Global Silicon Infrared (IR) Camera Market

Global Silicon Infrared (IR) Camera Market Size, Share, By Wavelength Type (Near Infrared (NIR), Short-Wave Infrared (SWIR), and Extended Silicon Range) By Technology (CMOS-based IR Cameras and CCD-based IR Cameras) By Application (Industrial Inspection, Security and Surveillance, Automotive Systems, Consumer Electronics, and Healthcare Imaging) and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2026 ? 2035

REPORT COVERAGE

Global

Market Snapshot

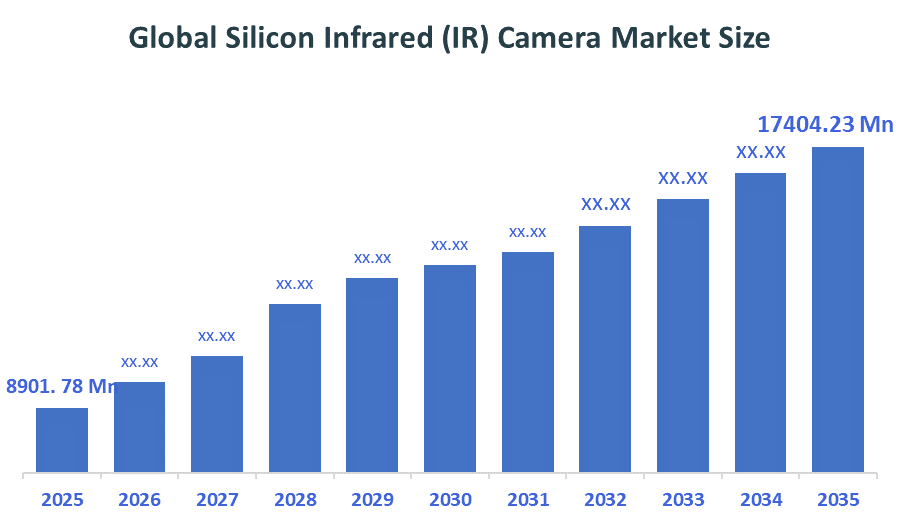

- Global Silicon Infrared (IR) Camera Market Size (2025): USD 8901.78 Million

- Global Silicon Infrared (IR) Camera Projected Market Size (2035): USD 17404.23 Million

- Global Silicon Infrared (IR) Camera Compound Annual Growth Rate (CAGR): 6.93%

- Regional Market: North America

- Fastest Growing Region: Asia-Pacific

- 3rd Largest Region: Europe

- Base Year: 2025

- Historical Period:2020–2024

- Forecast Period: 2026–2035

According to Decision Advisors, the Global Silicon Infrared (IR) Camera Market size was expected to grow from USD 8901.78 million in 2025 to USD 17404.23 million by 2035, with a CAGR of 6.93% during the forecast period from 2026 to 2035. It is expected that there will be a stable growth trend in this market owing to the growing incorporation of high-resolution thermal imaging and automatic sensing devices into the security and industry sectors across the world. The growth of this market is largely attributed to the growing demand for advanced surveillance systems in the defense industry, as well as the adoption of infrared technology for predictive maintenance applications in industries. There have been new innovations in silicon photonics technology compatible with CMOS, along with the shrinking of uncooled modules used in these imaging systems.

Market Overview / Introduction

Silicon infrared cameras describe a state-of-the-art imaging solution that incorporates silicon-based sensor systems, including CMOS-compatible micro bolometers or photodiodes, to accurately sense and produce accurate signals of infrared radiation for thermal imaging solutions. With the initial origin being bulky equipment with cryogenic applications, the system has evolved into extremely advanced and sophisticated non-cooled devices featuring high pixel density, fast-frame rate, and the ability to generate thermal information from very small-sized packages. The growing importance of efficiency in terms of resolution-based thermal detection and optical imaging, particularly within security environments and self-driving vehicles, has been one of the significant drivers in the Global Silicon Infrared (IR) Camera Market. Silicon infrared cameras play an extremely vital role when it comes to ensuring efficiency in high-performance diagnostic solutions, especially with regard to the real-time analysis of heat signatures in situations where industry and defence engineers use the technology in place of more expensive alternatives such as InGaAs sensors or cooled thermal imaging systems.

- Industrial Inspection constitutes around 20% of the total market share due to the rising importance of quality control, maintenance, and defect detection in semiconductors and manufacturing processes.

- The automotive industry is experiencing high growth at a compound annual growth rate of more than 9%, driven by the increasing use of driver assistance systems, night vision, and pedestrian detection in vehicles.

- North America represents about 38% of total revenue owing to the high adoption of imaging technology in defense applications, automated manufacturing, and autonomous cars, along with the presence of major semiconductor and imaging solutions vendors.

Notable Insights: -

- The near-infrared sector occupies the largest market share of around 45%, owing to the extensive application in consumer gadgets, face recognition technology, and silicon sensor-based infrared cameras, which are less expensive than those using other infrared waves.

- Owing to improvements in picture quality, real-time monitoring capabilities, and enhanced system efficiency, more than 68% of firms began to prefer silicon infrared cameras for implementation in their systems.

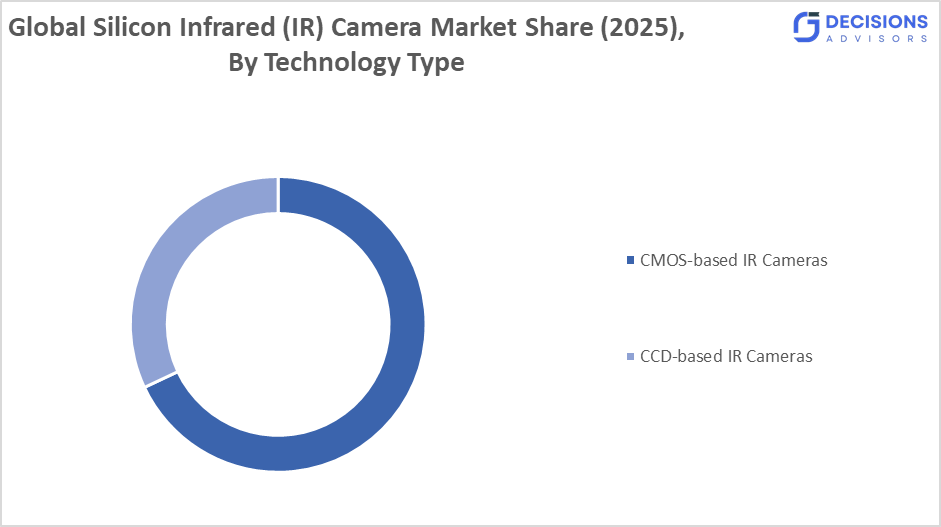

- CMOS infrared cameras have approximately above 65% of market share since they are characterised by reduced power consumption, smaller physical size, and affordable prices that render them feasible for large-scale commercial manufacturing.

- The government agencies have been setting strict standards in terms of safety and inspection of infrastructure in industries such as energy, manufacturing, and construction, leading to increased demand for infrared cameras in these areas.

What is the role of technology in shaping the market?

Technology is revolutionising the field of silicon IR cameras through improvements in thermal sensitivity, processing speed, and imaging accuracy. Contemporary infrared devices are transitioning from heavy, temperature-cooled apparatuses used in laboratories to highly integrated, non-temperature-cooled sensors that are compatible with CMOS, fast digital signal processors, and multispectral data integration technology. This innovation enables defence experts and industrial researchers to detect threats with greater precision, avoid maintenance problems associated with extreme temperatures, and ensure accurate visualisation under varying weather conditions ranging from heavy smog to total darkness.

How are Recent Developments Helping the Market?

Innovations like the deployment of thermal analytics powered by artificial intelligence, the use of three-dimensional infrared imaging technology, and real-time edge computing are playing a crucial role in driving market growth. Suppliers are offering miniature and lightweight sensor components that can be used in small-scale UAVs and wearables with enhanced accuracy in thermal images. With cloud computing-based diagnostic tools, immediate interpretation and distribution of temperature fingerprints have become possible, making it easier to make critical decisions related to industrial safety and medical examinations. Furthermore, innovations in semiconductor manufacturing processes, such as silicon photonics, have facilitated seamless transmission of signals between infrared sensors and centralised control units.

Market Drivers

The worldwide silicon IR camera market is seeing a rise owing to the rising investments by government defence departments in the development of advanced border surveillance and night vision technologies to increase operational accuracy and situational awareness during tactical operations. The use of silicon cameras has been increasing steadily in the market owing to the benefits of incorporating multiple functionalities, such as live tracking of heat signature, high-resolution thermal imaging, and mount ability on a range of platforms, such as robotic armatures and security masts, in a single unit. On the other hand, the recent advancements in autonomous car technology are propelling the market because of the demand for accurate pedestrian detection sensors that could make the cars operate more safely and perform better in harsh environments like fog or sun glare. Increasing concern about the energy usage efficiency of facilities is leading facility managers to invest in infrared sensors that could help in finding heat leakages and electrical issues.

Restraints

However, there are some constraints that hinder the expansion of the worldwide silicon IR camera market due to the high cost incurred in manufacturing high-grade silicon wafers and using lenses that are made up of other special materials, such as germanium. Other sources of costs include system integration expenses, periodic calibration services, and the use of enhanced imaging algorithms. Moreover, the availability of semiconductor components on the global market and the necessity to employ experts to analyse the results obtained from these cameras are some of the reasons why they cannot be widely adopted in developing countries.

Competitive Analysis:

The report offers the appropriate analysis of the key organisations/companies involved within the silicon infrared (IR) camera market, along with a comparative evaluation primarily based on their product offerings, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborate analysis focusing on the current news and developments of the companies, which includes product development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

Top 10 Companies in the Silicon Infrared (IR) Camera Market

- Teledyne FLIR LLC (Teledyne Technologies)

- Raytheon Technologies Corporation

- Leonardo DRS

- Axis Communications AB

- L3Harris Technologies, Inc.

- Hamamatsu Photonics K.K.

- Seek Thermal, Inc.

- Fluke Corporation

- Xenics NV

- OPGAL Optronic Industries Ltd.

Government Initiatives

|

Country |

Key Government Initiatives |

|

US |

In the United States, infrared sensor development is strongly supported by defence and research programs, with federal backing through the CHIPS and Science Act providing approximately 52 billion USD for semiconductor manufacturing and innovation. At the same time, the U.S. Department of Energy promotes infrared-based energy audits, which can improve building efficiency by up to 30%, boosting the adoption of silicon infrared camera technologies across commercial and residential sectors. |

|

European Union |

The European Union supports infrared and photonics innovation through Horizon Europe, investing millions of euros in projects focused on compact sensors and spectrometry solutions. In parallel, the European Chips Act aims to double the region’s global semiconductor share by 2030, strengthening the development of silicon-based infrared sensor technologies. |

|

India |

In India, the Ministry of Electronics and Information Technology (MeitY) has launched the Programme for Semiconductors and Display Manufacturing Ecosystem, offering fiscal support of 50% of capital expenditure for setting up Silicon Photonics and Sensor Fabs. |

Study on the Supply, Demand, Distribution, and Market Environment

The market for silicon IR cameras stems from the equilibrium between the high sensitivity to thermal radiation and the ever-growing need for automation across industries. From the supply perspective, companies are focusing on producing sensors and microbolometers with high pixel densities and capable of functioning without heavy cooling mechanisms required by cooled CMOS detectors. The demand comes from global trends of developing AI-driven surveillance, implementing thermal imaging technologies into ADAS systems, and creating contactless diagnostic tools in industry and healthcare. In terms of distribution, this technology depends on lucrative defense contracts and specialised value-added dealers in the IT industry, making sure the components get into the hands of defense contractors, automotive manufacturers, and smart factory designers.

Price Analysis and Consumer Behaviour Analysis

Price levels for silicon IR cameras depend on the range and thermal resolution involved. The cost is higher for top-of-the-line devices that incorporate SWIR technology along with sophisticated processing algorithms, whereas conventional LWIR sensors make for an affordable option when it comes to industrial surveillance and portable inspection. Consumer preferences reveal a marked tendency towards longevity; companies look for durable equipment that consumes minimal amounts of energy and provides immediate start-up performance. In this regard, a modular approach to sensors is gaining traction with the advent of new predictive and autonomous criteria.

Market Segmentation

The Global Silicon Infrared (IR) Camera Market share is classified into wavelength type, technology, and application.

By Wavelength Type, the Short-Wave Infrared (SWIR) segment holds the largest share, contributing approximately 42% of the market in 2025.

The silicon infrared camera market is segmented into near infrared (NIR), short-wave infrared (SWIR), and extended silicon range. By wavelength type, the short-wave infrared (SWIR) segment holds the largest share, contributing approximately 42% of the market in 2025. This particular wavelength range has dominated the market during the year 2024, and it is expected that this segment will continue to register steady growth owing to increasing demand for low-light imaging and moisture detection information in the industries and defense sectors.

By Technology, CMOS-based IR Cameras dominate the global silicon infrared camera market, accounting for approximately 68% of the total market share in 2025.

The silicon infrared camera market is segmented into CMOS-based IR cameras and CCD-based IR cameras. By technology, CMOS-based IR cameras dominate the global silicon infrared camera market, accounting for approximately 68% of the total market share in 2025. CMOS was the dominant segment in the market in 2024, and it is anticipated that it will maintain steady growth with a CAGR of about 8.5% over the forecast period. The reasons for this are that they are used extensively in consumer electronics products and portable security gadgets as they have low power consumption, fast frame rate, and are suitable for many miniaturised sensing techniques.

By Application, Security and Surveillance accounts for the largest share, representing over 38% of the global market in 2025.

The silicon infrared camera market is categorised into Industrial Inspection, security and surveillance, automotive systems, consumer electronics, and healthcare imaging. By application, security and surveillance accounts for the largest share, representing approximately 38% of the global market in 2025. The security and surveillance sector dominates the market owing to the necessity of precise measurements related to threat assessments, perimeter safety ratings, and effects of continuous monitoring. These measurements can only be performed at high frequency.

Strategies to Implement for Growth of the Market in Non-Leading Regions

The growth rate in the market for silicon IR cameras in countries other than the leading countries can be further augmented through the implementation of certain strategies within such countries. Firstly, the best strategy to promote adoption in developing countries is to provide inexpensive and uncooled silicon sensor systems to security firms and industrial companies in these countries. Secondly, the development of digitalisation programs and smart surveillance systems in cities will greatly contribute to the demand for infrared imaging in such countries. Thirdly, more funds are needed for training engineers and technicians in optoelectronics and thermographic data analysis. Better distribution channels could be developed through partnerships with electronics distributors in such countries and through e-commerce websites for sensor components.

Regional Segment Analysis of the Silicon Infrared (IR) Camera Market

- North America (U.S., Canada, Mexico)

- Europe (Germany, France, U.K., Italy, Spain, Rest of Europe)

- Asia-Pacific (China, Japan, India, South Korea, Rest of APAC)

- Latin America (Brazil and the Rest of Latin America)

- The Middle East and Africa (UAE, South Africa, Rest of MEA)

North America is expected to hold the largest share of the silicon infrared (IR) camera market during the forecast period. This region makes up 38% of the global revenue share, supported by the very sophisticated infrastructure of defence, along with high usage of thermal imaging technology in aerospace and self-driving vehicle testing applications. The US generates most of the revenue share in this region because of heavy investments made in advanced reconnaissance missions as well as semiconductor development within the country. The consistent improvements in the performance of night vision systems, along with the early adoption of silicon photonics in consumer electronic gadgets, drive the market in this region.

Asia-Pacific is projected to be the fastest-growing region over the forecast period. The area will experience an average annual growth rate of around 7.5%, while it holds a significant market share in the global market. This is due to the fast evolution in the automation industry in the manufacture of products and the expansion of electronic product manufacturing in China, South Korea, and India. The reasons also include investment in regional security, government initiatives on semiconductor production, and a huge leap in the use of IR sensors in automotive safety applications and portable devices.

Europe is anticipated to hold the third-largest share, contributing approximately 24% of the global market share. The region is in a strong position owing to established research clusters in photonics and consistent investment in sustainable industrial monitoring and medical diagnostics. Countries like Germany, France, and the UK are important players due to their high level of expertise in precision engineering and the implementation of strict safety standards in the manufacturing sector. Moreover, the existence of major optoelectronic equipment producers and the modernisation of healthcare imaging facilities are contributing to the steady uptake of silicon-based infrared cameras.

Recent Developments

- In March 2026, Teledyne FLIR introduced an upgraded compact infrared camera module with enhanced sensitivity and image processing capabilities, improving detection accuracy by approximately 25% in low-light and thermal contrast environments, supporting advanced surveillance and industrial inspection applications.

- In February 2026, the U.S. Department of Defence increased funding for advanced infrared imaging systems under next-generation surveillance programs, leading to an estimated 18% rise in procurement of high-performance silicon-based IR sensors for military and border monitoring applications.

- In November 2025, the European Commission expanded funding under semiconductor initiatives to support infrared and photonics research, contributing to a projected 2× increase in regional chip production capacity by 2030, benefiting silicon-based IR sensor manufacturing.

- In September 2025, Teledyne FLIR launched an advanced thermal imaging platform with improved sensitivity, enhancing detection accuracy by approximately 25% for industrial inspection and security monitoring applications.

Market Segmentation

This study forecasts revenue at global, regional, and country levels from 2020 to 2035. The silicon infrared (IR) camera market is segmented based on the following categories:

Global Silicon Infrared (IR) Camera Market, By Wavelength Type

- Near Infrared (NIR)

- Short-Wave Infrared (SWIR)

- Extended Silicon Range

Global Silicon Infrared (IR) Camera Market, By Technology

- CMOS-based IR Cameras

- CCD-based IR Cameras

Global Silicon Infrared (IR) Camera Market, By Application

- Industrial Inspection

- Security and Surveillance

- Automotive Systems

- Consumer Electronics

- Healthcare Imaging

Global Silicon Infrared (IR) Camera Market, By Regional Analysis

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- United Arab Emirates

- Saudi Arabia

- Qatar

- South Africa

- Rest of Middle East & Africa

Frequently Asked Questions (FAQ)

What is a silicon infrared (IR) camera, and why is it important?

A silicon infrared (IR) camera is an advanced imaging device that utilizes silicon-based sensors to detect radiation in the infrared spectrum and convert it into visual electronic signals. It plays a crucial role in capturing thermal data, enabling night vision, and performing non-destructive testing, which helps industries maintain safety standards, improve security monitoring, and ensure precision in autonomous navigation.

What factors are driving the growth of the silicon infrared (IR) camera market?

The market is growing due to increasing investments in defence and border security, rising demand for advanced driver-assistance systems (ADAS) in the automotive sector, and the adoption of uncooled thermal imaging in consumer electronics. The expansion of smart city surveillance and the need for real-time industrial temperature monitoring are also contributing significantly to market growth.

Which technology type dominates the silicon infrared (IR) camera market?

CMOS-based IR cameras hold the largest market share. This is because they offer superior integration capabilities, lower power consumption, and faster readout speeds, making them highly suitable for high-volume applications in smartphones, security cameras, and portable diagnostic tools.

Which wavelength types are widely used in this market?

Wavelengths such as Short-Wave Infrared (SWIR) and Near Infrared (NIR) are widely used due to their ability to provide high-resolution imaging through atmospheric haze and low-light conditions. These segments support both tactical military reconnaissance and complex industrial sorting applications, improving overall operational efficiency.

Check Licence

Choose the plan that fits you best: Single User, Multi-User, or Enterprise solutions tailored for your needs.

We Have You Covered

- 24/7 Analyst Support

- Clients Across the Globe

- Tailored Insights

- Technology Tracking

- Competitive Intelligence

- Custom Research

- Syndicated Market Studies

- Market Overview

- Market Segmentation

- Growth Drivers

- Market Opportunities

- Regulatory Insights

- Innovation & Sustainability

Report Details

| Scope | Global |

| Pages | 210 |

| Delivery | PDF & Excel via Email |

| Language | English |

| Release | Apr 2026 |

| Access | Download from this page |