- 3rd Largest Region: Europe

- Base Year: 2024

- Historical Period: 2021–2024

- Forecast Period: 2025–2035

According to Decision Advisors, the Global STD Diagnostic Market Size is expected to grow from USD 18.25 billion in 2025 to USD 35.40 billion by 2035, at a CAGR of 6.85% during the forecast period 2025–2035. The market is projected to expand steadily over the next decade, driven by the increasing global incidence of infections like Chlamydia and Syphilis and a rising emphasis on early clinical intervention. This growth is further supported by the shift toward decentralised testing, including point-of-care (POC) and home-based kits that offer users greater privacy and convenience. As government-led screening programs expand and technological advancements in molecular diagnostics make testing more accessible, the consumption of diagnostic reagents and consumables is increasing worldwide, solidifying the market’s long-term trajectory.

Market Overview/ Introduction

The global STD diagnostic market involves the production and sale of medical tests used to detect infections transmitted primarily through sexual contact, including vaginal, anal, and oral intercourse. However, several sexually transmitted diseases can also spread through non-sexual routes such as blood transfusion, sharing contaminated needles, mother-to-child transmission during pregnancy, childbirth or breastfeeding, and exposure to infected bodily fluids. This market includes diagnostic tools for major pathogens like HIV, Chlamydia, Gonorrhea, Syphilis, and HPV. There is a clear trend toward Molecular Diagnostics, including PCR testing, which provides high accuracy and the ability to test for multiple infections at once. This shift meets the needs of modern healthcare providers and patients who want faster, more reliable results than traditional lab methods offer. The market is moving from hospital labs toward decentralised testing, including point-of-care (POC) and at-home kits. Patients prefer these options for their privacy and convenience, which aligns with the growth of telehealth. This trend is driven by a tech-savvy generation that favours home-based screening over clinical visits. Looking ahead, companies are making tests more portable and user-friendly to ensure accurate diagnostics are available everywhere. This reflects a broader shift toward patient-focused and technology-driven diagnostic solutions in global healthcare systems, supported by increasing awareness of early detection, prevention strategies, and routine screening programs across both developed and emerging regions.

- The Government of India is aggressively scaling up testing under the National AIDS and STD Control Programme (NACP) Phase-V, which allocated a significant budget of $1.85 billion (?15,471 crore) through 2026.

- Abbott Laboratories is a leading global diagnostics company, which generated over $9.34 billion in revenue from its diagnostics segment in 2024.

- India is a major emerging hub for diagnostic manufacturing, with companies like Mylab Discovery Solutions

Notable Insights: -

- North America holds the largest regional market share, accounting for approximately 42.8% of the global STD diagnostics sector in 2025.

- Asia-Pacific is the fastest-growing region, driven by expanding healthcare access and aggressive government screening programs in India and China.

- By disease type, the Chlamydia testing segment holds a dominant position, representing roughly 38.6% of the total market share due to high global prevalence.

- By testing location, the Laboratory Testing segment remains dominant, accounting for over 46% of the market share as of 2025.

- The Compound Annual Growth Rate (CAGR) of the global STD diagnostic market is 6.85%.

- The market is likely to achieve a valuation of USD 35.40 billion by 2035, growing from a base of USD 18.25 billion in 2025.

What is the role of technology in grooming the market?

Technology is playing a major role in transforming the global STD diagnostics market by making testing more accurate, faster, and easier to access. The rise of at-home testing and telehealth services is making a strong impact on the industry, with the digital sexual health market surpassing USD 6.5 billion in 2024 and continuing to grow steadily. Advanced methods such as molecular diagnostics and multiplex PCR are now widely used in clinical labs, allowing multiple infections to be detected from a single sample, which improves both accuracy and patient outcomes. At the same time, automation and AI-powered lab systems are helping diagnostic centres manage large volumes of tests more efficiently while reducing errors and operational costs. Emerging technologies such as blockchain are also being explored to improve data security and ensure better tracking of patient results. Overall, these innovations are helping companies improve patient engagement, expand their reach, and support long-term growth in the market. This trend highlights the increasing reliance on digital and automated solutions to improve diagnostic efficiency and accessibility.

How are Recent Developments Helping the Market?

Recent developments like product innovation, decentralised testing, and digital health expansion are fuelling the global STD diagnostic market's growth. In 2025, a significant number of new diagnostic products and kits have been introduced in recent years, showcasing rapid innovation in multiplex PCR and home-based testing technologies. The preference for high-sensitivity molecular tests is rising. A majority of healthcare providers are increasingly adopting nucleic acid amplification tests (NAAT) over traditional methods. Furthermore, online sales of discreet testing kits have surged by nearly 30%, driven by the rise of e-commerce and direct-to-consumer health platforms. Laboratory efficiency is also improving through automated high-throughput screening, which reduces operational costs and manual errors. These advancements are enhancing patient privacy, expanding global testing reach, and securing the market's long-term expansion. This indicates a strong industry focus on innovation and scalability to meet the rising global demand for faster and more reliable testing.

Market Drivers

The global STD diagnostics market is growing steadily as healthcare systems adopt faster and more precise testing solutions. Methods like molecular diagnostics and multiplex testing are increasingly preferred because they allow for early detection and can identify multiple infections in one test. North America is expected to remain the leading region, with an estimated 37.5% share in 2025, backed by significant healthcare investment and quick adoption of technologies like NAAT. The United States is a major contributor, driven by strong demand for high-quality molecular tests and automated lab systems. At the same time, the move toward decentralised healthcare is boosting the use of point-of-care and at-home testing kits, which provide quick results and greater privacy. Growing awareness and a gradual decrease in stigma are also encouraging more people to choose self-sampling and mail-in testing instead of traditional clinic visits. Furthermore, innovative testing methods that screen for multiple infections from a single sample are appealing to younger users who value speed, convenience, and less invasive options. This trend shows a long-term shift toward decentralised and user-friendly diagnostic approaches.

Restraints

The global STD diagnostics market faces several challenges, including strict regulatory approvals and changing quality standards that delay product launches. High costs of advanced testing methods and falling reimbursement rates limit accessibility. Social stigma in conservative areas reduces testing rates, while data privacy regulations create hurdles for digital health platforms. Additionally, supply chain disruptions and rising operational costs for labs are further limiting market growth. These challenges emphasise the need for balanced regulatory frameworks and cost-effective solutions to ensure broader access to diagnostics.

Competitive Analysis

The report offers the appropriate analysis of the key organisations/companies involved within the std diagnostic market, along with a comparative evaluation primarily based on their product offerings, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborate analysis focusing on the current news and developments of the companies, which includes product development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

Top 10 Companies in the STD Diagnostic Market

- Abbott Laboratories

- F. Hoffmann-La Roche AG

- Hologic, Inc.

- Becton, Dickinson and Company (BD)

- Danaher Corporation (Cepheid)

- Thermo Fisher Scientific Inc.

- Siemens Healthineers

- Qiagen NV

- Bio-Rad Laboratories, Inc.

- bioMérieux SA

Government Initiatives

|

Country |

Key Government Initiatives |

|

US |

In the United States, a dedicated national strategy was introduced to improve awareness and expand access to affordable diagnostic services, supported by federal funding of over USD 1.3 billion annually under STI and HIV prevention programs. The focus is not just on treatment, but also on early detection and prevention, with initiatives aiming to reduce new HIV infections by 75% by 2025 and 90% by 2030 under the Ending the HIV Epidemic Initiative. |

|

India |

Public–private partnerships are playing an important role. Governments are working closely with laboratories and healthcare providers to make STI testing more accessible, often at little to no cost. India has strengthened STI/RTI control under the National AIDS Control Programme (NACP), which supports over 1,200+ designated STI/RTI clinics across the country, aiming to expand access in rural and underserved populations through free or subsidised diagnostic and treatment services. |

|

China |

The Action Plan for Eliminating Mother-to-Child Transmission (2022–2025) is designed to protect newborns from infections such as HIV, syphilis, and hepatitis B (HBV). A key priority of this initiative is to significantly reduce cases of congenital syphilis, with a targeted goal of bringing the rate down to a minimal level per 100,000 live births. |

Market Segmentation

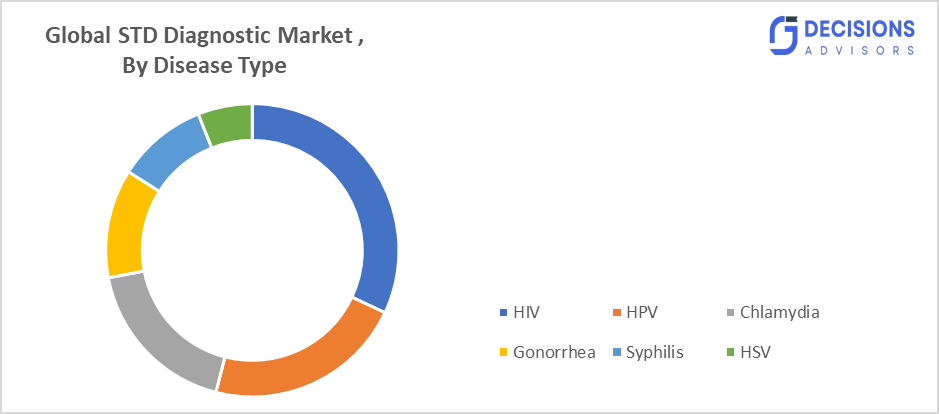

The STD diagnostics market share is classified into disease type, technology, and end user.

• The HIV segment dominated the market in 2024 and is projected to grow at a substantial CAGR of 7.5% to 8.5% during the forecast period.

Based on the disease type, the STD diagnostics market is divided into chlamydia, gonorrhea, syphilis, HIV, HPV, and HSV. The HIV segment dominated the market in 2024 and is projected to grow at a substantial CAGR of 7.5% to 8.5% during the forecast period. This dominance is primarily due to the high global disease burden and the continuous need for early and routine testing. Governments and healthcare organisations are actively promoting HIV screening programs, which significantly boost demand for diagnostic solutions. Additionally, advancements in rapid and self-testing kits have made HIV testing more accessible and convenient. The Asia-Pacific and African regions act as major growth drivers due to increasing awareness initiatives, improving healthcare infrastructure, and rising infection rates.

• The molecular diagnostics segment accounted for the largest share in 2024 and is anticipated to grow at a significant CAGR of 8.5% to 10.5% during the forecast period.

Based on the technology, the STD diagnostics market is divided into molecular diagnostics, immunoassays, and rapid, point-of-care (POC) tests. The molecular diagnostics segment accounted for the largest share in 2024 and is anticipated to grow at a significant CAGR of 8.5% to 10.5% during the forecast period. This is because molecular testing methods, such as PCR-based techniques, offer high accuracy, sensitivity, and early detection of infections. These technologies are widely preferred in clinical settings due to their reliability and ability to detect multiple infections simultaneously. The increasing adoption of automated diagnostic platforms and continuous technological advancements are further strengthening this segment. North America leads this segment due to a strong healthcare infrastructure and high adoption of advanced diagnostic technologies.

• The diagnostic laboratories segment dominated the market in 2024 and is projected to grow at a substantial CAGR of 6.5% to 7.8% during the forecast period.

Based on the end user, the STD diagnostics market is divided into hospitals, diagnostic labs, and home-care and self-testing. The diagnostic laboratories segment dominated the market in 2024 and is projected to grow at a substantial CAGR of 6.5% to 7.8% during the forecast period. This dominance is driven by the availability of specialised equipment, skilled professionals, and the ability to handle large volumes of testing with high accuracy. Diagnostic labs are often the primary choice for confirmatory testing and comprehensive screening services. However, there is a growing shift toward home care and self-testing due to increasing awareness, privacy concerns, and convenience. The demand is particularly rising in urban regions where individuals prefer discreet and quick testing options.

What is the Reason for Regional Dominance?

The dominance of certain regions in the global STD diagnostics market is mainly driven by advanced healthcare infrastructure, higher awareness levels, strong government support, and greater access to testing services. Regions such as North America lead the market due to well-established healthcare systems, high healthcare spending, and widespread adoption of advanced diagnostic technologies like molecular testing and NAAT. In addition, strong screening programs and favourable reimbursement policies encourage regular testing, further strengthening market demand. The presence of major diagnostic companies and continuous technological innovation also contributes to regional leadership. At the same time, increasing awareness about sexual health and reducing social stigma have improved testing rates. In contrast, regions like Asia-Pacific are emerging as fast-growing markets due to improving healthcare access, rising population, and expanding government-led screening initiatives, which are gradually boosting overall diagnostic adoption.

Strategies to Implement for Growth of the Market in Non-Leading Regions

Growth in non-leading regions of the global STD diagnostics market can speed up with targeted investments, better accessibility, and local healthcare strategies. Companies can increase their presence by introducing affordable and easy-to-use diagnostic solutions, particularly rapid and point-of-care testing kits designed for low-resource settings. Strengthening distribution networks, including partnerships with local clinics, pharmacies, and community health centres, can greatly improve access to testing services. Additionally, expanding digital health platforms and telemedicine services can help reach underserved populations, especially in rural and remote areas. Collaborating with governments and public health organisations to support screening programs and awareness campaigns can further boost adoption. Educating communities to reduce stigma around STD testing is also essential for raising testing rates. Furthermore, investing in local manufacturing and supply chains can lower costs and ensure the steady availability of diagnostic products. Companies that prioritise user-friendly, discreet, and culturally sensitive testing solutions are more likely to gain acceptance and build long-term growth in emerging markets.

Regional Segment Analysis of the STD Diagnostics Market

• North America (U.S., Canada, Mexico)

• Europe (Germany, France, U.K., Italy, Spain, Rest of Europe)

• Asia-Pacific (China, Japan, India, Rest of APAC)

• Latin America (Brazil and the Rest of Latin America)

• The Middle East and Africa (UAE, South Africa, Rest of MEA)

Asia-Pacific is anticipated to hold the fastest growth in the STD diagnostics market over the predicted timeframe. Asia-Pacific is expected to witness the highest growth during the forecast period, with an estimated CAGR of around 10%, while accounting for approximately 25% of the global market share, driven by improving healthcare infrastructure, rising awareness about sexually transmitted infections, and large population bases in countries like China and India. The region is benefiting from increasing government-led screening programs and expanding access to diagnostic services, especially in urban and semi-urban areas. Rapid urbanisation, growing disposable incomes, and a rising focus on preventive healthcare are further supporting market expansion. Countries such as India and China, with their large populations, are generating significant demand for STD testing, making the region a key growth engine for the global market.

North America is anticipated to hold the largest share of the STD diagnostics market during the forecast period. North America dominates the market, accounting for approximately 43% of the global revenue share, supported by advanced healthcare systems and high adoption of modern diagnostic technologies such as molecular testing and NAAT. The United States contributes the majority of the regional revenue due to strong healthcare spending, widespread screening programs, and early adoption of innovative diagnostic solutions. In addition, the increasing use of at-home testing kits and point-of-care diagnostics is further boosting market growth. Consumers in this region are more inclined toward regular health check-ups and early disease detection, which strengthens the demand for STD diagnostics.

Europe is expected to hold the third-largest share in the STD diagnostics market during the forecast period, contributing approximately 28% of the global market share. Europe maintains a strong position in the market due to well-established healthcare systems and consistent government support for sexual health programs. Countries such as Germany, France, and the U.K. contribute significantly due to high awareness levels and routine screening initiatives. The region also shows a strong presence of diagnostic companies and advanced laboratory infrastructure, supporting accurate and widespread testing. While the growth rate is moderate compared to Asia-Pacific, the demand remains stable due to continuous public health efforts and increasing focus on preventive care.

Future Market Trends in Global STD Diagnostics Market: -

- Rapid Growth of Point-of-Care (POC) and At-Home Testing

There is a clear shift from traditional laboratory-based testing to decentralised solutions such as point-of-care (POC) and at-home testing kits. These methods provide faster results, improve patient convenience, and help reduce transmission rates by enabling early diagnosis.

- Rising Adoption of Molecular Diagnostics and Advanced Technologies

Advanced diagnostic methods such as nucleic acid amplification tests (NAATs) and multiplex PCR are becoming the standard due to their high accuracy and ability to detect multiple infections simultaneously.

- Increasing Focus on High-Burden and Emerging Regions

Market growth is accelerating in regions with high infection rates, particularly in Asia-Pacific, Africa, and other low- and middle-income countries. Expanding government screening programs, improving healthcare access, and rising awareness are driving demand for STD diagnostics in these regions, especially for infections like HIV and syphilis.

Recent Developments

- In December 2025, Becton, Dickinson and Company expanded its BD MAX system menu with new molecular assays for detecting infections such as herpes simplex virus and syphilis, strengthening its STI diagnostic portfolio and improving testing efficiency.

- In November 2025, Abbott Laboratories expanded approval for its Alinity m high-risk HPV assay to support self-collected samples, strengthening its position in patient-centric and decentralised diagnostic solutions.

- In September 2024, a joint initiative involving QIAGEN and Becton, Dickinson and Company introduced a urine-based liquid biopsy solution that supports molecular testing workflows, enhancing non-invasive sample collection and expanding diagnostic capabilities.

- In May 2024, Roche received FDA approval for one of the first HPV self-collection solutions in the United States, improving access to screening by allowing patients to privately collect samples for testing.

- In November 2023, the FDA approved one of the first diagnostic tests allowing at-home sample collection for chlamydia and gonorrhea, supporting the growing trend toward remote and patient-centric testing approaches.

Market Segment

This study forecasts revenue at global, regional, and country levels from 2020 to 2035. The STD diagnostics market is segmented based on the following categories:

Global STD Diagnostics Market, By Disease Type

• Chlamydia

• Gonorrhea

• Syphilis

• HIV

• HPV

• HSV

Global STD Diagnostics Market, By Technology

• Molecular Diagnostics

• Immunoassays

• Rapid/Point-of-Care (POC) Tests

Global STD Diagnostics Market, By End User

• Hospitals

• Diagnostic Laboratories

• Home-care/Self-Testing

Global STD Diagnostics Market, By Regional Analysis

• North America

• US

• Canada

• Mexico

• Europe

• Germany

• UK

• France

• Italy

• Spain

• Russia

• Rest of Europe

• Asia Pacific

• China

• Japan

• India

• South Korea

• Australia

• Rest of Asia Pacific

• Latin America

• Brazil

• Argentina

• Rest of Latin America

• Middle East & Africa

• UAE

• Saudi Arabia

• Qatar

• South Africa

• Rest of the Middle East & Africa

Frequently Asked Questions (FAQ)

- How are advanced technologies influencing growth in the global STD diagnostics market?

Advanced technologies such as molecular diagnostics and nucleic acid amplification tests (NAAT) are significantly improving testing accuracy and speed. These innovations allow early detection and the identification of multiple infections from a single sample, which is driving overall market growth.

- Why does North America dominate the global STD diagnostics market?

North America leads the market due to its advanced healthcare infrastructure, high healthcare spending, strong awareness programs, and widespread adoption of modern diagnostic technologies. Regular screening practices and supportive reimbursement systems further strengthen its position.

- What role does home-based testing play in market expansion?

Home-based testing is becoming a key growth factor as it offers privacy, convenience, and quick results. It helps overcome social stigma and encourages more individuals to undergo regular testing, especially among younger populations.

- How is increasing awareness impacting the STD diagnostics market?

Rising awareness about sexual health and early disease detection is encouraging more people to opt for routine screening. Government initiatives and public health campaigns are playing a crucial role in improving testing rates and reducing infection spread.

Check Licence

Choose the plan that fits you best: Single User, Multi-User, or Enterprise solutions tailored for your needs.

We Have You Covered

- 24/7 Analyst Support

- Clients Across the Globe

- Tailored Insights

- Technology Tracking

- Competitive Intelligence

- Custom Research

- Syndicated Market Studies

- Market Overview

- Market Segmentation

- Growth Drivers

- Market Opportunities

- Regulatory Insights

- Innovation & Sustainability

Report Details

| Scope | Global |

| Pages | 210 |

| Delivery | PDF & Excel via Email |

| Language | English |

| Release | Apr 2026 |

| Access | Download from this page |