United States Veterinary Diagnostics Market

United States Veterinary Diagnostics Market Size, Share, By Product Type (Instruments, Consumables, Reagents), By Technology (Immunodiagnostics, Molecular Diagnostics, Clinical Biochemistry, Hematology), By Animal Type (Companion Animals, Livestock), By End User (Veterinary Hospitals & Clinics, Diagnostic Laboratories, Research Institutes), Analysis and Forecast 2025-2035

REPORT COVERAGE

country

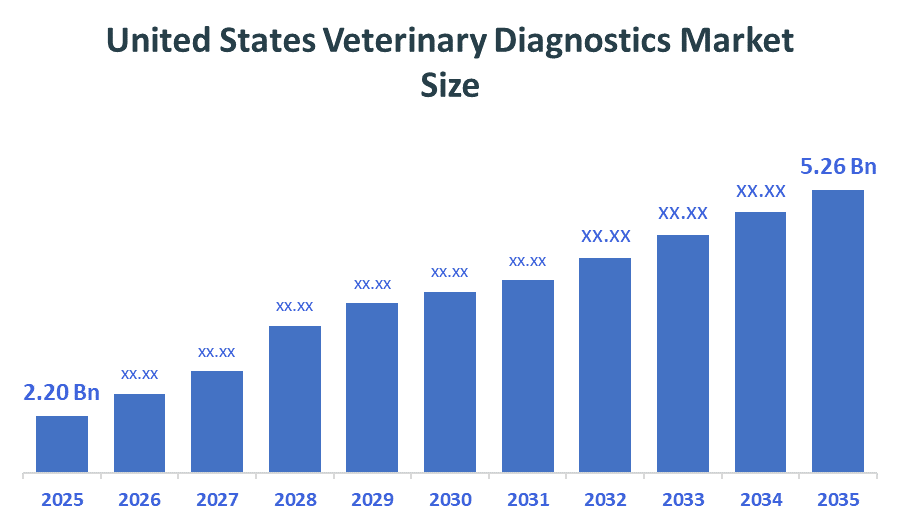

The United States Veterinary Diagnostics Market Size is foreseen to grow from USD 2.20 Billion in 2025 and is govern to reach around USD 5.26 Billion by 2035. According to Decision Advisors, a detailed research report on the US Veterinary Diagnostics Market is boosts by integration of Artificial Intelligence, accounting for nearly upto the 21% to 30% share of the total share worldwide. IDEXX Laboratories is the prime player in the market with approximately USD 1 million in annual turnover and a 15-25% global market share, positioning it as the primary driver of the US Veterinary Diagnostics Market.

Market Snapshot

- United States Veterinary Diagnostics Market Size (2025): USD 2.20 Billion

- Projected United States Veterinary Diagnostics Market Size (2035): USD 5.26 Billion

- United States Veterinary Diagnostics Market Compound Annual Growth Rate (CAGR): 9.11%

- Market Base Year: 2025

- Historical Period: 2021–2024

- Forecast Period: 2026–2035

Market Overview/Introduction

The U.S. Veterinary Diagnostics Market is the high-tech doctor’s office for our pets. It’s the entire world of blood tests, scans, and lab work used to figure out why a dog is limping or a cat isn't eating. Because we now treat pets like family members, this market is booming. We were seeing a steady 8% to 11% growth every year because people are more willing than ever to pay for senior wellness checks and preventive care to keep their furry best friends around longer. Even the government is getting involved through the One Health initiative. This program treats human and animal health as one big picture, funding new ways to track diseases like bird flu or Lyme disease before they jump to people. Meanwhile, big companies like IDEXX and Zoetis are racing to put Artificial Intelligence (AI) right into the vet's clinic. Instead of waiting days for a lab to mail back results, new AI machines can scan a blood sample and give the vet an answer in minutes. The biggest future opportunity is moving from fixing a sick pet to predicting the sickness. We were moving toward a world where a smart collar or a simple routine test can catch kidney or heart issues months before the pet even feels a symptom, making healthcare proactive rather than just a last-minute emergency.

Notable Insights: -

- By product type, the consumables & reagents segment dominated the market in 2025, accounting for approximately 57% of market share, and is projected to grow at a substantial CAGR during the forecast period.

- By end user, the veterinary hospitals & clinics segment dominated the market in 2025, accounting for approximately 53% of market share, and is projected to grow at a substantial CAGR during the forecast period.

- The compound annual growth rate of the US veterinary diagnostics market is 9.11%.

- The Market is likely to achieve a valuation of USD 5.26 Billion by 2035.

What is the role of technology in grooming the market?

Technology plays a crucial role in advancing the US veterinary diagnostics market through innovations such as rapid diagnostic kits, molecular testing, and digital imaging systems. Point-of-care diagnostic devices enable veterinarians to obtain real-time results, improving treatment outcomes. Artificial intelligence and data analytics are increasingly being integrated into diagnostic platforms to enhance accuracy and efficiency. Additionally, automation in laboratories and advancements in genomic testing are enabling early disease detection and personalized treatment approaches in veterinary medicine.

Market Drivers

The real engine behind the U.S. Veterinary Diagnostics Market is the humanization of our pets. We no longer see dogs and cats as just backyard animals, they are family members sleeping in our beds, which makes us far more willing to pay for advanced medical checkups. This shift has turned senior wellness panels and routine blood work into a standard part of pet ownership, creating a massive, recurring demand for testing. Beyond our emotional bond, technology is a huge driver. On top of that, a rise in zoonotic diseases, illnesses that can jump from animals to humans, like Lyme or Bird Flu, has pushed the government to pour more funding into diagnostic surveillance. Essentially, we were seeing a perfect storm where deeper pockets, better tech.

Study on the Supply, Demand, Distribution, and Market Environment of the US Veterinary Diagnostics Market

The US veterinary diagnostics market operates within a well-established supply chain supported by domestic manufacturers and global players. On the supply side, companies focus on continuous innovation and development of advanced diagnostic solutions. Demand is driven by veterinary clinics, hospitals, and diagnostic laboratories, with increasing adoption of point-of-care testing.

Distribution channels include direct sales, distributors, and online platforms, ensuring efficient product availability. The market environment is highly regulated, promoting product safety, quality standards, and innovation while ensuring compliance with regulatory requirements

Price Analysis and Consumer Behaviour Analysis

Pricing in the US veterinary diagnostics market is influenced by technology type, product complexity, and brand positioning. Advanced diagnostic tools and molecular testing solutions typically command higher prices due to their accuracy and efficiency. However, increasing competition among market players helps maintain pricing balance.

From a consumer behaviour perspective, veterinary professionals prioritize diagnostic accuracy, reliability, and speed over cost. Pet owners are increasingly willing to pay premium prices for advanced diagnostics, particularly for companion animals. There is also a growing preference for rapid and point-of-care diagnostic solutions that provide immediate results.

Market Segmentation

- The consumables & reagents segment dominated the market in 2025, accounting for approximately 57% of market share, and is projected to grow at a substantial CAGR during the forecast period.

Based on the product type, the US veterinary diagnostics market is divided into instruments, consumables, and reagents. Among these, the consumables & reagents segment dominated the market in 2025, accounting for approximately 57% of the market share, and is projected to grow at a substantial CAGR during the forecast period. This segment dominates due to the recurring need for test kits, assay reagents, and diagnostic consumables in routine veterinary testing. Unlike instruments, which are one-time investments, consumables generate continuous demand across veterinary clinics and laboratories. The increasing volume of diagnostic testing, especially for infectious and chronic diseases in animals, further supports the growth of this segment. Additionally, advancements in test kit accuracy and ease of use are enhancing adoption, while instruments continue to witness steady demand driven by technological upgrades.

- The immunodiagnostics segment accounted for the largest share in 2025 and is anticipated to grow at a significant CAGR during the forecast period.

Based on the technology, the US veterinary diagnostics market is divided into immunodiagnostics, molecular diagnostics, clinical biochemistry, hematology, and others. Among these, the immunodiagnostics segment accounted for the largest share in 2025 and is anticipated to grow at a significant CAGR during the forecast period. This segment dominates due to its widespread application in detecting infectious diseases, allergens, and hormonal disorders in animals. Immunodiagnostic techniques are widely preferred because of their cost-effectiveness, reliability, and rapid turnaround time. In the US, the increasing prevalence of zoonotic diseases and routine health screening of pets are driving demand for these solutions. Additionally, advancements in ELISA and lateral flow assays are further boosting segment growth. Molecular diagnostics is also gaining traction due to its high sensitivity and precision, while other technologies maintain steady demand.

- The companion animals segment dominated the market in 2025, accounting for approximately 63% of market share, and is projected to grow at a substantial CAGR during the forecast period.

Based on the animal type, the US veterinary diagnostics market is divided into companion animals and livestock. Among these, the companion animals segment dominated the market in 2025, accounting for approximately 63% of the market share, and is projected to grow at a substantial CAGR during the forecast period. This dominance is driven by the rising trend of pet humanization and increasing expenditure on pet healthcare in the US. Pet owners are increasingly opting for regular health check-ups and advanced diagnostic testing to ensure early disease detection and better treatment outcomes. Additionally, the growing prevalence of chronic conditions such as diabetes, cancer, and infections in pets is further supporting demand. The livestock segment also contributes significantly, particularly in disease surveillance and food safety, but remains secondary compared to companion animals.

- The veterinary hospitals & clinics segment dominated the market in 2025, accounting for approximately 53% of market share, and is projected to grow at a substantial CAGR during the forecast period.

Based on the end user, the US veterinary diagnostics market is divided into veterinary hospitals & clinics, diagnostic laboratories, research institutes. Among these, the veterinary hospitals & clinics segment dominated the market in 2025, accounting for approximately 53% of the market share, and is projected to grow at a substantial CAGR during the forecast period. This dominance is driven by the high volume of patient visits and the increasing adoption of in-house diagnostic solutions in veterinary practices. Clinics and hospitals rely heavily on diagnostic tools for routine screening, disease diagnosis, and treatment monitoring. The availability of point-of-care testing devices has further strengthened this segment by enabling rapid results and improved clinical decision-making. Diagnostic laboratories also play a crucial role in advanced testing, while research institutes contribute to innovation and development in veterinary diagnostics.

Recent Development

- In April 2026, IDEXX Laboratories’ bullish investment case received a modest boost following the launch of its Cancer Dx Panel for canine lymphoma in the US on April 1, 2026. The new blood-based diagnostic test, already used by thousands of veterinary practices in North America, aims to support early cancer detection and expand preventive care adoption.

- In April 2026, IDEXX Laboratories was highlighted as a leading player in the veterinary diagnostics market, with continued expansion driven by innovation and global demand for advanced animal healthcare solutions. The company’s strong portfolio of diagnostic instruments, consumables, and reference lab services supports recurring revenue growth and reinforces its market leadership.

Competitive Analysis

The report offers the appropriate analysis of the key organisations/companies involved within the US veterinary diagnostics market, along with a comparative evaluation primarily based on their product offering, business overviews, geographic presence, enterprise strategies, segment Market share, and SWOT analysis. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes product development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the Market.

Top Key Companies in the US Veterinary Diagnostics Market

- Croda International Plc

- Innospec

- Elementis

- A & E Connock

- Surfachem Group

Key Target Audience

- Market Players

- Investors

- End-users

- Government Authorities

- Consulting and Research Firm

- Venture capitalists

- Value-Added Resellers (VARs)

Market Segment

This study forecasts revenue at the United States, regional, and country levels from 2020 to 2035. Decision Advisors has segmented the US veterinary diagnostics market based on the below-mentioned segments

US Veterinary Diagnostics Market, By Product Type

- Consumables & Reagents

- Instruments

US Veterinary Diagnostics Market, By Technology

- Immunodiagnostics

- Molecular Diagnostics

- Clinical Biochemistry

- Hematology

US Veterinary Diagnostics Market, By Animal Type

- Companion Animals

- Livestock Animals

US Veterinary Diagnostics Market, By End User

- Veterinary Hospitals & Clinics

- Diagnostic Laboratories

- Research Institutes

Frequently Asked Questions (FAQ)

Q1. How is telemedicine influencing the US veterinary diagnostics market?

A. The rise of veterinary telemedicine is increasing demand for remote diagnostic tools and digital platforms that allow veterinarians to assess animal health virtually, often supported by portable or at-home diagnostic kits.

Q2. What impact does pet insurance have on veterinary diagnostics adoption in the US?

A. Growing adoption of pet insurance is encouraging pet owners to opt for advanced and often expensive diagnostic tests, as insurance coverage reduces out-of-pocket costs and improves access to high-quality care.

Q3. How are point-of-care diagnostic devices transforming veterinary practices?

A. Point-of-care devices are enabling rapid, on-site testing within veterinary clinics, reducing reliance on external laboratories and allowing faster clinical decision-making and improved treatment outcomes.

Q4. What role do reference laboratories play in the US veterinary diagnostics market?

A. Reference laboratories handle complex and specialized diagnostic tests that require advanced equipment and expertise, supporting veterinary clinics by providing accurate and comprehensive diagnostic results.

Q5. How is data integration shaping the future of veterinary diagnostics?

A. Integration of diagnostic data with electronic veterinary health records and analytics platforms is improving disease tracking, enabling predictive diagnostics, and enhancing overall clinical efficiency in veterinary care.

Check Licence

Choose the plan that fits you best: Single User, Multi-User, or Enterprise solutions tailored for your needs.

We Have You Covered

- 24/7 Analyst Support

- Clients Across the Globe

- Tailored Insights

- Technology Tracking

- Competitive Intelligence

- Custom Research

- Syndicated Market Studies

- Market Overview

- Market Segmentation

- Growth Drivers

- Market Opportunities

- Regulatory Insights

- Innovation & Sustainability

Report Details

| Scope | country |

| Pages | 240 |

| Delivery | PDF & Excel via Email |

| Language | English |

| Release | Apr 2026 |

| Access | Download from this page |