United States Plasma Therapy Market

United States Plasma therapy market Size, Share, By Product Type (Immunoglobulins (IVIG, SCIG), Albumin, Coagulation Factors (Factor VIII, Factor IX), Protease Inhibitors), By Application (Immunology, Hematology, Neurology, Critical Care), By End User (Hospitals, Clinics, Research Institutes, Ambulatory Surgical Centers) Analysis and Forecast 2026-2035.

REPORT COVERAGE

Country

Market Snapshot

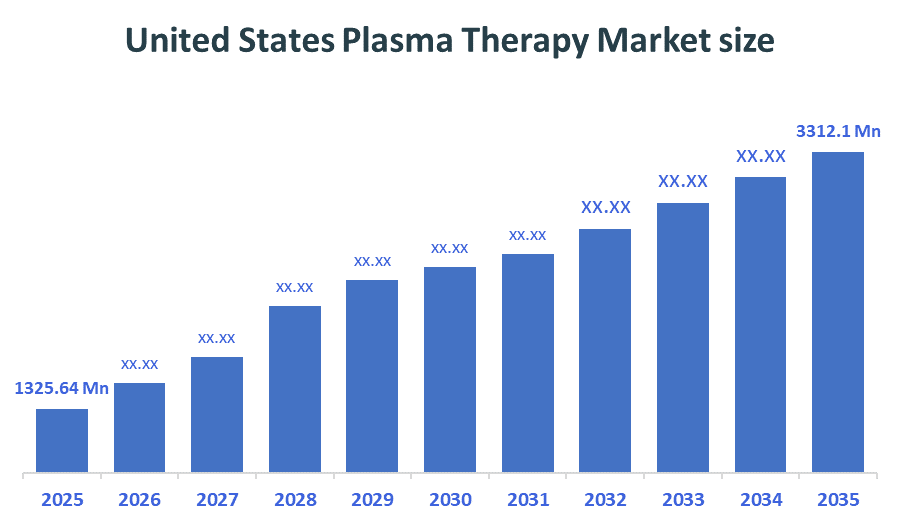

- United States Plasma Therapy Market size (2025): USD 1325.64 Million

- Projected United States Plasma Therapy Market Size (2035): USD 3312.1 Million

- United States Plasma Therapy Market Compound Annual Growth Rate (CAGR): 9.59%

- Base Year: 2025

- Historical Period: 2021–2024

- Forecast Period: 2026–2035

Market Overview/Introduction

The United States plasma therapy market refers to the healthcare industry involved in the collection, processing, and distribution of human blood plasma to produce life-saving plasma-derived medicines, which include immunoglobulins, albumin, and clotting factors. Plasma therapy is a medical treatment that uses blood plasma components to treat immune deficiencies, bleeding disorders, and other chronic conditions. The market will expand because more people develop rare and chronic diseases, immunoglobulin therapies become more popular, and healthcare facilities become more available. The future offers new possibilities through three technological advances, which include fractionation technology, recombinant plasma products, and AI-based supply chain optimization. Public understanding of early diagnosis and treatment, combined with existing regulatory frameworks and plasma donation center growth, creates vital pathways for plasma therapies to establish themselves as fundamental components of modern precision and regenerative medicine within the United States healthcare system.

- The Expanded Access Program (EAP), supported by federal agencies and research institutions, provided large-scale access to convalescent plasma across the U.S., treating tens of thousands of patients while generating real-world clinical data. This initiative strengthened plasma therapy adoption and infrastructure.

- The U.S. Food and Drug Administration approved licensed high-titer convalescent plasma (via Biologics License Application) for immunocompromised patients, improving long-term access to plasma therapies beyond emergency use. This marks a transition from emergency programs to permanent regulatory pathways.

- The National Institutes of Health supports plasma therapy through clinical trials and funding programs focused on immunotherapy, biologics, and infectious disease treatment. These initiatives promote research into plasma-derived therapies and next-generation antibody treatments.

Notable Insights: -

- The immunoglobulins (IVIG, SCIG) segment dominated the market in 2025 and holds the largest market share, accounting for approximately 62% during the forecast period.

- The immunology segment dominated the market in 2025 and holds the largest market share, accounting for approximately 40% during the forecast period.

- The hospitals segment dominated the market in 2025 and holds the largest market share, accounting for approximately 50% during the forecast period.

- The compound annual growth rate of the United States Plasma therapy market is 9.59%.

- The market is likely to achieve a valuation of USD 3312.1Million by 2035.

What is the role of technology in grooming the market?

Technology plays a crucial role in shaping and accelerating the United States plasma therapy market by improving efficiency, safety, and scalability across the value chain. Advanced apheresis technologies enable faster and safer plasma collection from donors, increasing overall supply. Modern fractionation techniques and automated bioprocessing systems enhance yield and purity of plasma-derived products such as immunoglobulins and albumin. Digital tracking systems and AI-driven analytics improve donor management, inventory forecasting, and supply chain optimization, reducing wastage and shortages. Cold chain innovations ensure better storage and transportation of sensitive plasma products. Additionally, automation in manufacturing facilities supports consistent quality and regulatory compliance. Emerging technologies like recombinant protein production and pathogen reduction systems further enhance product safety and reliability. Collectively, these technological advancements are driving operational efficiency, cost optimization, and sustainable growth in the U.S. plasma therapy market while meeting rising patient demand for advanced therapies.

Market Drivers

The United States plasma therapy market is being driven by several key factors. The increasing number of people who have immunodeficiency disorders, together with chronic diseases, creates a continuous demand for plasma-derived medical products, which physicians use to treat these conditions. The market expansion receives additional support from rising quality requirements and sustainability needs, together with new developments in plasma fractionation technology. The increasing number of sports injuries that occur during athletic activities drives more medical facilities to use plasma therapy for their specialized treatment needs. The market develops new possibilities because researchers explore new medical applications and test new treatments. Medical experts can now identify patients who need plasma therapy through enhanced diagnostic methods.

Restrain

The United States plasma therapy market faces restraints such as limited plasma donor availability, high production and processing costs, and stringent regulatory requirements. Supply chain vulnerabilities, long fractionation timelines, and dependence on specialized infrastructure also restrict scalability. Additionally, price pressures and reimbursement challenges can limit broader patient access to therapies.

Study on the Supply, Demand, Distribution, and Market Environment of the United States Plasma Therapy Market

The United States plasma therapy market operates in a highly structured supply-demand environment, where supply is primarily dependent on voluntary plasma donations collected through an extensive network of donation centers, making the U.S. the largest global source of raw plasma. Demand is driven by rising cases of chronic and rare diseases requiring immunoglobulins, albumin, and coagulation factors, creating a persistent supply–demand gap. Distribution is controlled by vertically integrated companies that manage collection, fractionation, and global supply chains. The market environment is shaped by strict FDA regulations, high capital investment, and strong competition among key players. Raw material in this market is human blood plasma, which undergoes fractionation to extract therapeutic proteins. Limited donor availability, seasonal variations, and increasing global demand for plasma-derived medicines further intensify supply pressures, while technological advancements in fractionation and expanding healthcare access continue to support long-term market growth and stability in the U.S. healthcare system.

Price Analysis and Consumer Behaviour Analysis

The United States plasma therapy market is characterized by relatively high treatment costs due to complex collection, fractionation, and storage processes, as well as stringent regulatory compliance requirements. Plasma-derived therapies such as immunoglobulins and albumin are premium-priced, often leading to annual treatment costs ranging from several thousand to over $100,000 depending on the condition and dosage frequency. Price variation is also influenced by hospital settings, insurance coverage, and availability of specialty plasma products. From a consumer behavior perspective, demand is largely driven by patients with chronic and rare diseases, including immunodeficiency disorders and hemophilia, who require long-term or lifelong therapy. Patients and healthcare providers show strong preference for trusted, branded therapies with proven clinical efficacy and safety. Additionally, increasing awareness, improved diagnosis rates, and expanding insurance reimbursement coverage are significantly boosting adoption of plasma therapies across the United States healthcare system.

Market Segmentation

The United States Plasma Therapy Market share is classified into material type, application, and end user

- The immunoglobulins (IVIG, SCIG) segment dominated the market in 2025 and holds the largest market share, accounting for approximately 62% during the forecast period.

Based on the product type, the plasma therapy market is divided into immunoglobulins (IVIG, SCIG), albumin, coagulation factors (factor VIII, factor IX), and protease inhibitors. Among these,the immunoglobulins (IVIG, SCIG) segment dominated the market in 2025 and holds the largest market share, accounting for approximately 62% during the forecast period. The immunoglobulins (IVIG, SCIG) segment is driven by its extensive use in treating immunodeficiency, autoimmune, and neurological disorders. High clinical effectiveness, recurring long-term treatment needs, strong physician preference, and increasing disease prevalence contribute to sustained demand.

- The immunology segment dominated the market in 2025 and holds the largest market share, accounting for approximately 40% during the forecast period.

Based on the application, the plasma therapy market is divided into immunology, hematology, neurology, and critical care. Among these, the immunology segment dominated the market in 2025 and holds the largest market share, accounting for approximately 40% during the forecast period. The immunology segment in the U.K. is attributed to the high prevalence of primary and secondary immunodeficiency disorders requiring long-term treatment. Strong reliance on immunoglobulin therapies, increasing diagnosis rates, and rising awareness among healthcare providers drive demand.

- The hospitals segment dominated the market in 2025 and holds the largest market share, accounting for approximately 50% during the forecast period.

Based on the end user, the bioplasma therapy market is divided into hospitals, clinics, research institutes, and ambulatory surgical centers. Among these, the hospitals segment dominated the market in 2025 and holds the largest market share, accounting for approximately 50% during the forecast period. The hospitals segment in the U.K. is driven by the availability of advanced healthcare infrastructure, skilled professionals, and specialized equipment required for plasma therapy administration. Hospitals handle complex cases, ensure patient monitoring, and benefit from strong reimbursement systems.

Recent Development

- In November 2025, Stanford Blood Center launched nationwide distribution of FDA-approved convalescent plasma therapy under a Biologics License Application (BLA), expanding access for immunocompromised patients and strengthening plasma therapy commercialization.

- In December 2024, the U.S. Food and Drug Administration formally transitioned convalescent plasma from Emergency Use Authorization (EUA) to fully licensed biologic therapy status, enabling large-scale market launch and interstate distribution of plasma-based treatments.

Competitive Analysis

The report offers the appropriate analysis of the key organisations/companies involved within the United States Plasma therapy market, along with a comparative evaluation primarily based on their product offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes product development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

Top Key Companies in the United States Plasma Therapy Market

- CSL Limited

- Grifols

- Takeda Pharmaceutical Company

- Octapharma

- Kedrion Biopharma

- Others

Key Target Audience

- Market Players

- Investors

- End-users

- Government Authorities

- Consulting and Research Firm

- Venture capitalists

- Value-Added Resellers (VARs)

Market Segment

This study forecasts revenue at the United States, regional, and country levels from 2020 to 2035. Spherical Insights has segmented the United States plasma therapy market based on the below-mentioned segments

United States Plasma Therapy Market, By Product Type

- Immunoglobulins (IVIG, SCIG)

- Albumin

- Coagulation Factors (Factor VIII, Factor IX)

- Protease Inhibitors

United States Plasma Therapy Market, By Application

- Immunology

- Hematology

- Neurology

- Critical Care

United States Plasma Therapy Market, By End User

- Hospitals

- Clinics

- Research Institutes

- Ambulatory Surgical Centers

Frequently Asked Questions (FAQ)

Q. What factors influence plasma collection capacity in the United States?

A. Plasma collection capacity in the U.S. is influenced by donor availability, number of plasma donation centers, regulatory policies, and advancements in apheresis technology. Incentive programs, donor awareness campaigns, and operational efficiency of collection centers also play a crucial role in maintaining a stable plasma supply.

Q. How does regulatory oversight impact the U.S. plasma therapy market?

A. Strict regulations by authorities such as the U.S. Food and Drug Administration ensure product safety, quality, and efficacy. While these regulations enhance patient trust, they also increase compliance costs and extend approval timelines, impacting market entry and expansion for manufacturers.

Q. What role do plasma-derived therapies play in rare disease treatment?

A. Plasma-derived therapies are essential for managing rare and life-threatening conditions such as hemophilia and primary immunodeficiency. These therapies often serve as the only effective treatment option, making them critical in improving patient survival rates and quality of life in the U.S. healthcare system.

Q. How is the competitive landscape evolving in the U.S. plasma therapy market?

A. The market is becoming increasingly competitive with companies focusing on vertical integration, strategic partnerships, and technological innovation. Firms are expanding plasma collection networks and investing in advanced fractionation facilities to strengthen their market position and meet growing global demand.

Check Licence

Choose the plan that fits you best: Single User, Multi-User, or Enterprise solutions tailored for your needs.

We Have You Covered

- 24/7 Analyst Support

- Clients Across the Globe

- Tailored Insights

- Technology Tracking

- Competitive Intelligence

- Custom Research

- Syndicated Market Studies

- Market Overview

- Market Segmentation

- Growth Drivers

- Market Opportunities

- Regulatory Insights

- Innovation & Sustainability

Report Details

| Scope | Country |

| Pages | 240 |

| Delivery | PDF & Excel via Email |

| Language | English |

| Release | Apr 2026 |

| Access | Download from this page |