Global Intraductal Papilloma Market

Global Intraductal Papilloma Market Size, Share By Diagnosis (Imaging, Biopsy), By Treatment (Surgical Excision, Minimally Invasive Procedures, Medication), By End User (Hospitals, Specialty Clinics, Diagnostic Centers), and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East & Africa), Analysis and Forecast 2026?2035.

REPORT COVERAGE

Global

Market Snapshot

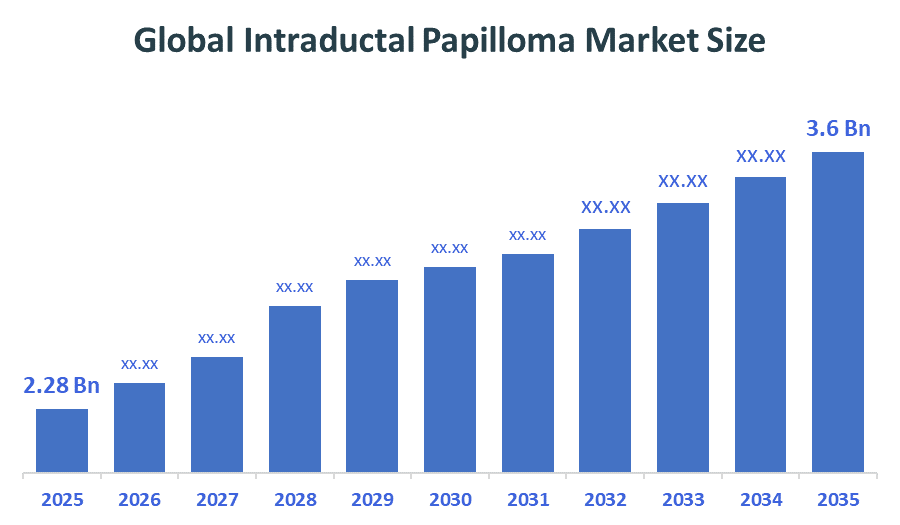

- Global Intraductal Papilloma Market Size (2025): USD 2.28 Billion

- Projected Global Intraductal Papilloma Market Size (2035): USD 3.6 Billion

- Global Intraductal Papilloma Market Compound Annual Growth Rate (CAGR): 4.67%

- Largest Regional Market: North America

- 2nd Largest Region: Europe

- Fastest Growing Region: Asia-Pacific

- Base Year: 2025

- Historical Period: 2021–2024

- Forecast Period: 2026–2035

According to Decision Advisors, the Global Intraductal Papilloma Market Size is expected to grow from USD 2.28 Billion in 2025 to USD 3.6 Billion by 2035, at a CAGR of 4.67% during the forecast period 2025-2035. The Global Intraductal Papilloma Market is projected to grow significantly over the next decade. The growth of the intraductal papilloma market is primarily driven by the rising incidence of breast disorders, increasing adoption of minimally invasive diagnostic and treatment procedures such as vacuum-assisted excision, and ongoing advancements in breast imaging and interventional technologies.

Market Overview/ Introduction

The Global Intraductal Papilloma Market is undergoing a deep human transformation, shifting its focus from simple clinical diagnosis to the emotional and physical well-being of women. At its core, this market involves managing benign, wart-like growths within the breast ducts that, while non-cancerous, often cause significant anxiety. The market’s steady CAGR is driven by a safety-first culture where early detection via 3D mammography and high-resolution ultrasound has become the global standard. This momentum is further sustained by compassionate government initiatives, such as the UK’s NHS screening protocols and India’s Ayushman Bharat scheme, which have democratised access by providing financial coverage for benign lump removals. By replacing traditional open surgery with Vacuum-Assisted Excision (VAE), these companies have reduced patient recovery times by nearly 40%. In tandem, industry leaders like Hologic, GE HealthCare, and Siemens Healthineers are revolutionising the patient experience through company initiatives that prioritize scarless recovery.

- Nearly 1 in 8 women globally are at risk of developing breast-related abnormalities during their lifetime, increasing the need for early diagnostic procedure.

- More than 70% of breast abnormalities are detected through imaging techniques such as mammography and ultrasound, highlighting the importance of diagnostic technologies.

- Minimally invasive procedures, including vacuum-assisted biopsy and excision, have adoption rates exceeding 60% in developed markets.

Notable Insights: -

- North America is anticipated to hold approximately 40% share of the Global Intraductal Papilloma Market over the predicted timeframe.

- Europe is expected to grow at a rapid CAGR in the Global Intraductal Papilloma Market by holding approximately 28% of the share during the forecast period.

- By diagnosis, the biopsy segment dominated the market and holds approximately 55% share in 2025, and is projected to grow at a substantial CAGR during the forecast period.

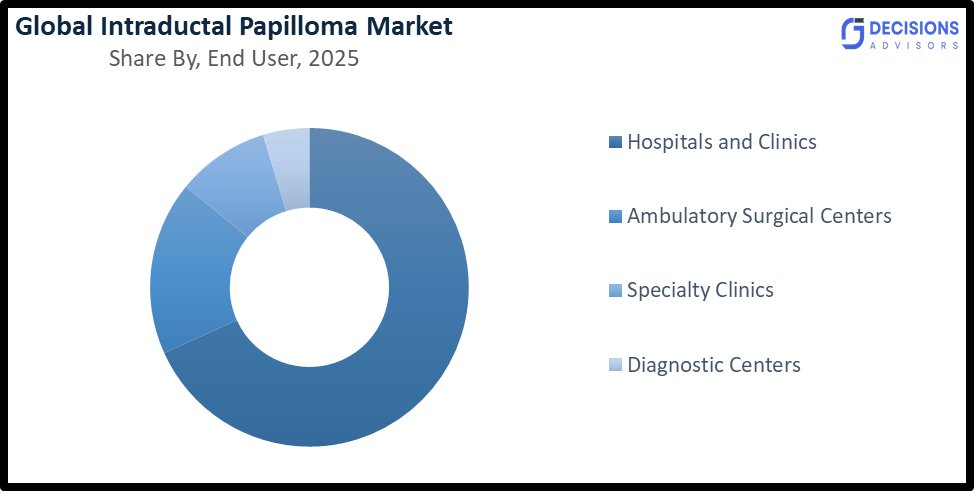

- By end user, the hospitals & clinics segment dominated the market and holds approximately 58% share in 2025 and is projected to grow at a substantial CAGR during the forecast period.

- The compound annual growth rate of the Global Intraductal Papilloma Market is 4.67%.

- The market is likely to achieve a valuation of USD 3.6 Billion by 2035.

What is the role of technology in grooming the market?

Technology is playing a crucial role in improving early detection and treatment outcomes. Advanced imaging techniques such as 3D mammography (tomosynthesis) and contrast-enhanced imaging allow precise identification of intraductal lesions. Minimally invasive biopsy techniques, including vacuum-assisted breast biopsy (VABB), enable accurate diagnosis with minimal tissue damage. AI-powered imaging tools are also being integrated to enhance lesion detection and reduce false positives, improving clinical decision-making.

Market Drivers

The Global Intraductal Papilloma market is being propelled by a fundamental shift toward proactive breast health and the rapid integration of high-precision diagnostic technologies. the growth of the intraductal papilloma market is about a worldwide shift toward putting women’s peace of mind first. Beyond clinical necessity, the market is increasingly humanized by a transition toward minimally invasive techniques like Vacuum-Assisted Excision (VAE). By replacing traditional open surgery with needle-based procedures, clinicians have reduced patient recovery times by 30–40% and virtually eliminated surgical scarring. We’re moving away from simply reacting to health issues and toward a culture of proactive care, powered by screening programs that catch concerns long before they become crises. This safety-first mindset is vital because even a benign-looking lump can carry a small risk of hidden complexities. a quick biopsy isn't just a medical step it’s the definitive all-clear they need to breathe easier. This technological evolution, combined with rising healthcare expenditure in emerging economies and a growing cultural emphasis on psychological reassurance through definitive diagnosis, has created a robust environment for sustained market expansion.

Restrain

The Intraductal Papilloma Market faces several restraints, including the high cost of advanced diagnostic procedures such as MRI and biopsy systems, which limits adoption in developing regions. Limited access to specialized healthcare facilities and a shortage of skilled professionals further restrict early diagnosis and treatment. Additionally, the risk of overdiagnosis and unnecessary surgical interventions may discourage patients, while lack of awareness about benign breast conditions in low-resource settings continues to hinder overall market growth.

Competitive Analysis:

The report offers the appropriate analysis of the key organizations/companies involved within the Global Intraductal Papilloma Market, along with a comparative evaluation primarily based on their product of offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes product development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

Top Companies in the Global Intraductal Papilloma Market

- Teva Pharmaceutical Industries Ltd

- Bayer AG

- Pfizer Inc.

- Novartis International AG

- GlaxoSmithKline plc

- Medtronic

- Hologic, Inc.

- Abbott Laboratories

- Cook Medical

- Boston Scientific Corporation

Government Initiatives

|

Country |

Key Government Initiatives |

|

India |

The Ayushman Bharat card explicitly covers Benign Breast Lump Excision at hundreds of empanelled hospitals across the country, including major private and public facilities in Delhi, Bangalore, and Rajasthan. |

|

UK |

The NHS audits screening units to ensure that at least 75% of appropriate B3 lesions are managed with these gentler, non-surgical methods. |

|

US |

National Breast and Cervical Cancer Early Detection Program (NBCCEDP): This CDC program covers clinical breast exams, diagnostic mammograms, and the tissue biopsies necessary to confirm that a papilloma is non-cancerous |

Study on the Supply, Demand, Distribution, and Market Environment of the Global Intraductal Papilloma Market

The demand for diagnosing intraductal papilloma is rising, mainly because more people are taking part in breast cancer screenings. As awareness of early detection grows, regular mammograms and ultrasounds are catching these issues earlier, pushing more patients to seek specialized diagnostic tools. On the supply side, tech is keeping up. High-res ultrasounds, MRIs, and digital mammography alongside better, less invasive biopsy methods have made diagnosis faster and more accurate. This means doctors can pinpoint problems with much higher precision than before. Most of these services are found in hospitals, diagnostic centers, and clinics. To reach more people, equipment makers are also partnering directly with healthcare providers, making sure this tech is available in both cities and smaller towns. Combined with global investments in healthcare tech, it’s becoming much easier for facilities to adopt these advanced tools and for patients to access the care they need.

Price Analysis and Consumer Behaviour Analysis

It used to be that high-tech scans and biopsies for something like an intraductal papilloma felt like a huge, daunting expense. But that’s changing. People are starting to see these advanced diagnostics like MRIs not just as a bill, but as an investment. There’s a growing catch it early mind-set, patients would much rather pay a bit more now to avoid a major health crisis (and a much bigger medical bill) down the road. We’re also seeing a huge shift in what people value. Today’s patient is looking for the "painless" path. If a procedure means less time in a hospital bed, a smaller scar, and getting back to work or family faster, they’re often willing to pay a premium for it. It’s about choosing comfort and convenience over the old-school, more invasive ways of doing things. A big part of this comes down to being informed.

Market Segmentation

The Global Intraductal Papilloma Market share is classified into diagnosis, treatment and end user

- The biopsy segment dominated the market and holds approximately 55% share in 2025, and is projected to grow at a substantial CAGR during the forecast period.

Based on the diagnosis, the global intraductal papilloma market is divided into imaging (mammography, ultrasound, MRI) and biopsy. Among these, the biopsy segment dominated the market and holds approximately 55% share in 2025 and is projected to grow at a substantial CAGR during the forecast period. This dominance is attributed to its high accuracy in confirming intraductal papilloma cases and differentiating benign from malignant lesions. Biopsy procedures, including core needle biopsy and vacuum-assisted biopsy, are widely used due to their reliability and precision. Imaging techniques are also essential for initial detection and screening; however, they hold a comparatively smaller share as they require confirmatory biopsy for definitive diagnosis.

- The surgical excision segment accounted for the largest share of approximately 52% in 2025 and is anticipated to grow at a significant CAGR during the forecast period

Based on the treatment, the global intraductal papilloma market is divided into surgical excision, minimally invasive procedures, and medication. Among these, the surgical excision segment accounted for the largest share of approximately 52% in 2025 and is anticipated to grow at a significant CAGR during the forecast period. This is primarily due to its effectiveness in completely removing papillomas and preventing recurrence or potential complications. Minimally invasive procedures, such as vacuum-assisted excision, are gaining traction due to reduced recovery time and improved patient comfort. Medication plays a limited role and is generally used for symptom management rather than definitive treatment.

- The hospitals & clinics segment dominated the market and holds approximately 58% share in 2025 and is projected to grow at a substantial CAGR during the forecast period

Based on end user, the global intraductal papilloma market is divided into hospitals & clinics, ambulatory surgical centers, specialty clinics, and diagnostic centers. Among those, the hospitals & clinics segment dominated the market and holds approximately 58% share in 2025 and is projected to grow at a substantial CAGR during the forecast period, owing to the availability of advanced diagnostic imaging systems, skilled healthcare professionals, and higher patient inflow for breast-related conditions. Ambulatory surgical centers are witnessing rapid growth due to the increasing preference for outpatient minimally invasive procedures, offering cost-effectiveness and shorter hospital stays. Specialty clinics and diagnostic centers are also expanding steadily, particularly in urban and developed regions where early screening programs are widely adopted.

Strategies to Implement for Growth of the Market in Non-Leading Regions

To expand the intraductal papilloma market in non-leading regions, companies and healthcare stakeholders should focus on improving accessibility, affordability, and awareness. One of the key strategies is to increase awareness and screening programs related to breast health. Many developing regions face low diagnosis rates due to limited awareness, so government-led campaigns and partnerships with healthcare organizations can significantly boost early detection and patient inflow. Another important approach is to expand access to affordable diagnostic technologies. Introducing cost-effective imaging systems and minimally invasive biopsy solutions can help healthcare providers in resource-limited settings adopt advanced diagnostic practices. Local manufacturing and distribution partnerships can further reduce costs and improve availability.

Regional Segment Analysis of the Global Intraductal Papilloma Market

- North America (U.S., Canada, Mexico)

- Europe (Germany, France, U.K., Italy, Spain, Rest of Europe)

- Asia-Pacific (China, Japan, India, Rest of APAC)

- South America (Brazil and the Rest of South America)

- The Middle East and Africa (UAE, South Africa, Rest of MEA)

North America is anticipated to hold approximately 38% share of the Global Intraductal Papilloma Market over the predicted timeframe.

North America is anticipated to hold approximately 38% share of the global intraductal papilloma market over the predicted timeframe. It maintains dominant market leadership due to well-established healthcare infrastructure, high breast cancer screening rates, and strong adoption of advanced diagnostic imaging technologies. The United States is the key driver, supported by high healthcare expenditure and the increasing prevalence of breast-related disorders. Additionally, the growing adoption of minimally invasive diagnostic procedures such as vacuum-assisted biopsy and digital mammography across hospitals and diagnostic centers further strengthens regional demand. The presence of major healthcare companies and continuous technological advancements also contribute to market growth.

Europe is expected to grow at a rapid CAGR in the Global Intraductal Papilloma Market by holding approximately 27% of the share during the forecast period.

Europe is expected to grow at a rapid CAGR in the global intraductal papilloma market by holding approximately 27% of the share during the forecast period. Europe’s market is supported by advanced healthcare systems, favorable reimbursement policies, and widespread implementation of organized breast screening programs. Key countries such as Germany, France, and the United Kingdom emphasize early diagnosis and treatment of breast abnormalities, contributing to increased screening volumes. Additionally, rising investments in healthcare infrastructure and growing awareness about early breast disease detection are driving steady market growth across the region.

Asia Pacific is the fastest-growing region in the Intraductal Papilloma Market during the period, holding approximately 24% share.

Asia Pacific is the fastest-growing region in the intraductal papilloma market during the period, holding approximately 24% share. This growth is driven by rising healthcare investments, increasing awareness about breast health, and improving access to diagnostic services. Countries such as China, India, and Japan are witnessing significant growth due to large patient populations and expanding healthcare infrastructure. Government initiatives promoting early breast cancer screening, increasing number of diagnostic centers, and growing medical tourism are further contributing to the rising demand and overall market expansion in the region.

Future Market Trends in the Global Intraductal Papilloma Market: -

1. Increasing Adoption of Minimally Invasive Diagnostic and Treatment Procedures

The market is witnessing a strong shift toward minimally invasive techniques such as vacuum-assisted biopsy (VABB) and image-guided excision procedures. These approaches significantly reduce patient discomfort, recovery time, and hospital stays by nearly 30–40%, making them highly preferred over traditional surgical methods. This trend is expected to accelerate as healthcare providers focus on improving patient outcomes and cost efficiency.

2. Integration of Artificial Intelligence (AI) in Breast Imaging

AI-powered imaging technologies are transforming the diagnosis of intraductal papilloma by enhancing detection accuracy and reducing false positives. Advanced AI algorithms integrated with digital mammography and ultrasound systems can improve diagnostic efficiency by over 20–25%. This trend is expected to streamline clinical workflows and support early detection, thereby driving market growth.

3. Expansion of Breast Cancer Screening Programs Globally

Governments and healthcare organizations are increasingly investing in large-scale breast screening initiatives to promote early detection of breast abnormalities, including intraductal papilloma. Rising awareness campaigns and improved access to screening facilities, especially in emerging economies, are expected to significantly boost diagnosis rates and overall market demand in the coming years.

Recent Development

- In January 2026, A leading cancer center in New Delhi launched MRI-guided vacuum-assisted breast biopsy (VABB) technology, enabling detection of lesions that may be missed in conventional mammography, especially in dense breast tissue cases.

- In July 2025, An AI-based breast imaging technology developed by Washington University School of Medicine received FDA Breakthrough Device designation. This innovation enhances risk prediction and improves early detection of breast abnormalities, including intraductal papilloma.

- In February 2024, Mammotome launched the AutoCore Core Needle Biopsy System, designed to streamline breast biopsy procedures with single-insertion capability. This innovation improves efficiency, reduces procedure time, and enhances patient comfort during diagnosis of conditions such as intraductal papilloma.

How is Recent Developments Helping the Market?

Recent developments are significantly supporting the growth of the intraductal papilloma market by improving both diagnosis and treatment outcomes. Advancements in biopsy techniques, such as vacuum-assisted and core needle biopsy, have increased diagnostic accuracy and enabled early detection of lesions. At the same time, the shift toward minimally invasive procedures has reduced recovery time, complications, and hospital stays, making treatment more efficient and patient-friendly. Additionally, the integration of AI in breast imaging is enhancing detection precision and reducing false positives, while growing awareness and screening programs are increasing patient diagnosis rates. Together, these developments are making intraductal papilloma management more effective, accessible, and cost-efficient, thereby driving overall market expansion.

Market Segment

This study forecasts revenue at global, regional, and country levels from 2020 to 2035. Decision Advisors has segmented the global intraductal papilloma market based on the below-mentioned segments:

Global Intraductal Papilloma Market, By Diagnosis

- Imaging

- Biopsy

Global Intraductal Papilloma Market, By Treatment

- Surgical Excision

- Minimally Invasive Procedures

- Medication

Global Intraductal Papilloma Market, By End User

- Hospitals

- Specialty Clinics

- Diagnostic Centers

Global Intraductal Papilloma Market, By Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa

Frequently Asked Questions (FAQ)

Q. What age group is most commonly affected by intraductal papilloma?

A. Intraductal papilloma is most commonly diagnosed in women between the ages of 35 and 55, although it can occur at any age.

Q. Are their differences between single and multiple intraductal papillomas?

A. Yes, single (solitary) papillomas usually occur near the nipple and have a lower cancer risk, whereas multiple papillomas often develop deeper in the breast and may carry a slightly higher risk.

Q. How does insurance coverage impact treatment adoption?

A. Favorable reimbursement policies in developed regions encourage early diagnosis and treatment, while limited insurance coverage in developing regions can delay medical intervention.

Q. What role do lifestyle factors play in the occurrence of intraductal papilloma?

A. While the exact cause is unclear, hormonal changes, age, and certain lifestyle factors may influence the development of benign breast conditions like intraductal papilloma.

Q. Can an intraductal papilloma recur after treatment?

A. Recurrence is uncommon but possible, especially if the lesion is not completely removed, making follow-up monitoring important.

Check Licence

Choose the plan that fits you best: Single User, Multi-User, or Enterprise solutions tailored for your needs.

We Have You Covered

- 24/7 Analyst Support

- Clients Across the Globe

- Tailored Insights

- Technology Tracking

- Competitive Intelligence

- Custom Research

- Syndicated Market Studies

- Market Overview

- Market Segmentation

- Growth Drivers

- Market Opportunities

- Regulatory Insights

- Innovation & Sustainability

Report Details

| Scope | Global |

| Pages | 210 |

| Delivery | PDF & Excel via Email |

| Language | English |

| Release | Apr 2026 |

| Access | Download from this page |