Global Zygomatic and Pterygoid Implants Market

Global Zygomatic and Pterygoid Implants Market Size, Share, By Type (Zygomatic Implants, Pterygoid Implants) By Length of Implant (Up to 30 mm, 31 ? 50 mm, Above 50 mm) By Application (Severe Atrophy of Maxillary Bone, Maxillary Sinuses, Trauma & Other Indications) By Procedure Approach (Immediate Loading, Delayed Loading) By End User (Hospitals, Dental Clinics, Ambulatory Surgical Centers) By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2025-2035.

REPORT COVERAGE

Global

Market Snapshot

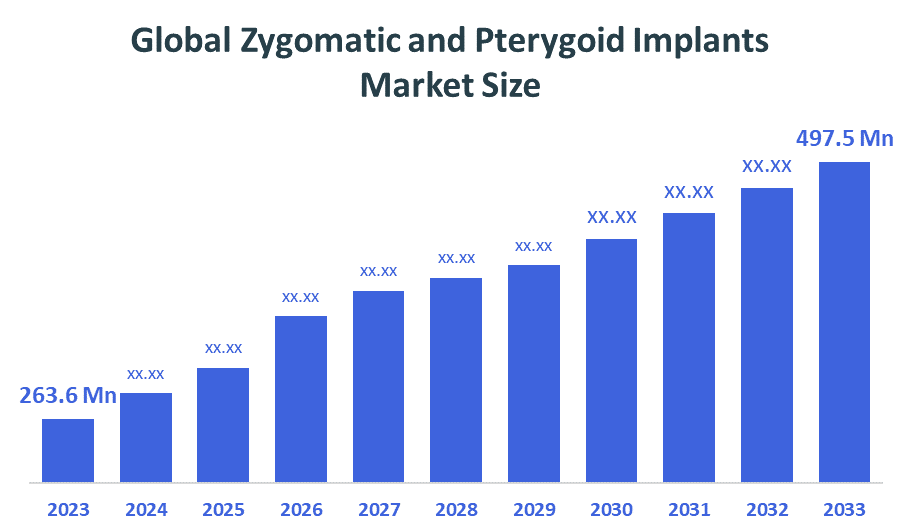

- Market Size (2025): USD 263.6 Million

- Projected Market Size (2035): USD 497.5 Million

- Compound Annual Growth Rate (CAGR): 6.56%

- Largest Regional Market: North America

- Fastest Growing Region: Asia Pacific

- 3rd Largest Region: Europe

- Base Year: 2025

- Historical Period: 2021–2024

- Forecast Period: 2025–2035

According to Decision Advisors, the global zygomatic and pterygoid implants market Size is expected to grow from USD 263.6 million in 2025 to USD 497.5 million by 2035, at a CAGR of 6.56% during the forecast period 2025-2035. The global zygomatic and pterygoid implants market is driven by increasing cases of severe maxillary bone loss where conventional implants fail. Rising demand for graftless, immediate loading full-arch rehabilitation is accelerating adoption. Growth in edentulous patients, advancements in implant design, and increasing expertise among maxillofacial surgeons are further supporting procedural demand and expanding clinical utilization globally.

Market Overview/ Introduction

The global zygomatic and pterygoid implants market refers to specialized dental implant solutions designed for patients with severe maxillary bone loss where conventional implants are not feasible. Zygomatic implants anchor in the zygomatic bone, while pterygoid implants engage the pterygoid plate, enabling stable fixation without the need for bone grafting procedures. These implants are primarily used in full-arch rehabilitation and complex oral reconstruction cases. The scope of the market includes implant manufacturing, surgical planning technologies, guided implant systems, and clinical procedures performed by oral and maxillofacial surgeons. It covers applications in edentulous patients, cases of advanced periodontal disease, trauma-related bone loss, and failed prior implant treatments. Increasing adoption of graftless solutions and immediate loading protocols is expanding the clinical applicability of these implants across developed and emerging markets. Future opportunities in this market are driven by advancements in digital implantology, including CBCT-based planning and navigation-assisted surgery, which enhance procedural accuracy and accessibility. Growing focus on minimally invasive techniques, expansion of specialized surgical training programs, and rising demand for faster full-arch rehabilitation solutions are expected to significantly increase adoption and unlock strong long-term growth potential.

- Medicare continues to exclude routine dental implant procedures from coverage however, private insurers in the United States provide conditional reimbursement for zygomatic implants when used in medically necessary maxillary reconstruction following trauma or cancer-related maxillectomy, as observed in 2026.

- Central Government Health Scheme maintains exclusion of dental implants from standard coverage, positioning zygomatic and pterygoid implant procedures as primarily out-of-pocket treatments, with market growth driven by private dental care providers and increasing dental tourism demand, as of 2025.

Notable Insights: -

- North America holds the largest regional market share of approximately 41% in the global zygomatic and pterygoid implants market.

- Asia-Pacific is the fastest growing regional market share of approximately 21% in the global zygomatic and pterygoid implants market.

- Europe holds the third-largest share of approximately 32% in the global zygomatic and pterygoid implants market.

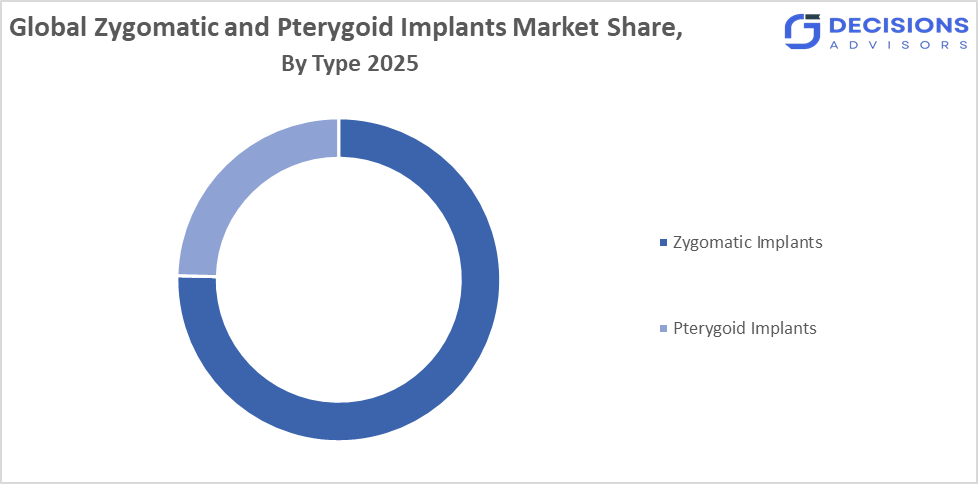

- By type, the zygomatic implants segment dominated the market with approximately 75.4% share in 2025.

- By length of implant, the 31–50 mm segment accounted for approximately 48.19% of the global market share in 2025.

- By application, the maxillary-sinus segment dominated with approximately 58.06% share in 2025.

- By procedure approach, the immediate loading segment held a dominant share of approximately 61.84% in 2025.

- By end user, the hospitals segment accounted for approximately 54.63% of the global market share in 2025.

- The compound annual growth rate of the global Zygomatic and Pterygoid Implants market is 6.56%.

- The market is likely to achieve a valuation of USD 497.5 million by 2035.

What is role of technology in grooming the market?

Technology plays a critical role in grooming the global zygomatic and pterygoid implants market by enabling wider clinical adoption of complex graftless procedures. CBCT-based diagnostics improve identification of patients with severe maxillary atrophy suitable for zygomatic and pterygoid implants. CAD/CAM-guided surgery and dynamic navigation systems reduce surgical complexity, allowing more clinicians to perform precise implant placement. Digital workflow integration supports immediate loading protocols, shortening treatment cycles and increasing patient acceptance. Advanced implant surface technologies enhance osseointegration in dense cortical bone, improving success rates. Additionally, virtual training platforms and simulation-based learning are expanding surgeon expertise globally, directly increasing procedural volumes and accelerating market penetration of these specialized implant solutions.

How is Recent Developments Helping the Market?

Recent developments in the global zygomatic and pterygoid implants market are focused on improving outcomes in patients with severe maxillary bone loss without grafting. Manufacturers are introducing longer zygomatic implants with enhanced surface treatments to ensure stability in dense bone structures. New pterygoid implant designs enable posterior fixation by engaging the pterygoid process, eliminating the need for sinus augmentation. Immediate loading techniques, including quad-zygoma protocols, are reducing treatment duration for full-arch rehabilitation. Additionally, increased adoption of digital planning software and hands-on surgical training programs is improving procedural accuracy and expanding the number of clinicians capable of performing these specialized implant procedures globally.

Market Drivers

The global zygomatic and pterygoid implants market is driven by the rising number of patients with severe maxillary bone resorption where traditional implants cannot achieve primary stability. Increasing demand for graftless full-arch rehabilitation is accelerating the use of zygomatic implants anchored in cortical bone and pterygoid implants engaging posterior maxillary structures. Growth in edentulous cases due to advanced periodontal disease, trauma, and implant failures is further supporting demand. Clinical preference is shifting toward immediate loading protocols that reduce treatment time compared to sinus lift and bone grafting procedures. Advancements in implant geometry and surgical planning technologies are improving success rates, while increasing specialization among oral and maxillofacial surgeons is driving higher procedural adoption globally.

Restrain

The global zygomatic and pterygoid implants market is limited by the need for highly specialized surgical expertise in placing implants within zygomatic bone and pterygoid regions. High procedural costs and limited reimbursement restrict access. Potential complications including sinusitis, nerve injury, and inaccurate implant angulation, along with preference for conventional grafting techniques, constrain wider clinical adoption.

Competitive Analysis:

The report offers the appropriate analysis of the key organizations/companies involved within the global zygomatic and pterygoid implants market, along with a comparative evaluation primarily based on their product of offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes product development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

Top Companies in Global Zygomatic and Pterygoid Implants Market

- Straumann Holding AG

- Nobel Biocare

- Dentsply Sirona

- Zimmer Biomet

- Noris Medical

- S.I.N. Implant System

- Southern Implants

- IDC Implant & Dental Co.

- BioHorizons

- Osstem Implant Co., Ltd.

- Implance

Government Initiatives

|

Country |

Key Government Initiatives |

|

United States |

FDA regulatory standardization for 510(k) pathways (e.g., NobelZygoma TiUltra) and Medicare increased facility fees for Ambulatory Surgical Centers handling complex dental rehabilitations. |

|

Saudi Arabia |

Saudi Arabia government-funded specialty centers hiring European-trained surgeons to establish digital implant suites, enhancing local specialized care capabilities. |

Market Segmentation

The global zygomatic and pterygoid implants market share is classified into type, length of implant, application, procedure approach, and end user

- The zygomatic implants segment dominated the market in 2025, and is projected to grow at a substantial CAGR of approximately 75.4% during the forecast period.

Based on type, the global zygomatic and pterygoid implants market is divided into zygomatic implants and pterygoid implants. Among these, the zygomatic implants segment dominated the market in 2025, holding approximately 75.4% of the global market share, and is projected to grow at a substantial CAGR during the forecast period. It is because of its widespread clinical adoption for full?arch rehabilitation in patients with severe maxillary bone loss. The segment’s strong preference among dental surgeons and hospitals, high procedural success rates, and versatility in complex anatomies drive its dominance.

- The 31–50 mm implant segment dominated the market in 2025, and is projected to grow at a substantial CAGR of approximately 48.19% during the forecast period.

Based on length, the global zygomatic and pterygoid implants market is divided into up to 30 mm, 31–50 mm, and above 50 mm. Among these, the 31–50 mm segment dominated the market in 2025, holding approximately 48.19% of the global market, and is projected to grow at a substantial CAGR during the forecast period. It is because of its optimal balance between implant stability, surgical ease, and suitability for most maxillary anatomies, leading to strong adoption among clinicians and high procedural predictability.

- The maxillary?sinus application segment dominated the market in 2025, and is projected to grow at a substantial CAGR of approximately 58.06% during the forecast period.

Based on application, the global zygomatic and pterygoid implants market is divided into severe atrophy of maxillary bone, maxillary sinuses, and trauma & other indications. Among these, the maxillary?sinus segment dominated the market in 2025, holding approximately 58.06% of the global market, and is projected to grow at a substantial CAGR during the forecast period. It is because of the high prevalence of sinus augmentation procedures, widespread adoption of graft?less rehabilitation approaches, and strong clinical outcomes in posterior maxillary deficiencies.

- The immediate loading procedure segment dominated the market in 2025, and is projected to grow at a substantial CAGR of approximately 61.84% during the forecast period.

Based on procedure approach, the global zygomatic and pterygoid implants market is divided into immediate loading and delayed loading. Among these, the immediate loading segment dominated the market in 2025, holding approximately 61.84% of the global market, and is projected to grow at a substantial CAGR during the forecast period. It is because clinicians prefer same?day provisionalization, faster functional outcomes, reduced chair time, and higher patient satisfaction, leading to broad adoption in advanced dental centers.

- The hospitals segment dominated the market in 2025, and is projected to grow at a substantial CAGR of approximately 54.63% during the forecast period.

Based on end user, the global zygomatic and pterygoid implants market is divided into hospitals, dental clinics, and ambulatory surgical centers. Among these, the hospitals segment dominated the market in 2025, holding approximately 54.63% of the global market, and is projected to grow at a substantial CAGR during the forecast period. It is because hospitals provide comprehensive surgical facilities, specialized teams, high procedural volumes, and are preferred for complex implant procedures requiring advanced support and postoperative care.

What is the Reason of the Region Dominance?

Regional dominance in the global zygomatic and pterygoid implants market is driven by the concentration of advanced implantology centers capable of handling severe maxillary atrophy cases. Higher availability of specialists trained in zygomatic and pterygoid implant placement increases procedural volumes. Integration of digital planning tools such as CBCT and guided surgery improves clinical outcomes, making these procedures more reliable. Additionally, higher case acceptance for graftless full-arch rehabilitation and established referral networks between general dentists and specialists further strengthen dominance in leading regions.

Strategies to Implement for Growth of the Market in Non-Leading Regions

Market growth in non-leading regions can be accelerated by increasing the number of clinicians trained specifically in zygomatic and pterygoid implant techniques. Expanding access to diagnostic and surgical technologies such as CBCT and guided systems will improve treatment feasibility. Introducing simplified surgical protocols and cost-optimized implant systems can enhance adoption in price-sensitive markets. Strengthening referral pathways and building dedicated centers for full-arch rehabilitation will also increase procedural volumes. Additionally, targeted awareness programs focusing on graftless solutions can improve patient acceptance and drive demand.

Regional Segment Analysis of the Zygomatic and Pterygoid Implants Market

- North America (U.S., Canada, Mexico)

- Europe (Germany, France, U.K., Italy, Spain, Rest of Europe)

- Asia-Pacific (China, Japan, India, Rest of APAC)

- South America (Brazil and the Rest of South America)

- The Middle East and Africa (UAE, South Africa, Rest of MEA)

North America is anticipated to hold the largest share of the global zygomatic and pterygoid implants market over the predicted timeframe. This market accounts for approximately 41% of the total market share. The dominance is driven by high procedural volumes of graftless full-arch rehabilitation in patients with severe maxillary atrophy. Strong presence of experienced oral and maxillofacial surgeons and early adoption of CBCT-guided and navigation-assisted implant placement support precision in complex cases. Advanced dental infrastructure and availability of immediate loading protocols further improve treatment efficiency. Higher patient awareness, better affordability, and established implantology practices in the United States and Canada continue to sustain consistent demand for zygomatic and pterygoid implant procedures across the region.

Asia Pacific is expected to grow at the fastest CAGR in the global zygomatic and pterygoid implants market during the forecast period. This region accounts for approximately 21% of the total market share. Growth is driven by increasing prevalence of edentulism and untreated severe maxillary bone loss across countries such as China and India. Expanding dental tourism is attracting patients seeking cost-effective graftless implant procedures. Rapid improvements in dental infrastructure and growing adoption of CBCT imaging and guided implantology are enhancing procedural accuracy. Additionally, the rising number of trained implantologists and increasing awareness of advanced full-arch rehabilitation solutions are accelerating the adoption of zygomatic and pterygoid implants across emerging economies in the region.

Europe is the third largest region in the global zygomatic and pterygoid implants market during the forecast period. This region accounts for approximately 32% of the total market share. Growth is supported by strong clinical expertise in advanced implantology and widespread use of immediate loading protocols for full-arch rehabilitation. Countries such as Germany, France, Italy, and Spain have well-established dental implant practices and high adoption of graftless solutions for patients with severe bone resorption. Increasing aging population and rising incidence of edentulism are further driving demand. Continuous integration of digital dentistry technologies, including CBCT planning and guided surgery, is enhancing treatment precision and supporting steady market expansion across the region.

Future Market Trends in Global Zygomatic and Pterygoid Implants Market: -

- Rising Demand for Premium and Advanced Implant Solutions

The market is witnessing a shift toward premium zygomatic and pterygoid implants featuring advanced surface coatings, enhanced biocompatibility, and superior osseointegration properties. Clinicians and patients increasingly prefer high-quality, long-lasting implant solutions, contributing significantly to revenue growth and improving procedural success rates globally.

- Increasing Adoption of Minimally Invasive and Immediate Loading Techniques

Growing preference for minimally invasive procedures and immediate loading protocols is transforming the market landscape. Zygomatic and pterygoid implants enable graftless solutions for severe bone loss cases, reducing treatment time and improving patient outcomes, thereby driving adoption among dental professionals worldwide.

- Technological Advancements and Digital Dentistry Integration

Integration of digital dentistry, including 3D imaging, CAD/CAM systems, and guided implant surgery, is enhancing precision and treatment efficiency. These technologies enable better planning and placement of complex implants, supporting higher success rates and expanding the applicability of zygomatic and pterygoid implant procedures.

Recent Development

- In August 2025, Nobel Biocare received FDA 510(k) clearance for its NobelZygoma TiUltra implant system, strengthening its zygomatic implant portfolio and expanding advanced treatment options for patients with severe maxillary bone loss.

- In March 2025, Chennai Dental Research Foundation achieved a significant clinical milestone by completing a high volume of zygomatic implant procedures, supporting the adoption of graftless solutions for full-arch rehabilitation in patients with atrophic maxilla.

- In February 2026, advancements in AI, CBCT, and CAD-CAM technologies enhanced precision in zygomatic and pterygoid implant planning and placement, reducing the surgical learning curve and improving treatment outcomes in complex maxillary rehabilitation cases.

Market Segment

This study forecasts revenue at global, regional, and country levels from 2020 to 2035. Decision Advisor has segmented the global zygomatic and pterygoid implants market based on the below-mentioned segments:

Global Zygomatic and Pterygoid Implants Market, By Type

- Zygomatic Implants

- Pterygoid Implants

Global Zygomatic and Pterygoid Implants Market, By Length of Implant

- Up to 30 mm

- 31- 50 mm

- Above 50 mm

Global Zygomatic and Pterygoid Implants Market, By Application

- Severe Atrophy of Maxillary Bone

- Maxillary Sinuses

- Trauma & Other Indications

Global Zygomatic and Pterygoid Implants Market, By Procedure Approach

- Immediate Loading

- Delayed Loading

Global Zygomatic and Pterygoid Implants Market, By End User

- Hospitals

- Dental Clinics

- Ambulatory Surgical Centers

Global Zygomatic and Pterygoid Implants Market, By Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa

Frequently Asked Questions (FAQ)

Q1. How do zygomatic and pterygoid implants compare in long-term survival rates versus conventional implants in complex maxillary cases?

A. Zygomatic and pterygoid implants generally show high long-term survival rates, often comparable to or higher than conventional implants in severe maxillary atrophy cases, as they anchor into dense cortical bone rather than compromised alveolar bone.

Q2. What are the key patient selection criteria for zygomatic versus pterygoid implant procedures?

A. Patient selection depends on anatomical factors such as bone volume, sinus condition, and degree of maxillary resorption. Zygomatic implants are preferred in extreme bone loss cases, while pterygoid implants are used when posterior maxillary support is adequate.

Q3. What are the major training and certification requirements for surgeons performing zygomatic implant procedures?

A. These procedures require advanced expertise in oral and maxillofacial surgery, along with specialized training programs focused on zygomatic implant placement due to the complexity and proximity to critical anatomical structures.

Q4. How does patient recovery time differ between graftless zygomatic implant procedures and traditional bone grafting approaches?

A. Graftless zygomatic implant procedures typically result in faster recovery, as they eliminate the need for bone graft healing, allowing quicker functional restoration compared to traditional multi-stage grafting techniques.

Check Licence

Choose the plan that fits you best: Single User, Multi-User, or Enterprise solutions tailored for your needs.

We Have You Covered

- 24/7 Analyst Support

- Clients Across the Globe

- Tailored Insights

- Technology Tracking

- Competitive Intelligence

- Custom Research

- Syndicated Market Studies

- Market Overview

- Market Segmentation

- Growth Drivers

- Market Opportunities

- Regulatory Insights

- Innovation & Sustainability

Report Details

| Scope | Global |

| Pages | 240 |

| Delivery | PDF & Excel via Email |

| Language | English |

| Release | Apr 2026 |

| Access | Download from this page |