United Arab Emirates Genetic Testing Market

United Arab Emirates Genetic Testing Market Size, Share, By Type (Diagnostic Testing, Predictive & Presymptomatic Testing, Carrier Testing, Prenatal & Newborn Testing, Pharmacogenomic Testing), By Technology (PCR, Next-Generation Sequencing, Microarrays, CRISPR-based Diagnostics), By Application (Oncology, Rare & Inherited Diseases, Reproductive Health, Pharmacogenomics, Ancestry & Wellness), By End Use (Hospitals & Clinics, Diagnostic Laboratories, Academic & Research Institutes, Direct-to-Consumer), United Arab Emirates Genetic Testing Market Insights, Industry Trend, Forecasts to 2035

CAGR

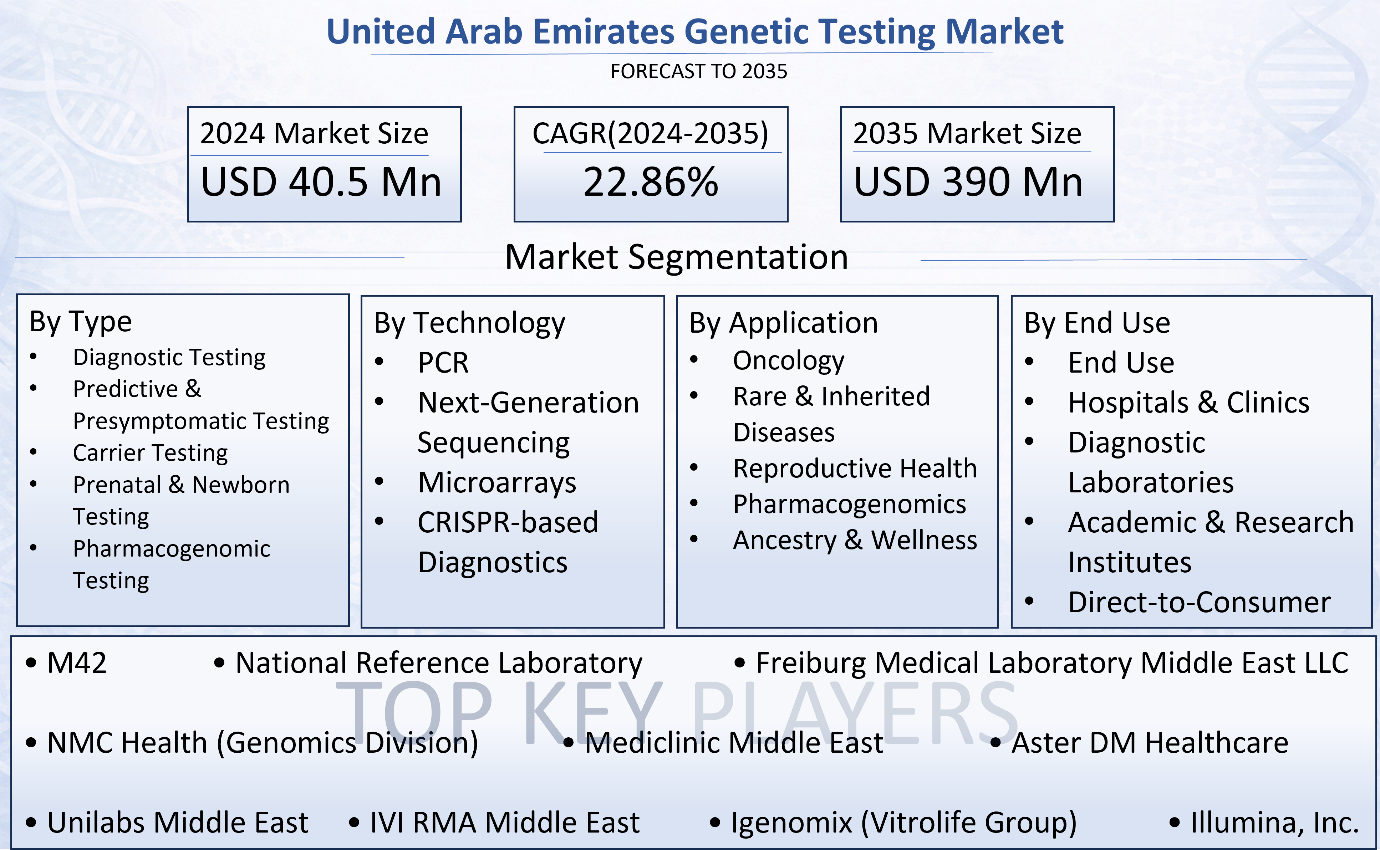

22.86%

REVENUE 2024

USD Million 40.5

FORECAST 2035

USD Million 390.0

REPORT COVERAGE

Country

United Arab Emirates Genetic Testing Market Size Insights Forecasts to 2035

- United Arab Emirates Genetic Testing Market Size 2024: USD 40.5 Million

- United Arab Emirates Genetic Testing Market Size 2035: USD 390 Million

- United Arab Emirates Genetic Testing Market CAGR 2024: 22.86%

- United Arab Emirates Genetic Testing Market Segments: Type, Technology, Application, and End Use.

The UAE genetic testing market includes diagnostic and analytical services that assess and analyze DNA, RNA or chromosomal differences to determine the presence or absence of inherited diseases or the risk of developing them and to establish how someone responds to specific treatments, is now evolving rapidly to support oncological practices, reproductive health, diagnostic testing for rare diseases, and pharmacogenomic applications as part of precision medicine frameworks. Demand for genetic tests in the UAE will be significantly impacted by growing recognition that hereditary conditions exist throughout the population, an increase in the overall incidence of cancer the establishment of many new molecular diagnostics laboratories and an increase in the use of next-generation sequencing technologies for genetic testing. With a strong infrastructure for healthcare and growing private sector investments in molecular diagnostics, the demand for more comprehensive genetic screening services continues to grow.

The UAE genetic testing market is supported by government initiatives, as the UAE’s government has invested heavily in the genetic testing market and regulates the genetic testing sector through a variety of programs and standards. For instance, the Emirates Genome Project is a national initiative focused on conducting large-scale genome sequencing to support preventive health care strategies and to personalize treatment regimens utilizing genomic and phenotypic information. The Dubai Health Authority and Department of Health- Abu Dhabi have regulatory oversight of genetic testing and are dedicated to preserving data integrity and ensuring that genetic testing remains clinically relevant and complies with regulatory requirements. Continued investments in artificial Intelligence driven genomic analytics, expanding newborn screening programs and utilizing pharmacogenetics in routine clinical practice are expected to continue driving growth in the genetic testing market at double digit rates through 2035.

Market Dynamics of the United Arab Emirates Genetic Testing Market:

The driving forces behind this UAE genetic testing market include the growing demand for tailored medicine and treatments for cancers, the variety of chronic and hereditary diseases and the effort to modernize public healthcare system throughout the UAE. The rise of hospitals establishing molecular diagnostic units and the greater frequency of hospitals implementing NGS testing technologies have significantly improved the speed and volume of genetic testing performed across the UAE. In addition to the continuing increase in the number of laboratories performing genetic testing, an increase in public understanding of preventive medicine and early detection of diseases will result in higher volumes of carrier screening, pre-natal genetic testing and predictive genetic testing throughout the country.

The challenges faced by the UAE genetic testing market include the expense associated with NGS testing technologies and an increased need for specialized laboratory facilities, which is a major impediment to the widespread availability of genetic testing. Concerns regarding the privacy of genetic information and ethical issues related to how genetic information is managed creates regulatory obstacles. The limited availability of trained genetic counselors and molecular geneticists restricts scalability for many laboratories offering genetic testing. Lastly, current reimbursement policies for some genetic testing continue to be inadequate and will reduce affordability for some segments of the population.

The UAE's future prospects for growth are positive due to its continued establishment of itself as a regional center of technological advances in the field of health care (e.g., precision medicine). Health systems will benefit from greater use of AI-assisted decoding of DNA data; an increase in the number of hospitals using genetic tests to inform medication selection decisions; and further collaboration between multinational biotechnology companies and local health care providers. The broader adoption of genetic testing will allow for greater use of precision medicine and preventive health policies in medical practice in the UAE resulting in continued growth throughout the forecast period.

Market Segmentation

The United Arab Emirates genetic testing market share is classified into type, technology, application, and end use.

By Type:

The United Arab Emirates genetic testing market is divided by type into diagnostic testing, predictive & presymptomatic testing, carrier testing, prenatal & newborn testing, and pharmacogenomic testing. Among these, diagnostic testing dominated the share in 2024 and is anticipated to grow at a remarkable CAGR during the forecast period. The diagnostic testing market is dominated because it provides the basis to make clinical decisions in oncology, cardiology, and rare diseases, as hospitals are turning to molecular diagnostics to confirm the disease accurately, identify mutations, and choose therapies. The routine implementation of genetic panels in hospital workflows and the growth in demand for oncology biomarker testing have led to increased demand for these services. In addition, with the increase in chronic and hereditary diseases, there will continue to be a high level of demand from patients who require ongoing and repetitive diagnostic genetic services.

By Technology:

The market is divided by technology into PCR, next-generation sequencing (NGS), microarrays, and CRISPR-based diagnostics. Among these, next-generation sequencing dominated in 2024 and is anticipated to grow at a remarkable CAGR during the forecast period. Next-generation sequencing (NGS) is the most widely used because it is the most cost-effective of all available methods for carrying out high-throughput testing for multiple genes and for performing comprehensive tumor profiling, identifying rare diseases and conducting large-scale genomic projects. As such, NGS is the core platform for national sequencing programs. Rapid improvements in technology have resulted in dramatically reduced sequencing turnaround times as well as increased accuracy and depth of data produced from NGS. As precision medicine continues to grow, NGS is likely to remain the primary platform for all research and clinical genomic applications.

By Application:

The market is divided by application into oncology, rare & inherited diseases, reproductive health, pharmacogenomics, and ancestry & wellness. Among these, oncology dominated in 2024 and is anticipated to grow at a remarkable CAGR during the forecast period, as with an increasing number of patients diagnosed with cancer and an increase in the use of biomarkers to determine how to treat patients, oncology is becoming the main area of growth. The most important thing that doctors look for when prescribing immunotherapy (or "targeted" therapy) to treat breast, colon, and lung cancers is whether a certain type of genetic mutation exists within the patient's tissue. The increased availability of both companion diagnostics and tumor genome sequencing will contribute to the continued demand for precision medicine, as will the federal Government's investments in precision medicine.

By End Use:

The market is divided by end use into hospitals & clinics, diagnostic laboratories, academic & research institutes, and direct-to-consumer. Among these, hospitals & clinics dominated the share in 2024 and are anticipated to grow at a remarkable CAGR during the forecast period. The increasing incorporation of genetic testing into clinical pathways, particularly in oncology, reproductive medicine, and neonatal screening, has strengthened hospital dominance. The establishment of integrated molecular diagnostic units in tertiary care facilities has further improved testing turnaround times and enabled physicians to interpret results directly. The growth of specialized genomic departments and partnerships with international technology providers has reinforced hospitals as the primary location for genomic testing. Additionally, patients demonstrate greater trust in hospital environments, where regulatory compliance is stronger compared to independent or direct-to-consumer settings.

Competitive Analysis:

The report offers the appropriate analysis of the key organisations/companies involved within the United Arab Emirates genetic testing market, along with a comparative evaluation primarily based on their product offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes product development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

Top Key Companies in United Arab Emirates Genetic Testing Market:

- M42

- National Reference Laboratory

- Freiburg Medical Laboratory Middle East LLC

- NMC Health (Genomics Division)

- Mediclinic Middle East

- Aster DM Healthcare

- Unilabs Middle East

- IVI RMA Middle East

- Igenomix (Vitrolife Group)

- Illumina, Inc.

- Thermo Fisher Scientific, Inc.

- Roche Diagnostics

Key Target Audience

- Market Players

- Investors

- End-users

- Government Authorities

- Consulting and Research Firm

- Venture capitalists

- Value-Added Resellers (VARs)

Market Segment

This study forecasts revenue at the UAE, regional, and country levels from 2020 to 2035. Decisions Advisors has segmented the United Arab Emirates genetic testing market based on the below-mentioned segments:

United Arab Emirates Genetic Testing Market, By Type

- Diagnostic Testing

- Predictive & Presymptomatic Testing

- Carrier Testing

- Prenatal & Newborn Testing

- Pharmacogenomic Testing

United Arab Emirates Genetic Testing Market, By Technology

- PCR

- Next-Generation Sequencing

- Microarrays

- CRISPR-based Diagnostics

United Arab Emirates Genetic Testing Market, By Application

- Oncology

- Rare & Inherited Diseases

- Reproductive Health

- Pharmacogenomics

- Ancestry & Wellness

United Arab Emirates Genetic Testing Market, By End Use

- End Use

- Hospitals & Clinics

- Diagnostic Laboratories

- Academic & Research Institutes

- Direct-to-Consumer

FAQ

1. What is the size of the United Arab Emirates genetic testing market in 2024?

The United Arab Emirates genetic testing market size was valued at USD 40.5 million in 2024. The market is projected to experience rapid expansion due to increased adoption of precision medicine, rising cancer prevalence, and advancements in next-generation sequencing technologies.

2. What is the projected growth of the UAE genetic testing market by 2035?

The UAE genetic testing market is expected to grow from USD 40.5 million in 2024 to USD 390 million by 2035, registering a strong CAGR of 22.86% during the forecast period 2025–2035. This high growth rate reflects increasing investment in genomic infrastructure and rising demand for personalized healthcare solutions.

3. What are the major drivers of the United Arab Emirates genetic testing market?

The primary growth drivers include increasing demand for precision medicine, rising incidence of cancer and hereditary diseases, expansion of molecular diagnostic laboratories, and broader implementation of next-generation sequencing (NGS) technologies. Government-backed initiatives such as the Emirates Genome Program are further accelerating large-scale genome sequencing and preventive healthcare strategies.

4. Which type segment dominates the UAE genetic testing market?

Diagnostic Testing dominates the UAE Genetic Testing Market in 2024. This segment leads because it forms the foundation of clinical decision-making in oncology, cardiology, and rare disease management. Hospitals increasingly rely on genetic panels and mutation analysis to confirm diagnoses, guide therapy selection, and monitor disease progression.

5. Which technology is most widely used in the UAE genetic testing market?

Next-Generation Sequencing (NGS) is the dominant technology segment. NGS is preferred due to its high-throughput capability, cost efficiency for multi-gene testing, comprehensive tumor profiling, and suitability for national genome projects. It remains the core platform for precision medicine and advanced genomic research in the UAE.

6. Which application segment holds the largest share in the UAE genetic testing market?

The Oncology segment holds the largest market share. Increasing cancer prevalence and the growing use of biomarker-based targeted therapies are driving demand for tumor genomic profiling and companion diagnostics across UAE hospitals and diagnostic laboratories.

7. What challenges are affecting the UAE genetic testing market?

Key challenges include high costs associated with NGS platforms, limited availability of trained genetic counselors, concerns regarding genetic data privacy, and incomplete reimbursement coverage for certain genetic tests. These factors may limit accessibility and scalability despite strong market growth.

8. How is the UAE government supporting the genetic testing market?

The UAE government supports the market through national initiatives such as the Emirates Genome Program, which focuses on large-scale genome sequencing to enable preventive healthcare and personalized treatment strategies. Regulatory oversight from the Dubai Health Authority and Department of Health – Abu Dhabi ensures compliance, data integrity, and clinical standards.

Check Licence

Choose the plan that fits you best: Single User, Multi-User, or Enterprise solutions tailored for your needs.

We Have You Covered

- 24/7 Analyst Support

- Clients Across the Globe

- Tailored Insights

- Technology Tracking

- Competitive Intelligence

- Custom Research

- Syndicated Market Studies

- Market Overview

- Market Segmentation

- Growth Drivers

- Market Opportunities

- Regulatory Insights

- Innovation & Sustainability

Report Details

| Scope | Country |

| Pages | 255 |

| Delivery | PDF & Excel via Email |

| Language | English |

| Release | Feb 2026 |

| Access | Download from this page |