United Kingdom Plasma Fractionation Market

United Kingdom Plasma fractionation market Size, Share, By Product Type (Immunoglobulins (IVIG, SCIg), Albumin, Coagulation Factors, Protease Inhibitors), By Application (Immunodeficiency Disorders, Hemophilia and Bleeding Disorders, Neurological Disorders, Critical Care & Shock Treatment), By End User (Hospitals, Clinical & Diagnostic Laboratories, Specialty Clinics), Analysis and Forecast 2026-2035.

REPORT COVERAGE

Global

Market Snapshot

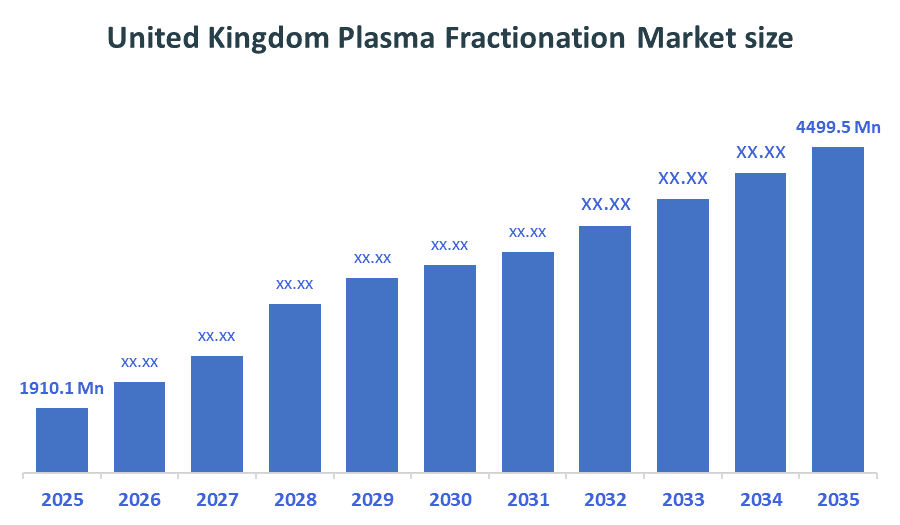

- United Kingdom Plasma Fractionation Market size (2025): USD 1910.1 Million

- Projected United Kingdom Plasma Fractionation Market Size (2035): USD 4499.5 Million

- United Kingdom Plasma Fractionation Market Compound Annual Growth Rate (CAGR): 8.95%

- Base Year: 2025

- Historical Period: 2021–2024

- Forecast Period: 2026–2035

Market Overview/Introduction

The United Kingdom plasma fractionation market functions as a healthcare sector that manages all operations from blood plasma collection until the production of therapeutic products that contain immunoglobulins, albumin, and medical treatment clotting factors. Plasma fractionation uses industrial biochemical techniques to separate plasma proteins, which produce essential medicines that treat immunodeficiency disorders, hemophilia, and other persistent medical conditions. The market will experience growth according to the projection because of increasing occurrence rates of rare diseases and rising requirements for immunoglobulin treatments, and the expansion of plasma collection initiatives, which the NHS Blood and Transplant organization supports. The upcoming possibilities will result from technological progress that enhances fractionation processes while increasing yield capabilities and developing national plasma self-sufficiency systems. The market experiences growth because of substantial government healthcare funding and permanent product supply contracts, and international company alliances, which improve the distribution of healthcare products and treatment options throughout the United Kingdom.

- The UK government, through the Department of Health and Social Care, launched the Plasma for Medicines Programme (2021–ongoing) by lifting a decades-old ban on using UK donor plasma for manufacturing immunoglobulin therapies. This initiative aims to improve domestic production and reduce reliance on imports.

- The NHS Blood and Transplant is implementing a national plasma collection and supply strategy (2024 onward) to build self-sufficiency in plasma-derived medicines, including immunoglobulin (IVIG). The program focuses on expanding donor bases and modernizing plasma infrastructure.

- The UK government initiated a Domestic Plasma Fractionation Contract (2025–2029) led by NHS England, awarding a long-term agreement (worth approximately £600 million) to process UK-collected plasma into medicines. This strengthens local manufacturing capacity and supply chain resilience.

Notable Insights: -

- The immunoglobulins (IVIG, SCIg) segment dominated the market in 2025 and holds the largest market share, accounting for approximately 67% during the forecast period.

- The immunodeficiency disorders segment dominated the market in 2025 and holds the largest market share, accounting for approximately 62% during the forecast period.

- The hospitals segment dominated the market in 2025 and holds the largest market share, accounting for approximately 75% during the forecast period.

- The compound annual growth rate of the United Kingdom Plasma Fractionation Market is 8.95%.

- The market is likely to achieve a valuation of USD 8110.9Million by 2035.

What is the role of technology in grooming the market?

Technology plays a crucial role in shaping the United Kingdom plasma fractionation market by improving efficiency, safety, and yield of plasma-derived therapies. Advanced fractionation techniques such as chromatography and automated separation systems enhance the purification of immunoglobulins, albumin, and clotting factors. Digital tracking and cold-chain monitoring systems ensure full traceability and compliance across the supply chain managed by the National Health Service. Single-use bioprocessing technologies reduce contamination risks and operational downtime, while continuous processing improves scalability. Additionally, automation and AI-driven quality control systems enhance consistency and reduce human error. These innovations support collaboration with global leaders like CSL Behring, helping to strengthen supply security, optimize production costs, and meet rising clinical demand for plasma-derived medicinal products in the UK healthcare system.

Market Drivers

The United Kingdom plasma fractionation market exists because more chronic illnesses occur, which include bleeding disorders and different neurological diseases that need plasma-derived treatments. The market is mainly dominated by immunoglobulins because their use for treating immune deficiencies and related disorders has been increasing. The rising demographic of elderly people results in higher requirements for plasma-based solutions that treat age-related medical conditions. The improvements to plasma collection techniques, together with the technological advances in fractionation methods, have produced safer and more effective products which are now more widely accessible. The removal of restrictions on UK-donated plasma usage for immunoglobulin manufacturing has improved domestic plasma supply capabilities, although the country still depends on US imports for plasma.

Restrain

The United Kingdom plasma fractionation market faces restraints such as a limited domestic plasma supply, historically dependent on imports, and strict policies from the National Health Service. High processing costs, stringent regulatory requirements, and complex fractionation technologies further restrict market expansion and create supply-demand imbalances.

Study on the Supply, Demand, Distribution, and Market Environment of the United Kingdom Plasma Fractionation Market

The United Kingdom plasma fractionation market is shaped by controlled plasma supply, rising clinical demand, and a regulated distribution framework. Plasma, the key raw material, is sourced through government-backed collection programs led by the NHS Blood and Transplant and supplemented by international imports due to limited domestic volumes. Demand is increasing steadily, driven by growing cases of immune deficiencies and neurological disorders requiring immunoglobulins. Distribution is centralized, with products supplied primarily to hospitals via the National Health Service, ensuring equitable access and strict quality control. The market environment is highly regulated, emphasizing safety, traceability, and long-term supplier contracts, while partnerships with global fractionators enhance supply security and support the expansion of domestic plasma utilization capacity.

Price Analysis and Consumer Behaviour Analysis

Price dynamics in the United Kingdom plasma fractionation market are influenced by high production costs, strict regulatory compliance, and limited domestic plasma supply. Pricing of immunoglobulins and albumin remains premium due to complex fractionation processes and reliance on contracts with the National Health Service. Long-term procurement agreements help stabilize prices, though global supply fluctuations can create periodic cost pressures. From a consumer behavior perspective, demand is largely institutional rather than individual, driven by hospitals and clinicians. There is strong preference for high-quality, safe, and traceable plasma-derived therapies. Increasing awareness of rare diseases and immune disorders has boosted demand for immunoglobulins. Additionally, trust in government-backed supply chains and preference for domestically sourced plasma products are shaping procurement and usage patterns across the UK healthcare system.

Market Segmentation

The United Kingdom Plasma Fractionation Market share is classified into material type, application, and end user

- The immunoglobulins (IVIG, SCIg) segment dominated the market in 2025 and holds the largest market share, accounting for approximately 67% during the forecast period.

Based on the product type, the plasma fractionation market is divided into immunoglobulins (IVIG, SCIg), albumin, coagulation factors, and protease inhibitors. Among these, the immunoglobulins (IVIG, SCIg) segment dominated the market in 2025 and holds the largest market share, accounting for approximately 67% during the forecast period. The immunoglobulins (IVIG, SCIg) segment is driven by the increasing number of people with chronic diseases, together with the growing need for continuous medical treatments and the widespread use of medical treatments in hospital environments. Immunoglobulins treat more medical conditions and receive better funding from the National Health Service compared to albumin, coagulation factors, and protease inhibitors, which establishes their dominance in the UK's plasma fractionation industry.

- The immunodeficiency disorders segment dominated the market in 2025 and holds the largest market share, accounting for approximately 62% during the forecast period.

Based on the application, the plasma fractionation market is divided into immunodeficiency disorders, hemophilia and bleeding disorders, neurological disorders, and critical care & shock treatment. Among these, the immunodeficiency disorders segment dominated the market in 2025 and holds the largest market share, accounting for approximately 62% during the forecast period. The immunodeficiency disorders segment in the U.K. is attributed to the material providing moisture and contamination protection through its lightweight design, affordable price, and effective barrier capabilities. The material serves as the standard packaging solution for bottles and blister packs, and closures in pharmaceutical manufacturing operations. The growing need for packaging solutions that offer both convenience and durability, and flexible use, combined with increased adoption of generic drugs and oral medication forms, drives the current market demand.

- The hospitals segment dominated the market in 2025 and holds the largest market share, accounting for approximately 75% during the forecast period.

Based on the end user, the plasma fractionation market is divided into hospitals, clinical & diagnostic laboratories, and specialty clinics. Among these, the hospitals segment dominated the market in 2025 and holds the largest market share, accounting for approximately 75% during the forecast period. The hospitals segment in the U.K. is driven by their central role in drug development, large-scale manufacturing, and distribution of medicines. The companies need extensive amounts of dependable primary and secondary packaging systems which will protect their products, meet regulatory requirements and support their supply chain activities. The increased production of biologics, injectable therapies, and personalized medicines that these companies develop will enhance their existing market dominance.

Recent Development

- In April 2025, the UK officially launched plasma-derived medicines produced from domestically collected plasma for the first time in over 25 years. This includes key products like immunoglobulins and albumin supplied to NHS patients.

- In March 2025, the UK government announced the rollout of home-grown plasma-derived treatments, marking a major development in the United Kingdom plasma fractionation market by enabling domestic production of immunoglobulin and albumin through plasma fractionation processes.

- In July 2023, Octapharma was appointed as the sole fractionation partner for the UK’s Plasma for Medicines Programme, beginning the processing of UK-collected plasma into medicines in 2024, with the first supplies delivered to NHS patients in early 2025.

Competitive Analysis

The report offers the appropriate analysis of the key organisations/companies involved within the United Kingdom Plasma fractionation market, along with a comparative evaluation primarily based on their product offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes product development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

Top Key Companies in the United Kingdom Plasma Fractionation Market

- CSL Limited

- Grifols

- Octapharma

- Kedrion Biopharma

- Bio Products Laboratory (BPL)

- Others

Key Target Audience

- Market Players

- Investors

- End-users

- Government Authorities

- Consulting and Research Firm

- Venture capitalists

- Value-Added Resellers (VARs)

Market Segment

This study forecasts revenue at the United Kingdom, regional, and country levels from 2020 to 2035. Spherical Insights has segmented the United Kingdom plasma fractionation market based on the below-mentioned segments

United Kingdom Plasma Fractionation Market, By Product Type

- Immunoglobulins (IVIG, SCIg)

- Albumin

- Coagulation Factors

- Protease Inhibitors

United Kingdom Plasma Fractionation Market, By Application

- Immunodeficiency Disorders

- Hemophilia and Bleeding Disorders

- Neurological Disorders

- Critical Care & Shock Treatment

United Kingdom Plasma Fractionation Market, By End User

- Hospitals

- Clinical & Diagnostic Laboratories

- Specialty Clinics

Frequently Asked Questions (FAQ)

Q. What challenges affect plasma collection capacity in the United Kingdom?

A. The UK faces limitations in plasma collection due to historically restricted domestic donation policies, donor shortages, and reliance on voluntary blood donation systems. Although recent policy changes have improved collection potential, infrastructure constraints and donor recruitment challenges still restrict large-scale self-sufficiency.

Q. How does the UK ensure quality control in plasma-derived therapies?

A. Quality control is ensured through strict regulatory oversight by the MHRA, along with standardized manufacturing protocols, viral inactivation steps, and continuous batch testing. These measures ensure safety, purity, and traceability of plasma-derived medicinal products used in clinical treatment.

Q. What role do international partnerships play in the UK plasma fractionation supply chain?

A. International partnerships help bridge domestic plasma shortages by enabling imports of plasma and finished fractionated products. Collaborations with global manufacturers ensure supply stability, technology transfer, and access to advanced fractionation capabilities not fully available within the UK.

Q. How is sustainability influencing plasma fractionation operations in the UK?

A. Sustainability is becoming important through reduced waste processing, energy-efficient fractionation technologies, and adoption of environmentally friendly manufacturing practices. Companies are also focusing on lowering carbon footprints in cold-chain logistics and optimizing resource utilization in plasma processing facilities.

Check Licence

Choose the plan that fits you best: Single User, Multi-User, or Enterprise solutions tailored for your needs.

We Have You Covered

- 24/7 Analyst Support

- Clients Across the Globe

- Tailored Insights

- Technology Tracking

- Competitive Intelligence

- Custom Research

- Syndicated Market Studies

- Market Overview

- Market Segmentation

- Growth Drivers

- Market Opportunities

- Regulatory Insights

- Innovation & Sustainability

Report Details

| Scope | Global |

| Pages | 240 |

| Delivery | PDF & Excel via Email |

| Language | English |

| Release | Apr 2026 |

| Access | Download from this page |